Source: KeyPoints Summary

Author: Chang Yuan

On March 13, Cathie Wood, the founder of ARK Invest and known as the 'Oracle of Wall Street,' along with her core research team, provided an in-depth analysis of the 'Big Ideas 2026' report, offering the latest insights into future technological trends.

In this sharing session, ARK Invest focused on the convergence of five major innovation platforms: artificial intelligence (AI), multi-omics, public blockchain, robotics, and autonomous taxis. The team believes that the synergy of these five platforms will trigger an unprecedented acceleration. As a staunch supporter of disruptive innovation, Cathie Wood argues that we are in the midst of a fully unfolding technological revolution, the seeds of which were planted as early as the 1980s and 1990s and are now beginning to take root and sprout.

We have summarized the core information from this podcast, and the key highlights are as follows:

We have summarized the core information from this podcast, and the key highlights are as follows:

1. AI is evolving from simple text-based conversations into agents with long-term execution capabilities.

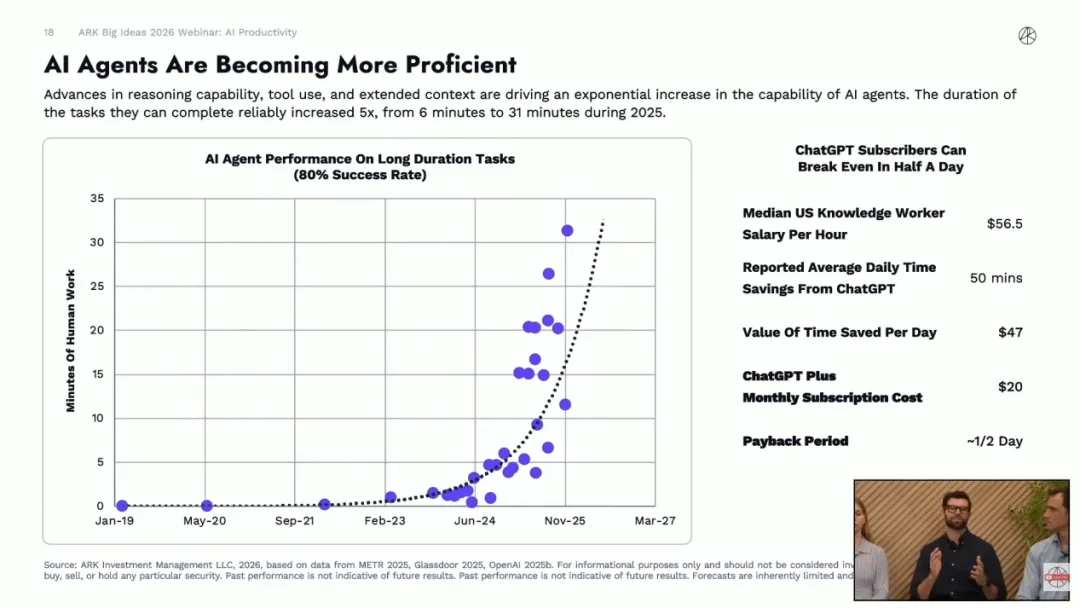

The new computing platform shift brought about by AI is transforming human-computer interaction interfaces from keyboards and touchscreens to natural language. More importantly, AI models are reaching a fundamental tipping point in capability: they are no longer limited to handling short tasks requiring frequent interventions of just five minutes but can now reliably and independently perform complex long-duration tasks lasting over 55 minutes.

This significant boost in productivity will deliver extremely high returns on investment for enterprises. As models progressively gain the ability to generate synthetic data for self-iteration, AI is not only helping companies reduce costs but also creating pure net revenue growth. Driven by this strong commercial demand, AI software spending in the trillions of dollars will fuel a massive surge in computational power and data center infrastructure development.

2. The integration of AI and biology is forming a powerful flywheel that will lead healthcare back to its golden age.

While autonomous driving may become the largest revenue-generating field in the future, the revolutions in multi-omics and genomics represent the most profound and disruptive applications of AI. The fusion of AI and biology is creating a powerful flywheel where vast amounts of data train better models, and those improved models, in turn, enable more precise molecular diagnostics and targeted drug discovery.

