On February 18, Eastern Time, the Federal Reserve's official website released the minutes of the January 2026 meeting.Federal Open Market CommitteeMinutes of the meeting. The latest minutes released by the Federal Reserve once again revealed significant divisions among policymakers regarding the future direction of interest rates. In addition to those supporting rate cuts and those adopting a wait-and-see approach, the minutes also explicitly mentioned for the first time discussions about the possibility of raising interest rates. This reflects that, with inflation persistently remaining above the Fed's 2% target and the economy maintaining resilience, the central bank’s policy focus has shifted back to inflation risks rather than a slowdown in employment.

The minutes of the Federal Reserve meeting revealed:

Nearly all participants supported pausing interest rate actions in January. Several participants indicated that further rate cuts would likely be appropriate if inflation declines as expected.

A majority of participants warned that the progress toward the 2% inflation target could be slower and more uneven than widely anticipated, with the risk of persistent above-target inflation assessed as significant.

A majority of participants warned that the progress toward the 2% inflation target could be slower and more uneven than widely anticipated, with the risk of persistent above-target inflation assessed as significant.Participants noted that economic activity appeared to be expanding at a solid pace; growth in 2026 was broadly expected to remain robust.

Participants generally believed that, under appropriate monetary policy implementation, the labor market would likely stabilize first and then improve over the course of the year.

Participants anticipated that inflation would retreat toward the 2% target, though the speed and timing of the decline remained uncertain.

Several participants stated they would have supported adopting a two-sided approach in future interest rate decisions to reflect that rate hikes might be appropriate if inflation remains persistently above target levels.

Multiple participants believed that further rate cuts could undermine market perceptions of the commitment to the inflation target.

A few participants favored a rate cut in January.

The Federal Reserve staff's outlook for economic activity is stronger than in December, with inflation expected to be slightly higher than previously anticipated, and the unemployment rate projected to gradually decline starting from 2026.

Two-way possibilities emerge for the interest rate path.

As expected by the market, the Federal Reserve decided to pause rate cuts at its January 27-28 meeting. Among the 12 FOMC voting members, two dissented from this decision. The two dissenters — Governor Waller, who was then one of the candidates for Fed Chair, and another governor, Milan, appointed by President Trump — both supported continuing to cut rates by 25 basis points.

The minutes released this Wednesday showed that some Fed policymakers were cautious about further rate cuts during discussions on monetary policy prospects at the January meeting, at least in the short term. The minutes stated:

Several participants cautioned that further easing of monetary policy amid elevated inflation data could be misinterpreted as a weakening of policymakers' commitment to the 2% inflation target.

This position contrasts with the view of another group of officials. The minutes showed that several officials believed that if inflation declines as expected, the possibility of further rate cuts remains. However, most officials noted that progress on inflation might be slower than widely anticipated.

All participants unanimously agreed that monetary policy does not proceed along a predetermined path but is instead determined by the latest data, evolving economic prospects, and the balance of risks.

Fed Wire: Fed Meeting Minutes Show Little Appetite for Rate Cuts

"Fed Wire" Nick Timiraos wrote that Federal Reserve officials showed little inclination toward cutting interest rates at last month’s meeting. More officials expressed reduced concerns about the labor market, while their worries about inflation increased. The minutes noted that most officials cautioned that progress in reducing inflation "might be slower and more uneven than widely anticipated." They believed that the risk of inflation remaining persistently above the Fed’s 2% target was "significant."

According to the minutes, the Fed staff's inflation forecast described a scenario of more persistent and above-target inflation as a "notable risk." Data released after the January meeting could give officials who see no urgency to continue cutting rates more confidence. Markets broadly expect the Fed to remain on hold at its next meeting. Last week, the Labor Department reported that employers added 130,000 jobs in January, exceeding expectations, with the unemployment rate edging down to 4.3%, alleviating concerns over a sharper slowdown in the labor market. Nevertheless, annual revisions showed a significant deceleration in job growth over the past year.

