Wall Street analysts believe that despite the government's rapid implementation of alternative tariffs, the effective tax rate has slightly decreased, and policies have trended towards moderation after July. The core variable of the ruling lies in potential refunds amounting to as much as $180 billion, of which approximately $120 billion may be converted into stimulus payments for the middle class prior to the midterm elections. As inflation transmission is largely complete, the direct impact of the ruling on economic growth and prices is limited; however, it may support the economy through fiscal expansion and lead to a weaker medium-term outlook for the US dollar due to restrictions on tariff tools.

After the U.S. Supreme Court overturned Trump's tariffs implemented under the International Emergency Economic Powers Act (IEEPA), major Wall Street investment banks believed that the ruling would have a limited actual impact on the economy and markets, but it created room for a milder tariff policy in the second half of the year. Additionally, it might give rise to a voter tax rebate program as large as $120 billion. Analysis from Goldman Sachs and Morgan Stanley showed that the effective tariff rate would only decrease slightly by about one percentage point, with inflation transmission largely completed, while tariff expirations after July would force the government to adopt more exemption measures.

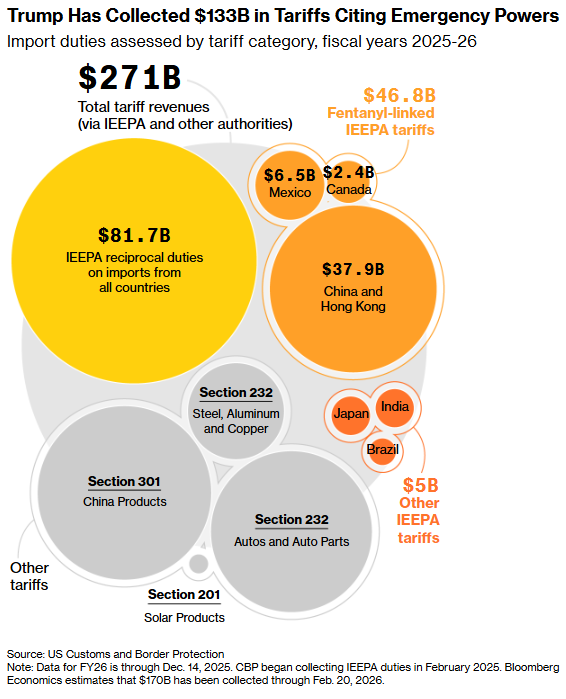

According to CCTV News, on the 20th, the U.S. Supreme Court ruled that the U.S. government's imposition of large-scale tariffs was 'overreaching.' In a 6-3 vote, the court ruled that the tariffs imposed by the Trump administration under the International Emergency Economic Powers Act (IEEPA) were unconstitutional. According to CCTV, on the 21st, Trump announced an increase in the newly imposed 'global import tariff' rate from 10% to 15%. These tariffs will remain in effect until July 24, after which more enduring tariff measures may be implemented under Section 301.

According to Goldman Sachs estimates, following the policy adjustment, the increase in the effective tariff rate since early 2025 will drop from just above 10 percentage points to around 9 percentage points, generally in line with prior market expectations. Morgan Stanley noted that assuming the current tariff structure shifts to different legal authorizations and remains largely unchanged, and with limited rebate sizes (with $85 billion as the midpoint estimate), there will be no significant changes in corporate spending or hiring intentions.

According to Goldman Sachs estimates, following the policy adjustment, the increase in the effective tariff rate since early 2025 will drop from just above 10 percentage points to around 9 percentage points, generally in line with prior market expectations. Morgan Stanley noted that assuming the current tariff structure shifts to different legal authorizations and remains largely unchanged, and with limited rebate sizes (with $85 billion as the midpoint estimate), there will be no significant changes in corporate spending or hiring intentions.

Significant uncertainties remain regarding the rebate issue. The Supreme Court did not specify whether the government must refund the tariffs or provide a timeline. Goldman Sachs estimated that about $180 billion in IEEPA tariffs had been collected, most of which would be refunded in batches over the next year. Since U.S. consumers bore approximately 90% of the tariff burden, this essentially provided Trump with an opportunity to distribute up to $120 billion in stimulus payments directly to the middle class before the midterm elections.

