According to the latest disclosed 13F report on U.S. stocks, Baillie Gifford, a century-old giant, held total portfolio assets worth $120.34 billion in Q4 2025, representing a decrease of approximately 10.8% from $135 billion in Q3.

This decline was driven not only by the pullback in some high-growth stocks but also primarily by its overall 'net selling' operational stance.

In terms of major holdings, $NVIDIA (NVDA.US)$ despite being reduced for the second consecutive quarter (with an approximate 5.76% reduction this quarter), it remained the largest holding with a 6.80% portfolio share.

Following closely is MercadoLibre, $MercadoLibre (MELI.US)$ in which Baillie Gifford made a 4.95% reverse increase during Q4, raising its portfolio share to 5.83%, further solidifying its position as a cornerstone asset in the portfolio.

Following closely is MercadoLibre, $MercadoLibre (MELI.US)$ in which Baillie Gifford made a 4.95% reverse increase during Q4, raising its portfolio share to 5.83%, further solidifying its position as a cornerstone asset in the portfolio.

The remaining slots among the top five holdings are occupied by $Amazon (AMZN.US)$ 、 $Shopify (SHOP.US)$ and $Sea (SE.US)$ , with the combined share of the top ten holdings reaching as high as 43.4%.

In addition to NVIDIA, Baillie Gifford significantly reduced its positions in Amazon, Shopify, Meta, and others. $Cloudflare (NET.US)$ , etc.

The notable move in the fourth quarter was a significant increase in holdings of $Alphabet-A (GOOGL.US)$ , with the increase reaching 166%. This action complements Berkshire Hathaway's logic for establishing a position in Google in the third quarter of last year. If Buffett values Google's monopolistic moat, Baillie Gifford places more emphasis on its cost advantages in AI-customized chips and large-scale computing power.

Of course, considering the initially low stake in Google, after this increase, Baillie Gifford's market value of Google shares (including both Class A and Class C shares) is approximately $1.7 billion.

Recently, I reviewed two sets of communication materials from key figures of SMT (Scottish Mortgage Investment Trust), Baillie Gifford’s “crown jewel,” which provide some insight into the overarching logic behind Baillie Gifford's various portfolio adjustments.

SMT traces its history back to 1909 and has been continuously operating for 116 years, making it one of the oldest investment trusts globally and a portfolio managed by legendary Baillie Gifford fund manager James Anderson for 20 years.

Although SMT is “old” in terms of its age, the soul of its portfolio remains youthful. Its holdings include global leaders such as MercadoLibre, Amazon, Meta, PDD Holdings, and Taiwan Semiconductor, as well as innovative companies in private stages like SpaceX, ByteDance, and Epic Games.

At the SMT Professional Investor Forum held in early 2026, the two fund managers who took over from Anderson, Tom Slater and Lawrence Burns, stated that we are entering a “golden age of transformation,” a highly innovative period whose impact may “far exceed the progress of the past two decades.”

Drawing from investment expert Hamish Maxwell’s discussions on SMT's investment situation in the fourth quarter of last year, we have summarized the core team at Baillie Gifford's investment thinking in this era of innovation for reference and learning, providing a deeper understanding of how this century-old giant, renowned for its 'ultra-long-term investment' philosophy, envisions the future of AI investments.

AI has created a new paradigm of intelligence.

Slater borrowed a surfing metaphor from NVIDIA CEO Jensen Huang: companies that try to resist the wave cannot rise with the tide; what truly matters is 'sensing the direction of the wave and riding it accordingly'.

This effort must start early, 'paddling before the AI wave fully arrives,' and then going all out when the trend truly takes shape.

He pointed out that the most dangerous moment in surfing is 'the drop,' the instant of transitioning from paddling to standing on the board.

For businesses, this means that once they identify product-market fit, they must decisively abandon outdated business models and fully commit to delivering new products and meeting demand.

He mentioned that a conversation with Spotify's co-CEO Alex Nordström aptly summarized this shift in thinking: what companies need now is 'anticipatory capability.'

Slater strongly agreed: success over the past decade often came from linear extrapolation, but today 'we are back to an era where we must proactively anticipate.'

He views 'intelligence' as the next paradigm shift following 'internet-mobile-cloud computing.' The previous paradigm shaped the large network companies that dominate today’s global economy, while the new paradigm will redefine how value is distributed within ecosystems.

“For long-term growth investors like us, the most exciting aspect of this shift is that every paradigm change gives rise to new large companies and fresh growth opportunities.”

So far, he believes that 'the vast majority of value remains concentrated at the silicon chip level, primarily around NVIDIA.' This trend may continue as computing power is still scarce, 'and we still need a significant increase in new chips.'

Slater pointed out that the two major application fields that have truly taken shape currently are personal assistant chatbots and programming assistance tools.

