Nio achieved a historic breakthrough in Q4 2025, turning its first quarterly profit. Revenue for Q4 reached 34.65 billion yuan, with deliveries surpassing 124,000 vehicles, both setting new historical records. Gross margin for vehicle sales surged to 18.1%, resulting in a quarterly net profit of 727 million yuan. Through organizational optimization and cost reduction via technology, Nio significantly improved its operational leverage. Looking ahead to Q1 2026, the company forecasts deliveries to reach between 80,000 and 83,000 vehicles, corresponding to a revenue range of 24.48 billion to 25.18 billion yuan, representing a year-over-year increase of over 100%.

In the fourth quarter of 2025, $NIO Inc (NIO.US)$ / $NIO-SW (09866.HK)$ The company delivered an inspiring set of results to the market. In Q4, it achieved several historic milestones: both delivery volume and revenue hit record highs, and it turned its first quarterly operational and net profit.

At the start of US trading, Nio surged more than 10%.

On March 10, Nio released its unaudited financial report for the fourth quarter and full year of 2025. Key data showed:

On March 10, Nio released its unaudited financial report for the fourth quarter and full year of 2025. Key data showed:

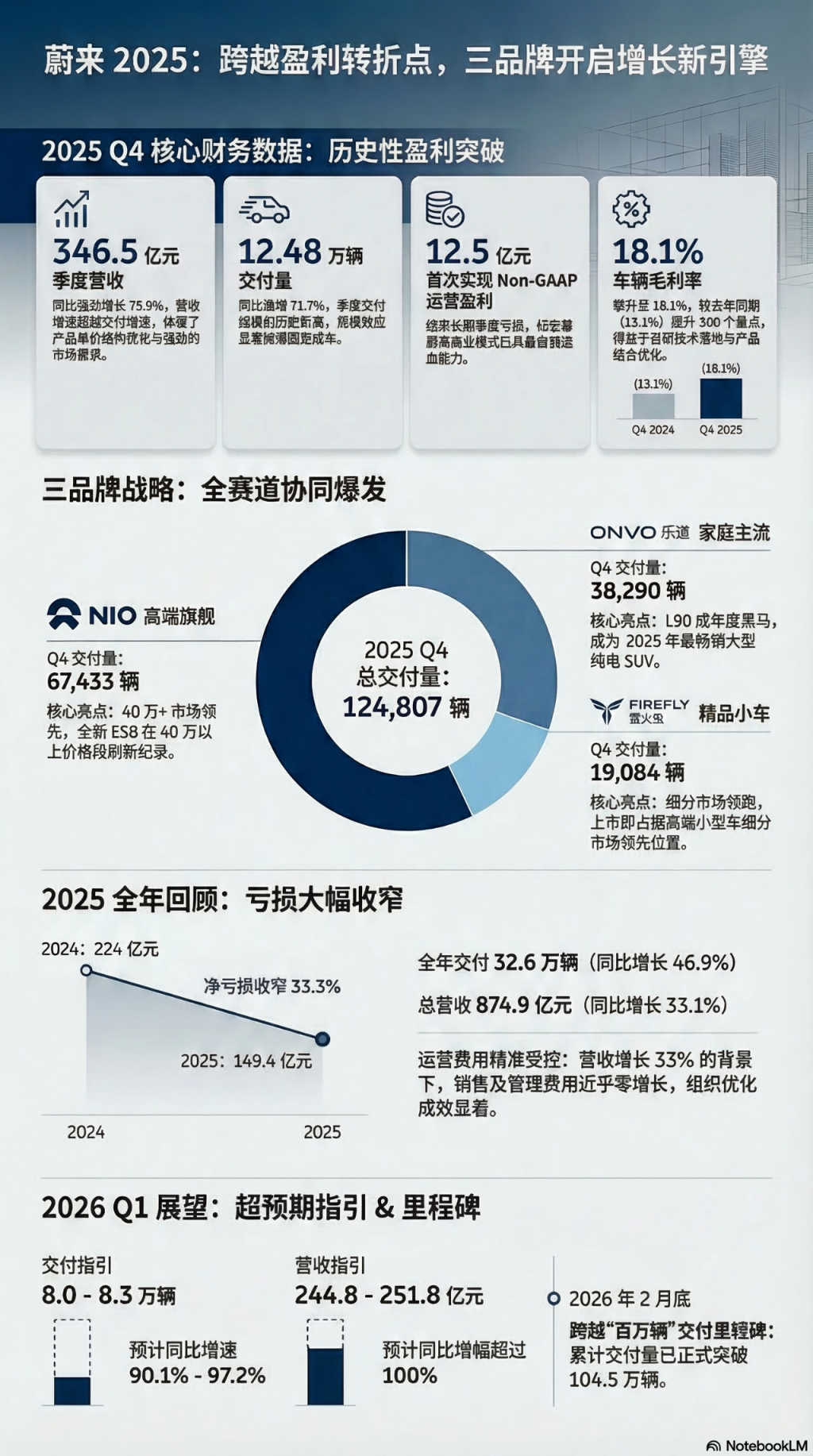

Nio's Q4 2025 revenue reached RMB 34.65 billion, a significant year-on-year increase of 75.9%;

Fourth-quarter deliveries reached 124,807 units, a year-on-year increase of 71.7%.

Q4 vehicle gross margin soared to 18.1%.

Under non-GAAP (Non-GAAP), adjusted operating profit reached RMB 1.251 billion, with adjusted net profit reaching RMB 727 million.

From the perspective of annual performance and forward guidance, Nio’s growth flywheel has been set in motion. In the full year of 2025, Nio's total revenue reached RMB 87.488 billion, a year-on-year increase of 33.1%, with the annual net loss narrowing by 33.3% year-on-year. At the same time, the company provided extremely robust guidance for the first quarter of 2026, predicting that Q1 deliveries would reach between 80,000 and 83,000 vehicles, corresponding to a revenue range of RMB 24.48 billion to RMB 25.18 billion, representing a year-on-year increase of over 100%. The comprehensive implementation of Nio's multi-brand strategy, coupled with deep cost reductions and efficiency enhancements, is reshaping this new force in automobile manufacturing.