The underlying driver of this flywheel is the dramatic drop in sequencing costs. The cost of sequencing a full human genome has plummeted from nearly $3 billion initially to around $100 today and is expected to fall to just $10 by 2030. Biology is becoming the largest data-generating engine on Earth, and with the help of AI, the time required for new drug development will be reduced by 40%. This paradigm shift will allow one-time curative gene therapies to replace long-term chronic disease management, with the economic value of such therapies potentially being 20 times higher than that of traditional drugs.

3. Reusable rockets break cost barriers, ushering in a new era of space infrastructure.

According to Wright's Law, every time the cumulative scale of sending effective mass into orbit doubles, the cost of rocket launches decreases by 17%. With the partial reusability technology of Falcon 9, SpaceX has already reduced launch costs by approximately 95%.

Once fully reusable heavy rockets at the Starship level are achieved, the cost of sending payloads into space will plummet from the current $1,000 per kilogram to less than $100. This magnitude of breakthrough will not only significantly expand satellite communication networks but also make space-based orbital data centers commercially viable. After crossing a specific cost threshold, the cost of AI computing power operating in space could be up to 25% cheaper than on Earth, which is constrained by land and power grid limitations.

4. Driverless taxis represent the first large-scale commercialization of embodied intelligence, transforming a $10 trillion mobility market.

The public often views autonomous driving as merely an advanced driver-assistance feature. However, ARK believes it represents the first large-scale commercial application of embodied intelligence that consumers can encounter in daily life. The key determinant of success in this mobility revolution lies in the per-mile operational cost of the underlying vehicles.

In the future, scaled operations of driverless taxis could reduce mobility costs to as low as 25 cents per mile, which is less than one-tenth of the cost of human-driven ride-hailing services in Europe and the United States. Such low prices will unlock an enormous latent demand for transportation. By the end of this century, driverless taxis are expected to generate a staggering $10 trillion in total addressable market (TAM) revenue. In this emerging ecosystem, platform operators who master core autonomous driving technologies will capture the majority of the economic value.

5. The convergence of five innovation platforms will disrupt global economic paradigms.

In response to current concerns and polarized debates about overinvestment in the technology sector, ARK argues that the current AI infrastructure boom mirrors the railroad construction frenzy of the late 19th century, which once accounted for 75% of the U.S. stock market’s value.

AI, multi-omics, public blockchains, robotics, and autonomous driving—these five innovation platforms have not only individually reached critical mass but are also profoundly reshaping economic paradigms. For instance, the widespread adoption of autonomous driving will convert an estimated $4 trillion annually in hidden human driving time across the U.S. into tangible GDP growth. This is not merely industrial upgrading but a complete overhaul of the fundamental engines driving the global economy.

In the video's conclusion, Cathie Wood emphasized that although disruptive technologies may initially trigger societal anxiety about job losses, historical patterns demonstrate that the AI era will ultimately become a net job creator. As natural language programming dramatically lowers technical barriers, we will witness an unprecedented surge in individual entrepreneurship. Future AI will not just be about computing power and code; it will become an empowering infrastructure for human civilization, enabling innovations across all industries to materialize in the physical world at an unparalleled pace.

The following is a transcript of ARK's video podcast:

1. Five major innovation platforms lay the foundation for economic growth

Cathie Wood: Hello everyone. I am Kathy Wood, CEO and Chief Investment Officer of ARK Invest. Today, together with the research and portfolio management teams, I am pleased to present the highlights of our 104-page research report, 'Big Ideas 2026.' We believe this is the kind of research investment bankers conducted in the 1980s and 1990s after the advent of personal computers, aiming to gain insights into the future of technology. The seeds of that technological revolution were sown then and have continued to sprout. Now, we are in the midst of a full-scale technological revolution, requiring original research to explore the future and understand its implications.

It is an honor to share these findings with you today while introducing two new members of our team who form our Multiomics research group, also known as genomics in Europe. While autonomous driving may be the largest revenue generator, we believe the genomics or multiomics revolution will be the most profound application of AI.

Host: Thank you, Kathy. Good afternoon, everyone. It is exciting to be here sharing 'Big Ideas 2026' and answering selected questions from over 800 submitted. To start, I would like to ask: From a macro perspective, how do the various technologies we observe converge to drive what is called the 'Great Acceleration'?

