This article is sourced from: Sixiang Gangyin

Valuation can only be relatively reasonable.

The recent market has been like a nightmare for long-term value investors, especially due to the collapse of Moutai, the valuation anchor of value investing, which has caused the entire valuation system to waver.

Long-term investment primarily seeks to profit from corporate growth, but the volatility of valuations in the A-share market far exceeds the growth in performance. It is like passengers walking on a train that speeds up and slows down unpredictably, unable to discern their true speed. Similarly, investors find it difficult to distinguish what proportion of current stock price fluctuations stem from changes in performance versus changes in valuation. This is why value investing requires a high margin of safety.

However, the margin of safety you calculate cannot shield against volatility that exceeds your ability to assess valuation. Events like the sharp devaluation of Moutai, though relatively rare, serve as a powerful reminder that valuation can only be relatively reasonable, not absolutely so.

However, the margin of safety you calculate cannot shield against volatility that exceeds your ability to assess valuation. Events like the sharp devaluation of Moutai, though relatively rare, serve as a powerful reminder that valuation can only be relatively reasonable, not absolutely so.

In other words, valuation is not an objective standard but rather a subjective perspective reflecting investors' judgment of a company's value.

Alternatively, valuation is a result continuously shaped by various factors.

Although the criteria for assessing valuation are subjective, complex, and dynamic, in order to roughly evaluate the probability of investment success, the odds, and the margin of safety, we must still strive to align with mainstream valuation standards.

I categorize the most common factors influencing valuation into four levels:

First level: Company fundamentals

Second level: Corporate life cycle

The third level: Industry cycle

The fourth level: Market style cycle

The objective of this article is to systematically review the factors influencing valuation. These factors have been covered in previous articles in the valuation series, so each valuation factor will not be discussed in great detail.

02 The first level of valuation: Company fundamentals

There are many factors related to valuation, primarily including growth rate, industry characteristics, business model, competitive landscape, and financial risk. If one can grasp this level, most valuation conclusions will be reliable.

Growth rate

The PEG valuation method, which investors are most familiar with, assigns a valuation based on the growth rate. This falls under the level of fundamental valuation.

Although the growth rate is the most important valuation factor, the factor with the greatest influence is ——

Industry characteristics

Industry characteristics are the most influential factors on the valuation level. Banks typically have a PE ratio of only a few times, while some TMT industries have PE ratios of dozens of times. Many investors tend to question the valuation systems of these industries based on the PEG ratio, believing that the market will correct this 'incorrect' valuation.

Business model

Those capable of generating long-term stable cash flows are often assigned higher valuations by the market. This explains why project-based companies in the computer software industry typically have low PE ratios, whereas SaaS companies are valued much higher. This serves as a classic example of how business models influence valuation.

Investors need to continuously monitor business models that the market recognizes and is willing to assign premium valuations to.

Competitive landscape

When comparing two companies with similar conditions otherwise, the leading company can often command a higher valuation. This represents a premium arising from competitive positioning, a phenomenon prevalent across most industries.

Similarly, if an industry previously suffered from poor competitive dynamics, such as frequent price wars, but has since improved after undergoing mergers and consolidations, allowing key enterprises to reset pricing strategies, this improvement in stability and performance growth can lead to an increase in the valuation of related companies.

Financial risk

Companies that have long been suspected of financial fraud often experience significant valuation discounts until these allegations are disproven. Examples include Kangde Xin and Kangmei Pharmaceutical, which illustrate the “low valuation trap” set for unsuspecting retail investors.

The above factors represent the valuation elements at the fundamental level, where earnings growth rate is considered a 'growth factor,' while the other four are 'certainty factors.' Together, they explain the valuation of most companies with stable performance at a given point in time.

However, enterprise operations are a dynamically evolving process, and valuation should also reflect a dynamic outcome. The second and third levels of valuation involve adopting a developmental and dynamic perspective.

Level Two of Valuation: Enterprise Lifecycle

Before 2015, A-shares tended to assign high valuations to small companies, justified precisely by this lifecycle.

There is a core underlying logic to corporate valuation: the valuation of a company equals the discounted value of its future perpetual cash flow.

Assume a small company with only one million in profits. If we can clearly foresee that the discounted value of its future growth cash flows could reach a market capitalization of hundreds of billions, theoretically, the market could assign it a PE ratio of 100,000 times.

Of course, this is just an exaggerated assumption, but it represents a way of thinking about valuation. If a company convincingly demonstrates to the market its enormous future growth potential, it can receive a valuation far exceeding its current growth rate.

The most typical example is CATL. When it first went public, its market capitalization was already in the tens of billions. Its profit growth rate was similar to what it is now, but at that time, it was valued at over a hundred times earnings, whereas now it trades at only twenty to thirty times earnings.