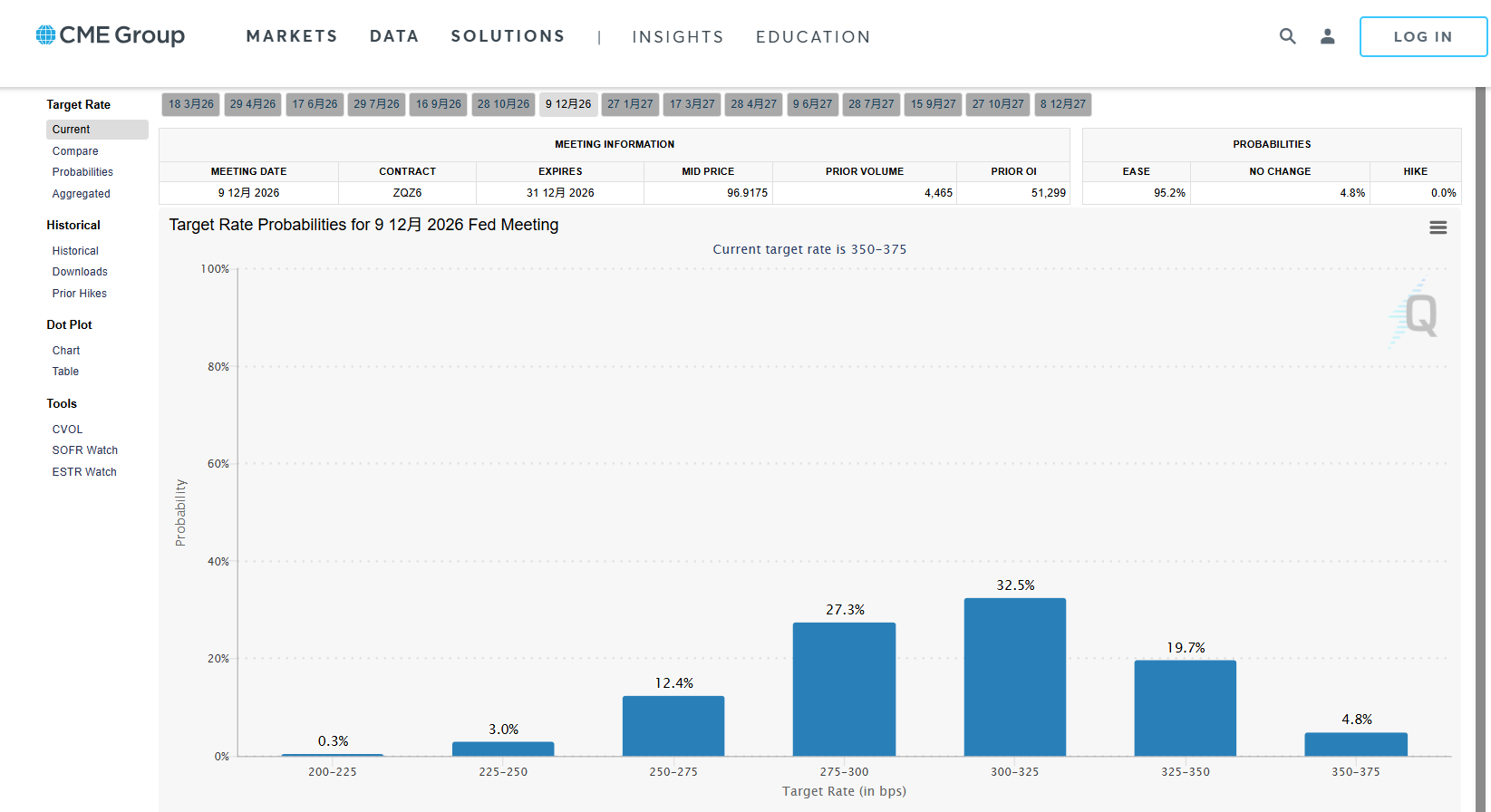

The probability of three interest rate cuts within the year has dropped to less than 30%.

Following the release of the Federal Reserve's interest rate decision, CME data showed that the probability of the Fed cutting interest rates three times in 2026 has dropped to less than 30%. The likelihood of two rate cuts within the year stands at 32.5%, while the probability of a single rate cut is 19.7%. Additionally, the probability of the Fed maintaining interest rates unchanged in March is 94.1%.

Minutes of the Meeting Original Text

Financial Markets and Open Market Operations Dynamics

The manager of the System Open Market Account first provided an overview of overall market dynamics during the inter-meeting period. Respondents to the Open Market Trading Desk's Survey of Market Expectations continued to view the U.S. economy as resilient, revising up their forecasts for real GDP growth in 2026, while expectations for the overall personal consumption expenditure (PCE) inflation rate and unemployment rate remained largely unchanged. Policy rate expectations based on both market data and surveys also stayed relatively stable. Market-based expectations for the policy rate indicated that the Federal Reserve might implement 1-2 rate cuts of 25 basis points this year. The median path from the trading desk survey still showed market expectations of two 25-basis-point rate cuts in the federal funds rate during the current year.

