Key Points:

The Federal Reserve cut interest rates for the first time in nine months, with the magnitude and timing of the move in line with market expectations.

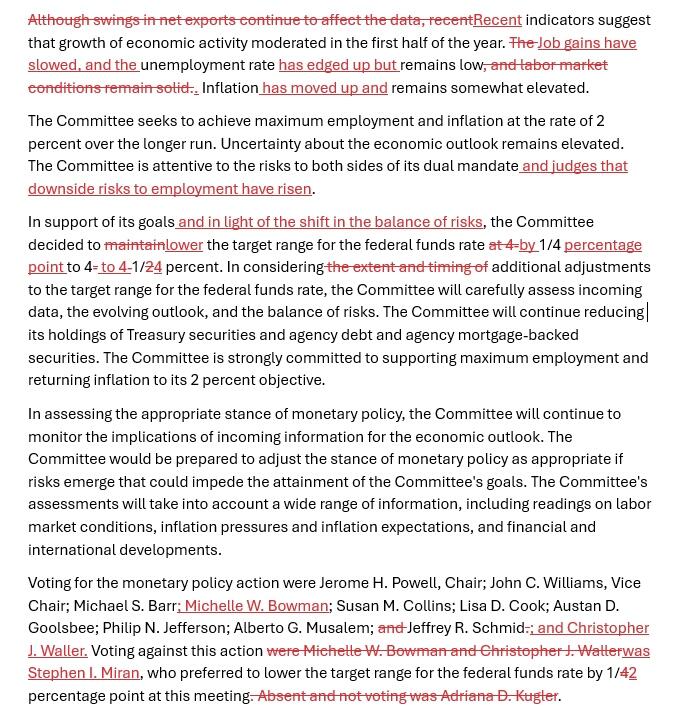

The statement from this meeting newly pointed out that U.S. job growth has slowed, the unemployment rate has risen slightly, downside risks to employment have increased, and the balance of risks has shifted, while removing references to a robust labor market.

Milan, the newly appointed governor chosen by Trump, cast the sole dissenting vote, advocating for a 50-basis-point rate cut. The two members who opposed the previous meeting’s decision both supported the current rate resolution.

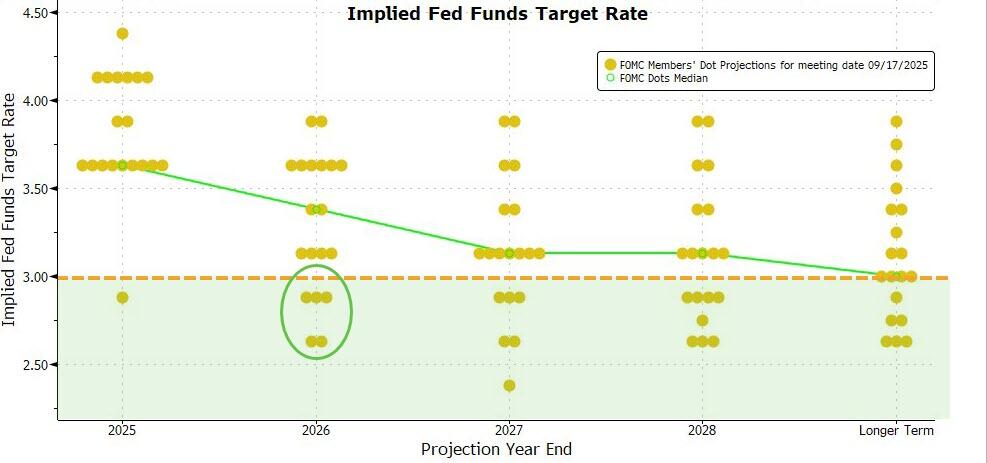

The median forecast for interest rates indicates that the Fed expects to cut rates three times this year, one more time than previously projected, and once more next year. The dot plot shows that nine members expect two more rate cuts this year, though not constituting a majority; six members anticipate no further cuts this year, while one member projects five cuts, amounting to a total reduction of 150 basis points this year.

