Entering 2026, global capital markets have reached a critical juncture. If the past few years were characterized by a 'grand reshuffle of macroeconomic expectations,' this year resembles more of a 'year of tangible validation'—Wall Street has reached a consensus: the broader economic trend is positive, but expecting easy gains is unrealistic; market volatility will only increase.

Leading institutions such as Goldman Sachs and Morgan Stanley have issued optimistic forecasts, but the more seemingly 'perfect' the market conditions, the more cautious one should be. For seasoned investors, 2026 is not the year to blindly believe in 'buy and hold.' Genuine profit opportunities lie in assets with 'realizable earnings' and 'policy tailwinds,' as market bifurcation becomes increasingly evident, making indiscriminate purchases prone to losses.

I. The Macro Environment: Economic Resilience, but Markets 'Fear Mistakes More Than Missing Out'

The keyword for this year's macroeconomic situation is resilience. The previously heated debate about an 'economic recession' has now largely subsided. Goldman Sachs forecasts that U.S. GDP growth could reach 2.6%, implying the economy has transitioned from a soft landingstandstill directly into an 'acceleration phase.' This shift is underpinned by two key drivers:

First, AI has truly become an 'economic engine.' Investment in AI now rivals traditional consumption-driven growth in its contribution to GDP. Second, the 'dual dividend' of policy and monetary easing—the implementation of the One Big Bold Bill Act (OBBBA) and relaxed final rules of Basel III—are expected to release $160 billion to $200 billion in idle capital into the banking system. This capital will likely flow into stock buybacks or lending, further fueling the market.

First, AI has truly become an 'economic engine.' Investment in AI now rivals traditional consumption-driven growth in its contribution to GDP. Second, the 'dual dividend' of policy and monetary easing—the implementation of the One Big Bold Bill Act (OBBBA) and relaxed final rules of Basel III—are expected to release $160 billion to $200 billion in idle capital into the banking system. This capital will likely flow into stock buybacks or lending, further fueling the market.

Interestingly, the market now exhibits 'rational exuberance.' On one hand, FactSet forecasts S&P 500 earnings growth at 15%, and Morgan Stanley projects a year-end target of 7800 points, indicating clear upside potential. On the other hand, valuations are nearing historical highs, and the market has zero tolerance for 'imperfections'—any earnings miss or policy uncertainty could trigger a pullback. In essence, investors are 'fearful of missing out on this rally but even more fearful of picking the wrong stocks,' a sentiment of 'rational FOMO' that will persist throughout the year.