Subsequently, the account manager outlined developments in the U.S. Treasury market and changes in market-based inflation compensation indicators. Yields on short-term Treasuries were largely flat, while yields on long-term Treasuries rose slightly, leading to a modest steepening of the Treasury yield curve. Short-term inflation compensation continued to decline due to lower-than-expected consumer price index readings, falling energy prices, and weaker-than-anticipated pass-through effects of tariffs to consumers. Forward rates indicate that short-term inflation levels will stabilize near current levels for the remainder of the year. Model-based measures of short-term inflation expectations also retreated during the inter-meeting period, with forward rates suggesting that inflation will continue to drift lower this year. The U.S. Treasury market operated smoothly amid a low-volatility environment. Given the ongoing increase in the proportion of Treasury securities financed through repurchase agreements, the account manager highlighted that stability in the repo market is crucial for the sustained smooth functioning of the Treasury market.

Recent announcements indicating that Fannie Mae and Freddie Mac may expand their mortgage loan portfolios attracted significant market attention, resulting in a notable decline in yields on mortgage-backed securities relative to Treasury securities of comparable maturities. However, the account manager noted that this decline in yields is unlikely to drive a substantial increase in mortgage refinancing activity, as current mortgage rates remain significantly higher than the weighted-average rate of outstanding mortgages.

The account manager then discussed equity market performance. Shares of leading technology companies continued to underperform the broader market, as investors remained focused on their elevated valuations and large capital expenditures. Excluding these firms, the S&P 500 Index rose nearly 3% during the inter-meeting period, with cyclical sectors and small-cap indices outperforming.

Regarding international market dynamics, private-sector consensus forecasts still anticipate that the U.S. dollar will depreciate this year, driven by expectations that the Federal Reserve will cut policy rates more aggressively than other advanced economies. However, depreciation expectations for the dollar have moderated significantly over the past few months, reflecting the improving outlook for U.S. economic growth relative to other major economies. A few days before the meeting, the dollar depreciated sharply following news that the Open Market Trading Desk had inquired about indicative quotes for the dollar-yen exchange rate. The account manager clarified that this inquiry was conducted by the Federal Reserve Bank of New York, acting as the fiscal agent of the U.S. Treasury and representing the Treasury exclusively.

The account manager then analyzed developments in the money market. During the inter-meeting period, the effective federal funds rate remained stable at a level slightly below the interest rate on reserve balances, while pressures on repo rates eased overall. Despite a notable increase in repo rates at year-end, the pressure was less severe than widely anticipated by investors. Market participants attributed this better-than-expected outcome to several factors: increased liquidity from the initiation of reserve management purchases and a decline in the Treasury General Account balance, recent adjustments to the design and communication mechanisms of standing repo facility operations, greater adoption of centrally cleared repos, and investor preparedness for potential year-end funding stress.

The account manager noted that adjustments to the standing repo facility implemented in December 2025 may have increased market participants' willingness to engage — usage of the facility rose compared to periods prior to December when market rates exceeded the standing repo facility rate. Market participants cited the removal of caps on operation sizes, clarification that the facility serves monetary policy implementation objectives, and the Chair's statement that operations would be conducted "when economically rational" as key factors driving increased participation.

Finally, the account manager outlined the expected trajectory of core items on the Federal Reserve's balance sheet. With reserve management purchases continuing, bank reserves are projected to grow until early April 2026, after which they will decline sharply due to inflows into the Treasury General Account from tax receipts. The trough in reserves is expected to match levels seen at the end of last year. Over most of the forecast horizon, reserves are expected to fluctuate around $3 trillion.

By unanimous vote, the Committee ratified the domestic open market operations conducted by the Open Market Trading Desk during the inter-meeting period. No foreign exchange intervention operations were undertaken for system accounts during this time.

Staff Economic Review

The information available at the time of the meeting indicated that the U.S. real GDP continued to expand in 2025, albeit at a slightly slower pace than in 2024. The labor market showed signs of stabilization after a period of gradual cooling. Inflation in consumer prices remained at a marginally elevated level.