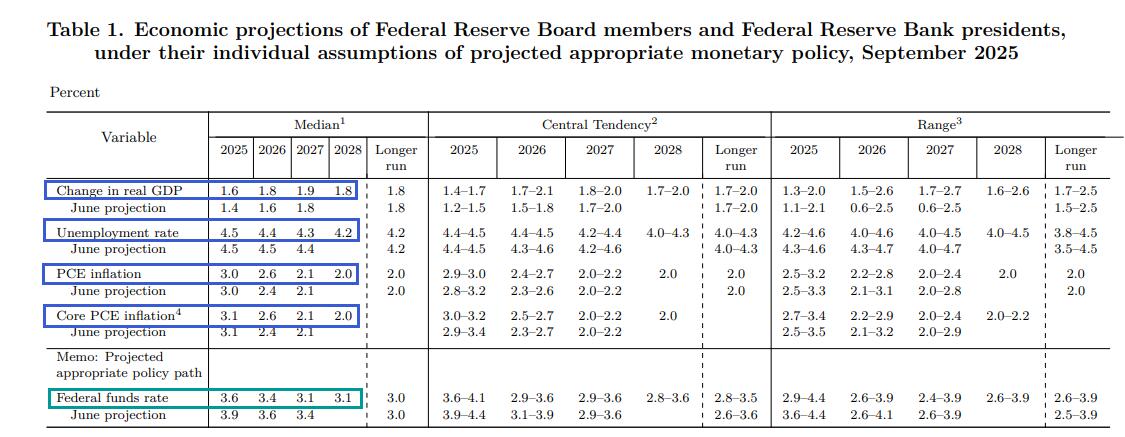

The Fed raised its GDP growth forecasts for this year and the next two years, lowered its unemployment rate projections for the next two years, and revised upward its PCE inflation expectations for the next two years. It anticipates reaching the target inflation rate of 2% by 2028.

The 'New Fed Wire': Concerns about a slowdown in the labor market have outweighed worries about inflation, providing justification for the Fed to pivot toward smaller rate cuts.

The Federal Reserve's first rate cut this year has arrived as expected, with Fed officials emphasizing increased risks to employment and raising the projected magnitude of rate cuts for the year.

On Wednesday, September 17, Eastern Time, following the meeting of the Federal Open Market Committee (FOMC), the Federal Reserve announced a reduction in the target range for the federal funds rate from 4.25%-4.5% to 4.00%-4.25%, a decrease of 25 basis points. This marks the Fed's first decision to cut rates within nine months since the beginning of the year. After three consecutive rate cuts between September and December of last year, this latest move brings the total reduction in the current easing cycle to 125 basis points.

The decision to cut rates at this meeting was entirely anticipated by investors. By Tuesday’s market close, tools from the Chicago Mercantile Exchange (CME) indicated that futures markets assigned about a 96% probability to a 25-basis-point rate cut by the Fed this week, an approximately 80% likelihood of another rate cut at the next meeting in October, and a nearly 74% chance of further easing in December. U.S. Treasury SecretaryBessent said on Tuesdaythat the market is pricing in expectations of a cumulative 75-basis-point rate cut between now and the end of the year.

In the post-meeting statement, the Federal Reserve primarily adjusted its language regarding employment, specifically highlighting increased downside risks to employment. Updated interest rate projections indicate that most Fed policymakers now expect three rate cuts this year, up from the two cuts projected in June, implying two additional 25-basis-point reductions after this week’s cut.

The decision to cut interest rates this time was opposed by only one voting member of the FOMC—Governor Milan, who was appointed by Trump. At least for now, the internal divisions within the Fed regarding rate cuts do not appear as pronounced as during the last meeting, when there were two dissenting votes.

Nick Timiraos, a senior Federal Reserve reporter known as the 'new Fedwire,' wrote after the Fed’s meeting that concerns about a slowing labor market outweighed worries about inflation, providing justification for the Fed's shift toward small rate cuts.

Timiraos pointed out that a slight majority of Fed officials expect at least two more rate cuts this year, implying that the Fed will continue to cut rates at its two remaining meetings in October and December. These forecasts suggest that, against the backdrop of significant policy shifts making economic conditions harder to predict, markets have broadly shifted toward concerns about potential cracks in the labor market.

Job growth has slowed, the unemployment rate has edged up slightly, and downside risks to employment have increased.

Compared to the statement issued after the late-July meeting, the key adjustments in this post-meeting resolution were made in the economic assessment section.

The opening sentence of the previous meeting’s statement read: 'Although fluctuations in net exports have impacted the data, recent indicators suggest moderate economic growth in the first half of the year.' This time, the first part was removed, retaining only the latter portion, reaffirming that 'recent indicators suggest moderate economic growth in the first half of the year.'

This time, the statement did not reiterate that the U.S. unemployment rate remains low, the labor market robust, and inflation still slightly elevated. Instead, it removed references to a robust labor market and added language about slower job growth and a slight rise in the unemployment rate, stating:

"Job growth has slowed, and the unemployment rate has risen slightly but remains low. The inflation rate has increased and is still slightly elevated."

