①How will Kevin Warsh's policy mix of "interest rate cuts alongside balance sheet reduction" affect the capital flow landscape in emerging markets?

②Within the context of a moderate appreciation channel for the RMB, which Hong Kong stock sub-sectors are most likely to achieve dual benefits of "profit recovery and valuation enhancement"?

The formal nomination of former Federal Reserve Governor Kevin Warsh by U.S. President Trump for the position of Federal Reserve Chair has drawn market attention. According to GF Securities, the global dollar cycle is currently in a phase of peaking and retreating, with the RMB entering a moderate appreciation channel. Coupled with foreign capital inflows and valuation recovery, Hong Kong stocks are in a relatively advantageous repricing window.

The brokerage recommends that investors seize the triple convergence opportunities of southbound capital inflows, valuation discounts, and improved exchange rate environment. Priority should be given to deploying leading technology companies, internet platforms, energy resources, and financial sectors with both dividend capacity and growth attributes. Investors should remain vigilant about the risks of a simultaneous downturn in stocks, bonds, and currencies, as well as geopolitical conflicts' impact on exchange rate stability.

The brokerage recommends that investors seize the triple convergence opportunities of southbound capital inflows, valuation discounts, and improved exchange rate environment. Priority should be given to deploying leading technology companies, internet platforms, energy resources, and financial sectors with both dividend capacity and growth attributes. Investors should remain vigilant about the risks of a simultaneous downturn in stocks, bonds, and currencies, as well as geopolitical conflicts' impact on exchange rate stability.

Fed Transition Reshapes Global Asset Pricing System

Warsh Policy Expectations and Short-Term USD Trends

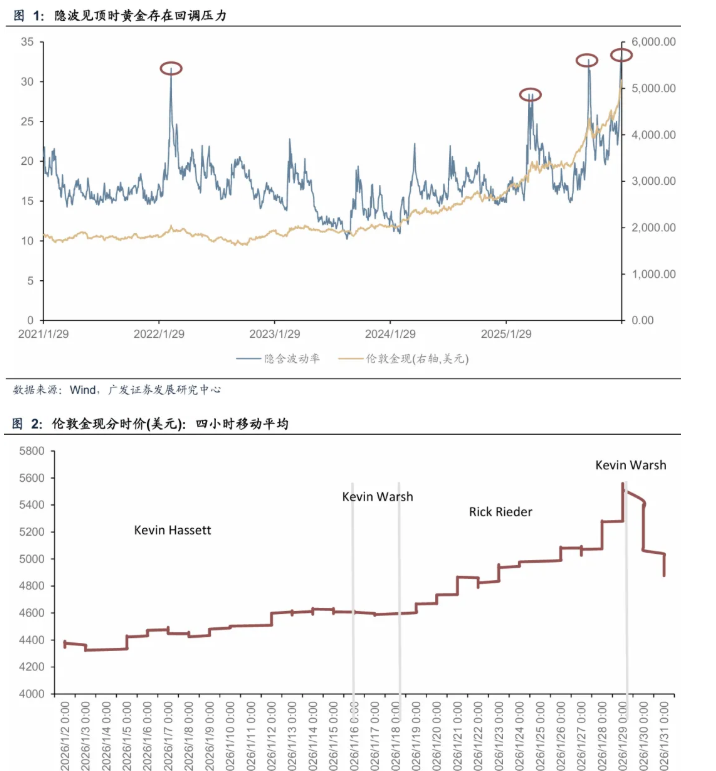

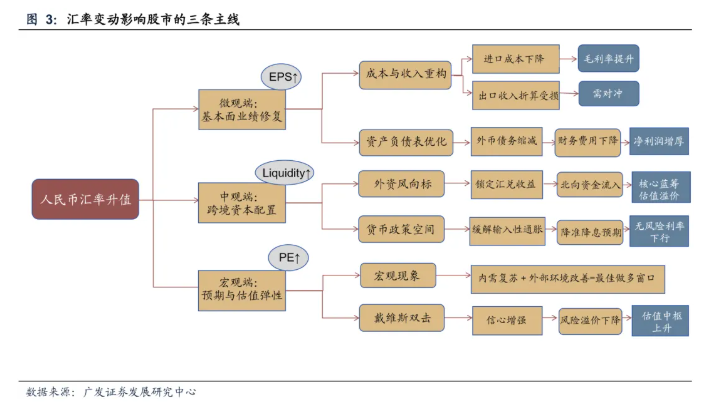

In January 2026, the probability of Kevin Warsh being nominated as Federal Reserve Chair rose to the top spot, prompting a swift market reaction where London gold retreated by approximately $30. Warsh’s most distinctive policy mix involves "simultaneous interest rate cuts and balance sheet reduction," reflecting a delicate balance between political demands and market credibility: on one hand, moderately cutting rates to address the White House’s desire to lower financing costs, while advocating for balance sheet reduction to restore the Fed’s credibility and inflation anchor.

