Morgan Stanley stated that industry research indicates a substantial acceleration in demand. NVIDIA has fully resolved the early rack-related issues, while demand continues to surge. The full-scale production ramp-up of the Blackwell chip will be a key driver. NVIDIA's positive announcements at the GTC conference further reinforced this trend. Current growth bottlenecks are primarily on NVIDIA’s supply side as well as in complementary hardware (storage, servers), and space/power constraints, but these should not slow down the evident acceleration in demand.

Morgan Stanley raised $NVIDIA (NVDA.US)$ the price target to $220. Analysts expect NVIDIA’s upcoming Q3 earnings report to mark a breakthrough quarter, potentially dispelling market perceptions that its growth has peaked.

According to the Storm Chaser trading platform, in a report released on November 14 by Morgan Stanley analyst Joseph Moore, industry surveys indicate a substantial acceleration in demand. NVIDIA has fully resolved early rack-related issues, while demand continues to surge. Current bottlenecks are primarily on NVIDIA’s supply side as well as in complementary hardware (storage, servers), and space/power constraints, but these factors should not slow the evident acceleration in demand.

The ramp-up of Blackwell chip production into full-scale mass production will serve as a key driver. NVIDIA’s positive remarks at the GTC conference further reinforced this trend.

The ramp-up of Blackwell chip production into full-scale mass production will serve as a key driver. NVIDIA’s positive remarks at the GTC conference further reinforced this trend.

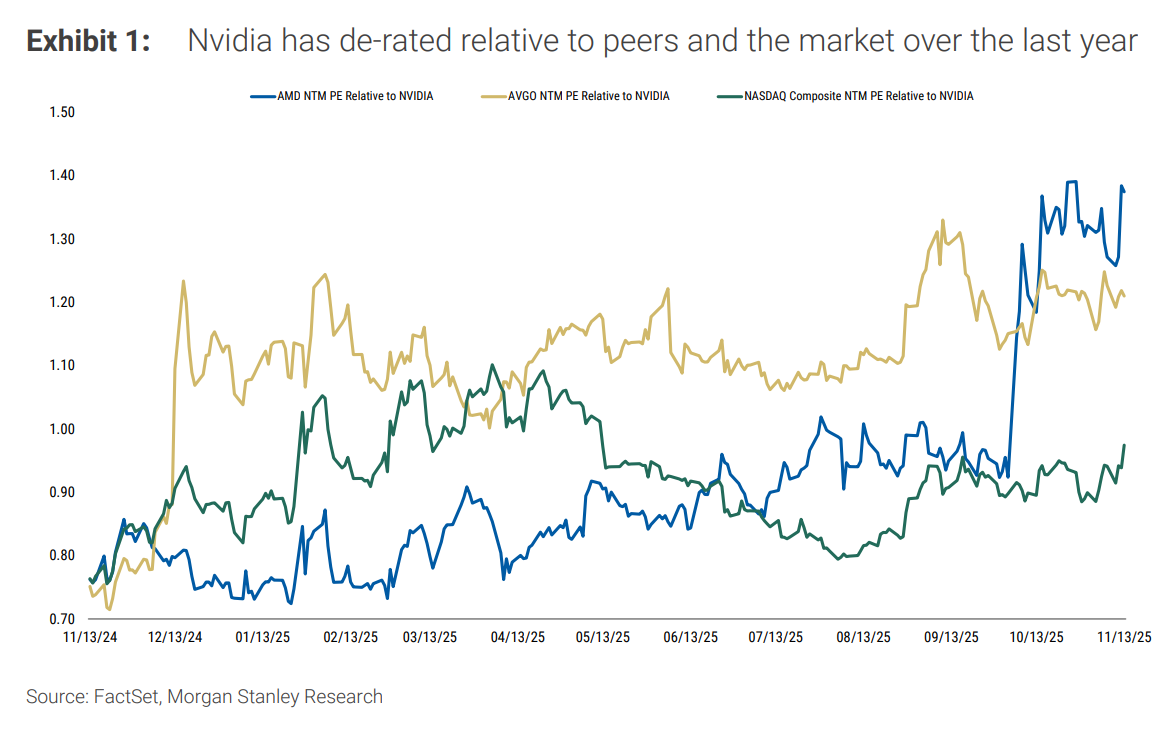

Morgan Stanley believes that next week’s results will represent one of NVIDIA’s strongest earnings reports over recent quarters. Despite NVIDIA’s solid stock performance, it has lagged relative to AI peers, a situation expected to reverse.

Supply and demand data show accelerating demand exceeding expectations.