The U.S. unemployment rate stood at 4.4% in December 2025, unchanged from September. The monthly average change in total nonfarm employment turned negative in the fourth quarter, primarily due to a significant reduction in government employment following the conclusion of deferred resignation plans in October; average job additions in November and December were broadly in line with those in the third quarter. Over the 12 months ending in December, average hourly earnings increased by 3.8% year-over-year, slightly below the growth rate from the previous year.

As of November, the year-over-year increase in the personal consumption expenditures (PCE) price index was 2.8%, slightly higher than 2.6% in the previous year; the core PCE price index, which excludes energy and most food prices, rose by 2.8% year-over-year, down from 3.0% in the prior year. Core services inflation moderated on an annual basis, driven mainly by a slowdown in housing services price growth; conversely, core goods inflation accelerated, which staff attributed primarily to tariff increases. In December, the consumer price index (CPI) increased by 2.7% year-over-year, while the core CPI rose by 2.6%, both lower than the previous year's levels. Based on CPI estimates, staff projected the overall PCE price index to rise by 2.9% year-over-year in December and the core PCE price index by 3.0%. Staff also noted that data collection issues caused by the government shutdown may have depressed the statistical values of the CPI and PCE prices for November and December.

The U.S. real GDP experienced robust growth in the third quarter of 2025, but indicators suggested a moderation in growth during the fourth quarter, with the government shutdown expected to reduce real GDP growth by approximately 1 percentage point. Real private domestic final purchases (comprising personal consumption expenditures and private fixed investment, which typically provide a better gauge of the economy’s underlying momentum than GDP) grew at a pace matching real GDP over the first three quarters of 2025; indicators showed that growth in real private domestic final purchases slowed in the fourth quarter as well, though less sharply than real GDP. Nominal exports of goods continued to grow in October, while nominal imports of goods rebounded significantly in October after declining in the third quarter. As a result, the trade deficit in goods continued to narrow — earlier in 2025, the deficit had widened substantially as firms accelerated imports in anticipation of expected tariff hikes.

Recent indicators pointed to foreign economic activity growing below trend levels in the second half of 2025. U.S. tariff policies continued to weigh on foreign manufacturing sectors, with particularly pronounced impacts on Canada and Mexico’s automotive, aluminum, steel, and related industries. By contrast, strong demand driven by the artificial intelligence boom spurred substantial growth in high-tech exports from some emerging Asian economies; China’s economy benefited from robust exports to markets outside the U.S.

Overall inflation rates in most foreign economies approached central bank targets, although upward pressure persisted in food and services prices in some economies. A few foreign central banks cut interest rates, including the Bank of England and the Bank of Mexico, while most maintained rates unchanged; a notable exception was the Bank of Japan, which raised its key policy rate to near the neutral range.

Staff Review of Financial Conditions

During the inter-meeting period, the market-implied path of the federal funds rate, nominal Treasury yields, and swap-based inflation compensation measures remained largely unchanged. Broad equity indices experienced modest gains overall, with credit spreads at historically low levels. One-month options on the S&P 500 indexImplied volatilitywere broadly flat from the beginning to the end of the period, remaining at a historically moderate level.

Geopolitical events caused some volatility in foreign financial markets during the inter-meeting period, but market risk appetite recovered quickly. Foreign equity indices generally rose and outperformed U.S. indices, continuing last year’s trend. Heightened political uncertainty and investor concerns about fiscal prospects led to a sharp rise in Japanese government bond yields, but spillover effects on other advanced economies’ bond yields were limited. The U.S. dollar depreciated against most currencies, and toward the end of the inter-meeting period, the yen appreciated amid market speculation that Japanese authorities might intervene in the foreign exchange market to support the currency.

Short-term funding markets operated smoothly. The Federal Reserve’s initiation of reserve management purchases and short-term Treasury redemptions helped ease upward pressure on money market rates. Following a 25-basis-point reduction in the target range for the federal funds rate in December 2025, secured and unsecured money market rates adjusted promptly. Year-end pressures in short-term funding markets were mild, supported by increased liquidity from reserve management purchases, a decline in the Treasury General Account balance, rising utilization of standing repurchase agreement facilities, and some dealers locking in year-end financing early.

