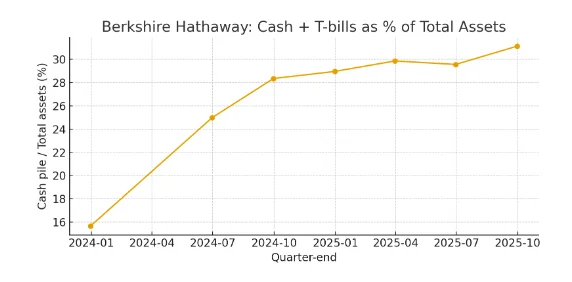

In the past two years, $Berkshire Hathaway-B (BRK.B.US)$ The scale of cash and short-term U.S. Treasuries has surged: from approximately $168 billion at the end of 2023, to $277 billion by mid-2024, and further to a record $381.7 billion in the third quarter of 2025. When viewed as a percentage of total assets, this trend becomes even clearer—cash accounted for about 15% of total assets in 2023, a moderate level, but has now risen to roughly one-third.

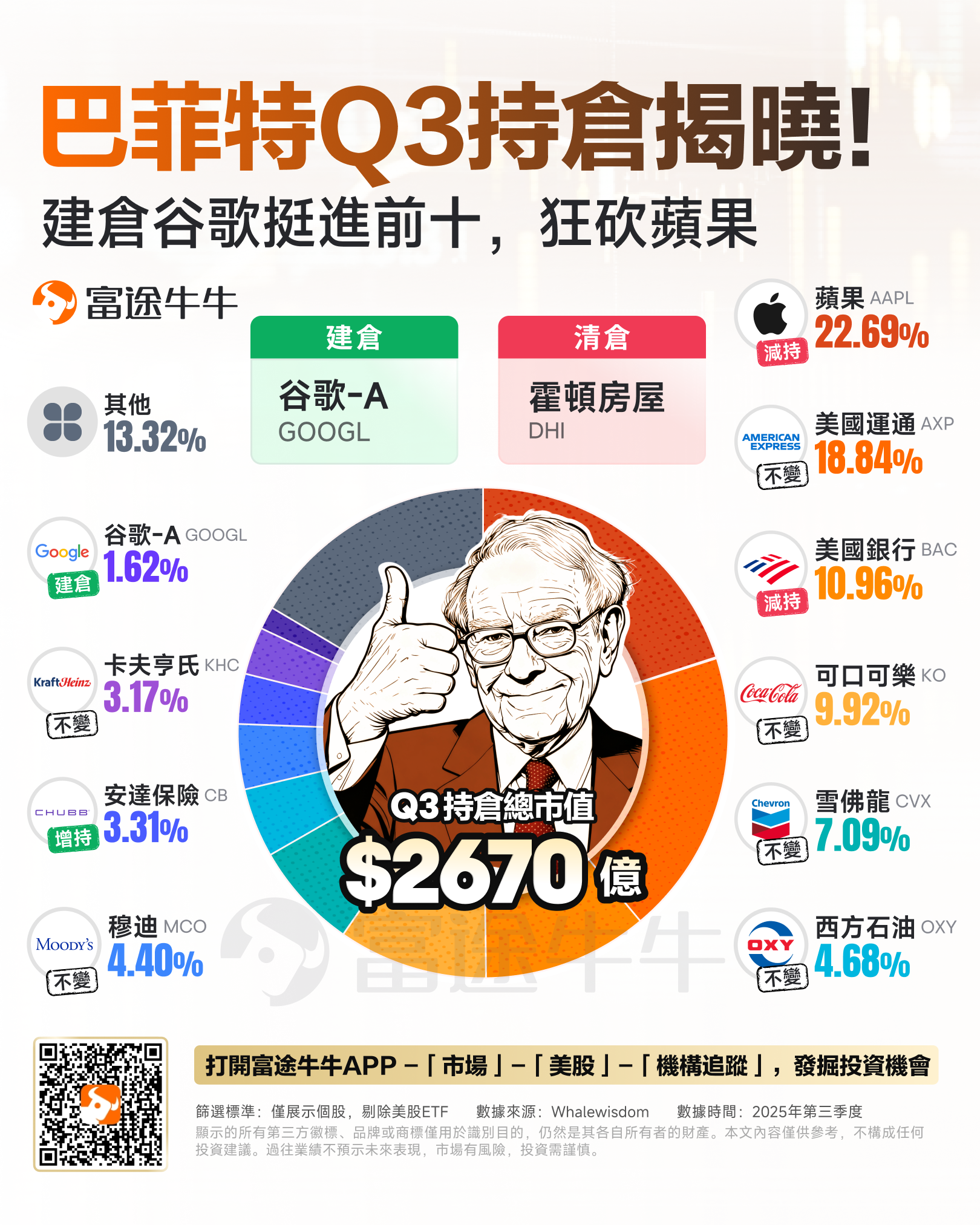

However, while setting a new record for the largest corporate cash reserve in history, Berkshire Hathaway did something unusual: it disclosed for the first time a holding worth $4.3 billion in $Alphabet-C (GOOG.US)$ , while reducing its stake in $Apple (AAPL.US)$ . Currently, Google has become one of Berkshire Hathaway's top ten holdings; Apple, though still its largest position, has seen its share count drop sharply from over 900 million shares at its peak to approximately 238 million shares.