Limited actual decline in tariff rates; inflationary pressures past their peak

Despite the Supreme Court overturning the IEEPA tariffs, Wall Street believes the impact on inflation and economic growth will be extremely limited. Goldman Sachs' analysis indicated that the transmission of tariff costs to consumer prices is largely complete.

Goldman Sachs estimated that as of January, tariff transmission had pushed up the core Personal Consumption Expenditures Price Index (PCE) by approximately 0.7%, and would only add another 0.1% to prices for the remainder of 2026. For goods subject to tariffs for ten months, the tariff transmission rate has exceeded 60%, with incremental transmission being minimal after the first five months, indicating that most price transmission occurred prior to the Supreme Court's ruling. Goldman Sachs assumed the transmission rate would peak at 70%.

Goldman Sachs Chief Political Economist Alec Phillips pointed out that despite the slight decline in the effective tariff rate, the bank does not expect net deflation effects for the remainder of 2026, as companies are reducing prices in response to tariff cuts much more slowly than they raised prices due to earlier tariff increases. However, price increases for most goods facing tariff reductions will be lower than usual levels going forward.

In terms of economic activity, the latest changes will most directly affect U.S. imports. Tariff rates for certain countries will drop significantly, potentially leading to rebounds in their exports to the U.S. from depressed levels in Q1 and Q2. However, Goldman Sachs believes the impact on GDP will likely be offset by increased inventory accumulation, reduced imports from other re-export trading nations, and slight declines in imports from tariff-increased countries.

Goldman Sachs set its Q1 2026 GDP tracking forecast at 3.4%, including a 1.3 percentage point contribution from the end of the government shutdown in Q4 2025, implying a more moderate underlying growth rate of 2.1% excluding this special factor. The bank maintained its forecast of 2.5% year-over-year growth for Q4 2026, accelerating by 0.3 percentage points compared to the 2.2% year-over-year growth in Q4 2025, partly reflecting positive policy impulses as tariff drags dissipate and tax cuts boost the economy.

Tariffs may become more relaxed after July, with the scope of exemptions expected to expand.

The statutory limitations of Section 122 provide a key clue for Wall Street that tariff policy may shift towards moderation. The provision caps tariffs at 15% and limits their implementation period to 150 days, "unless Congress passes legislation to extend this timeframe." The executive order signed by Trump on February 20 explicitly stated that the current rate would expire on July 24.

Morgan Stanley believes that although Trump quickly announced an increase in Section 122 tariffs to 15%, the president is expected to quietly pursue a more moderate tariff policy. This implies more exceptions, exemptions, extensions, and similar measures consistent with recent actions taken by the administration over the past few months. This could benefit countries and products ultimately not covered by new Section 232 or Section 301 investigations.