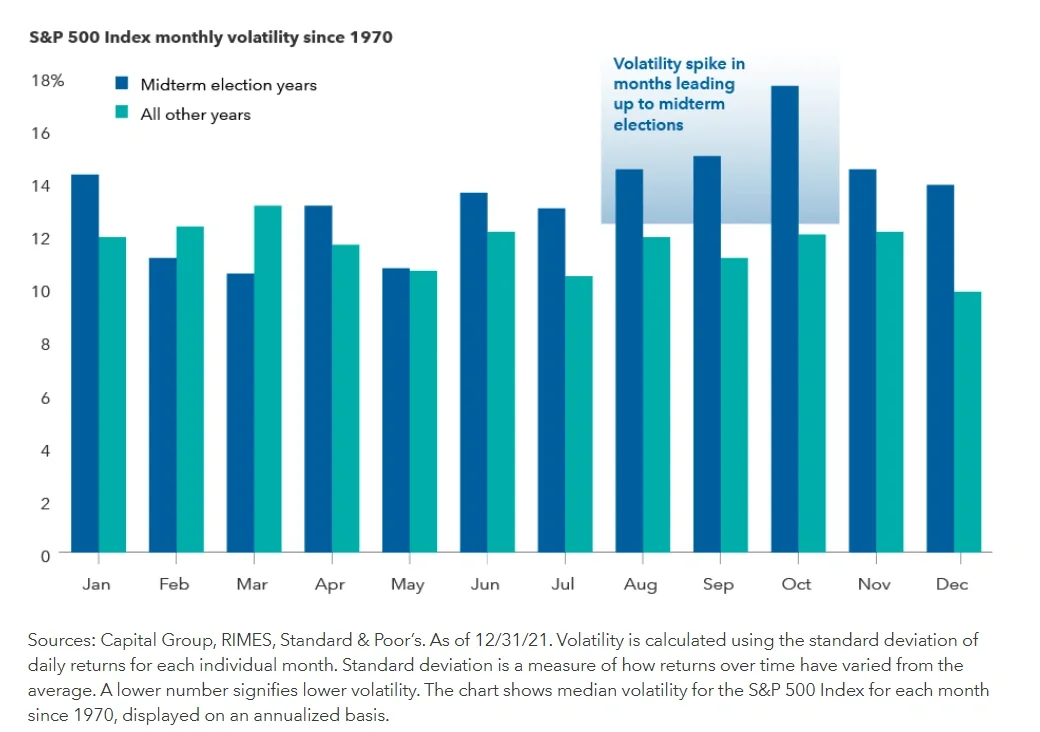

Of course, risks cannot be ignored. Two 'Swords of Damocles' loom over 2026: the leadership transition at the Federal Reserve and the U.S. midterm elections. Historical experience shows that market volatility tends to rise during midterm election years, especially in the second and third quarters. A shift in Congressional power dynamics could introduce policy uncertainty, potentially causing market chaos. These two junctures require close monitoring.

Thus, the investment logic for 2026 must evolve: stop listening to 'pie-in-the-sky stories' and focus on 'tangible cash flows' and 'concrete policy benefits.' These are the keys to navigating volatility.

II. Can MAG7 Continue to Lead? The Answer: They Must Serve as the 'Anchor of Diversification'

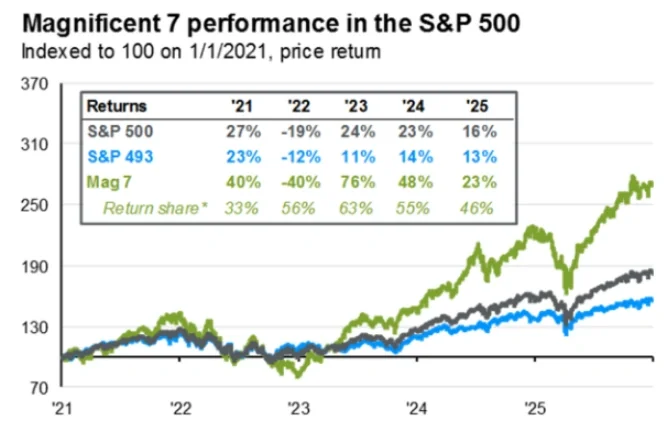

When discussing U.S. equities in 2026, MAG7 is unavoidable. In 2025, the S&P 500 rose 16%, the S&P 493 gained 13%, while MAG7 surged 23%, marking its third consecutive year of outperformance against the broader market.

Looking specifically at individual stock performances: $Alphabet-C (GOOG.US)$ up 65%, $NVIDIA (NVDA.US)$ up 36%, $Tesla (TSLA.US)$ up 16%, $Microsoft (MSFT.US)$ up 13%, $Apple (AAPL.US)$ up 11%, $Meta Platforms (META.US)$ up 9%, $Amazon (AMZN.US)$ up 3%. Aside from Google and NVIDIA, the gains for the other stocks are not particularly extreme. This is something to keep in mind when planning your investment strategy—avoid blindly chasing high performers.

Why will MAG7 still be important in 2026? It’s not because they are 'large-cap stocks,' but rather because they have become the 'cornerstone' of the S&P 500:

With a total market capitalization of approximately $21.55 trillion, accounting for 35.45% of the total market capitalization of the S&P 500;

Contributing approximately 25% of the S&P 500's profits.

This implies that the market’s valuation premium for MAG7 is justified — investors are not only paying for current profitability but also for their sustainability, industry position, and the confidence in maintaining leadership.