From a market impact perspective, Warsh is seen as the "path of least resistance" between politics and the market, with his stance on maintaining central bank independence further solidifying global capital’s willingness to hold the dollar. In the short term, this policy expectation will support dollar recovery and drive steepening in the U.S. Treasury yield curve, pressuring precious metal prices. However, it should be noted that Warsh’s policies may slow the rate of dollar depreciation rather than fundamentally reversing its trend, with medium- to long-term impacts constrained by structural issues in U.S. debt.

Dollar Cycle and Shifts in Global Asset Allocation

Since the peak of the dollar index at the end of 2022, the global dollar cycle has shown characteristics of fluctuating downward trends. At the beginning of 2026, influenced by factors such as the rise of de-dollarization narratives, strengthening fundamentals of non-dollar currencies, policy fluctuations under the Trump administration, and accumulating geopolitical risks,$USD (USDindex.FX)$On January 27, it hit a four-month low of 95.77, forming a stark contrast.$S&P 500 Index (.SPX.US)$Reaching a new historical high in mid-January 2026, presenting a mirror image of 'new lows for the US dollar and new highs for the US stock market.'

This phenomenon reveals a profound evolution in the logic of global asset pricing: the impact of the US dollar cycle on global asset valuation is shifting from a single liquidity-driven 'tidal effect' to rational choices based on 'relative asset endowments.' Starting from 2025, non-US markets have outperformed US stocks in terms of returns in certain phases, indicating that global capital is initiating a dynamic rebalancing process from US equities to non-US assets. In this context, emerging markets, including China, especially the undervalued Hong Kong stock market, are entering a favorable window period for relative return recovery.

Exchange Rate Mechanism and Linkage with the Hong Kong Stock Market

Three Transmission Channels Through Which Exchange Rates Affect Equity Assets

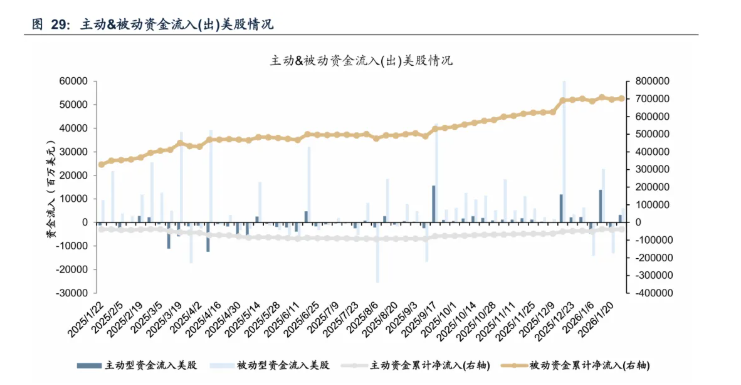

As a key link between macroeconomic conditions and microeconomic entities, exchange rates influence equity markets such as Hong Kong stocks through the following three core channels:

Corporate Cost-Benefit Analysis and Profit Elasticity: The Hong Kong dollar is pegged to the US dollar, while most companies listed on the Hong Kong Stock Exchange are Chinese enterprises whose balance sheets are significantly affected by the Renminbi exchange rate. Renminbi appreciation reduces import costs denominated in foreign currencies and improves foreign exchange gains or losses for companies with US dollar liabilities, directly boosting profit margins for related industries. For example, sectors with high US dollar debt, such as aviation, papermaking, and basic chemicals, tend to perform well during periods of Renminbi appreciation; export-oriented enterprises, however, face certain pressures related to currency conversion and competitiveness.

Capital Flows and Asset Pricing Effects: Exchange rate trends serve as a 'barometer' for both southbound and foreign capital allocation in Hong Kong stocks. Renminbi appreciation increases the expected investment return of Hong Kong stock assets, hedges foreign exchange risks, and drives an acceleration of cross-border capital inflows. From 2024 to 2025, the scale of net inflows of southbound funds reached record highs, coinciding with periods of Renminbi strength and low valuations in Hong Kong stocks, confirming the market momentum generated by the combined effects of 'Renminbi appreciation + loose overseas liquidity + deep discounts in Hong Kong stocks.'

Macroeconomic Expectations and Risk Appetite: A strong exchange rate is often regarded as a comprehensive signal of improving fundamentals and a favorable external environment. Moderate Renminbi appreciation reinforces market expectations of economic recovery in China, boosts risk appetite among domestic and foreign investors for Hong Kong stocks, and promotes valuation recovery alongside increased trading activity.

Global Experiences and the Specifics of Hong Kong Stocks

In global markets, the US dollar and US stocks exhibit periodic negative correlations; the depreciation of the Japanese yen and the rise of Japanese stocks form a chain reaction of 'depreciation - foreign capital inflows - increased trading volume - rising valuations'; the linkage between stocks and exchange rates in the Eurozone is relatively weaker; and emerging markets such as Brazil demonstrate characteristics of 'high volatility and high interconnection.'

