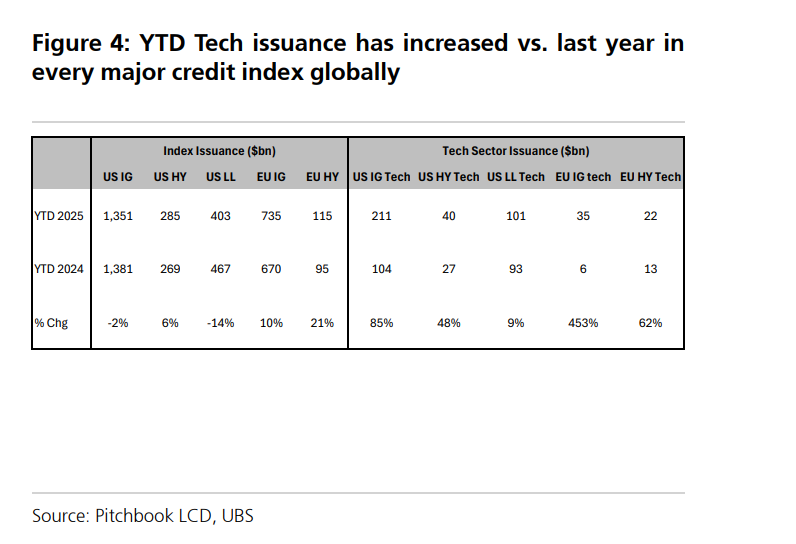

The global wave of technology bond issuance is spreading from the United States to international markets, with U.S. investment-grade technology bond issuance surging 115% year-on-year to USD 211 billion. Issuance in Europe’s investment-grade and high-yield markets has also grown significantly, while the private credit market has absorbed over USD 100 billion in financing. This global debt issuance boom, driven by the AI capital race, is reshaping the credit bond market landscape across countries.

A capital expenditure race driven by artificial intelligence is propelling global tech giants into the debt market at an unprecedented pace, reshaping the credit bond landscape from the United States to Europe. Despite the record-breaking scale of bond issuance, analysis suggests that its impact on overall credit spread may be relatively limited.

The US market has been the first to feel this wave of enthusiasm. Industry giants, including $Meta Platforms (META.US)$ 、 $Alphabet-C (GOOG.US)$ and $Oracle (ORCL.US)$ , have collectively raised over $70 billion in recent times. So far this year, the issuance volume of US investment-grade technology bonds has surged 115% year-on-year, reaching $211 billion. Its share of the total issuance volume in the investment-grade market reached a multi-year high in October.

The implications of this trend are far from over. Projections indicate that if capital expenditure expectations for hyperscale data centers materialize by 2026, the public investment-grade credit market could see an additional $140 billion to $175 billion in new bond supply, while the private market will absorb at least $100 billion to $125 billion in financing.

The implications of this trend are far from over. Projections indicate that if capital expenditure expectations for hyperscale data centers materialize by 2026, the public investment-grade credit market could see an additional $140 billion to $175 billion in new bond supply, while the private market will absorb at least $100 billion to $125 billion in financing.

This surge in bond issuance is not unique to the U.S. Data shows that the issuance of tech bonds across major global credit markets is growing in tandem, spanning both investment-grade and high-yield markets in Europe as well as the rapidly expanding private credit sector. This underscores that funding AI infrastructure has become a shared financial theme across the global tech industry.

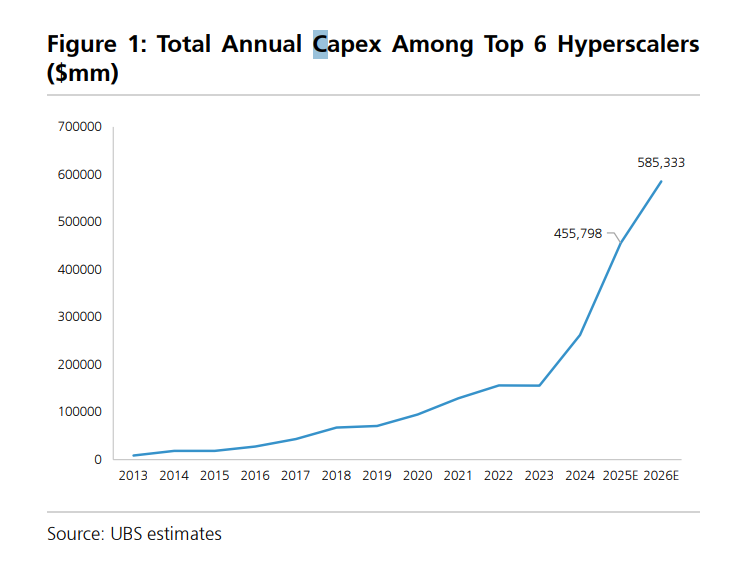

AI Arms Race Drives Trillion-Dollar Capital Expenditure

The direct impetus behind the large-scale bond issuance by tech giants lies in the massive investments required for AI infrastructure. Analysts predict that the total capital expenditure of the top six hyperscale data center operators will soar from approximately $260 billion in 2024 to nearly $600 billion by 2026.

