Overview of Key Events This Week

The Fed's December FOMC interest rate decision and Powell's press conference are imminent.

At 3:00 AM Beijing time on December 11, the Federal Reserve will announce its December interest rate decision, followed by a press conference held by Powell half an hour later. The market anticipates with an 84% probability that the FOMC will cut rates by 25 basis points for the third time, achieving a total easing of 75 basis points this year.

Despite the government shutdown causing some data to be missing, September’s PCE showed a slowdown in consumption and moderate inflation, while JOLTS job openings declined, supporting expectations for rate cuts. However, there has been a rare divergence within the Fed: at least five of the twelve voting members prefer to pause rate cuts, while a few others advocate for more aggressive easing. If there are more than three dissenting votes this time, it would mark the first such occurrence since 2019, and only the ninth time since 1990.

The market is highly focused on three key aspects: whether Powell can push through a rate cut with minimal dissenting votes, demonstrating leadership; whether his tone at the press conference leans dovish, especially given weak ADP employment data and a subdued Beige Book; and the latest dot plot and economic forecasts—if the GDP growth projections for 2025-2026 are raised but only one rate cut is signaled for next year, it could be seen as a hawkish signal.

The market is highly focused on three key aspects: whether Powell can push through a rate cut with minimal dissenting votes, demonstrating leadership; whether his tone at the press conference leans dovish, especially given weak ADP employment data and a subdued Beige Book; and the latest dot plot and economic forecasts—if the GDP growth projections for 2025-2026 are raised but only one rate cut is signaled for next year, it could be seen as a hawkish signal.

This decision will not only determine the year-end performance of risk assets but also provide crucial guidance for the path of interest rate cuts in 2026 and global central bank policies. Against the backdrop of Trump's era potentially ending Powell's term prematurely, the level of division at this meeting, adjustments to the dot plot, and Powell's tone may become his last significant policy signal during his tenure.

In addition to the Federal Reserve, central banks in Canada, Australia, Switzerland, Brazil, Peru, the Philippines, South Africa, Ukraine, and Turkey will also announce their interest rate decisions next week.

China's economic data releases and major year-end meetings are approaching.

On December 8 (Monday), China will release its November import and export data. On December 10 (Wednesday), China will announce its November CPI and PPI data. Market expectations are currently optimistic, with Zhejiang Securities forecasting a 3.3% increase in exports and a 2.5% rise in imports. They noted that expanding non-U.S. markets and the Sino-U.S. agreement may respectively support export resilience and year-end imports.

Additionally, China is expected to release its November financial data next week, including key indicators such as new RMB loans, total social financing, and money supply M1 and M2. The critical signal lies in the change in M1 growth rate, particularly whether the 'scissors gap' with M2 narrows, which will directly reflect the activity of corporate current deposits and whether there are significant signs of 'deposit migration' towards investment or consumption areas.

In addition, a year-end high-profile meeting is about to convene to set the tone for next year's economic work. According to惯例, the Political Bureau of the Central Committee of the Communist Party of China and the Central Economic Work Conference will be held in early to mid-December to deploy the economic work for 2026.

Ming Ming, Chief Economist at CITIC Securities, stated that as the first year of the '15th Five-Year Plan,' the policy direction for 2026 is expected to be more proactive. The meeting will likely follow the overarching principle of 'seeking progress while maintaining stability' and form a systematic deployment focusing on consumption expansion, technological innovation, and fiscal-monetary coordination. 'Stabilizing growth and expectations in the short term is the core task; mid-term efforts will promote industrial and investment structure optimization, and long-term focus will be on building new productive forces and a new development model.'

After the Federal Reserve's interest rate decision, officials will make frequent public statements.

After the Federal Reserve's interest rate decision, officials will make frequent public statements. Next Friday, Chicago Fed President Austan Goolsbee will host a fireside chat at an economic outlook seminar. Cleveland Fed President Beth Hammack will deliver a speech at the University of Cincinnati. Patrick Harker, a voting member of the 2026 FOMC and president of the Philadelphia Fed, will speak on the economic outlook.