Researcher: Currently, five major innovation platforms are entering the market, with AI serving as the core driver accelerating all other platforms. The other four platforms include multiomics, public blockchains, robotics, and energy storage combined with autonomous mobility, including RoboTaxis. These five innovation platforms are at critical inflection points, triggering the largest cycle of technological infrastructure investment since the railway era. This not only impacts macroeconomic growth in the short term but also transforms the business landscape through data centers and investments in AI agents (Agents), laying the groundwork for sustained economic growth in the future.

As investments yield positive returns, we expect the global economy to achieve a real compound annual growth rate exceeding 7% by the end of this decade. While the consensus expectation is around 3%, this aligns with historical economic patterns during periods of significant technological transformation. Markets will follow macro trends, and we anticipate that more than 60% of the global stock market capitalization will be attributed to disruptive innovation platforms. The key takeaway is this: You must embrace innovation. If your assets do not center on innovation, their relative value may decline over the next decade. Just as 75% of the U.S. stock market’s value in the late 19th century was attributed to the railway industry, these five platforms will similarly experience explosive corporate valuations. This is what we call the 'Great Acceleration.'

2. AI Infrastructure Construction Boom

Host: Alright. The first specific question is: Are we overbuilding AI infrastructure relative to current energy availability? What impact might this have? Additionally, what about the feasibility and economics of space-based data centers? What technological and commercial milestones need to be achieved for them to compete with ground-based alternatives?

Researcher: People are concerned not only about energy availability but also whether the massive influx of capital into AI is wise. Our measure of AI performance is the value it brings to knowledge workers. Currently, fully leveraging AI can increase output from one unit of work to 1.5 units. Companies can achieve remarkable business returns by paying only a fraction of employee salaries.

With the advancement of AI, we anticipate that investment in AI software will reach $7 trillion under a baseline scenario, which would be sufficient to support over $1 trillion worth of data center infrastructure construction. While energy constraints are indeed an issue in certain regions (such as central Ohio), many emerging cloud companies are actively addressing this challenge, and we do not consider it to be an absolute global limitation. Unlike the stagnation that followed the extensive laying of fiber optics in the 1990s, today every GPU is being utilized to its full potential or is even in short supply for applications ranging from text language models to multi-omics, autonomous driving, and embodied robotics. Regarding space-based data centers, launching them on existing platforms like Falcon 9 does not currently make economic sense. However, with the introduction of SpaceX's next-generation reusable rocket, Starship, the cost per ton to reach orbit could drop to just a few hundred dollars. Once this threshold is crossed, AI computing based in space will become more cost-competitive than ground-based computing. This not only addresses challenges in constructing data centers due to political resistance or energy grid limitations on Earth but also allows AI computing to scale without local constraints. Elon Musk once said this is merely an engineering problem, and as he demonstrated when he defied skeptics by building cars using mobile phone batteries, when he focuses on solving an engineering problem, he has consistently proven to be correct.

Host: Very insightful. Could you briefly introduce us to the overall perspective on current AI development trends? In terms of revenue generation, in which areas is AI creating genuine net new revenue rather than merely compressing profit margins through efficiency gains? How does ARK differentiate between hype and meaningful signals?

Researcher: We believe AI represents a generational platform shift, similar to the transition from PCs to smartphones. AI is transforming the user interface from keyboards to natural language, enabling an entirely new way of interacting with computers that is both easier to use and more powerful. We will see new product forms equipped with built-in AI assistants, such as Meta Ray-Ban smart glasses. Compared to the internet and smartphones, AI adoption is more than twice as fast, reaching a 20% adoption rate within just three years. Driving this rapid progress is the significant decline in the costs of training and inference for AI models.

In the consumer space, personal AI agents are becoming the primary entry point for accessing internet services and information, with users increasingly trusting ChatGPT or Claude. This creates new monetization opportunities and business models where AI agents can conduct transactions on our behalf, and the shift in attention will attract substantial advertising spend toward these new assistants. For instance, integrating Instacart into ChatGPT allows users to simply take a photo of a recipe, and AI can handle 90% of the grocery ordering process, offering a convenient experience that breaks old habits and generates incremental revenue that did not previously exist.

In enterprise knowledge work, since the end of last year, there has been a fundamental turning point in the long-term reasoning capabilities of models. The average duration for which AI agents can reliably complete tasks has increased from 5 minutes to over 55 minutes without constant human supervision. This greatly enhances enterprises' willingness to pay, as the monthly subscription fee for a basic enterprise chatbot can be recouped by employees saving less than a day’s time. As for distinguishing hype from real signals, we observe accelerating revenue growth among cloud service providers like AWS, Azure, and GCP, with GCP even achieving 48% year-over-year growth, demonstrating that the demand for computing power is generating substantial new revenue.