To finance these extensive spending plans, companies are actively turning to the bond market. Notable recent deals include Meta’s $30 billion bond issuance, Alphabet’s $24 billion offering, and Oracle’s $18 billion issuance. These substantial financings have driven a 115% year-over-year surge in U.S. investment-grade tech bond issuance, reaching $211 billion, with hyperscale data center operators contributing $80 billion.

This wave of issuance has significantly increased the weight of the tech sector within the credit bond market. In October, tech bonds accounted for 34% of total U.S. investment-grade bond issuance, up sharply from 7% in June, marking a multi-year high. Although the total issuance volume of the investment-grade market has remained flat year-over-year, issuance in the tech sector has nearly doubled since the beginning of this year.

The bond issuance boom has spread from the United States to the rest of the world.

In line with trends in the U.S. market, technology companies globally are ramping up their debt issuance efforts. Data shows that issuance activity in the tech sector has significantly increased across multiple major credit bond indices. Compared to the same period last year, high-yield tech bond issuance in the U.S. market rose from $27 billion to $40 billion, the European investment-grade market grew from $6 billion to $35 billion, and the European high-yield market expanded from $13 billion to $22 billion.

In most markets, the rolling annual average of tech bond issuance as a proportion of total index volume has surpassed the five-year average, particularly in the U.S. investment-grade market. Meanwhile, the private placement credit market has also become an important financing channel for tech companies. As of 2025, tech issuers have raised approximately $120 billion through private placements, surpassing the $88 billion in all of 2024 and $53 billion in 2023. Additionally, over $40 billion in project finance and infrastructure transactions across recent quarters remain unaccounted for.

However, the surge in issuance has raised concerns about concentration risk. Data indicates that the top five issuers this year account for approximately 50% of the total issuance of U.S. investment-grade tech bonds.

Credit spread impact may be limited.

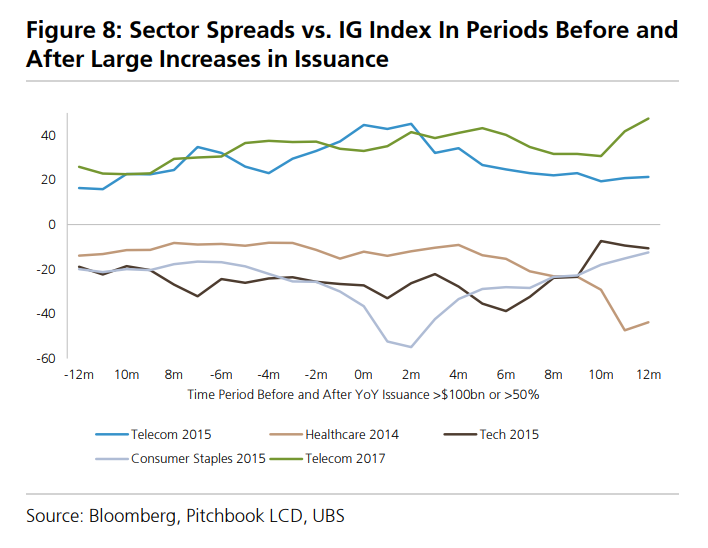

Despite the notable scale of debt issuance in the tech industry currently, historically, issuance peaks in specific industries have not been isolated incidents and have not caused sustained negative impacts on the market.

Similar issuance waves have occurred in various sectors. For instance, the healthcare industry in 2015 saw substantial bond issuance due to reforms under the Affordable Care Act and merger and acquisition activities, such as AbbVie's acquisition of Pharmacyclics. In 2013 and 2017, the telecommunications sector experienced heightened issuance driven by large-scale deals like Verizon’s acquisition of Vodafone’s stake and AT&T’s merger with Time Warner. The tech industry itself underwent a similar cycle between 2014 and 2017, driven by the expansion of 4G LTE networks and cloud infrastructure development.

Looking back at these periods, the average annual issuance growth in related industries was 83%, but it did not lead to sustained poor performance of their bonds. Data shows that, in the 12 months following issuance peaks, the average spreads of these industries narrowed by approximately 2 basis points relative to the investment-grade index.

Based on historical experience, analysts believe that the impact of this wave of technology sector bond issuance on the overall investment-grade index spread will be "negligible." For spreads within the technology sector itself, the impact will be "limited to moderate," depending on the scale of issuance, maturities, and market sentiment towards AI prospects. Therefore, analysts have maintained their year-end forecasts for U.S. investment-grade spreads at 90 basis points and high-yield spreads at 325 basis points.

Editor/Doris