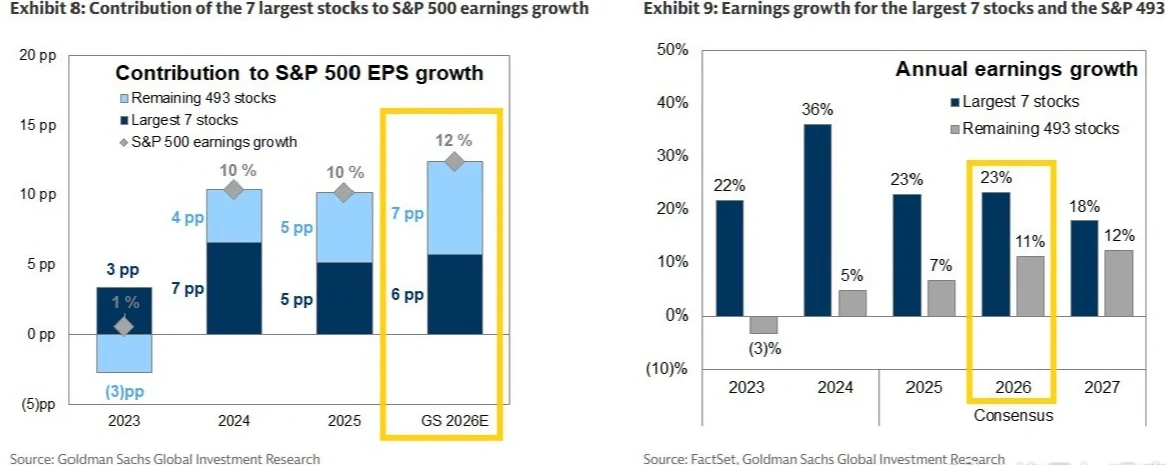

From a growth perspective, the premium is not 'overvalued.' Goldman Sachs forecasts a 12% increase in S&P 500 earnings per share by 2026, with MAG7 contributing 6 percentage points and the remaining 493 stocks contributing 7 percentage points. In other words, MAG7 alone accounts for nearly half of the growth contribution (46%).

The conclusion is straightforward: even though valuations are currently high, MAG7 can still deliver 'excess growth' in the short term. In the long run, the 'stronger gets stronger' logic will allow these leading platforms to maintain higher and more stable growth rates. Therefore, by 2026, MAG7 will remain the 'anchor' of investment portfolios — holding them minimizes risks while capturing structural dividends, ensuring more stable compound growth.

However, there is differentiation within MAG7. The overall forward P/E ratio is about 26x (excluding Tesla), and each company has its own logic and highlights, requiring targeted positioning by 2026:

Apple: Driving upgrades in high-end products through device-based AI and ecosystem experience, while its services business generates steady cash flow and profits, making it a 'steady yet progressive' choice;

Microsoft: Azure + Copilot will capture significant corporate AI budgets, but the market will focus on whether 'investment translates into profit,' with key metrics being cRPO/bookings, capital expenditure efficiency in converting to gross margins and free cash flow;

Amazon: AWS is expected to re-accelerate, driven by growing AI demand and improved delivery capabilities, complemented by cost reductions from custom chips, with the need to verify if high capital expenditures yield returns;

Google: AI must be integrated into search without undermining profitability, while ensuring AI-related businesses grow and generate profits;

Meta: AI-driven advertising efficiency will continue to improve, but risks lie in whether 'increased spending and capital expenditure compress profit margins.'

NVIDIA: Relying on the scaling of Blackwell and Rubin, the key is whether data center growth and gross margin can sustain platform-level premium.

Tesla: The key lies in whether FSD/autonomous ride-hailing can scale to support current valuations; the automotive business serves as the cash flow foundation, while energy storage represents the true growth engine.

Three, want to earn excess returns? Keep a close eye on these three 'under-the-radar sectors.'

The 'alpha returns' (excess returns) for 2026 are unlikely to be found in popular stocks but instead hidden in overlooked corners. These three sectors merit significant attention:

Space Economy: SpaceX IPO ignites the industry.

Reports suggest that SpaceX will go public in 2026, an event that would undoubtedly be a 'mega-event' in the capital markets of this century. Once listed, the entire space industry will undergo revaluation, with sub-sectors such as satellite communications, launch services, and orbital infrastructure becoming market focal points, potentially giving rise to a group of standout stocks.

Digital Assets: Officially 'entering institutional view.'

Regulatory frameworks for digital assets are becoming increasingly clear, and institutional infrastructures such as ETFs and tokenization have matured. Many institutions predict that 2026 will be the year when digital assets achieve true 'institutional adoption'—no longer a niche player's game, more institutional capital will enter the sector, enhancing its certainty.

Biotechnology and Pharmaceuticals: Dual Drivers of M&A and New Products.

Mergers and acquisitions in the pharmaceutical industry will be particularly active in 2026, primarily due to large pharmaceutical companies facing the 'patent cliff' (expiration of many blockbuster drug patents), holding substantial cash reserves, and benefiting from low interest rates, which will lead to aggressive pipeline replenishment through acquisitions. Additionally, the obesity treatment sector remains highly promising, with oral GLP-1 receptor agonists (such as Wegovy pills) set to hit the market in January, further expanding the market size and making related companies worth watching.

Final Summary

In 2026, investors should not be swayed by index fluctuations, as volatility is inherently a normal state of the market. It is recommended that: the core portfolio be locked into 'certainty assets' such as MAG7 to ensure a solid foundation; simultaneously, flexible allocations should be made in the three sectors of space economy, digital assets, and biotechnology to achieve excess returns; most importantly, during the turbulent period of the midterm election year, if high-quality assets are undervalued, seize the opportunity to buy at the bottom decisively—opportunities often lie within volatility.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Editor/Lee