Not only are technology enablers benefiting, but ultimate beneficiaries are also seeing revenue growth. For example,$Palantir(PLTR.US)$assisting insurers like AIG in leveraging AI agents to evaluate and underwrite hundreds of thousands of contracts that were previously backlogged due to insufficient manual review capacity. Such applications of AI across the economy to fill human resource gaps not only reduce high operational costs but also generate true net new revenue and enable significant market expansion.

Host: As insurers like AIG and other enterprises continue adopting AI, what will be the biggest bottleneck to scaling AI over the next three years? Will it be electricity, computing power, data quality, regulation, or talent?

Researcher: That's an excellent question, and the market has been continuously debating what the current bottlenecks are. I believe the ultimate bottlenecks boil down to electricity and computing power.

If OpenAI wants to release a new product, or if Claude Code is scaling up, or Anthropic seeks to acquire new users, they all need GPUs, data centers to house those GPUs, and the electricity to connect them to the power grid—xAI is even building its own power plant. All these factors must come together, and I think this is the main bottleneck, potentially outweighing issues related to data or talent.

Based on the latest research trends from models and AI labs, models are increasingly generating their own training data. While human thought remains crucial as seed data, it can be infinitely expanded through synthetic data generation. Moreover, models also contribute to discovering new algorithmic breakthroughs to enhance their own performance. For instance, OpenAI's recent programming model is the first new model trained with the assistance of its predecessors. This alleviates, to some extent, the talent bottleneck. However, talent remains critical, which is why there is significant talent mobility among the four core AI labs.

Nevertheless, I would still prioritize computing power, provided you have access to data centers and sufficient electricity to power these chips. Additionally, trade-offs and compromises can be made when encountering bottlenecks. People used to say that data was running out, but the concept of a chain of thought has made us realize that we can generate new data based on existing data by leveraging additional computing power. If you encounter a bottleneck in one area, you can enhance AI capabilities by consuming another resource.

3. AI Empowered Multi-Omics Sequencing

Host: Excellent. We will now move on to the next segment about Multi-Omics. You have made remarkably accurate predictions in this field. As AI accelerates drug discovery and diagnostics, where do you see the greatest value capture within the entire multi-omics technology stack? Is it in data generation, model development, or the commercialization of therapies?

