①Amid the Middle East conflict, the performance of traditional safe-haven assets such as U.S. Treasuries currently appears even weaker than that of riskier assets like U.S. stocks… ②Market data shows that while U.S. stocks rebounded strongly on Wednesday, the sell-off in U.S. Treasuries continued unabated.

Amid the Middle East conflict, traditional safe-haven assets like U.S. Treasuries currently appear to be faring even worse than risk assets such as U.S. stocks…

Market data shows that while U.S. stocks staged a strong rebound on Wednesday, the sell-off in U.S. Treasuries showed no signs of abating — the yield on the benchmark $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ climbed for a third consecutive trading session on Wednesday, closing up 3.65 basis points at 4.096%. Bond yields move inversely to prices.

From this week’s performance, the U.S.-led attack on Iran has nearly brought an end to weeks of gains in U.S. Treasuries and pushed the yield on the 10-year Treasury note back above 4%, a development that could increase borrowing costs for businesses and consumers in the future.

From this week’s performance, the U.S.-led attack on Iran has nearly brought an end to weeks of gains in U.S. Treasuries and pushed the yield on the 10-year Treasury note back above 4%, a development that could increase borrowing costs for businesses and consumers in the future.

Although previous similar geopolitical conflicts typically caused stock market turbulence while prompting investors to seek refuge in bonds, this time, the safe-haven appeal of U.S. Treasuries has clearly dimmed.

Many bond traders attribute this primarily to the rise in energy prices driven by the Middle East conflict. For investors, the impact of rising energy costs is now more critical, fueling concerns about a resurgence in inflation, which in turn drags down bond prices.

The recent sell-off in U.S. Treasuries has also disappointed many, as yields had appeared poised to break below the lower boundary of their recent trading range. The 10-year Treasury yield plays a significant role in determining borrowing costs across the economy; its decline in February helped push 30-year mortgage rates to their lowest level in over three years — below 6%.

Zach Griffiths, Head of Investment-Grade Bonds and Macro Strategy at research firm CreditSights, noted, “The market is now reflecting renewed concerns about the long-term effects of inflation, while typical safe-haven capital flows have shown less pronounced characteristics.”

Inflation Threats Loom Over Bond Market

For investors, the biggest threat from inflation is that it may force the Federal Reserve to raise short-term interest rates or at least refrain from cutting them as much as expected. Rising rates would enhance the attractiveness of alternative investments such as money market funds, thereby diminishing the value of medium- and long-term U.S. Treasuries.

From the current situation, a significant rise in oil and gas prices is highly likely to push up the overall inflation index. Since Iran was attacked last weekend, international crude oil prices have surged by approximately 12%, reaching their highest level since June of last year.

Although Fed officials typically focus on core inflation, which excludes volatile food and energy categories, substantial energy price shocks will undoubtedly be treated differently. Such shocks tend to spread to other commodity prices, prompting businesses and consumers to begin expecting higher inflation in the coming years — economists warn that this expectation could become a self-fulfilling prophecy.

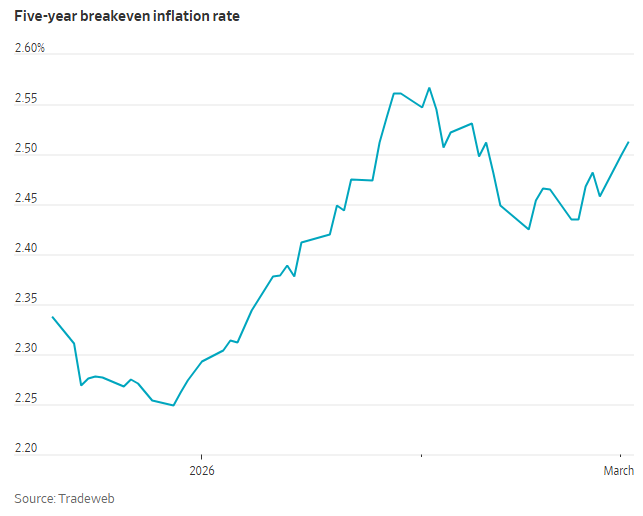

In fact, the conflict in the Middle East has already driven up certain market-based inflation expectations this week. The gap between the five-year nominal Treasury yield and the five-year Treasury Inflation-Protected Securities (TIPS) yield — known as the 'breakeven inflation rate' — rose from 2.46% on Friday to above 2.5%.

At the same time, investors have scaled back expectations for two Federal Reserve interest rate cuts this year. According to federal funds futures, the probability of two rate cuts fell from 79% on Friday to about 55%.

Even before the latest risks to the inflation outlook emerged, the Federal Reserve was already facing persistent price pressures indicated by its preferred inflation gauge — the core Personal Consumption Expenditures (PCE) price index. Based on estimates of January's consumer and wholesale prices, the January core PCE price index, due to be released next week, is expected to record its largest month-over-month increase in a year.

Notably, U.S. Treasuries have sometimes decisively moved in one direction and then completely reversed when faced with new dual threats in the past. A clear example occurred in April last year after Trump announced tariffs, when Treasuries initially rose before plummeting sharply.

Currently, some investors remain optimistic about U.S. Treasuries.

John Madziyire, head of U.S. Treasuries at Vanguard Group, stated that his baseline expectation is that as tariff impacts fade and inflation eases, the Fed will restart rate cuts in the second half of the year, at which point long-term yields will test lower levels.

He also pointed out that if the conflict with Iran persists, leading to rising energy prices, it may hinder the rate-cutting process. However, such a move would also weigh on economic growth, prompting investors to return to long-term Treasuries as a safe haven. 'The current yield levels are quite attractive, and volatility will create more opportunities for us,' he said.

Editor/Rice