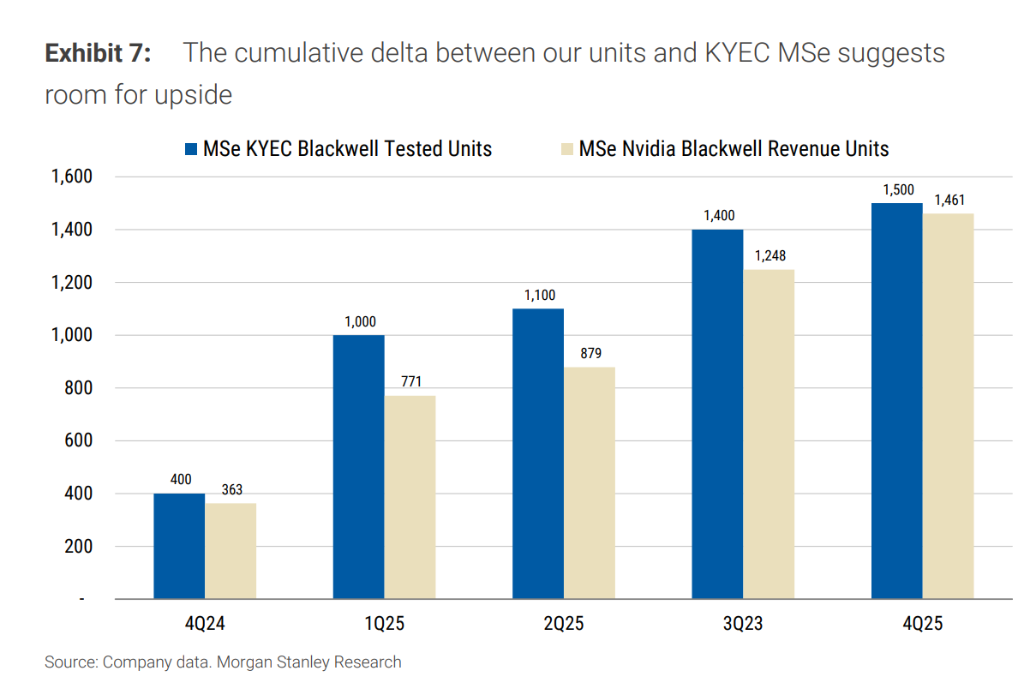

Morgan Stanley’s industry survey indicates that signals from NVIDIA’s customers and suppliers in Q3 all point to accelerating growth, contrasting sharply with the prevailing market view that NVIDIA’s growth metrics have peaked.

On the customer front, expectations for cloud capital expenditure in Q3 were revised upward to $142 billion, with each of the four hyperscale cloud service providers adding more than $20 billion. The dollar growth for 2025 now stands at $115 billion, up 60% from a quarter ago.

From the supplier perspective, ODM Quanta expects its AI server revenue to accelerate in Q1 2026, with year-on-year growth exceeding 100% in 2026. To support this demand, Quanta plans to double its AI server production capacity next year, as order visibility extends to 2027.

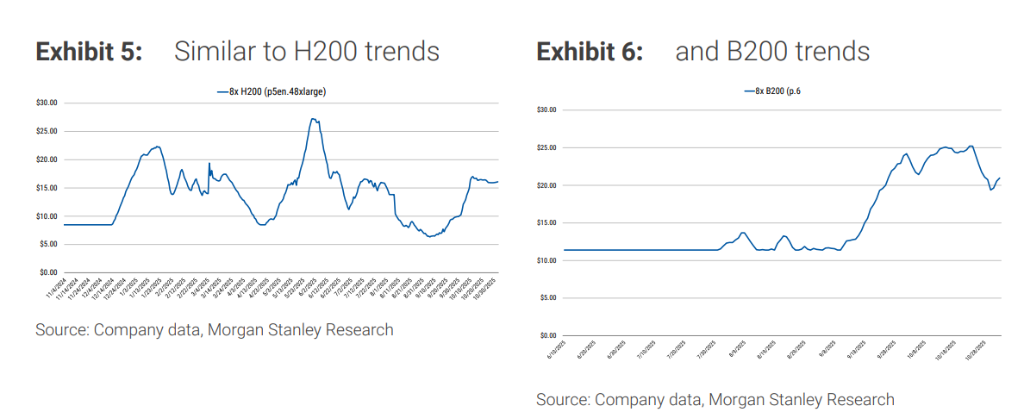

Blackwell chips emerge as the core growth engine.

Morgan Stanley raised its revenue forecast for NVIDIA’s October quarter from USD 54.4 billion to USD 55.0 billion and its January quarter forecast from USD 61.2 billion to USD 63.1 billion. Analysts noted that achieving an incremental growth of USD 8.0 billion sequentially in both October and January would set a record high in industry history.

The Blackwell chip remains the preferred choice for AI chips, with very strong demand signals for Vera Rubin. While competitors have shown enthusiasm, this reflects both progress and the robustness of market demand.

NVIDIA CEO Jensen Huang previously indicated that revenue needs to grow within the range of USD 70 billion to USD 80 billion over the next five quarters (Morgan Stanley increased this estimate by USD 22 billion). Currently, the stock price is 10% below its peak following that statement.

Morgan Stanley revised NVIDIA’s fiscal 2027 estimates upward from USD 278 billion in revenue / USD 6.59 non-GAAP EPS to USD 298.5 billion / USD 7.11. Analysts believe that, considering the robust order backlog, the company could provide higher guidance, contingent on how conservative it chooses to remain amid strong demand conditions.

The new target price of USD 220 is based on 26 times the fiscal 2027 ModelWare EPS estimate of USD 8.43, approximately equivalent to 25 times the non-GAAP forward P/E ratio. This valuation represents a discount compared to the average forward P/E ratio of 32 times over the past two years and the two-year average P/E of 28 times, reflecting expectations of slower growth while also remaining at a discount relative to larger AI semiconductor peer Broadcom.

Upgraded performance insights deliver a competitive edge in seizing opportunities!Come and experience it now >>

Upgraded performance insights deliver a competitive edge in seizing opportunities!Come and experience it now >>

Editor/Lambor