"OpenAI's ChatGPT has become one of the top five most visited websites globally... This is also why OpenAI's valuation has now reached 50 billion US dollars."

He stated that software development is 'the heart of the modern economy,' but at the same time, it is also 'the biggest bottleneck for growth' due to a shortage of engineers.

Moreover, Anthropic, held by SMT, has crossed the 'next wave point' and is truly riding the wave, becoming one of the fastest-growing technology companies in history, with an annual revenue compound growth rate reaching an astonishing 10 times.

As AI moves from pure software to embodied intelligence, which is intelligent systems deeply integrated with the physical world, Slater predicts that a more pronounced 'winner-takes-all' or 'winner-takes-most' economic landscape will emerge because only a few companies can afford the enormous investments required for this competition.

He predicts that this process will initially appear gradual but will eventually accelerate suddenly. In the 'Internet-Mobile-Cloud Computing' paradigm, progress is relatively linear; however, in the 'Intelligence Paradigm,' there may be sudden and dramatic leaps.

In the field of embodied intelligence, autonomous trucks are nearing a critical tipping point. Progress has been slow because safety is non-negotiable.

"If you're going to replace the driver of a heavy truck traveling at 60 miles per hour and weighing 36 tons with a computer, you must ensure it is safe."

But the situation is changing. Slater specifically mentioned Aurora, a company in which SMT holds shares, believing that it has successfully positioned itself to benefit when large-scale autonomous driving deployment occurs.

In the logistics industry, he used Zipline as an example to illustrate how speed changes consumer behavior. "Reducing delivery time from one hour to 15 minutes will completely alter consumer habits."

However, meeting the annual demand of 55 billion deliveries solely through human labor is clearly insufficient. 'This will be a market for drones.'

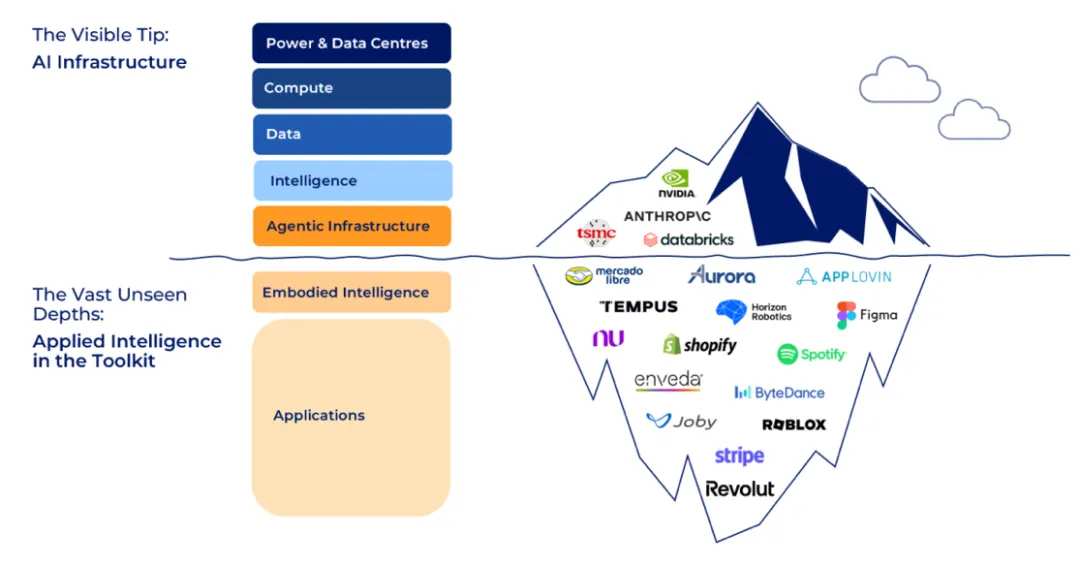

The 'Iceberg Model' of AI

According to Hamish Maxwell, AI is not just another technological trend but is becoming the new infrastructure for the global economy.

'Markets often view this opportunity from a short-term perspective: timing of orders, whether spending next year will increase or decrease. However, this perspective risks overlooking the bigger picture. We aim to hold companies that are building the future over the long term and listen to visionary leaders.'

He introduced that SMT holds NVIDIA, Taiwan Semiconductor, and ASML Holding at the hardware level. 'These are critical technologies, but we also recognize that this path will not be without challenges.' For instance, Taiwan Semiconductor indicated that AI demand remains strong, while ASML cautioned that optimistic expectations for demand will not immediately translate into equipment orders, as this will take time.

On the demand side, SMT focuses on real adoption and monetization. 'We do not attempt to predict the rhythm of capital cycles; rather, we aim to steadfastly support long-term winners as AI transitions from a conceptual hype to a global productivity driver.'

