The 'Sanae Takichi trade' ignites a surge in long-end Japanese government bond yields amid fiscal concerns and weak auction demand, triggering a sell-off in Japanese bonds that sends shockwaves through global bond and equity markets.

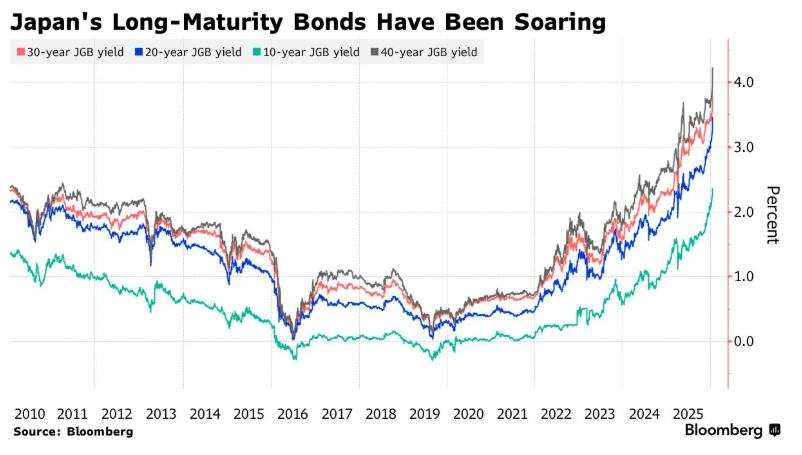

On Tuesday, Japan's sovereign bond market experienced an unprecedented large-scale sell-off, with long-term government bond yields surging to a record high.$Japan 40-Year Treasury Notes Yield (JP40Y.BD)$On Tuesday, it unprecedentedly surged past the 4% threshold, reaching its highest level since the issuance of this bond in 2007, and has been repeatedly hitting record highs recently. The latest round of the Japanese government bond collapse has spread comprehensively across global financial markets, with some senior Wall Street analysts even expressing concerns that the wave of Japanese bond sell-offs could trigger a collapse in global stock and bond markets following the plunge in Japanese bonds, potentially leading to a 'Black Monday' super crash across global equities, bonds, and currencies akin to early August 2024. As a result, calls have emerged for the Bank of Japan to immediately initiate emergency bond-buying operations to calm the markets.

The trigger for this massive sell-off in the Japanese government bond market was the Sanae Takamichi administration's promise to cut food consumption taxes to win the House of Representatives election without specifying the funding source, which sharply heightened concerns in the financial markets about Japan’s fiscal discipline and government spending expectations. On Tuesday, during a highly anticipated and critical Japanese government bond auction,$Japan 20-Year Treasury Notes Yield (JP20Y.BD)$the auction saw weak demand, ultimately driving$Japan 10-Year Treasury Notes Yield (JP10Y.BD)$、$Japan 20-Year Treasury Notes Yield (JP20Y.BD)$、$Japan 30-Year Treasury Notes Yield (JP30Y.BD)$and$Japan 40-Year Treasury Notes Yield (JP40Y.BD)$a rapid surge amid expectations of the Takamichi administration’s substantial fiscal spending. Among these,$Japan 30-Year Treasury Notes Yield (JP30Y.BD)$it once rose by 26.5 basis points to a record high of 3.875%,$Japan 40-Year Treasury Notes Yield (JP40Y.BD)$and at one point climbed 27 basis points to 4.215%, continuing to set new historical records.

Expectations of interest rate hikes by the Bank of Japan have continued to rise since 2025, compounded by the Sanae Takamichi administration's extraordinarily large stimulus plan at the level of ten trillion yen, leading to fearsome 'term premium' effects spreading from the United States to Japan and sweeping across Japan’s stock, bond, and currency markets. As a result, long-term Japanese government bond yields have collectively surged since the beginning of the year, while the yen exchange rate has continued to depreciate.