For ordinary investors, the question is straightforward: what signal is Buffett sending to the market with this move? What are his true views on the 'Magnificent Seven' of U.S. stocks and AI-related valuations? And how should we respond?

The current market is not a bubble akin to that of 2000, but the top tier has become extremely crowded.

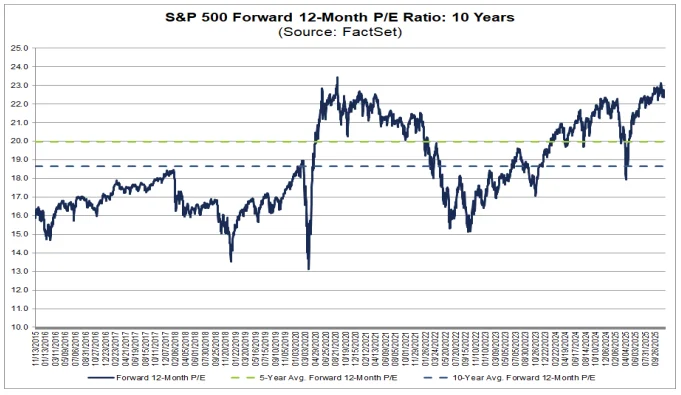

According to the latest Earnings Insight report released by FactSet,$S&P 500 Index (.SPX.US)$The forward price-to-earnings (P/E) ratio for the next 12 months is approximately 22–23 times, higher than its five-year average of 20 times and ten-year average of 18.7 times.

According to the latest Earnings Insight report released by FactSet,$S&P 500 Index (.SPX.US)$The forward price-to-earnings (P/E) ratio for the next 12 months is approximately 22–23 times, higher than its five-year average of 20 times and ten-year average of 18.7 times.