Therefore, the notion that small companies should be given high valuations is not entirely accurate. The lifecycle does not refer to the age or size of the company. For companies of the same scale, those demonstrating significant future growth potential are in their early growth phase and can command high valuations; those with limited growth prospects are mature companies in their lifecycle and will receive relatively low valuations.

Overall, long-term stock holding requires a focus on growth potential. Total market capitalization is a very important metric, and the mindset must shift from price-per-share coordinates to market-cap coordinates. For instance, instead of remembering a company as 'EPS 0.6, 30x PE, 18 yuan,' think of it as '600 million in profits, 30x PE, 18 billion market cap.'

The tenfold stocks of the future are highly likely to emerge from companies with market caps below 10 billion, while companies above 100 billion in market cap are almost impossible. For companies worth several hundred billion, strict conditions apply: either there is substantial room for industry penetration, or they are in a phase of rapid consolidation within a large industry, or outstanding enterprises are severely undervalued due to industry distress.

Certainly, in terms of growth certainty, mature companies have a slight edge. Therefore, if investing in large-cap companies with market values exceeding 100 billion, one must look for companies with clear competitive advantages and strong staying power within industries that have trillion-dollar market potential.

04 The third level of valuation: Industrial cycle

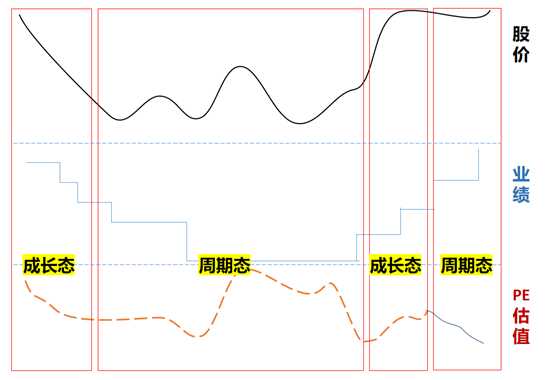

The third level of valuation is the industrial cycle, where the entire valuation range exhibits cyclical fluctuations.

Many investors consider commodities such as non-ferrous metals, steel, and pork to be cyclical industries. In reality, everything has a cycle; it's just a matter of degree. Consumer goods like baijiu are growth stocks, and high-end manufacturing sectors in TMT, such as semiconductors and new energy, are also growth stocks. The former represents long-term growth cycles, while the latter reflects industry trend-driven growth, which typically sustains high growth for only two to three years and remains more constrained by cyclicality.

It can be said that all stocks possess growth potential, and every company exhibits cyclicality. Their stock prices therefore reflect both 'cyclical states' and 'growth states.'

Growth state: During periods of rising performance, both profits and valuations increase (a Davis Double Play); during downturns, both earnings and valuations decline (a Davis Double Whammy). The emphasis here is not on the daily changes in valuation but on the overall shift in the valuation range.

This volatility is easy to understand. However, when a company's performance declines, it is often anchored by previous earnings forecasts, giving the impression of being undervalued. Therefore, when stock prices fall, it is crucial to distinguish whether it is the valuation itself that is cheap or if it is a decline in the valuation range.

Cyclical state: High valuation at the low point of the cycle, low valuation at the high point of the cycle.

In the peak and trough areas of large cycles, fluctuations occur where performance is poor but stock prices rise instead of falling, or where performance is good but stock prices fall instead of rising.

This type of valuation fluctuation is also easy to understand. Experienced investors naturally recognize this when dealing with strongly cyclical industries. However, when it comes to industry trend investing, due to cycles often lasting two to three years, investors may overlook this cyclical aspect of valuation, especially during boom periods, mistakenly believing that high prosperity implies cheap valuation. This error arises from mistaking a downward industry trend for undervaluation.

From Ping An to Maotai, from Hikvision to CATL, there will be more high-valuation giants exposed as their true nature emerges when they enter a downward cycle.

The fifth level of valuation: Market style.

The third level of valuation pertains to major market cycles or style cycles, which differ from index fluctuations. It involves internal structural adjustments irrespective of index movements, where the valuation of certain industries and sectors rises while that of others falls.

Typical shifts in market style include size-based styles (large-cap versus small-cap), growth versus value styles, and thematic trends (i.e., sector beta reinforcement).

The first three levels are related to companies or their respective industries, which investors may focus on to varying degrees. However, this factor is unrelated to companies or industries but rather stems from the inherent cyclical volatility of the capital market, lacking the pronounced significance of index movements. For example, the recent decline in Moutai reflects an overall reduction in valuation across leading consumer stocks.

Given the rarity of such occurrences, coupled with the belief among value investors that 'spending one more minute on macro analysis is a wasted minute,' even experienced investors often realize this too late, by which time stock prices have typically already fallen significantly.