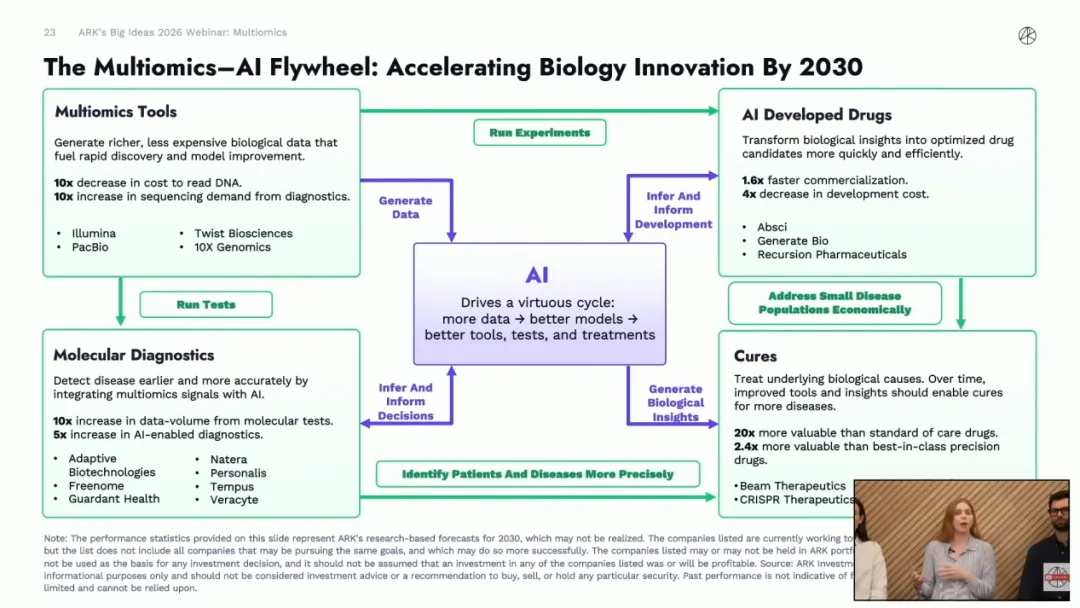

Researcher: That is an excellent question. People may instinctively want to pick one layer of the technology stack, but in reality, these components create compounding effects when layered upon each other. AI serves as the central hub here, driving the flywheel of biological innovation. Better and larger volumes of data translate into better models, and better models in turn enhance molecular diagnostics, therapeutic interventions, and tool development, which then generate richer datasets, forming a virtuous cycle.

We divide this cycle into four key areas: First, multi-omics tools, which enable the acquisition of higher-quality data at lower costs; second, molecular diagnostics, allowing for earlier and more accurate disease detection; third, AI-driven drug discovery, utilizing biological insights to develop superior drug candidates that can reach the market faster and at a lower cost; and finally, cures, representing one-time treatments targeting the root causes of diseases. These components do not operate independently in a vacuum but reinforce each other, creating a flywheel effect.

The primary driver accelerating this flywheel is the dramatic reduction in costs. Decades ago, the completion of the first human genome sequencing under the Human Genome Project took approximately 13 years, costing nearly $3 billion when accounting for infrastructure. Today, whole-genome sequencing can be completed for just $100. Looking ahead to 2030, we foresee this cost dropping another order of magnitude to around $10. This decline in cost curves has shifted the paradigm, including thresholds for testing, frequency of tests, and the resulting volume of data. As costs decrease, the number of tests will increase, and we predict that testing volumes will double by 2030.

Notably, the total number of tokens or data volume generated in the field of biology is already comparable to the token counts used to train cutting-edge large language models. By 2030, we expect this scale to grow tenfold. In summary, biology is becoming one of the largest data-generating engines globally, driving profound transformations across healthcare. As portfolio managers, it is a privilege to learn about these developments. The human body comprises approximately 35 to 40 trillion cells, and with the advent of single-cell sequencing, the scale of this data explosion will make everything we’ve seen in the computing era pale in comparison.

Host: You mentioned earlier that part of the flywheel effect relates to the impact on drug development. Can AI meaningfully reduce the costs, duration, and failure rates of clinical trials? What does this mean for capital efficiency in the biotech sector?

Researcher: That’s precisely the crux of the matter. More abundant data leads to better models, and one of the most evident impacts is on the economic efficiency of drug development. Currently, traditional drug development can take over a decade, cost billions of dollars, and see a failure rate as high as 90% for drug candidates entering clinical development. Clearly, there is an urgent need to improve efficiency in this area.

The dynamic effects brought by AI can accelerate the drug's time to market, thereby generating more revenue under patent protection while reducing costs, which creates a genuine compounding effect. Our model shows that AI has the potential to reduce the time to market for drug products by 40% and cut actual development costs to one-quarter of their original level. Historically, the return on investment (ROI) in pharmaceutical R&D has been in the single digits, but considering faster time to market, lower costs, and higher success rates, AI truly changes this capital efficiency paradigm. If further applied to curative therapies, this transformation becomes even more profound. Traditional early-stage assets hold almost no economic value, whereas therapies driven by AI could be worth over $2 billion per drug. We are building an excellent model with significant implications for Biotech capital efficiency.

Cathie Wood: Let me add another perspective here. The golden age of the healthcare industry was in the 1980s and 1990s when the ROI on R&D spending reached as high as 30%, whereas now it has dropped to the mid-to-low single digits. We believe the ROI will return to those previous highs, ushering in a new golden age for the healthcare sector. Given the current psychological expectations, this would be very surprising.

Host: Since I am highly interested in this topic, I would like to pose an additional question: How should investors view regulatory risks and the future development path of insurance coverage as gene therapy scales up?

Researcher: This is a multi-faceted question, which we can break down step by step. Regarding regulation, particularly over the past year, there have been significant changes. The U.S. FDA recognizes the extreme difficulty in bringing drugs to market and therefore aims to modernize the agency. They actively collaborate with drug developers to streamline the clinical development process.