Maxwell explained that SMT categorizes AI opportunities into two types: companies for which 'AI is core,' and companies for which 'AI serves as a toolkit,' quietly reshaping products and services in the background.

'This is precisely what we mean by the 'Iceberg Model': the visible portion above the waterline represents the creation layer of AI, including companies like NVIDIA, Taiwan Semiconductor, Anthropic, and Databricks, which help others access AI. This part naturally attracts the most market attention.'

The truly greater opportunity lies beneath the surface. AI is being embedded into workflows, customer interactions, decision-making systems, and creative processes, with its value accumulating over the long term.

This part may not be easily noticeable on a quarterly basis, but it builds a lasting advantage over time.

SMT has made extensive deployments at the application layer. A brief look at the portfolio companies reveals: MercadoLibre uses AI to comprehensively enhance the efficiency of e-commerce and fintech in Latin America; Shopify helps millions of merchants run their online businesses more efficiently; AppLovin improves advertising effectiveness through AI; Stripe, Nubank, and Revolut apply AI to foundational infrastructure, including better risk control, automated services, and anti-fraud measures; Spotify personalizes music recommendations; Roblox lowers the barrier for building digital worlds; ByteDance optimizes content distribution and user engagement through AI; Tempus is used for medical diagnostics; Enveda aids in drug discovery... and so on.

Our overall philosophy is this: above the iceberg lies the creative layer of AI, while beneath the iceberg lies the broader and deeper application layer of AI. We aim to position ourselves in both layers, investing in companies that can truly turn AI into a core competitive advantage rather than merely treating AI as an expense.

Section 03: China, Platform Companies, and 'Outlier Returns'

Lawrence Burns shared his observations from his recent trip to China.

He noted that market sentiment has shifted significantly, although 'the actual changes on the ground are far less dramatic than the sentiment suggests.' China remains 'a place where visionary entrepreneurs can thrive,' and technology continues to be implemented 'at an astonishing speed and scale.'

Burns pointed out that in the battery sector, '85% of global battery production capacity is in China,' and SMT's holdings $CATL (03750.HK)$ account for approximately 40% of the global market share.

He believes that as battery applications expand from electric vehicles to other areas like grid energy storage, the coming decades will present tremendous development opportunities.

In the electric vehicle sector, he described $BYD COMPANY (01211.HK)$ as "the undisputed global leader," accounting for approximately one-quarter of global electric vehicle sales. After meeting with the founder of BYD, Burns believed that the confidence of the counterpart stemmed not only from cost advantages but also from the assertion: "We can not only produce affordable cars profitably, but we are also making better cars."

He also frankly acknowledged the associated risks. "Geopolitical risks are real, and so are domestic regulatory risks."

Even so, Burns still maintained that "there remain a small number of outstanding companies in China with tremendous potential worthy of investment." In these cases, "technology and growth assets are still significantly undervalued and remain in a 'discounted sale' state."

He further pointed out that the market's pricing of geopolitical risks is uneven. Should a complete economic decoupling occur, enterprises with deep operational and revenue ties to China could face impacts far exceeding what their current valuations reflect.

He added: "The importance of understanding China has never been higher." In tracking the evolution of technology, China has become as significant as Silicon Valley.

Burns then discussed platform-based enterprises. He noted that most companies belong to "linear value chains," creating value by selling products or services directly to consumers. Platform companies, however, operate entirely differently, generating value by facilitating multi-party transactions, building ecosystems, setting rules, providing infrastructure, and enabling others to create value through incentive mechanisms.

"The larger the platform, the stronger it becomes." Scale enhances network effects, improves data and recommendation systems, and allows platforms to distribute infrastructure costs across millions of users. Moreover, these platforms demonstrate remarkable adaptability, with leading companies often undergoing continuous business transformations and experiencing successive waves of growth.

Burns suggested that investing in such companies requires a unique mindset: "You need imagination—not just to analyze what exists but also what might exist—and you need patience... because their financial curves often look unimpressive at first but can suddenly explode once monetization begins."

04 Why Invest in Private Companies

Hamish Maxwell noted that since 2012, the team has been actively investing in private companies, with cumulative committed capital exceeding £60 billion, supporting a group of enterprises truly transforming the world. "This is a highly distinctive part of the investment portfolio."

The reason for investing in private companies is simple: companies are remaining private for increasingly longer periods. In 2014, the average age of a company at IPO was seven years; by 2024, this figure had risen to eleven years. For investors who only invest in public markets, this period represents the loss of an entire era of growth – many dynamic companies now create most of their value before going public.

Meanwhile, the private equity market has expanded rapidly.

Globally, there are now over 1,500 privately held companies valued at more than $1 billion, with a total market capitalization exceeding $5 trillion.