Speech by the Governor of the Bank of Japan: Continued Attention on Interest Rate Hike Expectations

In addition to the Federal Reserve, the movements of the Bank of Japan also warrant investors’ attention and vigilance. Previously, Kazuo Ueda, Governor of the Bank of Japan, issued the clearest signal yet regarding an interest rate hike. The bank will hold a monetary policy meeting on December 18-19, during which it may achieve its first interest rate increase since January this year. The policy interest rate is expected to rise from 0.5% to 0.75%, reaching its highest level in thirty years.

Although there are still two weeks before the Bank of Japan’s interest rate decision meeting, Governor Kazuo Ueda will appear at a public event next Tuesday. Any confirmation of interest rate hike expectations could potentially weigh on global markets.

Markets are concerned about a reversal of yen carry trades, but analysts believe the impact this time may be less severe than last year. Carry trade positions have decreased, expectations for a rate hike have been partially absorbed, and global market spillover risks remain manageable.

Expected next Tuesday! OpenAI to 'urgently release ahead of schedule' GPT 5.2 in response to Gemini 3.

In response to fierce competition from Google and Anthropic, OpenAI CEO Sam Altman announced this week that the company has entered a "red alert" status and plans to release the new model GPT-5.2 ahead of schedule. According to The Verge, OpenAI's GPT-5.2 is planned for release as early as December 9, significantly earlier than the original late-December schedule. Based on comparison charts posted by users on social media, GPT-5.2 outperforms Gemini 3 and Claude 4.5 across nearly all metrics.

Broadcom and Oracle Earnings: Continued Validation of AI Infrastructure Growth Momentum

Next week, Broadcom (AVGO) and Oracle (ORCL) will successively release their third-quarter earnings reports for the 2025 fiscal year. The two companies remain key windows for observing the investment momentum in AI infrastructure, though market focus differs for each.

As a core design partner for Google's TPU, Broadcom is expected by the market to significantly outperform consensus again. Citi believes that the surge in demand driven by Google’s opening up of its TPU to external users is the primary driver. Investors will focus on verifying the specific growth rate of AI business (Citi forecasts a 147% surge in AI sales for the new fiscal year) and subsequent guidance.

Oracle, on the other hand, is under scrutiny for whether its cloud infrastructure (OCI) growth can truly “take off” and how it plans to manage the significant capital expenditure pressures triggered by large contracts such as those with OpenAI. TD Cowen noted that if the progress of the 'Stargate' data center in Texas, developed in collaboration with OpenAI, proceeds smoothly, it will significantly alleviate capacity bottlenecks and accelerate OCI growth. BNP Paribas analyst Stefan Slowinski estimates that the company would only need to issue an additional $25-35 billion in debt to meet its AI construction funding needs. He emphasized that clear spending plans from management, along with a commitment to maintaining investment-grade ratings, would effectively eliminate recent concerns weighing on the stock price.

These two earnings reports will not only impact individual stocks but also provide critical validation for the next phase of trends in the AI hardware supply chain (Broadcom) and the cloud services sector (Oracle). Despite the non-peak earnings season, they will significantly influence the direction of the “AI narrative.”