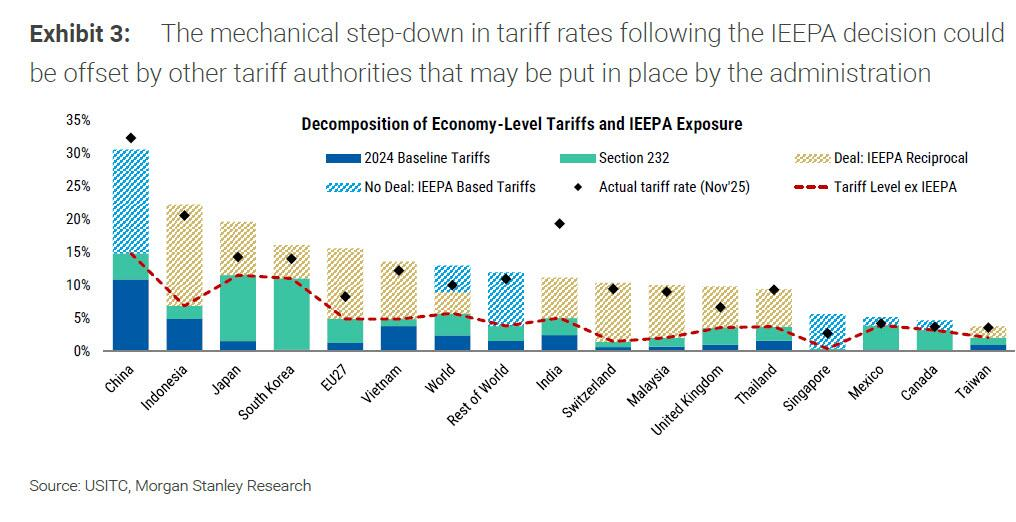

Goldman Sachs provided a detailed analysis of tariff changes faced by different trading partners. Several larger economies, particularly the EU, Japan, and Switzerland, previously reached agreements with the Trump administration to implement a maximum tariff rate of 15%, inclusive of existing U.S. tariffs (typically ranging between 0-2.5%). These trading partners may now face incremental tariff increases as the 15% rate will be "stacked" on top of existing U.S. tariffs.

On the other hand, Goldman Sachs expects that several other trading partners, accounting for slightly more than half of U.S. imports in 2025, have reached agreements with the U.S. and are unlikely to be prioritized in Section 301 investigations. This includes Argentina, Australia, Bangladesh, Cambodia, Ecuador, El Salvador, the EU, Guatemala, India, Indonesia, Japan, South Korea, Malaysia, Switzerland, Thailand, the UK, and Vietnam.

Goldman Sachs anticipates that countries representing approximately 10% of U.S. imports face the greatest risk of near-term Section 301 investigations, including Brazil and South Africa. Overall, Goldman Sachs expects a 15% tariff rate similar to the recently announced one to persist until the end of the year, with exemptions mirroring those under IEEPA tariffs. However, by early 2027, the administration is likely to utilize Section 301 and other authorities to restore tariff rates close to pre-Supreme Court ruling levels.

Morgan Stanley notes that risks point in different directions at various points in time. After July, the risk tends toward lower tariffs, as the administration may struggle to fully replace the expiring Section 122 tariffs using other authorities. However, following the midterm elections and leading into early 2027, the risk shifts towards higher tariffs.

Refund procedures remain uncertain and may serve as a stimulus tool for the midterm elections.

The issue of refunds could evolve into the biggest fiscal policy variable in 2026. The Supreme Court did not mandate whether the Trump administration must refund tariffs or do so within any specific timeframe. Justice Kavanaugh reiterated in his dissenting opinion that the refund process "could become a mess."

Nevertheless, tariff collection may halt immediately. Given the Supreme Court's broad overturning of IEEPA tariff authorization, continued collection would lack legal grounds. This could lead to prolonged uncertainty, as the refund issue will be left to lower courts for deliberation.

Goldman Sachs estimates that the IEEPA tariffs have collected approximately $180 billion to date, with the majority expected to be refunded in installments over the next year or so. In the past, refunds were initially limited to companies that proactively filed complaints or lawsuits through procedures established by Customs and Border Protection (CBP) or the Treasury Department, which could ultimately restrict the scope of refunds.

However, analysis suggests that since various politically motivated media calculations indicate that American consumers bore 90% of the tariff impact, this effectively enabled Trump to distribute stimulus payments to the American middle class before the midterm elections, potentially depositing as much as $120 billion (approximately 90% of the $133 billion in IEEPA tariff refunds) at some point. This could be referred to as the '2026 Trump Tariff Refund Stimulus Plan.'

Morgan Stanley believes that if importers receive refunds but are required to repay them in the form of additional future import tariffs, this would closely resemble the current outcome. However, if the government chooses to allow effective tariff rates to decline during the completion of new Section 232 and Section 301 investigations (most likely occurring later this year or in 2027), this would exert temporary downward pressure on inflation and delay the payment of new import tariffs by businesses until 2027, fostering a more constructive outlook for economic activity growth.

Market Impact: Short-term pressure on U.S. Treasuries, medium-term weakening of the dollar

Wall Street's views on the market impact of the ruling are diverging, with significant differences in short-term and medium-term logic.