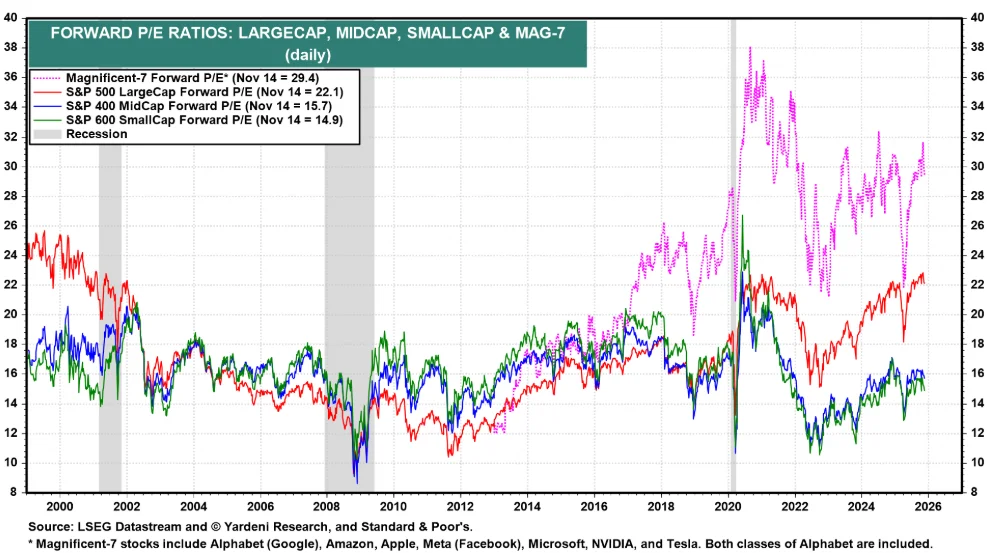

Meanwhile, the overall valuation multiples of the 'Magnificent Seven' are as high as approximately 29.4 times, significantly above the broader market level; in contrast, mid-cap and small-cap stocks are relatively inexpensive, with a P/E ratio of only about 15 times. In other words, the current valuation divergence is not between 'equities vs bonds,' but rather between 'the seven major technology giants vs all other companies.'

The issue lies in the fact that investors have stronger confidence in the AI-driven growth prospects of the 'Magnificent Seven' and are willing to pay a higher premium for them, whereas they generally hold a skeptical attitude toward small- and mid-cap stocks that do not directly benefit from the AI wave. As a result, this valuation gap is unlikely to narrow in the short term.

Among the 'Magnificent Seven,' which companies are overvalued, and which are not?