Synergy of three brands: ONVO and FIREFLY become new engines

Nio’s delivery surge in Q4 was not driven by a single brand but rather by the parallel efforts of three key brands. Among the 124,807 deliveries, the flagship brand NIO contributed 67,433 units, the family-oriented brand ONVO contributed 38,290 units, and the small premium brand FIREFLY contributed 19,084 units.

In terms of product highlights, the all-new Nio ES8 maintains a strong delivery momentum, setting a new monthly delivery record in the price segment above 400,000 yuan; ONVO L90 has become the best-selling large pure electric SUV in 2025; and FIREFLY has consistently led in the premium small car segment since its launch. These three brands cover three major tracks: high-end flagship, mainstream family, and premium compact vehicles, collectively forming Nio's multi-dimensional layout in the mid-to-high-end electric vehicle market.

Notably, the addition of ONVO and FIREFLY not only contributed to an increase in delivery volume but also, to some extent, drove the optimization of the average selling price structure – the earnings report explicitly stated that Q4 vehicle average selling prices benefited from a more favorable product mix, significantly improving gross margin.

Gross Margin Leap: Driven by Both Scale and Structure

The quarterly vehicle gross margin of 18.1% marks an unprecedented high point in Nio's history. This surge is the result of multiple compounding factors:

Economies of scale have become evident. The sharp increase in Q4 deliveries has made the dilution of fixed costs increasingly apparent. Although vehicle sales costs increased by approximately 70% year-over-year, this growth rate was significantly lower than the revenue growth rate of 80.9%, indicating the initial release of scale leverage.

Product mix continues to optimize. The increasing proportion of higher-priced and high-specification models directly improved both the average selling price per vehicle and the gross profit per vehicle.

Cost reductions from proprietary technology have been realized. CEO William Li highlighted in the earnings call that the company’s self-developed core intelligent electric vehicle technologies have continued to be mass-produced, “enhancing product competitiveness while delivering meaningful cost-efficiency improvements” – indicating that previous substantial R&D investments are now yielding scalable cost optimization returns.