We have already seen some tangible results, especially with the introduction of new regulatory frameworks targeting rare diseases and root-cause biological therapies. On the other hand, there are reimbursement and insurance barriers. Sometimes exorbitant price tags can be misleading; for instance, seeing a therapy priced at $2 million naturally raises questions about whether insurance will cover it. Take Casgevy, for example, a gene-editing therapy approved for treating sickle cell disease and transfusion-dependent beta-thalassemia, priced slightly above $2 million but where 90% of patients in the U.S. can receive reimbursement. The reason lies in comparing the cost of this drug to the lifelong treatments and frequent hospitalizations endured by chronic disease patients. This long-term immense value to the healthcare system justifies its pricing. It underscores how the economics of curative drugs fundamentally differ from traditional drugs.

Curative therapies require only a one-time treatment, allowing you to capture all the value upfront, pull forward cash flows, generate more patent-protected revenue, and avoid overlapping competition. This means curative therapies are far more valuable than traditional drugs, potentially up to 20 times greater in latent value. To make this more concrete, let’s look at the case of hereditary angioedema (HAE). HAE is a rare disease causing painful and potentially life-threatening swelling episodes. Currently, patients require lifelong management to control episodes, costing between $10 million and $20 million over their lifetime.

Take gene-editing therapy as an example, which has shown encouraging clinical data. We estimate its fair pricing to be around $3 million, while its true value-based pricing could be three to four times that amount, depending on efficacy and durability data. Applying this to the current 7,000 HAE patients in the U.S., it translates into cost savings of $52 billion for the healthcare system. Despite the high upfront price, it delivers better outcomes for patients, eliminates the burden of lifelong symptom management, and generates substantial savings for the healthcare system.

Finally, I’d like to briefly emphasize an important shift regarding market expansion. Gene-editing therapies are beginning to transition to in vivo editing, an approach enabling their expansion from rare diseases to common diseases, including cardiovascular conditions, the leading cause of death globally. For such diseases, value-based pricing may be around $165,000. While this is vastly different from the multimillion-dollar price tags of rare disease therapies, it represents a massive total addressable market (TAM). Taking the highest-risk cardiovascular patients in the U.S. alone, multiplying by this price yields a TAM of $2.8 trillion. By comparison, Lipitor, which once ranked as the best-selling drug in history, generated cumulative sales over 20 years that amounted to only one-twelfth of this figure. Thus, the core takeaway from multi-omics is that the convergence of AI and biology is driving a profound revolution in healthcare.

Cathie Wood: The stock market hasn't fully realized this yet, but it will catch up eventually. What surprises me most is that insurers have raised no objections to the $2 million price tag, and I don’t think the market has even noticed this yet.

4. Autonomous driving disrupts the automotive industry

Host: Thank you for your insightful sharing. Next, let’s move on to the topic of Autonomous Vehicles. Could you tell us about the developments in this field?