For investors seeking to gain exposure to the next generation of disruptive growth companies (such as those focused on training AI models), accessing private companies has become essential.

"This is precisely why we invest in both public and private companies. Our shareholders are thus able to capture a more complete growth curve, whereas these opportunities would be difficult to access if limited to public markets."

In terms of market value, SMT’s largest private holdings, including SpaceX and ByteDance, have surpassed the valuations of the UK's largest publicly listed blue-chip companies; its stakes in Anthropic, Databricks, and Stripe are also significant enough for them to rank among large public companies on their first day of listing.

Following a recent valuation increase to $800 billion (and according to the latest market projections, it has since risen to $1.2 trillion), SpaceX, which SMT invested in starting in 2018, has become the largest holding in SMT's portfolio, accounting for 15%.

In Maxwell’s view, these companies possess solid fundamentals, with revenue growth of approximately 140% last year among the top ten private companies, compared to single-digit revenue growth for benchmark indices.

Moreover, SMT is not forced to sell at IPO. "Many early successful private investments, such as Spotify and $MEITUAN-W (03690.HK)$ It has now become an important position in our open market.

Chapter 05: Bottom-Up Portfolio Construction

Burns emphasized that SMT’s portfolio remains constructed from the bottom-up while striving to avoid blind spots in future key areas.

He emphasized the breadth of the portfolio, stating, 'SMT is not, and will never be, a single bet on one country, one trend, or one new technology. It invests in global transformation, which manifests as progress in various forms.'

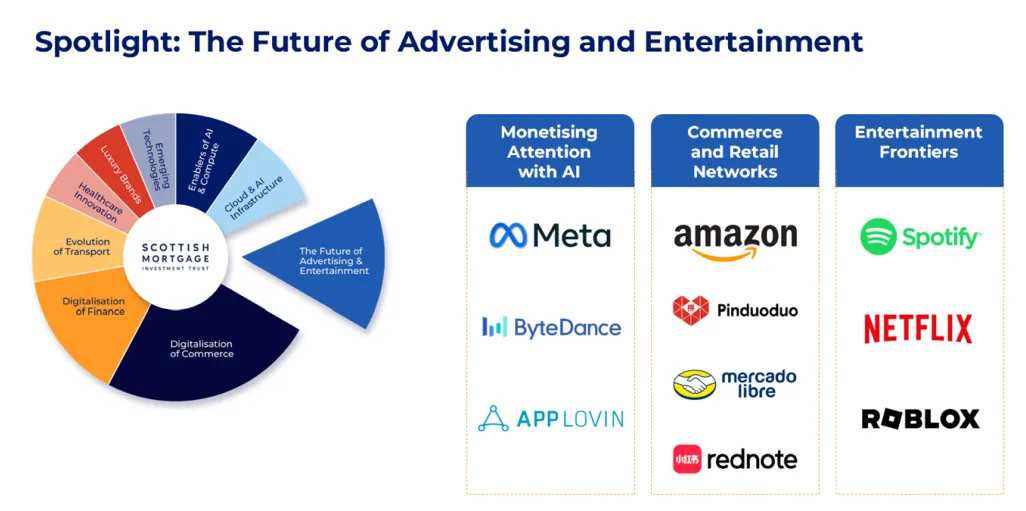

Maxwell elaborated on the dynamic adjustment approach for portfolio targets, making the aforementioned philosophy more tangible.

He used a chart.

On the left side of Figure 2 are companies that monetize attention, including Meta, ByteDance, and $Applovin (APP.US)$ . These companies leverage massive user bases and rich feedback loops to continuously enhance their relevance and alignment with users and advertisers.

The middle category consists of 'e-commerce and retail network-based' platforms, including Amazon, PDD Holdings, MercadoLibre, and Xiaohongshu. These companies are more closely aligned with actual purchasing behaviors, enabling them to build discovery mechanisms and advertising systems around transactions.

On the right side are the 'entertainment frontier' platforms, including $Spotify Technology (SPOT.US)$ 、 $Netflix (NFLX.US)$ and $Roblox (RBLX.US)$ . They connect creators with audiences, continuously enhancing their value by improving content discovery efficiency, deepening user engagement, and expanding monetization methods.

“We consistently and steadily recycle capital and reinvest it into the next generation of disruptive growth opportunities. On the left are cases of reductions or exits, while on the right are new investment deployments.”

Additionally, SMT has increased its investments in electrification trends, such as purchasing $CATL (03750.HK)$ . It has also increased its stake in Xiaohongshu, a Chinese consumer platform, as well as in Revolut, a UK-based fintech company.

Understand institutional holdings and stay updated with the latest investment trends. Market > US Stocks > Institutional Tracking

Understand institutional holdings and stay updated with the latest investment trends. Market > US Stocks > Institutional Tracking

Editor/KOKO