For the full year, the vehicle gross margin improved from 12.3% to 14.6%, and the overall gross margin rose from 9.9% to 13.6%, showing a clear upward trend. With continued expansion in delivery scale, further room for improvement remains.

Significant Reduction in Operating Expenses: Organizational Optimization Yields Notable Results

Q4 R&D expenses amounted to 2.03 billion yuan, a significant year-over-year decrease of 44.3%; sales and general administrative expenses were 3.54 billion yuan, down 27.5% year-over-year.

The main source of cost reduction stems from the organizational optimization initiated in the first half of 2025 —— the streamlining of personnel directly cut labor costs in R&D and marketing departments, while design and development expenses also decreased due to new models being at different stages of development.

On an annual basis, R&D expenses declined by 18.7% from 13.04 billion yuan in 2024 to 10.6 billion yuan; sales and administrative expenses remained largely flat, increasing only slightly by 2.2% to 16.09 billion yuan. This combination —— with operating expenses showing near-zero growth against a backdrop of 33% revenue growth —— is the core logic behind Nio's rapid improvement in operational leverage.

It is worth noting that despite the decline in absolute R&D investment, Li Bin clearly stated that in 2026, the company will "continue to firmly invest in twelve full-stack core technologies," and future trends in R&D expenses remain to be monitored.

On February 26, 2026, Shenji (Shenji/GeniTech), a Nio subsidiary responsible for intelligent driving chip operations, completed a significant round of external financing totaling 2.257 billion yuan. After the financing, Nio still holds a controlling stake of 62.7%, external investors collectively hold 27.3%, and the remaining 10% is allocated to an equity incentive plan.

Cash Reserves and Liquidity: Holding 45.9 billion yuan in 'ammunition,' but liquidity remains a concern.

As of December 31, 2025, Nio’s total cash and cash equivalents, restricted cash, short-term investments, and long-term fixed deposits amounted to 45.9 billion yuan (approximately 6.6 billion US dollars), providing ample 'ammunition' for the company’s ongoing operations.

Current liabilities of 78.58 billion yuan significantly exceed current assets of 76.63 billion yuan, with the current ratio slightly below 1. This is why Nio’s financial report separately addressed its 'ability to continue as a going concern.' The company stated in the report that, considering factors such as revenue growth, improved operational efficiency, and available bank credit lines, it expects existing funds to be sufficient to support normal operations over the next twelve months.

In terms of cash flow trends, both Q3 and Q4 achieved positive operating cash flows, a rare performance since Nio’s inception and an important signal of easing liquidity pressure. With continued expansion in scale and further improvements in profitability, this pressure is expected to be substantially alleviated in 2026.

On March 6, Nio’s board approved the granting of 248 million restricted stock units (RSUs) to founder, chairman, and CEO Li Bin. These RSUs will vest in ten tranches, with vesting conditions tied to specific performance targets related to the company’s market value and net profit. Additionally, Li Bin must continue to serve in a key executive role.

Q1 2026 Outlook: Revenue is expected to double, with growth momentum continuing.

For the first quarter of 2026, Nio provided guidance that significantly exceeded market expectations: deliveries are projected to reach 80,000 to 83,000 units, representing a year-on-year increase of 90% to 97%; revenue is expected to range from RMB 24.48 billion to RMB 25.18 billion, with a year-on-year growth exceeding 100%, marking another doubling in performance.

It should be noted that the delivery guidance for Q1 2026 (80,000-83,000 units) shows a noticeable decline compared to 124,807 units in Q4 2025, primarily reflecting the normal impact of seasonal factors such as the Spring Festival holiday. On a year-on-year basis, growth of over 90% clearly demonstrates the robust demand momentum across the three brands. CFO Qu Yu also stated in the earnings report that 2026 will continue to focus on enhancing operational efficiency and optimizing cost structures, "to consistently deliver stronger and more sustainable results for users, partners, and shareholders."

Editor/Rocky