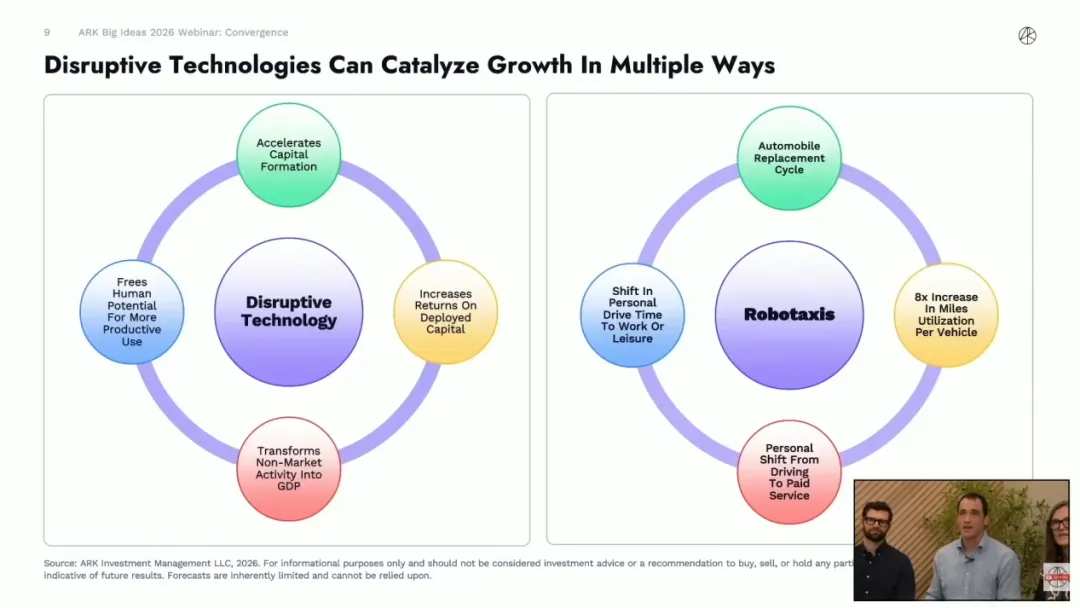

Researcher: Sure. Earlier, we mentioned Embodied AI. We believe that autonomous driving is the first large-scale application of Embodied AI that consumers can see, and it's already happening today. We have already seen vehicles on the road with no one in the driver’s or passenger’s seat, shuttling passengers around fully autonomously.

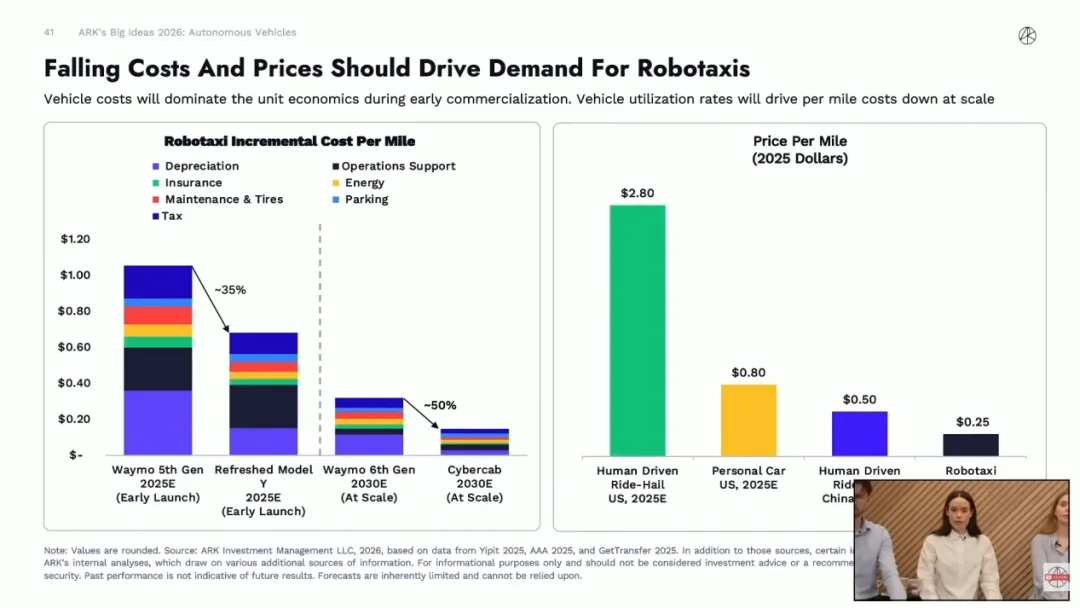

At this early stage of commercialization, one crucial factor is the underlying cost of the vehicle. When you have a small fleet and are trying to scale up or persuade partners, manufacturing costs are important, but what matters more is the operational cost per mile. Reducing the cost per mile will be the key driver in propelling this technology and innovation forward.

If compared$Tesla(TSLA.US)$When comparing Tesla Model Y with the fifth-generation Waymo, we see that the incremental cost per mile of the Tesla Model Y is over 30% lower. With newer models, this advantage will only widen further. For instance, when comparing Tesla’s Cybercab with the sixth-generation Waymo, we estimate a cost advantage of around 50%. This is crucial during the early stages of platform expansion and also relates to how competitive pricing strategies for consumers can be formulated.

Speaking of pricing, we believe that when operating at scale, Robotaxi platforms could potentially charge as little as 25 cents per mile. To put this into perspective, it would cost less than one-tenth of the ride-hailing services driven by humans in Western markets, over half less than the cost of driving your own private car, and nearly half as cheap as ride-hailing services in China. The reduction in cost will greatly expand the current ride-hailing market, enabling low-cost point-to-point mobility, allowing more people to enjoy transportation services, and ultimately making our roads much safer.