Within the U.S. domestic credit market, financing costs for corporations, households, and local governments remain significantly lower than the peak levels of 2023 but are higher than the average levels seen after the global financial crisis. During the inter-meeting period, yields on corporate bonds, leveraged loans, and commercial mortgage-backed securities declined, while interest rates on 30-year fixed-rate conforming mortgages and new auto loans also decreased in tandem.

Credit resources remained broadly accessible for most businesses, households, and local governments, with strong issuance volumes observed in corporate bonds, private credit, and long-term municipal bonds, alongside continued moderate expansion in bank lending. In contrast, credit conditions remained relatively tight for small businesses and individuals with low credit scores.

Results from the January Senior Loan Officer Opinion Survey indicated that overall bank lending standards eased slightly further in the fourth quarter of 2025, primarily reflecting relaxed standards for commercial real estate loans and consumer loans. Across all loan categories, banks’ overall lending standards are projected to remain at the median level since 2011.

The quality of credit assets remained generally stable, though weaker than pre-pandemic averages. The 12-month rolling default rates for corporate bonds and leveraged loans declined in November and December; defaults on direct private loans stayed low, but a significant portion of loans continued to defer interest payments through payment-in-kind arrangements. Delinquency rates for small business loans and commercial mortgage-backed securities were largely unchanged in November, remaining above pre-pandemic levels. On the household side, delinquency rates for most types of mortgages neared historical lows, while credit card and auto loan delinquency rates remained elevated compared to pre-pandemic levels.

Staff conducted an updated assessment of the stability of the U.S. financial system and concluded that significant vulnerabilities persist. Staff assessed that asset valuation pressures remain high, with equity price-to-earnings ratios in public markets positioned at the upper end of their historical distributions, partly driven by robust expectations of earnings growth among technology firms and elevated risk appetite among investors.

Vulnerabilities related to debt among non-financial corporations and households are at moderate levels. Corporate debt grew modestly over the past few years, with most of the increase concentrated in investment-grade public market issuers. Future investments in artificial intelligence may lead to higher corporate bond issuance, but most technology firms maintain low debt burdens, and overall debt growth has been moderate in recent years, indicating their capacity to absorb such increases.

Leverage-related vulnerabilities within the financial sector remain significant. Data indicates that leverage levels among hedge funds and life insurance companies remain elevated. Conversely, banks maintain high regulatory capital adequacy ratios, though their market-value-adjusted capital adequacy remains relatively low and is sensitive to long-term interest rate fluctuations.

Vulnerabilities associated with funding risks are at moderate levels. The total share of short-term funding instruments and cash management products as a percentage of GDP lies in the middle of its historical range, while uninsured bank deposits remain within normal historical levels. Life insurers face low funding risks from non-traditional short-term liabilities. The total market capitalization of stablecoins has grown substantially over the past two years, with some stablecoins posing potential run risks, though their scale remains small relative to other funding instruments.

Staff Economic Outlook

Compared to the projections made during the December 2025 meeting, staff presented a more optimistic outlook for economic activity, citing better-than-expected incoming data, stronger-than-anticipated support from financial conditions, and a slight upward revision to the potential output trajectory. As the drag from tariffs gradually dissipates, coupled with ongoing fiscal policy and supportive financial market conditions, real GDP growth is expected to remain above potential through 2028. Consequently, the unemployment rate is projected to decline steadily starting in 2026, falling below the staff's estimate of the natural rate of unemployment by year-end and remaining there through 2028.

Overall, staff’s inflation forecasts for this round were slightly higher than those presented in December, reflecting expectations of tighter resource utilization and stronger core import price dynamics than previously anticipated. With the impact of tariffs on inflation expected to fade starting in mid-2026, inflation is anticipated to revert to its prior downward trend.

The staff noted that, due to geopolitical tensions, adjustments in government policies and their impacts, as well as the uncertain role of artificial intelligence in the economy, overall economic uncertainty remains high. Additionally, delays in the release of statistical data and related data quality issues have further exacerbated this uncertainty. In an environment of elevated economic uncertainty, downside risks to employment and real GDP growth forecasts persist; inflation forecast risks remain tilted upward — a notable risk being that inflation has remained above 2% since early 2021, potentially exhibiting more persistence than anticipated by the staff.

Participants' views on the current situation and economic outlook

Participants observed that overall inflation in the United States has declined significantly from its peak in 2022 but remains slightly above the Committee's long-term target of 2%. Participants generally highlighted that the elevated inflation is primarily concentrated in core goods, seemingly driven by tariff increases. Unlike core goods, some participants noted that core services inflation continues to decline, with housing services inflation showing particular moderation.