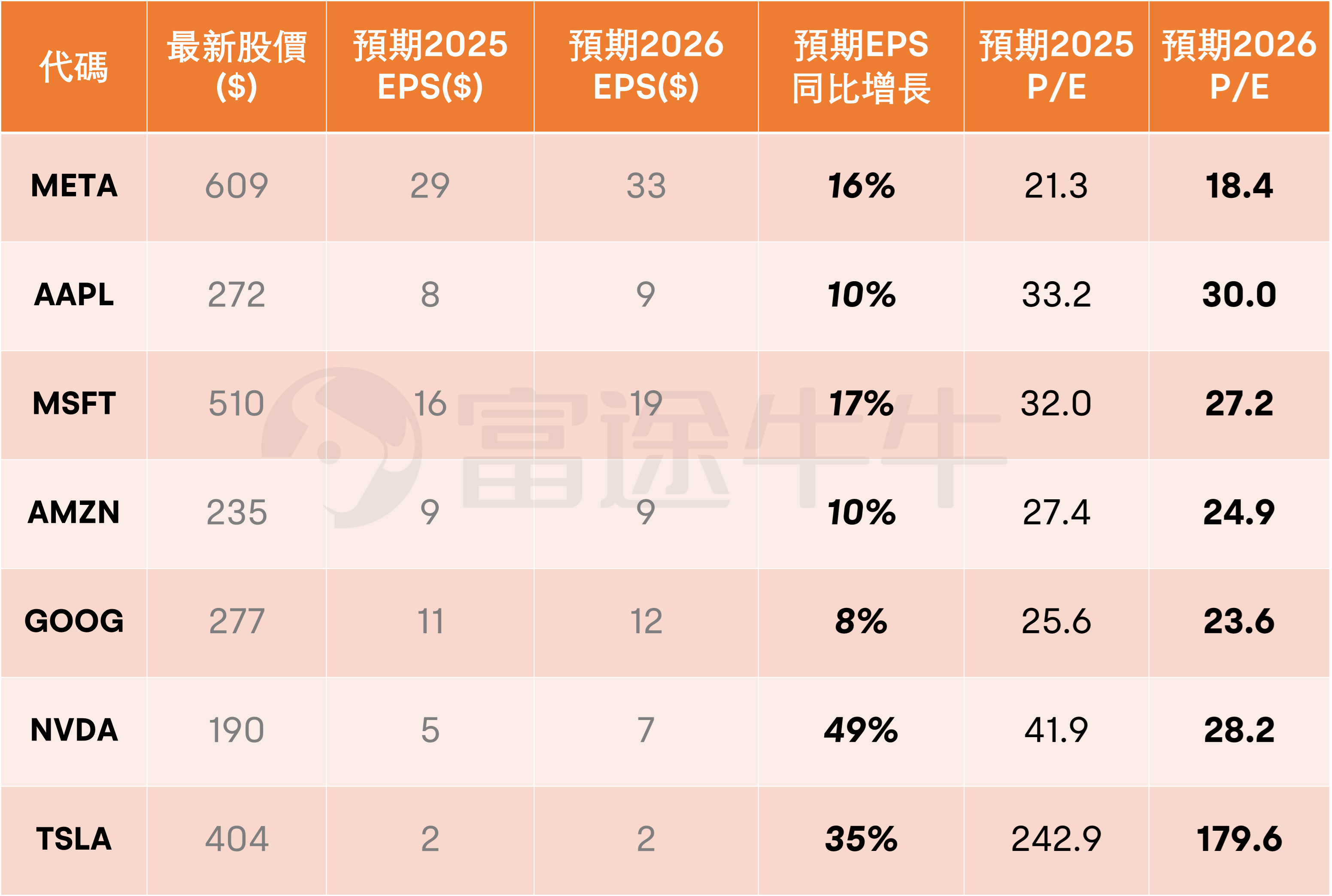

Bloomberg data shows that within the 'Magnificent Seven,' there are significant differences in how well each company’s valuation aligns with its growth:

$Meta Platforms (META.US)$ The forward P/E ratio for 2025 is 21 times, with earnings per share (EPS) growth of approximately 16%, corresponding to a PEG ratio (price-to-earnings-to-growth ratio) of about 1.3, making it a typical 'high-quality growth stock' rather than a bubble.

$Microsoft (MSFT.US)$The P/E ratio is approximately 32x, with EPS growth of 17% and a PEG close to 1.9;

$Amazon (AMZN.US)$The P/E ratio is about 27x, with EPS growth of 10% and the PEG rising to 2.7 — indicating that investors are paying a high premium for their sustained cloud computing and ecosystem scale.

In comparison:

$Apple (AAPL.US)$ The P/E ratio for 2025 is approximately 33x, but the EPS growth rate is only 10%;

$Alphabet-C (GOOG.US)$ The P/E ratio is about 25.6x, with an EPS growth rate of around 8%; both have PEGs exceeding 3. However, Google has a clearer growth narrative in AI infrastructure (e.g., TPU chips, Google Cloud, Gemini large model), provided execution is on track.

$NVIDIA (NVDA.US)$It presents a completely opposite picture: the P/E ratio is approximately 41.9x, but the expected EPS growth rate is close to 49%, with a PEG below 1. This suggests that as long as the AI data center boom continues, investors are willing to accept extremely high apparent valuations.

$Tesla (TSLA.US)$This valuation forms its own category: a forward P/E ratio exceeding 240 times, corresponding to approximately 35% EPS growth, with a PEG close to 7. Such a valuation only makes sense if the market is confident that its long-term robotaxi and robotics businesses will completely disrupt the current profit model.

Earnings Growth and Valuation of the Seven Giants in the U.S. Stock Market for 2025-26

What Are the Lessons from Buffett's Investment in AI?

Using a 'Buffett-style' cash buffer to control overall risk in a highly valued market, Berkshire Hathaway holds USD 381.7 billion in cash—not betting against AI's failure but purchasing insurance against uncertainty. For ordinary investors, this implies allocating a reasonable portion of their portfolio to cash or bonds. Once AI-related assets experience a valuation correction, they should buy the dip rather than panic sell.

Within the AI sector, shift toward high-quality growth stocks and accumulate on dips instead of chasing highs. Avoid stocks with the most extreme valuations and prioritize AI leaders with solid profitability and sustainable growth. In anticipation of an upcoming tug-of-war between 'earnings upgrades and valuation downgrades,' gradually increase positions in quality stocks during pullbacks instead of blindly chasing every short-term spike in AI concepts.

Futubull AI: Your Portfolio Manager!Your stock-picking think tank!

Futubull AI: Your Portfolio Manager!Your stock-picking think tank!

Editor/Richar, Rocky