Citi forecasts that NVIDIA's upcoming earnings report, scheduled for release on November 19, will demonstrate strong performance with 'revenue beating expectations and guidance being raised,' maintaining a 'Buy' rating while increasing the target price to $220. Citi believes the current constraints on NVIDIA’s growth are not due to weak AI demand but rather supply chain bottlenecks such as CoWoS packaging, rendering concerns about an AI bubble unfounded.

Amid an investment frenzy in the artificial intelligence (AI) sector sparking heated market debate over a potential bubble, Citigroup has cast a crucial vote of confidence in $NVIDIA (NVDA.US)$ .

In a research report released by Citi on November 10, the firm maintained its 'Buy' rating for NVIDIA's stock and raised its price target from $210 to $220. More notably, Citi initiated a '30-day short-term bullish' view on the stock, betting that its upcoming earnings report, scheduled for release on November 19, will deliver a robust performance characterized by 'better-than-expected revenue and upward guidance' ('beat and raise').

This report directly addresses investor concerns about the 'frothy' AI capital expenditure. Analysts Atif Malik and Papa Sylla noted in the report that despite questions regarding the source of AI investment funds, a more fundamental reality is that supply of AI chips will remain below demand until at least 2026 due to constrained advanced packaging (CoWoS) capacity.

This report directly addresses investor concerns about the 'frothy' AI capital expenditure. Analysts Atif Malik and Papa Sylla noted in the report that despite questions regarding the source of AI investment funds, a more fundamental reality is that supply of AI chips will remain below demand until at least 2026 due to constrained advanced packaging (CoWoS) capacity.

Citi suggested that NVIDIA’s stock remains attractive at current levels. The report stated that NVIDIA currently trades at a price-to-earnings ratio of approximately 28x, which is more favorable compared to its AI peers Broadcom at 38x and AMD at 37x.

Earnings Beat Imminent?

Citi expects NVIDIA's upcoming earnings report to easily surpass Wall Street’s consensus estimates. The report forecasts that the company’s sales for the quarter ended October will reach $57 billion, exceeding the market’s average estimate of approximately $55 billion.

Regarding future outlook, Citi anticipates that NVIDIA’s sales guidance for the January quarter will reach $62 billion, again surpassing the market expectation of around $61 billion.

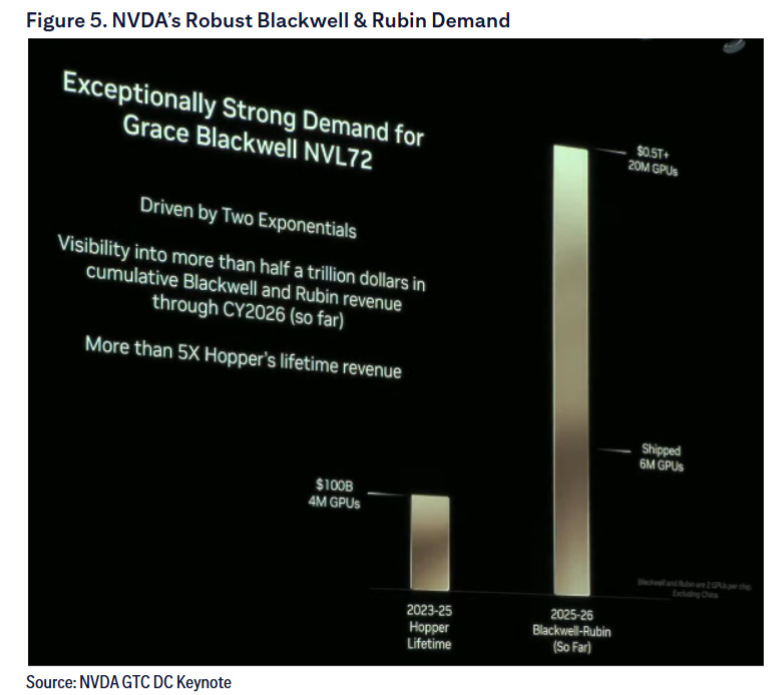

The report pointed out that behind this optimistic forecast is the robust shipment momentum of NVIDIA’s Blackwell architecture GPUs. Citi analysts believe that the information disclosed at NVIDIA’s GTC Washington event—indicating shipments of 6 million GPUs—is a strong signal that its October and January quarterly results may exceed expectations.

Citi stated in the report that its model assumes NVIDIA’s data center sales will grow sequentially by 24% and 12% for the October and January quarters, respectively, compared to market expectations of 19% and 15%, respectively.

The 'AI Bubble' Theory Rebuffed

In response to the increasingly heated 'AI bubble' rhetoric in the market, Citi presented a diametrically opposed view. The core argument of the report is that the primary contradiction in the current AI chip market lies in supply shortages rather than insufficient demand.

“Despite concerns about debt and revolving financing portfolios surrounding an AI capex bubble, we fundamentally see AI supply remaining below demand until 2026 due to CoWoS capacity constraints, and it may only catch up at some point in 2027.”

The report noted that this assessment implies strong demand is genuine and not driven by speculative hype.

To further substantiate robust demand, Citi also pointed out that cloud revenues for hyperscalers are set to reach an inflection point starting in 2025 and are expected to continue accelerating in 2026, primarily driven by the widespread adoption of enterprise-level AI applications.

Target Price Raised to $220

Based on strong confidence in NVIDIA’s growth prospects, Citi not only raised its target price but also comprehensively upgraded its financial forecasts. The new $220 target price is based on an earnings per share (EPS) forecast of $7.24 for NVIDIA in calendar year 2026, applying a 30x price-to-earnings (P/E) ratio.

The report shows that Citi increased its EPS forecasts for NVIDIA's fiscal years 2026, 2027, and 2028 by 2%, 7%, and 8%, respectively, to better align with the bank’s revised global AI capital expenditure model. Notably, Citi continues to assume zero sales from Chinese data centers in its model, which means any policy easing could bring additional upside potential.

Is the AI Chip Market Far From Peaking?

Citi's bullish view is not limited to NVIDIA itself but extends to the entire AI semiconductor market. The report significantly raised its forecast for the future market size, stating that the wave of AI has far from reached its peak.

According to Citi's latest model, by 2028, the total addressable market (TAM) for the global data center semiconductor market is expected to reach USD 654 billion, 16% higher than the previous forecast of USD 563 billion. The report explained that the main reason for the upward revision is 'higher-than-expected demand from key AI players such as OpenAI.'

Futubull AI: Your Portfolio Manager! Your Stock Selection Advisor!Come and experience it now >>

Futubull AI: Your Portfolio Manager! Your Stock Selection Advisor!Come and experience it now >>

Editor /rice