The statement reiterated once again that the FOMC Committee is focused on the dual risks it faces in achieving its dual mandate of full employment and price stability. Additionally, following this sentence, it included a new assessment that downside risks to employment have increased. The statement reads:

"The Committee is attentive to the risks associated with its dual mandate and judges that downside risks to employment have increased."

In addition to supporting its dual mandate of employment and inflation, the statement also mentioned that the decision to cut interest rates was made "in light of the shift in risk balance." At the Jackson Hole central bank symposium at the end of August,speech, Federal Reserve Chair Jerome Powell emphasized the downside risks to employment and pointed out that 'the balance of risks is evolving,' opening the door for an interest rate cut as soon as September.

Moreover, the statement reiterated that the Federal Reserve will continue to reduce its holdings of U.S. Treasuries, agency debt, and agency mortgage-backed securities (MBS).

Starting from April this year, the Fed further slowed the pace of its balance sheet reduction (quantitative tightening, or QT). Specifically, it reduced the monthly redemption cap for U.S. Treasuries from $25 billion to $5 billion, while maintaining the monthly redemption cap for agency debt and agency MBS at $35 billion.

As of this week, the Fed has left the guidance on balance sheet reduction unchanged for four consecutive meetings, indicating that the reduction continues at the aforementioned pace.

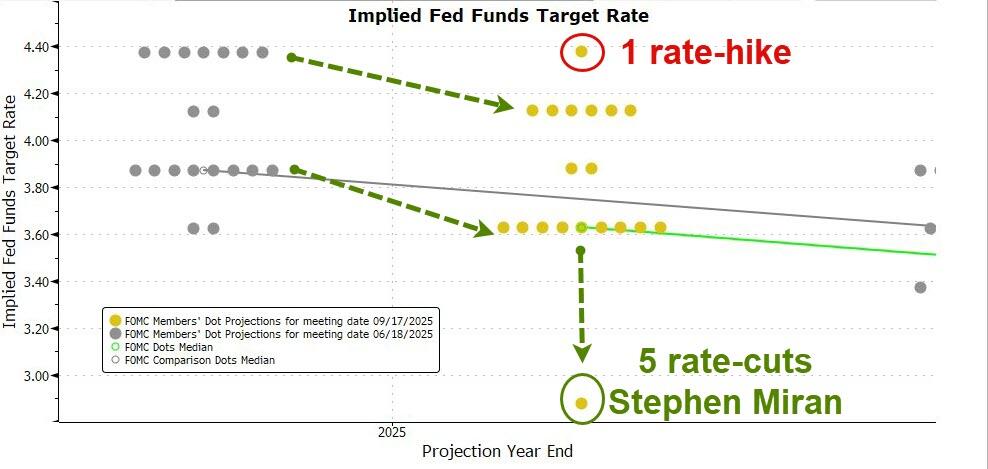

Newly appointed board member Stephen Miran cast a dissenting vote, advocating for a 50-basis-point rate cut.

Apart from economic commentary, another major difference in this statement compared to the previous one is the voting outcome of the Federal Reserve.

The statement showed that among the 12 FOMC members who voted this time, 11 supported a 25-basis-point rate cut, with only one dissenting vote. The dissenter was newly confirmed board member Stephen Miran, who preferred a 50-basis-point rate cut.

At the previous meeting, two members dissented from the decision to pause rate cuts, marking the first time since 1993 that two Fed governors had opposed a resolution. At that time, the dissenters were Fed Governor Christopher Waller and Michael Barr, the Fed Vice Chair for Supervision nominated by Trump, both of whom advocated for a 25-basis-point rate cut.

At this meeting, both Waller and Barr continued to advocate for this level of reduction and did not adopt as aggressive a stance as Miran.

Two recent developments involving Fed governors added drama to the FOMC's voting at this meeting: First, the U.S. Senate confirmed President Trump’s nominee, Stephen Miran, just before the FOMC meeting, making him the fastest person ever to assume a voting position on the FOMC; second, a U.S. appeals court rejected Trump's request to remove Lisa Cook, allowing her to continue attending FOMC meetings.

As previously noted, the Fed’s internal 'super-dovish' faction represented by Miran, Waller, and Barr might vote to support a 50-basis-point rate cut; the centrist faction led by Fed Chair Jerome Powell might support the market-expected 25-basis-point rate cut; Cook might unexpectedly vote for a 25-basis-point rate hike to counter pressure from the White House; officials such as Goolsbee and Harker might vote to maintain rates unchanged.

However, the voting outcome of this meeting did not reveal a more divided scenario.

The red text below highlights the deletions and additions in this resolution statement compared to the previous one.

