Trading volumes in the U.S. options market have repeatedly hit record highs, but the OCC clearing system's heavy reliance on a few banks for guarantees has raised concentration risk, prompting a public warning from Cboe's CEO.

The U.S. options market is heading toward a sixth consecutive year of record trading volumes, but some prominent industry players are increasingly concerned about the risks posed by the market's heavy reliance on a small group of banks providing trade guarantees to the largest market makers.

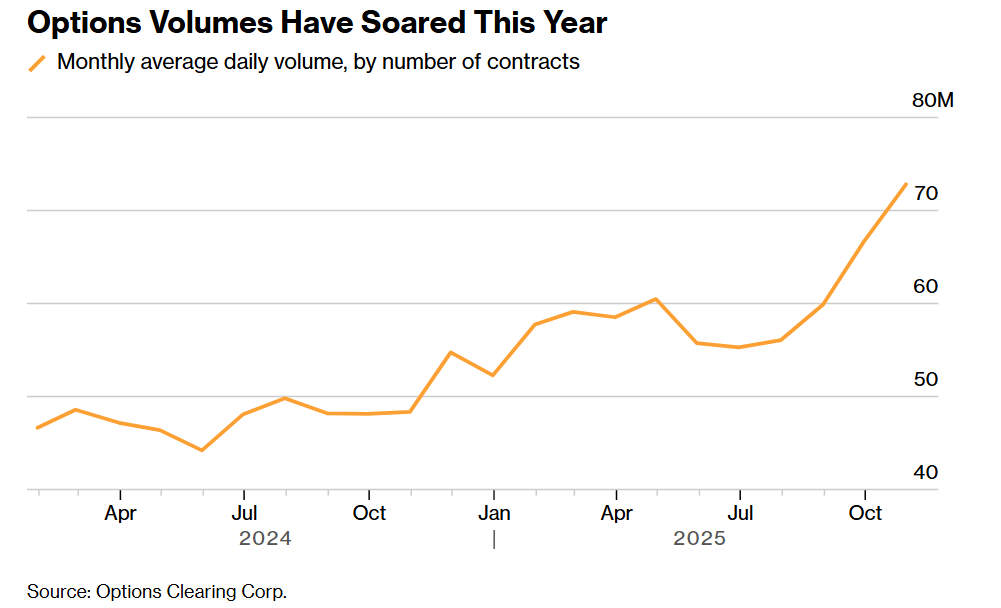

All U.S.-listed options trades must be processed through The Options Clearing Corporation (OCC) — the central counterparty that handles over 70 million contracts daily during peak trading periods. Trades are submitted to the clearinghouse by OCC members, who are responsible for facilitating clearance and acting as guarantors in the event of client insolvency.

Concentration in this area is extremely high. Among dozens of member institutions, the top five firms contributed nearly half of the OCC’s default fund as of the second quarter of 2025. Market participants noted that Bank of America, Goldman Sachs, and ABN AMRO are the three dominant institutions, shouldering most of the market makers’ positions — almost every options trade requires a market maker as the counterparty. Such concentration among a few institutions implies that if one were to face a crisis, it could trigger widespread losses.

Concentration in this area is extremely high. Among dozens of member institutions, the top five firms contributed nearly half of the OCC’s default fund as of the second quarter of 2025. Market participants noted that Bank of America, Goldman Sachs, and ABN AMRO are the three dominant institutions, shouldering most of the market makers’ positions — almost every options trade requires a market maker as the counterparty. Such concentration among a few institutions implies that if one were to face a crisis, it could trigger widespread losses.

“I believe there is significant concentration risk in the clearing intermediary space,” said Craig Donohue, CEO of Cboe Global Markets, Inc., in an interview (without naming specific banks). “I am genuinely concerned about it.”

While the risk of a major bank failure is low, it is not without precedent. Donohoe has personally experienced the fallout from a clearing member default: In October 2011, during his tenure as CEO of CME Group Inc., MF Global declared bankruptcy.

A more immediate risk lies in whether these banks can sustain their clearing capacity amid explosive growth in the listed derivatives market — OCC’s average daily volume surged 52% year-on-year in October. This has spurred the rise of a 'self-clearing' trend among market makers (where they become direct members of the clearinghouse), but given their weaker capital base compared to banks, this model itself carries inherent risks.

Bank of America and Goldman Sachs both declined to comment, while ABN AMRO did not immediately respond to requests for comment.

Only a few clearing brokers are capable of conducting cross-margining between futures and options – offsetting positions in related instruments to reduce the required margin. For instance, if a trader holds a long position in E-mini S&P 500 futures while simultaneously holding a short position in S&P 500 index options, their net risk exposure will be correspondingly reduced.

"Only a small number of member institutions can genuinely support certain market makers, especially in cross-margining operations," said Andrej Bolkovic, CEO of OCC, in an interview. "I believe market makers want this situation to change. It is a well-known issue within the industry, and we sincerely support such a change."

The challenge for banks lies in the fact that even if clearinghouses agree to offer margin discounts based on net risk levels, the banks' own capital frameworks may still account for the two transactions separately, thereby incurring additional costs.

Challenges Posed by Fragmented Regulation

The fragmented regulatory system in the United States exacerbates this dilemma. Banks are regulated by the Federal Reserve System, broker-dealers and options markets fall under the jurisdiction of the U.S. Securities and Exchange Commission (SEC), while futures markets, including equity futures, are overseen by the Commodity Futures Trading Commission (CFTC). This means that even if banks offer customers cross-margining benefits, they may still need to reserve funds to guarantee the trades.

The rise of zero-day-to-expiry options (0DTE options) and the surge in retail trading volumes have posed new challenges for clearing members. If the market shifts to a 7×24-hour trading model, it could place greater pressure on the system and raise the barriers to entry for other institutions in this space.

Capacity upgrades and technological investments aimed at handling increased trading volumes and risks are likely to result in costs being passed on to clients. According to informed sources, Bank of America has raised its per-transaction fee for options clearing from $0.02–$0.03 to a maximum of $0.04.

Default Fund Reform

OCC has proposed revising the calculation methodology for member contributions to the approximately $20 billion default fund to more equitably reflect the market risk of each broker's portfolio. The fund is designed to ensure sufficient resources to compensate other members in the event that the two largest clearing firms fail simultaneously.

Under the current mechanism, 70% of contributions are based on member institutions’ ability to withstand roughly 5% market volatility. OCC has applied to the SEC to adjust this metric to incorporate considerations of a market crash akin to the one in 1987 – when the Dow Jones Industrial Average plummeted 22.6% in a single day.

Donohue pointed out that the continued vigilance of clearing houses is itself a demonstration of strength: 'The regulatory and operational models have been continuously adjusted to better manage such risks.' Donohue, who served as chairman of the OCC from 2014 to 2025, hopes more institutions will become involved in the field of options clearing.

"If there were a magical way to introduce more competition, more clearing capabilities, with a more distributed and diversified presence in this space, it would obviously be highly beneficial for the market," said Donohue.

Editor/Liam