In the U.S. Treasury market, Morgan Stanley argues that given the government will utilize other existing authorities to reimpose tariffs, investors' expectations regarding the near-term trajectory of fiscal deficits are unlikely to change. Regarding refunds, the Supreme Court's ruling 'does not address today whether or how the government will refund billions already collected from importers' (quoted from Justice Kavanaugh's dissenting opinion).

Until investors understand the specific contours of the Supreme Court's ruling, they may perceive risks as tilting toward higher rather than lower Treasury yields. As expected, the first wave of market reaction involved investors selling Treasuries because they believed this would force the Treasury Department to accelerate the scale of bond issuance.

However, Morgan Stanley expects this reaction to be short-lived, as most investors will eventually realize that any potential increase in issuance resulting from the ruling will consist primarily of short-term Treasury bills. Another important consideration is that although the Treasury Department may face additional obligations, it does not need to wait for the timing of refunds to begin rebuilding its General Account (TGA) balance. Therefore, Morgan Stanley anticipates a second, more sustained response where investors 'buy on the fact' and push yields lower as their focus shifts back to the downside risks of inflation.

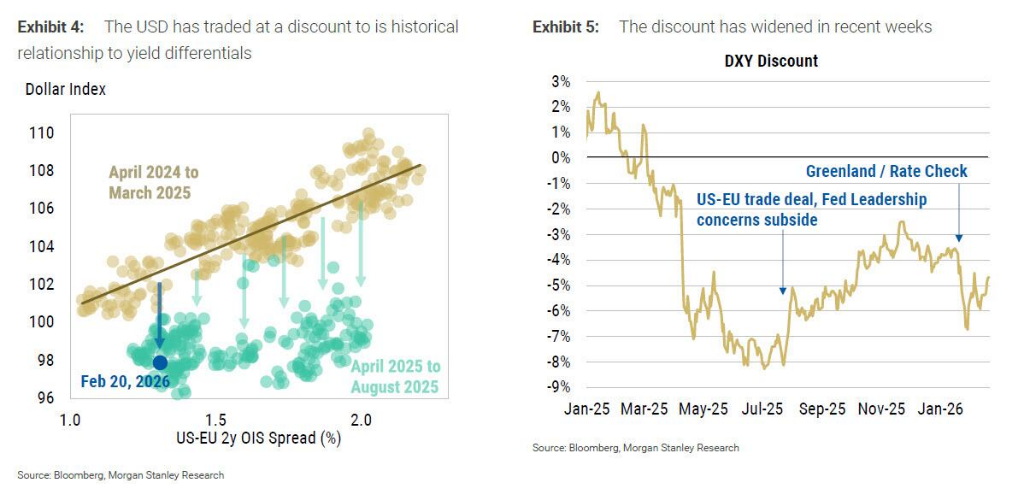

In the dollar market, Morgan Stanley expects reduced scope for the U.S. government to use immediate tariff authorization as a foreign policy tool, potentially marginally lowering the negative risk premium associated with investors maintaining caution about holding dollar exposure.

However, offsetting factors may sustain (or even widen) this negative risk premium for the dollar, including geopolitical uncertainties and questions surrounding U.S. monetary policy. Additionally, a mechanical positive impact on global growth (as tariffs imposed under different authorities take time to implement and may be applied at lower levels) could boost global growth expectations, further weighing on the dollar. Thus, Morgan Stanley continues to anticipate a decline in the dollar.

Goldman Sachs emphasized that tariff rates in some countries will decrease significantly, and imports from these countries to the U.S. may rebound from a low level in the first and second quarters, although the impact on GDP is expected to be offset by other factors. This shift in trade flows will also have differentiated effects on the currencies of different countries.

Overall, Wall Street believes that while the Supreme Court ruling is of significant importance from a legal perspective, its economic and market impact is relatively moderate. The real uncertainty lies in the path of tariffs after July and how tax rebates will translate into actual fiscal stimulus—both factors could bring unexpectedly positive impacts to the market in the second half of the year.

Futubull AI:Your portfolio manager! Your stock-picking advisor!

Futubull AI:Your portfolio manager! Your stock-picking advisor!

Editor/Rocky