Expectations of interest rate hikes by the Bank of Japan have continued to rise since 2025, compounded by the Sanae Takamichi administration's extraordinarily large stimulus plan at the level of ten trillion yen, leading to fearsome 'term premium' effects spreading from the United States to Japan and sweeping across Japan’s stock, bond, and currency markets. As a result, long-term Japanese government bond yields have collectively surged since the beginning of the year, while the yen exchange rate has continued to depreciate.

The spillover effects from the rare sell-off in Japan's long-term government bond yields are spreading to global stock and bond markets. Referred to as the 'anchor of global asset pricing,'$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$rose by 1.55%; futures for the three major U.S. stock indexes fell accordingly,$E-mini Dow Futures (MAR6) (YMmain.US)$Down 1.49%,$E-mini S&P 500 Futures (MAR6) (ESmain.US)$fell by 1.59%,$E-mini NASDAQ 100 Futures (MAR6) (NQmain.US)$with declines of 1.88%. European equity index futures indicate that the downturn in European markets will continue after Monday saw the worst single-day performance for European stocks since mid-November of the previous year.

The ongoing interest rate hike cycle and the prolonged dominance of Takamichi’s expansionary fiscal policy are driving yields on Japanese government bonds with maturities of 10 years or more to continuously reach new record highs due to 'term premium,' until the Bank of Japan signals a pause in rate hikes. It is well known that Japan holds vast overseas assets, so if yields on long-term Japanese government bonds surge in the short term, it may trigger Japanese overseas investment institutions to sell off highly liquid assets such as U.S. stocks, U.S. bonds, and European bonds to cover huge losses caused by the plunge in Japanese bonds. Alternatively, it could prompt a massive inflow of overseas funds back to Japan to embrace high-yield yen assets, potentially causing a global stock, bond, and currency crash akin to the 'Black Monday' event in August 2024—a point worthy of investors’ vigilance.

With trillions of yen in consumption tax cuts under the Takamichi administration, fewer and fewer investors dare to catch the falling knife of Japanese bonds.

As Japan approaches its general election, growing concerns over deteriorating fiscal discipline are rapidly spreading in the Japanese government bond market and across global stock and bond markets. Global investors are showing extreme caution in response to the possibility of substantial unfunded tax cuts promised by the Japanese government.

Japanese Prime Minister Sanae Takamichi announced at a press conference on the 19th local time that she will dissolve the House of Representatives on January 23 and hold a House of Representatives election on February 8. Takamichi stated that preparations will begin to cancel the two-year consumption tax on food and emphasized that the funding issue for the consumption tax reduction is still under consideration.

Due to the weak results of the day's bond auction, which exacerbated concerns about Takamichi’s revitalization plan and tax cuts, market sentiment plummeted sharply—selling pressure quickly formed a vicious cycle. 'What initially looked like routine 20-year bond auctions rapidly evolved into a collapse, after which everyone was glued to their screens,' said Shinji Kunibe, Chief Portfolio Manager of the Global Fixed Income Team at Sumitomo Mitsui DS Asset Management.

In Japan, some economists have noted that if the policy of canceling the two-year consumption tax on food is smoothly implemented under Sanae Takamichi’s leadership, it is expected to generate approximately five trillion yen in annual tax cuts. The core factor unsettling the market lies in the fact that the Japanese government has not disclosed specific funding sources to fill this enormous fiscal gap. Under these conditions, combined with the suppression from the Bank of Japan’s rate hike expectations and the weak 20-year JGB auction, the Japanese government bond market is facing increasingly severe selling pressure. The 'falling knife' of long-term Japanese bonds, which no investor dares to catch, continues to plummet.

What the market cares most about is not the tax-cutting policies of the Sanae Takaichi government per se, but a more critical issue: where will the funds come from to cover the approximately 5 trillion yen annual shortfall resulting from the reduction in food consumption tax. In the absence of a clear financing plan (tax increases, spending cuts, or other verifiable arrangements), investors have begun to reassess the tail risks associated with Japan's fiscal discipline and sovereign risk, leading to a significant rise in the 'term premium' in Japan’s government bond market.

