The Japanese government bond market is bracing for another challenging year as investors face the largest net increase in supply in over a decade.

This means private investors will need to absorb more bond issuance, potentially increasing the Hisao Sanae government’s interest expenses – a government that last year unveiled a record budget to support its massive stimulus program.

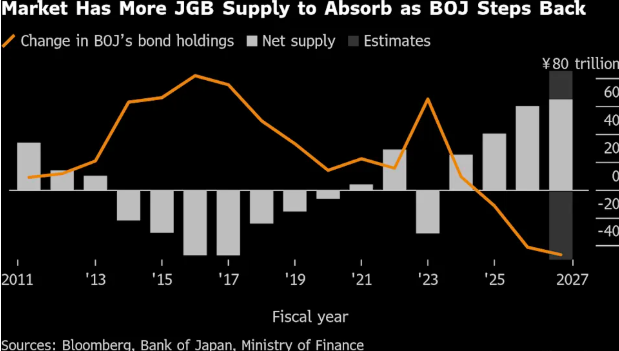

The Japanese government bond market is bracing for another challenging year as investors face the largest net increase in supply in over a decade.

According to industry estimates, net supply of the country's sovereign bonds—the worst-performing asset among major global bond markets last year—is projected to rise by 8% to approximately 65 trillion yen ($415 billion) in the new fiscal year starting in April. The data accounts for the Bank of Japan’s reduction in bond purchases and government debt repayments.

According to industry estimates, net supply of the country's sovereign bonds—the worst-performing asset among major global bond markets last year—is projected to rise by 8% to approximately 65 trillion yen ($415 billion) in the new fiscal year starting in April. The data accounts for the Bank of Japan’s reduction in bond purchases and government debt repayments.

This means that private investors will have to absorb more bond issuance, potentially raising the interest expenses of the Masako Takagi administration, which last year unveiled a record budget to support a large-scale stimulus plan.

Akio Kato, senior manager of the Strategic Research and Investment Department at Mitsubishi UFJ Asset Management in Tokyo, stated, “The supply and demand dynamics in the Japanese bond market have deteriorated to the point where the government may eventually need to adjust issuance volumes on a quarterly basis.”

Kato revealed that he is currently maintaining a bearish stance on Japanese bonds by keeping the duration of his portfolio below benchmark levels.

After adjusting for currency effects, Japanese government bonds fell by more than 6% last year, performing the worst among over 40 sovereign markets tracked by the industry, as the Bank of Japan’s gradual tightening measures failed to curb stubborn inflation. In contrast, U.S. Treasury bonds rose by 6.3%, while German bonds declined by 1.6% during the same period.

The main driver behind the increase in net supply of Japanese bonds is the slowdown in the Bank of Japan’s bond purchasing pace. The Bank of Japan plans to reduce its monthly total bond purchases by more than a quarter to approximately 2.1 trillion yen in the coming year. Data shows that this would result in its holdings decreasing by 46.5 trillion yen in the next fiscal year, compared to a reduction of 41.1 trillion yen this fiscal year.

Since the Bank of Japan began easing its control over the yield curve, local banks and pension funds in Japan have been the primary drivers of bond purchases. Since April 2023, their net purchases (net of redemptions) have exceeded 30 trillion yen cumulatively. However, concerns remain that this figure may still be insufficient amid the surge in net supply.

This week, the benchmark$Japan 10-Year Treasury Notes Yield (JP10Y.BD)$has further climbed to 2.13%, the highest level since 1999.

Miki Den, Senior Interest Rate Strategist at SMBC Nikko Securities, stated, 'We believe the fair value of Japan's 10-year government bond yield is currently around 2.2%-2.3%, and it should not be an issue for yields to rise to that level.'

The renewed pressure on Japanese bond yields also stems from Bank of Japan Governor Kazuo Ueda's hints this week that the central bank will raise interest rates further following last month’s increase of the policy rate to a 30-year high. Overnight index swaps indicate that the Bank of Japan may raise interest rates twice more before the end of 2026.

In line with this, the rise in yields, particularly for short-term bonds, also suggests that Japan’s Ministry of Finance may further adjust its issuance plans. Excluding short-term government bonds, the supply of medium- to long-term bonds in Japan is expected to slightly decrease to approximately 133 trillion yen in the 12 months ending March 2027. The issuance of 2-year and 5-year bonds will increase, while the issuance of bonds with maturities exceeding 10 years will decrease. The Ministry of Finance will issue 30-year bonds on Thursday.

“With the reduction in long-term bond supply and the increase in short-term bonds, the yield curve may flatten,” said Tadashi Matsukawa, Head of Bond Investments at PineBridge Investments Japan Co. in Tokyo. “Given the persistent strength in underlying inflation, the Bank of Japan is expected to continue raising interest rates to reach a neutral rate level.”

Editor/Melody