By comparison, the Hong Kong stock market has unique characteristics: on one hand, it is directly influenced by U.S. dollar interest rate policies (due to the Hong Kong dollar's linked exchange rate system), and on the other hand, corporate earnings are highly correlated with China's mainland economy. This "dual attribute" often enables Hong Kong stocks to perform prominently in an environment of a weakening U.S. dollar and RMB appreciation. Historical data shows that during periods of RMB appreciation, such as 2005-2007, 2016-2017, and 2023-2024, the Hang Seng Index has achieved significant excess returns.

Strategic Allocation in Hong Kong Stocks Amid Moderate RMB Appreciation

Current Exchange Rate Environment and Positioning of Hong Kong Stocks

The RMB exchange rate has moved past the depreciation clearance phase and entered a moderate appreciation channel. As of the end of 2025,$USD/CNY (USDCNY.FX)$the spot exchange rate is approximately 6.99, continuing to fluctuate narrowly around 6.96 in January 2026, representing an appreciation of about 4.4% compared to around 7.30 at the beginning of 2025. Driving factors include:

Trade surplus support: China continues to maintain a large-scale trade surplus, with accumulated actual foreign exchange settlement demand remaining high.

Net inflows under the capital account: Amid heightened volatility in overseas markets, some risk-averse and allocation funds have shifted toward the Chinese market.

Structural long-term trends: The internationalization of the RMB is steadily advancing, with global demand for RMB reserves and usage gradually increasing.

The current Hong Kong stock market is in a triple favorable environment: moderate RMB appreciation, loose overseas liquidity, and historically low valuations of Hong Kong stocks. The AH premium index remains at a high of 118.6 points, indicating that Hong Kong stocks still hold significant valuation advantages relative to A-shares. The three-month HIBOR rate has fallen to 2.83%, with marginal improvement in Hong Kong dollar liquidity conditions, providing support for Hong Kong stock valuation recovery.

Core Allocation Strategy for Hong Kong Stocks

In the current environment, the allocation of Hong Kong stocks should be based on the triple resonance opportunities of "southbound capital inflows + valuation discounts + improved exchange rate conditions," focusing on the following main themes:

High-dividend and value recovery sectors: High-dividend sectors such as energy resources, financial leaders, and utilities have allocation value in an environment where Hong Kong dollar interest rates are peaking and expected to decline. These sectors are currently trading at historically low valuations, with dividend yields generally exceeding 6%. In an environment of RMB appreciation, southbound funds show clear preferences, offering considerable room for valuation recovery.

Leading technology and internet platforms: The Hong Kong stock technology sector combines growth potential with dividend capabilities, trading at an average discount of over 30% compared to similar companies listed in mainland China. With improvements in the regulatory environments of both China and the US, alongside policy shifts favoring the domestic platform economy, leading technology companies are poised for a dual boost in earnings and valuation. RMB appreciation helps reduce foreign currency costs associated with technology firms' R&D investments while enhancing profitability from overseas operations.

Pro-cyclical and cross-border consumption sectors: Sectors benefiting from enhanced RMB purchasing power, including tourism, hotels, luxury goods, and duty-free shopping, deserve close attention. As border-crossing convenience between mainland China and Hong Kong advances and cross-border consumption rebounds, related enterprises exhibit significant profit elasticity. Historical data indicates that during periods of RMB appreciation, pro-cyclical sectors tend to lead gains in the Hong Kong stock market.

Capital flows and valuation recovery in the Hong Kong stock market

Sustained inflow trend of southbound capital

During the fourth week of January 2026 (January 26-30), net inflows of southbound capital amounted to HKD 10.372 billion, which slowed compared to the previous week’s HKD 14.519 billion but maintained a net inflow momentum. Cumulative net inflows of southbound capital in 2024-2025 reached record highs, reflecting strong and sustained demand from mainland investors for Hong Kong stock allocations.

In terms of industry structure, active trading was observed in Hong Kong Stock Connect internet and high-dividend sectors, with their respective trading volume shares (5-day moving average) standing at 15.8% and 8.2%, indicating concentrated investor preference in technology growth and stable value sectors. This structural characteristic aligns well with the current macroeconomic environment of moderate RMB appreciation and rising risk appetite.

Global capital reallocation towards emerging markets

Overseas market capital flow data shows that global funds are shifting from developed markets to emerging markets. As of the week ending January 28, although US equities saw a return to net inflows, inflows into the Japanese market significantly decreased, while developed European markets turned to net outflows.

The trend of capital flowing into emerging markets is also evident in broader asset allocation, with inflows into the gold market increasing to $6.754 billion, reflecting heightened global risk aversion and rising demand for non-U.S. dollar assets. This trend benefits undervalued emerging markets such as Hong Kong stocks by attracting incremental capital, thereby driving the valuation recovery process.

Editor/Melody