More troubling is that fiscal concerns are not occurring in an environment where expectations of interest rate hikes by the Bank of Japan are receding. Therefore, without funding support for fiscal commitments, investors are unwilling to bear duration risk, and the disappearance of buying pressure has forced yields to seek new marginal buyers at higher levels. Views from Wall Street institutions generally suggest that, for some time to come, long-term Japanese government bonds will experience sharp volatility around two main themes: whether the reduction in food consumption tax will be formally included in election pledges, and whether the Japanese government will provide an executable and quantifiable financing path.

Wall Street analysts loudly proclaim that the plunge in Japan’s long-term government bonds highlights immense policy challenges.

As Japan's sovereign bonds experienced a historically rare 'super collapse,'$Japan 40-Year Treasury Notes Yield (JP40Y.BD)$This marked the first time it soared above 4%. Some senior Wall Street analysts noted that this might prompt the Bank of Japan to act more swiftly, possibly even initiating emergency bond-buying operations immediately to stabilize the market.

The policy of reducing food taxes proposed by the Japanese government during the election underscores widespread concerns about fiscal expenditures and inflation rates, and also draws greater attention to the risks faced by the Japanese market as it gradually phases out years of ultra-loose monetary policy. Some market observers predict that continued expansion of fiscal deficits and inflation rates will further complicate Japan's economic situation, with some strategists forecasting that if the sell-off in long-term Japanese government bonds intensifies, the Bank of Japan may intervene and purchase Japanese government bond assets.

They noted that the proposal to reduce food taxes in the ruling party's election platform highlights broader financial market concerns about fiscal spending and inflation. This makes the risk of selloffs in Japan's market more prominent as the country gradually exits years of extremely accommodative monetary policy. Such selloff risks are highly likely to continue spilling over into global equity and bond markets.

Below are the immediate comments from some senior financial market observers:

Prashant Newnaha, Senior Rates Strategist for Asia-Pacific at TD Securities based in Singapore:

“Historically, successive Japanese governments have underestimated the risks of rising interest rates and yen depreciation that could result from expansionary policies. The market is pricing in these risks through higher neutral rates and a higher term premium, leaving the Japanese government bond market extremely short of buyers in the short term.”

“But make no mistake about the focus. The market is watching reflationary policies. With Trump seen as ‘fueling’ the market ahead of midterm elections, and the possibility of the Takaichi administration gaining control of the House, expansionary fiscal policy means there is still room for yields to continue rising. This is why the 40-year Japanese government bond yield may expand further above 4% in the coming months.”

Simon Ballard, Chief Economist at First Abu Dhabi Bank:

"The market continues to penalize this policy mix – most evidently in the exchange rate and long-term bonds – while effectively forcing investors to pivot towards value or defensive equity assets. The prevailing view remains that the Bank of Japan's policies are still too accommodative relative to nominal growth and fiscal deficits."

There are ongoing challenges and institutional inertia regarding the normalization of Japanese government bonds (we need to see four rate hikes, whereas the market currently prices in only two). With inflation at 3% and wage growth at 5%, the supplementary budget from the Saeko Takagi government and expectations of further fiscal deficits in 2026 have added complexity to the situation.

Rinto Maruyama, FX and Rates Strategist at SMBC Nikko Securities:

"Takagi was very firm in her press conference yesterday. The market had previously believed she would take bond market concerns into account. The supplementary budget is modest and has been viewed as a signal of restraint."

"Bond market participants now widely expect her to advance her preferred policies after the election. Unlike the UK gilt market during the 'Truss Shock,' Japan’s CDS has not risen significantly. There are also no highly leveraged players being forced to unwind their positions."

"Nevertheless, yields have surged rapidly under spending plans without clear funding sources. This is a major shock – arguably significant enough to warrant its own name. Unless campaign pledges become clearer, sentiment is unlikely to improve. The market does not see how the government will precisely fund the proposed cut in food consumption tax."