How does one assess changes in market style? Various strategies offer insights. For instance, when the economy begins recovering from a trough, small-cap stocks tend to outperform due to greater earnings and valuation elasticity, leading to small-cap rallies like those seen in the first half of 2019. Conversely, during economic downturns, large-cap stocks exhibit stronger resilience, resulting in large-cap rallies as observed in 2020.

Overall, market style represents a chaotic system influenced by numerous factors, making it difficult to predict. Investors can only passively endure its effects.

More importantly, do not mistake gains attributed to style shifts as profits earned through personal skill. The large-cap revolution from 2017 to 2021 reversed the previous preference for small-cap stocks. Low-valuation large-cap stocks sustained valuation increases for over three years, enabling many long-term investors to multiply their returns. Many believed this was due to their adherence to long-term value investing, unaware that these gains were simply a result of the four-year dominance of large-cap style.

Gains brought by style shifts, whether thematic trends or blue-chip stocks, are merely temporary placements in your portfolio, subject to reversal at any time.

06 Three Methods of Valuation

To summarize, here are the four levels influencing valuation.

The first level: company fundamentals, including earnings growth rate, industry characteristics, business model, competitive landscape, and financial risks.

The second level: the enterprise life cycle, with high valuations in the early and growth stages, and a decline in valuation upon entering the maturity stage.

The third level: the industrial cycle, divided into growth phases and cyclical phases. The growth phase involves the Davis Double Play and Davis Double Whammy, while the cyclical phase sees high valuations at cycle lows and low valuations at cycle highs.

The fourth level: market style cycles, which represent unreliable, transient, and loss-controlling capital.

From the above four levels, three valuation methods can be summarized.

Method one: consider the reasonableness of valuation comprehensively from these four levels.

The best approach is, of course, to comprehensively evaluate company valuations across these four levels. However, this requires establishing a complete valuation estimation system and making dynamic real-time adjustments. Not to mention retail investors, even institutions cannot fully achieve this.

Method two: consider only the reasonableness of relative valuation.

Among the four levels of valuation, for companies within the same industry, the impacts of the third and fourth levels are identical, and the second dimension is relatively easy to assess. The true differentiation lies in the first dimension, thus giving rise to a relative valuation method.

First, identify a 'valuation anchor' within the industry, typically companies with the most transparent fundamentals, numerous researchers, and minimal market expectation gaps. These are referred to as 'industry valuation anchors.' For example, Moutai for liquor and CATL for batteries.

You can assume that the valuation of certain targets is reasonable by default, then compare the differences between the company and the 'valuation anchor' at the first and second levels to determine the company’s relatively reasonable valuation.

This method is suitable for companies with stable operating conditions and distinct industry characteristics. The advantage is that it is simple, fast, and relatively accurate in valuation. However, the downside lies in the word 'relative,' as it requires constant attention to changes in the valuation of the 'valuation anchor.' Once it changes, the reasonable valuation range for all companies in the sector needs to be adjusted accordingly.

Method Three: Historical Valuation Approach

The idea behind the historical valuation approach is completely opposite to the third method. It does not consider fundamental valuation factors but instead treats the valuation range over the past one or two years as the first level of reasonable valuation, focusing on changes at the second, third, and fourth levels.

For example, if a company's valuation has been in the range of 30 to 50 times over a certain period, with a median of 40 times, we can initially assume 40 times as the midpoint of the reasonable valuation range. Then, assess whether the company’s growth rate will increase or decrease in the future? Will its lifecycle move toward high growth or maturity? Is the overall sector’s valuation cycle trending upward or downward? Is the broader market style cycle moving up or down?

If, after considering these factors comprehensively, it is believed that the valuation range is rising, we can appropriately shift the historical estimation range from 30 to 50 times upward.

This estimation method is very suitable for industries with rapid operational changes, but the downside is that it lacks quantitative precision; how much the range should be shifted up or down depends entirely on experience.

Therefore, it is more suitable for medium- and short-term investments, providing a rough estimate without requiring highly precise valuations.

07 Dare to Let Go

The latter two methods both focus exclusively on one dimension while abandoning other valuation dimensions.

In investment practice, mastering simple methods often yields better results than using complex ones. Therefore, in valuation, one can discard what they cannot grasp and focus only on what they can control.

For bottom-up long-term value investors, focus only on the first and second levels of factors; for top-down industry investors, emphasize the second and third levels of factors to construct a portfolio of individual stocks.

However, as a result, investors must recognize that their valuation methods are flawed and have a significant probability of failure. It is essential to fully consider the margin of safety beforehand and have the courage to terminate an investment upon discovering errors afterward.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/KOKO