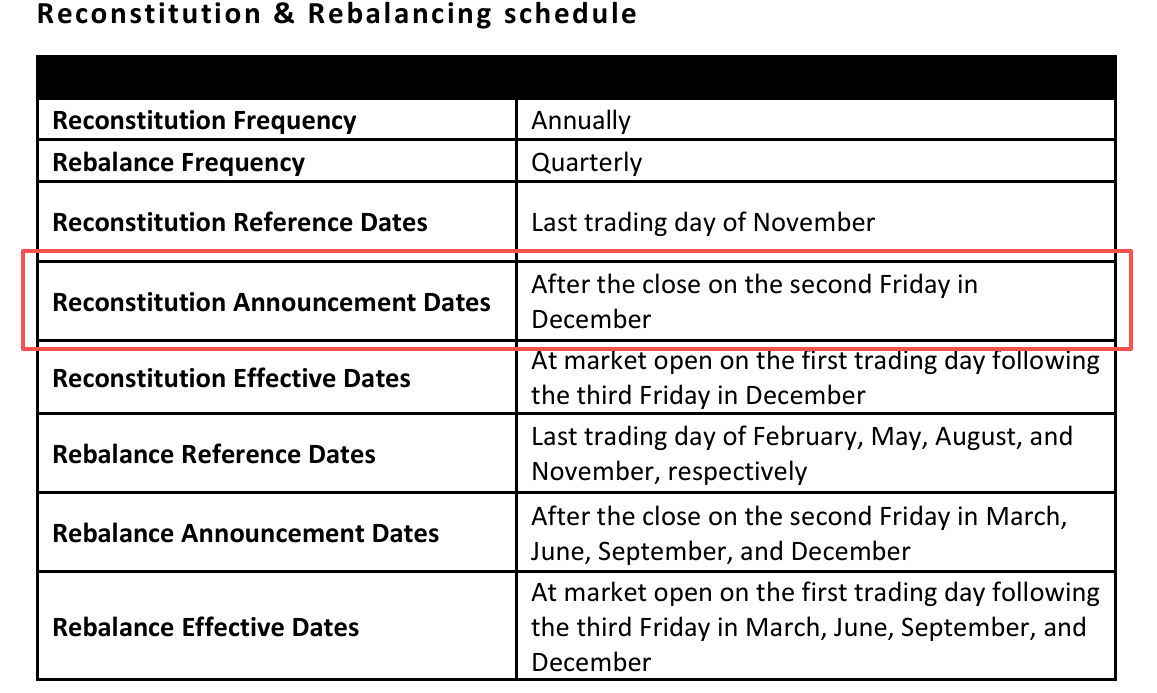

The Nasdaq 100 Index may announce its annual constituent adjustment after the market close next Friday.

According to the Nasdaq 100 Index compilation methodology, the results of the annual constituent adjustment will be announced after the market close on the second Friday of December each year, with the adjustment taking effect at the market open on the first trading day following the third Friday of December.

Key earnings calendar for the new week

[Related Reading]Cloud and Chips Converge! Oracle and Broadcom Earnings Releases Loom, Weekly Earnings Recap (Dec 8–Dec 12)

Monday (December 8)

Keywords: China's import and export data

In terms of economic data, investors may focus on China’s upcoming November import and export data, which mainly includes:

China's November year-on-year export growth rate

China's November year-on-year import growth rate

China's November trade balance (in billion yuan)

China's November trade balance in dollar terms (in billion USD)

Regarding financial events, attention can be paid to the Wall Street Journal CEO Council Summit, held in Washington and continuing until December 9. Attendees include Kevin Hassett, Director of the White House National Economic Council, who is considered a potential candidate for the next Federal Reserve Chair.

Additionally, Kazuo Ueda, Governor of the Bank of Japan, will deliver a speech at the Financial Times Global Boardroom conference in London, which runs from December 9 to December 11.

Google will host the 'Android XR Show' on Monday, expected to be a 30-minute live-streamed keynote showcasing advancements in AI glasses, headsets, and related ecosystems, particularly their integration with Gemini AI.

In terms of earnings reports, attention can be paid to after-hours trading in U.S. stocks. $Toll Brothers (TOL.US)$ and $Compass Minerals (CMP.US)$。

In terms of Hong Kong stock IPOs, $NOVOSENSE (02676.HK)$ 、 $ABLE DIGITAL (02687.HK)$ has officially gone public.

Tuesday (December 9th)

Keywords: GME earnings, OpenAI GPT 5.2 release

In terms of economic data, investors may focus on the U.S. JOLTs job openings data for October.

00:00 U.S. New York Fed 1-year inflation expectation for November

11:30 Reserve Bank of Australia announces interest rate decision

12:30 RBA Governor Michele Bullock holds press conference on monetary policy

19:00 U.S. NFIB Small Business Optimism Index for November

23:00 U.S. JOLTs Job Openings for October (in ten thousands)

Regarding earnings reports, $The Campbell's Co (CPB.US)$ 、 $AutoZone (AZO.US)$ will release earnings before the US stock market opens, $GameStop (GME.US)$ 、 $AeroVironment (AVAV.US)$ Companies such as will release their latest quarterly earnings reports after the US stock market closes.

In terms of financial events, according to The Verge, OpenAI's GPT-5.2 is planned for release as early as December 9 (Tuesday), significantly earlier than the originally scheduled late December.

Wednesday (December 10)

Keywords: China's November CPI year-on-year rate, Oracle/Synopsys earnings reports, JD.com Industrial gray market

In terms of economic data, China's November CPI year-on-year rate and November M2 money supply annual growth rate will be released. For U.S. stock-related economic data, attention can be paid to the Q3 labor cost index quarter-on-quarter rate.