Shinji Kunibe, Chief Portfolio Manager of the Global Fixed Income Team at Sumitomo Mitsui DS Asset Management:

"Everyone was glued to their screens because what seemed like a routine 20-year JGB auction quickly turned into a rout," he said. "This appears to be a warning from the market about fiscal expansion, and the lack of any positive comments from the government side is unsettling. It’s hard to say whether we can make it to the weekend without further significant volatility."

Katsutoshi Inadome, Senior Strategist at Sumitomo Mitsui Trust Asset Management:

The bond market was confused and surprised by the announcement from Koichi that he would commit to cutting consumption taxes without specifying the funding source. This has led to an uncontrolled rise in long-term yields.

Kazuhiro Sasaki, Head of Research at Phillip Securities Japan Ltd.:

The sharp rise in Japanese government bond yields is also becoming a negative factor for global stock markets. Of course, government spending could be beneficial to the economy, but if fiscal burdens increase, that becomes problematic.

Moreover, as the yen continues to weaken, market concerns are growing that the Bank of Japan may be forced to raise interest rates faster than expected. Such tensions will begin to weigh on global stock and bond markets.

Mansoor Mohi-Uddin, Chief Macro Strategist at Bank of Singapore:

This is the 'Koichi trade' at work. The rise in Japanese government bond yields, combined with renewed concerns about tariffs in the US and Europe, could lead to further increases in global sovereign bond yields. Prior to the election of the new prime minister, Japan's extremely high government debt was already quite significant, but it did not lead to such dramatic yield volatility.

Tadashi Matsukawa, Head of Bond Investments at PineBridge Investments Japan Co.:

As various political parties propose cutting consumption taxes, there is strong concern about the deterioration of fiscal conditions. Although the issuance of super-long-term bonds decreased somewhat last year, the supply-demand situation has not improved.

After interest rates have risen to this extent, calls for emergency operations by the Bank of Japan and for the Ministry of Finance to implement buybacks may intensify.

Carlos Casanova, Senior Economist for Asia at Union Bancaire Privee based in Hong Kong:

If the Koichi municipal government secures a stronger majority and adopts significantly looser fiscal policies, potential impacts include yen weakening and rising import-driven inflation, which could disrupt the normalization process. However, this might ultimately lead to higher terminal interest rates. The overall impact on equities could be positive due to increased yen-denominated earnings from tax cuts and currency depreciation, benefiting large exporters. Additionally, higher deposit rates may support domestic consumption.

Gareth Berry, strategist at Macquarie Bank in Singapore:

If the sell-off deepens further, the Bank of Japan may intervene to purchase Japanese government bonds. Governor Kazuo Ueda has been extremely reluctant to use the tool devised by his predecessor Haruhiko Kuroda, but he may soon have no choice. If the sell-off continues, especially if it spreads globally, we may see the Bank of Japan bring it back into use—potentially as early as tomorrow morning during routine policy operations.

Homin Lee, senior macro strategist at Lombard Odier Singapore:

The primary trigger for volatility is likely the escalating tit-for-tat across the Atlantic. However, the strong fiscal signals from the Koichi municipal government will certainly amplify tensions.

Until authorities provide clear signals about raising interest rates or defending the exchange rate, market participants may drive momentum trading with a 'double short' strategy targeting both Japanese government bonds and the yen. However, we suspect that if this trade persists, concerns over sudden reversals and unwinding may grow due to the political dimension embedded in bearish market narratives.

Gerald Gan, chief investment officer at Reed Capital Partners in Singapore:

I believe recent movements have largely been driven by forced selling, as evidenced by the evolution of technical price momentum. Nevertheless, weaker demand stemming from shifting sentiment, particularly concerns over poor government fiscal discipline, may keep long-term Japanese government bond yields at historically elevated levels.

If Prime Minister Sanae Takachi secures a stronger mandate with more seats in an upcoming snap election, the only sustainable way to keep long-term bond yields under control will be to articulate a credible and robust economic growth narrative. I anticipate this latest potential growth narrative will extend through 2026 and gain greater recognition. Therefore, current yield levels appear relatively attractive for investment.

Editor/Melody