A single rate cut is expected next year. The dot plot shows that those expecting two more rate cuts within the year do not constitute a majority.

The median value of the Fed officials’ interest rate projections published after Wednesday’s meeting showed that Fed officials lowered their interest rate outlooks for this year, next year, and the year after. The forecasts for this year and the year after were reduced by 30 basis points each, while the forecast for next year was cut by 20 basis points.

The median values of the specific forecasts are as follows:

The federal funds rate is expected to be 3.6% by the end of 2025, compared to the June forecast of 3.9%.

The federal funds rate is projected to be 3.4% by the end of 2026, compared to the June forecast of 3.6%.

The federal funds rate is anticipated to reach 3.1% by the end of 2027, compared to the June forecast of 3.4%.

The federal funds rate is expected to be 3.1% by the end of 2028. The longer-term federal funds rate is projected at 3.0%, unchanged from the June forecast.

Based on the median of the aforementioned interest rates, Fed officials currently anticipate one more rate cut this year compared to their June projections. This implies that, aside from this week’s action, the Fed expects two additional 25-basis-point cuts by the end of the year. Furthermore, the Fed anticipates one rate cut each in the following two years after three cuts this year.

The above projections indicate that, including this week's rate cut, the Federal Reserve is expected to implement a total of 125 basis points in interest rate cuts from September this year to the end of 2027. This reduction is significantly lower than the 300 basis points repeatedly called for by former President Trump.

Commentary suggests that the tilt of the dot plot still indicates a slowdown in rate cuts this year. The median forecast for next year not only declines but also shows five officials projecting that rates will fall below 3.0% by the end of next year, implying two rate cuts are likely.

The median interest rate projections reveal that the majority of Fed officials now expect a total of three rate cuts this year for the first time. However, compared to the dot plot released in June, the updated version shows that the number of officials supporting three cuts this year does not constitute a strong majority.

Among the 19 Fed officials who provided forecasts:

This time, nine members projected two more rate cuts this year, totaling three cuts for the year, accounting for 47% of the total, which is less than half. Last time, only two members made such a projection.

This time, two members projected one more rate cut this year, whereas last time, eight members anticipated a total of two rate cuts for the year.

This time, six members projected no further rate cuts for the remainder of the year, while last time, two members anticipated only one rate cut for the year.

One member projected a single rate hike this time, and another member anticipated five rate cuts this year.

The projection of five rate cuts implies that the official expects a cumulative reduction of 150 basis points in interest rates this year.

This indicates that, although the vast majority of Fed policymakers supported a 25-basis-point rate cut this time, there remains significant divergence regarding the prospect of further rate cuts over the next three months. The individual projecting five rate cuts was likely Milan.

Upward Revision of GDP Forecasts for This Year, Next Year, and the Following Year; Upward Revision of Inflation Forecasts for Next Year and the Following Year

The economic outlook released after the meeting showed that Fed officials revised upward their GDP growth forecasts for this year, next year, and the following year, lowered unemployment rate projections for the next two years, and raised forecasts for PCE inflation as well as core PCE inflation for the same period. They anticipate that by 2028, inflation will return to the Fed’s long-term target level of 2%. If these projections are accurate, it would mark the first time U.S. inflation has met the Fed's target after remaining above it for seven consecutive years.

The specific forecasts are as follows:

GDP growth for 2025 is projected at 1.6%, an increase of 0.2 percentage points from the June forecast of 1.4%. For 2026, growth is expected to be 1.8%, up from the June forecast of 1.6%. For 2027, growth is projected at 1.9%, compared to the June forecast of 1.8%. By 2028, growth is expected to remain steady at 1.8%, consistent with the longer-term forecast from June.

The unemployment rate for 2025 is projected to be 4.5%, unchanged from the June forecast. For 2026, it is expected to be 4.4%, down from the June forecast of 4.5%. In 2027, the unemployment rate is projected to be 4.3%, compared to the June forecast of 4.4%. By 2028, it is expected to reach 4.2%, consistent with the longer-term forecast of 4.2% from June.

The expected PCE inflation rate for 2025 is 3.0%, unchanged from the June forecast; the 2026 forecast is 2.6%, compared to 2.4% in June; the growth forecast for 2027 is 2.1%, unchanged from the June forecast; and the 2028 forecast is 2.0%, with the longer-term forecast remaining at 2.0%, consistent with the June projection.

The core PCE forecast for 2025 is 3.1%, unchanged from the June forecast; the 2026 forecast is 2.6%, compared to 2.4% in June; the 2027 forecast remains at 2.1%, consistent with the June projection; and the 2028 forecast is 2.0%.

Editor/joryn