1:00 EIA releases its monthly short-term energy outlook report;

2:00, U.S. 10-year Treasury bond auction as of December 9;

9:30, China's November CPI year-on-year rate;

21:30, U.S. Q3 labor cost index quarter-on-quarter rate;

23:30, U.S. EIA crude oil inventory for the week ending December 5

Regarding earnings reports, $Oracle (ORCL.US)$ The latest quarterly earnings will be released after the market close; $Synopsys (SNPS.US)$ will also release its earnings on the same day; last week, NVIDIA invested $2 billion in the company. Additionally, companies releasing earnings after market close include $Adobe (ADBE.US)$ . Companies releasing earnings before the market opens include $Chewy (CHWY.US)$ 、 $Hello Group (MOMO.US)$ 。

In terms of financial events, $CHINA VANKE (02202.HK)$ a domestic bond worth 2 billion yuan is seeking an extension. A bondholder meeting will be held on December 10 (Wednesday) to review matters related to the bond extension.

At 3:00 AM the next morning, the Federal Open Market Committee (FOMC) of the Federal Reserve will release its interest rate decision and Summary of Economic Projections, followed by a press conference on monetary policy held by Federal Reserve Chair Jerome Powell half an hour later.

In terms of new stock offerings, $JD INDUSTRIALS (07618.HK)$ After-hours trading in the gray market will commence today.

Thursday (December 11)

Keywords: Federal Reserve interest rate decision, Powell's speech, Broadcom earnings, unemployment claims data

In terms of economic data, attention can be paid to the number of initial jobless claims for the week ending December 6 in the United States, as well as trade balance data for September.

03:00 Federal Reserve interest rate decision (upper limit) as of December 10, United States

03:30 Federal Reserve Chair Jerome Powell holds a press conference on monetary policy

17:00 IEA releases its monthly oil market report;

To be determined, OPEC releases its monthly oil market report (generally published between 18:00-21:00 Beijing time);

At 21:30, the U.S. initial jobless claims for the week ending December 6 and the U.S. trade balance for September will be released;

At 23:00, the U.S. wholesale sales month-over-month rate for September will be announced.

In terms of earnings reports, optical communication concept stock $Ciena (CIEN.US)$ is scheduled to release its results before the U.S. stock market opens, while after the market close $Broadcom (AVGO.US)$ 、 $Costco (COST.US)$ 、 $Lululemon Athletica (LULU.US)$ Companies such as will release their earnings reports.

In terms of new stock offerings, $JD INDUSTRIALS (07618.HK)$Today is上市.

Friday (December 12)

Keywords: Statements by Federal Reserve officials

In terms of economic data, there will be no releases in China or the US. Investors may focus on relevant economic data from Europe and Canada.

At 15:00, the final month-over-month CPI for Germany in November;

At 15:00, the three-month GDP month-over-month rate for the UK in October, the month-over-month manufacturing output for the UK in October, the seasonally adjusted trade balance of goods for the UK in October, and the month-over-month industrial production for the UK in October;

At 15:45, the final month-over-month CPI for November in France will be released.

At 21:30, the month-over-month wholesale sales data for October in Canada will be announced.

On the economic events front, following the release of the December interest rate decision, Federal Reserve officials are scheduled to make several appearances on Friday:

At 21:00, Harker, the 2026 FOMC voting member and President of the Federal Reserve Bank of Philadelphia, will deliver a speech on the economic outlook.

At 21:30, Harker, the 2026 FOMC voting member and President of the Federal Reserve Bank of Cleveland, will deliver remarks.

At 23:35, Goolsbee, President of the Chicago Federal Reserve, will participate in a moderated discussion ahead of the 39th Annual Economic Outlook Symposium hosted by the Chicago Fed.

Additionally, the White House will convene an Artificial Intelligence Supply Chain Summit on December 12 with allies such as South Korea, the UAE, and Australia, where agreements are expected to be signed in areas including energy, critical minerals, advanced manufacturing, semiconductors, AI infrastructure, and transportation logistics.

Finally, $NASDAQ 100 Index (.NDX.US)$ The annual index composition adjustment may be announced after the market closes on Friday.

Stay ahead with the latest financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with the latest financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Wishing all fellow investors a successful new week ahead!

Editor/Rocky