The Liberal Democratic Party, led by Sanae Takachi, has secured a two-thirds supermajority in the House of Representatives independently, marking the highest proportion of seats held by any political party in Japan's postwar elections. The Nikkei 225 index surged by 5%, reaching 57,000 points for the first time in history, while the broader TOPIX index gained 3%. Meanwhile, the yen and government bonds face further downward pressure.

According to NHK statistics, the Liberal Democratic Party (LDP) has independently won an absolute majority of more than two-thirds of the 465 seats in the House of Representatives, and the ruling coalition has significantly expanded its advantage. This outcome far exceeded the expectations of some investors in recent weeks.

Tim Waterer, Chief Market Analyst at KCM Trade, stated: 'The election results are clear, and Sanae Takamichi's economic stimulus policies now have a clearer path forward, which is undoubtedly positive news for the Nikkei Index. However, the LDP’s fiscal stimulus plan has essentially been approved and implemented, potentially placing greater depreciation pressure on the yen.'

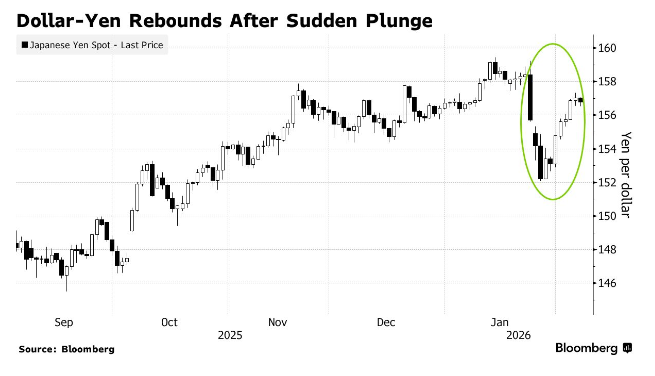

In early Asian trading on Monday, the yen fluctuated within a relatively narrow range. As of this writing, the yen weakened slightly against the US dollar to 157.61. The yen fell by 1.6% last week and remains close to the 160 level—a threshold that previously triggered Japanese authorities to intervene to defend the currency.

In early Asian trading on Monday, the yen fluctuated within a relatively narrow range. As of this writing, the yen weakened slightly against the US dollar to 157.61. The yen fell by 1.6% last week and remains close to the 160 level—a threshold that previously triggered Japanese authorities to intervene to defend the currency.

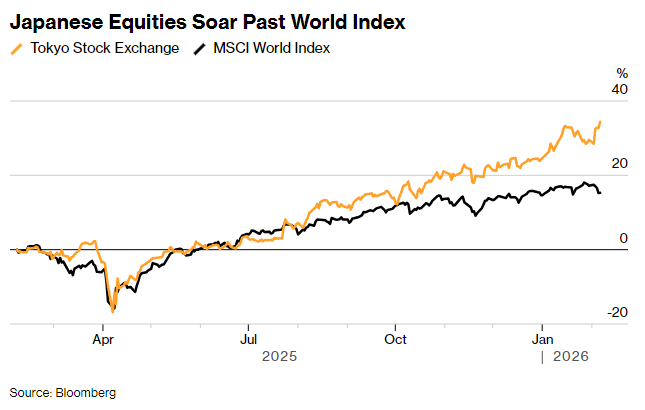

Supported by market expectations that Sanae Takamichi will expand fiscal spending to boost economic growth, Japan’s Topix index closed at a record high last Friday, with year-to-date gains exceeding 8%, while the global developed market stock index rose by only about 2% during the same period.

Rong Ren Goh, Fixed Income Portfolio Manager at Eastspring Investments, commented: 'The LDP’s victory in this election was significant, though not entirely unexpected by the market. In the weeks leading up to the election, Japanese government bond yields and the yen were consolidating, but now that the election is over, the market may return to its previous trend.'

Many investors believe that the core theme of the market on Monday will revolve around what is known as the 'Takamichi trade.' There is also a contrarian view awaiting validation: the larger Sanae Takamichi’s electoral victory, the less pressure she may face to introduce economic stimulus policies.

In the equity market, sectors such as defense and nuclear energy have garnered the most attention, aligning closely with Sanae Takamichi’s proposed national investment agenda.

Gerald Gan, Chief Investment Officer of Singapore-based Reed Capital Partners, said: 'Japan’s stock market will see another round of gains following this election victory. Defense, artificial intelligence, and semiconductors—areas where Sanae Takamichi plans to increase investment—are likely to become the biggest beneficiaries.'

The depreciation of the yen is a double-edged sword for Japan’s economy: while it boosts the profits of export-oriented companies, it significantly squeezes household budgets.

Since Sanae Takamichi assumed the presidency of the LDP in September last year, the yen has continued to weaken until late last month when signals emerged that the US and Japanese authorities might jointly stabilize the yen, briefly slowing the decline. However, in recent weeks, mixed signals from both sides have caused earlier stabilization expectations to fall through.

Neil Jones, Managing Director of Sales and Trading at TJM Europe, commented in an email: 'The natural trajectory for the yen is likely to be further depreciation. Last month, the yen fell below the 159 mark against the US dollar, hitting a new low. The global foreign exchange market now seems to anticipate that Japanese authorities may implement substantial intervention measures within the lower range of the yen.'

During the vote-counting process, Sanae Takagi clarified her earlier remarks on the 'benefits of yen depreciation,' stating that the related statements had been taken out of context. She reiterated her governance goal of building an economic system resilient to exchange rate fluctuations.

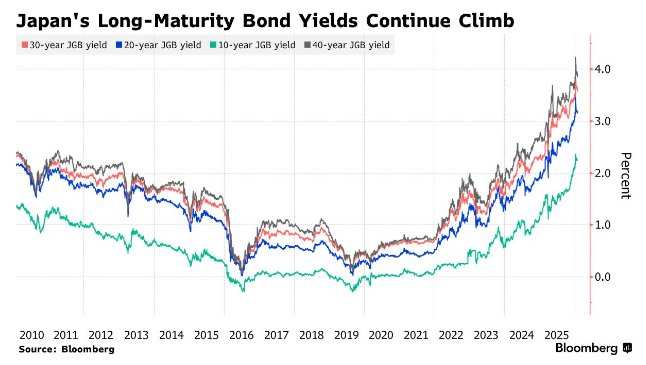

As for Japanese government bonds, which suffered a severe blow in January and triggered volatility across global markets, they now face the risk of further sell-offs.

Global asset management firms such as Schroders Group and JPMorgan Asset Management adopted underweight strategies on Japanese government bonds ahead of the general election, particularly ultra-long-term bonds. In addition to poor market liquidity, the temporary reduction in food consumption tax proposed by Sanae Takagi, along with renewed concerns about Japan's fiscal sustainability, have become core factors driving bond sell-offs.

Despite lingering concerns, Japanese government bonds showed signs of recovery last week, with upward pressure on yields easing. The decline in yields on ultra-long-term bonds was particularly pronounced.

Masanari Takada, Quantitative and Derivatives Strategist at JPMorgan Securities Japan Co., stated: 'While the election results have heightened tension among participants in the government bond market, the overwhelming victory of the Liberal Democratic Party may provide Prime Minister Sanae Takagi with more political maneuvering space, enabling her to focus on addressing the demands of the bond market.'

However, overnight index swaps and short-term government bond yields have begun to adjust, reflecting growing market expectations that the Bank of Japan may raise interest rates at its April policy meeting. Current market pricing indicates a roughly 75% probability of a 25-basis-point rate hike by the Bank of Japan in April, while a 25-basis-point increase in June has already been fully priced in.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Editor/Lambor