Regarding the inflation outlook, participants expected inflation to gradually return to the 2% target, but uncertainties regarding the pace and timing of this decline remain. Participants widely agreed that the impact of tariffs on core goods prices may begin to fade by 2026. Several participants noted that the continued slowdown in housing services inflation could exert downward pressure on overall inflation. Others anticipated that productivity gains driven by technological or regulatory developments might also contribute to downward pressure on inflation. Consistent with this view, a few participants mentioned feedback from businesses indicating increased automation efforts and other measures to offset rising costs, thereby reducing the need for firms to pass costs onto consumers or compress profit margins. However, most participants cautioned that the process of inflation returning to the 2% target may be slower and more volatile than expected, with the risk of inflation remaining persistently above target being a concern. Some cited business feedback suggesting plans to raise product prices in 2026 due to cost pressures such as tariffs, while others pointed to sustained strong demand potentially keeping inflation above the 2% target.

Participants noted that most indicators of long-term inflation expectations remain consistent with the Committee's 2% target. Furthermore, several participants emphasized that market- and survey-based measures of short-term inflation expectations have declined from their peaks in spring 2025.

In terms of the labor market, participants observed that the unemployment rate has remained broadly stable recently, while job additions have continued at low levels. Most participants noted that recent data on unemployment, layoffs, and job vacancies suggest the labor market may be stabilizing after a period of gradual cooling. Nearly all participants observed that layoffs remain at low levels, but hiring activity is also subdued. Consistent with this, several participants mentioned that feedback from businesses indicates ongoing caution in hiring decisions amid uncertainty about the economic outlook and the impact of automation technologies such as artificial intelligence. Some participants highlighted supply-side factors, including a decline in net immigration, as contributing to slower employment growth.

Participants generally agreed that, under appropriate monetary policy, the labor market may stabilize and subsequently improve in 2026, though uncertainties about its outlook remain. The majority of participants judged that signs of stabilization in the labor market have emerged, reducing downside risks to employment. However, some participants noted that, despite signals of labor market stabilization, certain indicators, such as measures of job availability and the share of part-time workers for economic reasons, still indicate weakening conditions. Moreover, most participants highlighted that downside risks to employment persist, particularly in an environment of subdued hiring, where further declines in labor demand could lead to a significant rise in unemployment. Concentration of employment growth in a few less cyclical industries may also signal increasing fragility in the broader labor market.

Participants noted that U.S. economic activity is expanding at a steady pace. They widely pointed out that household consumption remains resilient, supported importantly by growth in household wealth. Despite overall robust consumption, several participants cited business feedback or recent analyses indicating strong spending among high-income households but weaker spending among low-income households. Participants observed that business fixed investment remains solid, with particularly strong investment in the technology sector. Regarding agriculture, two participants noted continued weakness in crop farming, while livestock farming remains buoyant.

Participants generally expected that the U.S. economy will continue to grow robustly in 2026, though uncertainties about the growth outlook remain elevated. Most participants believed that improvements in financial conditions, fiscal policy support, or regulatory adjustments would provide a boost to economic growth. Additionally, several participants judged that ongoing productivity gains, driven by high investment in artificial intelligence and productivity improvements in recent years, would contribute positively to economic expansion.

In discussions on financial stability, several participants expressed concerns about elevated asset valuations and historically narrow credit spreads. Some participants discussed potential vulnerabilities arising from recent developments in artificial intelligence, including high equity market valuations, significant concentration of market capitalization and operations in a few firms, and rising debt financing levels. A few participants noted the financing of artificial intelligence-related infrastructure in opaque private markets as a point of concern. Several participants highlighted vulnerabilities in the private credit sector, which provides funding to high-risk borrowers and is interconnected with other non-bank financial institutions such as insurers, while banks also have exposure to this sector, necessitating vigilance against related risks. Several participants also raised concerns about hedge funds, including their growing participation and leverage in U.S. Treasury and equity markets, as well as the expansion of relative value trading, which could make the Treasury market more sensitive to shocks. Two participants noted that although household credit quality remains generally sound, financial conditions for middle- and lower-income families have shown signs of deterioration. A few participants pointed out the need to monitor potential spillover effects from volatility in global bond and foreign exchange markets.

