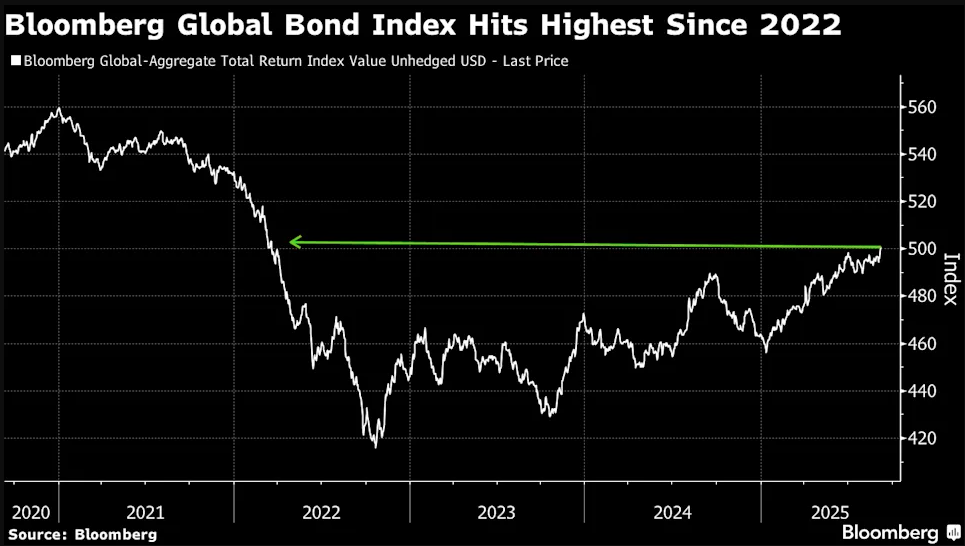

① With the comprehensive recovery of the fixed income market, the Bloomberg Global Aggregate Bond Index, which tracks the returns of sovereign and corporate bonds in developed and emerging markets, has surged over 20% from its low in 2022; ② This not only marks the highest level since March 2022 but also officially announces a return to the technical bull market territory.

Financial Associated Press, September 10 (Editor: Xiaoxiang) - After three years of global inflation wreaking havoc on the fixed income market, the global bond market has finally returned to bull market territory...

Market data shows that as the fixed income market fully recovers, the Bloomberg Global Aggregate Bond Index, which tracks the returns of sovereign and corporate bonds in developed and emerging markets, has surged over 20% from its low in 2022. This not only marks the highest level since March 2022 but also officially announces a return to the technical bull market territory.

The latest round of increases is attributed to cooling U.S. labor data, which has strengthened market expectations that the Federal Reserve will soon intensify its policy easing.

The latest round of increases is attributed to cooling U.S. labor data, which has strengthened market expectations that the Federal Reserve will soon intensify its policy easing.

Traders currently expect the Federal Reserve to cut interest rates by 25 basis points next week, with some bets even pointing to a 50 basis points cut. As major central banks significantly lower borrowing costs in response to signs of falling inflation and increasing pressures in the labor market, the global bond market has been strengthening recently.

Jim Reid, a strategist at Deutsche Bank, noted in a report sent to clients, "The dominant theme in the market over the past 24 hours has been the continued rise of global bonds. This has alleviated the pressure brought about by the latest political crisis in France."

The primary market is also showing strong demand, with issuers, including those from the UK, having recently seen oversubscription. On Tuesday, the European Union's issuance of 30-year bonds received over €98 billion (approximately $115 billion) in subscriptions, while the five-year bond subscriptions also exceeded €70 billion.

Government bonds continue to "lag behind."

However, due to the rising fiscal risks, long-term government bonds in some regions are still under pressure. In fact, although the global bond market has entered a new bull market according to standard technical definitions, this does not signify a recovery of confidence in sovereign debt—if anything, it may be quite the opposite.

The Bloomberg Global Aggregate Bond Index primarily consists of sovereign bonds, corporate bonds, and securitized debt. In this round of rebound, global corporate bonds have significantly outperformed other types of bonds.

Anxiety regarding sovereign debt is particularly concentrated in markets such as France—French Prime Minister Élisabeth Borne submitted her resignation to President Emmanuel Macron on the 9th, following a confidence vote in the National Assembly where her government received 194 votes in favor and 364 votes against, failing to pass. This marks the fourth Prime Minister to resign in France within two years.

In the UK, investors are awaiting Chancellor of the Exchequer Jeremy Hunt's announcement in November on how to balance growth plans with spending constraints. Last week, the yield on UK 30-year government bonds reached a high of 5.75%, the highest since 1998, before retreating to around 5.47%.

In Japan, Prime Minister Shigeru Ishiba's decision to resign last weekend has heightened uncertainty, with his successor widely perceived as potentially lacking commitment to fiscal discipline. The yield on Japan's 30-year government bonds has remained near historical highs this week.

In contrast, regarding corporate bonds, the Bloomberg Index indicates that the yield on global investment-grade bonds has declined for four consecutive days, dropping to 4.26% on Monday, marking a new low since August 2022.

Ben Hayward, CEO of TwentyFour Asset Management, pointed out that despite some tension arising from government debt levels, investors generally remain optimistic about current buying opportunities in the bond market. A recent survey by the company showed that 80% of institutional investors agree that bonds are attractive in cross-asset allocation at the current yield levels.

"Higher yields enhance potential returns while providing volatility protection for portfolios," Hayward stated. "Therefore, it is not surprising that investors are increasing their allocation to fixed income across various sectors."

编辑/rice