During this monetary policy discussion, participants noted that inflation remains slightly elevated, with various indicators showing robust expansion in economic activity. New job additions have remained low, and the unemployment rate has shown signs of stabilization. Against this backdrop, almost all participants supported maintaining the current federal funds rate target range at this meeting, with only two participants favoring a rate cut. Participants supporting the unchanged rate generally believed that after cumulative reductions of 75 basis points by 2025, the current monetary policy stance is within the estimated range of the neutral rate. They stated that keeping rates unchanged at this meeting would allow policymakers to better assess the magnitude and timing of future policy rate adjustments based on new data, changes in the economic outlook, and risk balance. Participants inclined towards a rate cut argued that the current policy rate remains significantly restrictive, and downside risks in the labor market are a more prominent concern compared to the persistent risk of elevated inflation.

Regarding the monetary policy outlook, several participants indicated that further reductions in the federal funds rate target range may be appropriate if inflation eases as expected. Some participants believed that the committee needs to maintain stable rates for a period to prudently evaluate new data; several judged that unless there are clear signs that the downward trajectory of inflation is back on track, no further easing measures are necessary. Several other participants expressed support for a two-way statement on future interest rate decisions, meaning that an increase in the federal funds rate target range could also be appropriate if inflation remains persistently above target. All participants unanimously agreed that monetary policy does not follow a predetermined path and will be adjusted based on new data, evolving economic prospects, and the balance of risks.

When discussing risk management considerations for the monetary policy outlook, the vast majority of participants believed that recent downside risks in employment have eased, but inflation persistence risks remain. Some participants indicated that these two types of risks have become more balanced. Several participants cautioned that further easing amid still-elevated inflation might be interpreted as policymakers weakening their commitment to the 2% inflation target, potentially entrenching high inflation. Conversely, a few participants emphasized that labor market conditions could deteriorate significantly while expressing confidence that inflation will continue to decline. They warned that maintaining an overly restrictive policy could lead to further labor market weakening. Participants agreed that achieving the committee’s dual mandate goals requires prudent balancing of various risks.

Committee Policy Actions

During this monetary policy discussion, members unanimously agreed that various indicators show robust expansion in U.S. economic activity. Almost all members acknowledged that recent developments in the labor market indicate continued low levels of new job creation and signs of stabilization in the unemployment rate. Similarly, considering the latest inflation data, members unanimously agreed that inflation remains slightly elevated and decided to remove comparisons with early last year’s levels from the statement as the new year begins. Members unanimously concurred that the committee is monitoring two-way risks related to its dual mandate, but almost all members believed that recent downside risks in employment have not increased.

To achieve policy objectives, almost all members decided to maintain the federal funds rate target range at 3.5%-3.75%, with two members dissenting and favoring a 25-basis-point reduction. Members unanimously agreed that when determining the magnitude and timing of future adjustments to the federal funds rate target range, the committee will carefully assess new data, changes in the economic outlook, and the balance of risks. They also unanimously agreed that the post-meeting statement should reaffirm the committee's firm commitment to achieving full employment and returning inflation to the 2% target.

Members unanimously agreed that when assessing the appropriate monetary policy stance, the committee will continuously monitor the impact of new information on the economic outlook. If risks emerge that could impede the achievement of objectives, the monetary policy stance will be adjusted accordingly. Members also unanimously agreed that assessments will comprehensively consider various information, including labor market conditions, inflation pressures and expectations, as well as financial and international market dynamics.

After the discussion concluded, the committee voted to direct the Federal Reserve Bank of New York, until further notice, to execute system open market account transactions according to the following domestic policy directive, released at 2:00 PM that afternoon:

Starting from January 29, 2026,Federal Open Market Committeeinstructed the Open Market Trading Desk to carry out the following operations:

Conduct necessary open market operations to maintain the federal funds rate within the target range of 3.5%-3.75%;

Conduct standing overnight repurchase agreement operations at an operation rate of 3.75%;

Conduct permanent overnight reverse repurchase agreement operations with a bidding rate of 3.5% and a daily limit of $160 billion per counterparty.

Expand the scale of securities holdings in the system open market account by purchasing short-term government bonds and, when necessary, other government bonds with residual maturities of up to three years, to maintain an adequate level of bank reserves.

The principal of maturing government bonds held by the Federal Reserve will be fully rolled over through auctions, and the principal of maturing agency securities will be entirely reinvested.

Editor/joryn