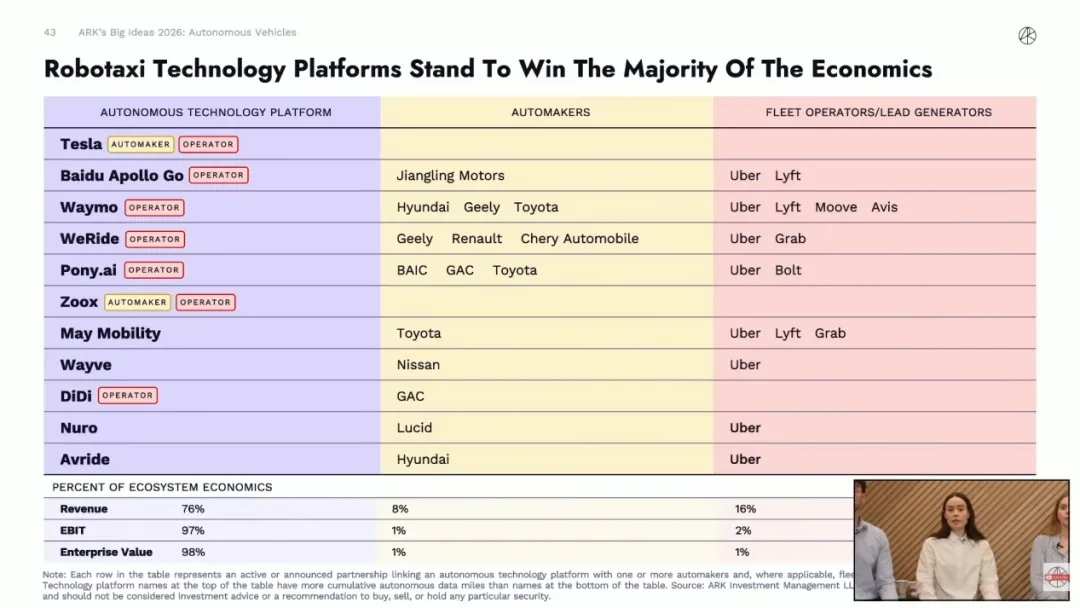

There is enormous market potential here. By the end of this decade, we believe that Robotaxis could create an enterprise value opportunity worth $34 trillion, most of which will accrue to autonomous driving technology providers or platform operators. Companies that independently develop core autonomous driving technologies can achieve a commercial closed-loop through Robotaxi services, representing one of the largest revenue opportunities available. The Total Addressable Market (TAM) for Robotaxis could reach $10 trillion or more, with revenues and profits in this space possibly reaching around $2 trillion by the end of the decade. Platform operators and technology providers capable of achieving extremely low costs per mile will capture the majority of the economic benefits. Meanwhile, we are also seeing traditional automakers partnering with autonomous driving technology providers and ride-hailing giants, with some companies shifting their business models to become maintenance service providers for autonomous driving companies and automakers.

We expect autonomous driving to completely transform the entire automotive industry. Companies currently operating on traditional fuel-based platforms will see significant consolidation. The future of Robotaxis lies in electrification, and electric vehicles will be critical to optimizing the economics of cost per mile and restoring its appeal. In the U.S., we are again observing an ideal price ceiling of approximately $2.80 per mile. In China, where competition in the ride-hailing market is much fiercer, many companies are turning to markets such as the Middle East in search of greater profit margins. Today, Robotaxis are already in actual operation, and the total mileage we have tracked across various platforms is approaching one million miles. The question now is when full-scale deployment will occur and how the rapid increase in fleet size will further reduce the cost per mile.

Cathie Wood: I’ve been to Europe many times, and when I share our team’s in-depth research on Robotaxis with them, they often cannot relate because European regulators have not yet reached that stage. However, we believe Europe will eventually follow suit because the safety statistics for autonomous driving are simply astonishing. In the long term, it would be unwise, and even unethical from a professional standpoint, for regulators to hinder this trend.

Researcher: Returning to the theme of 'The Great Acceleration,' take the U.S. as an example: the annual unpaid labor cost of manual driving exceeds $4 trillion. Relative to the U.S. economy, which stands at $30 trillion, converting this $4 trillion of non-monetized activity into economic activity—where you could pay someone else to drive at a cost lower than your own time—will result in a massive economic transformation and significantly boost GDP growth.

Regarding which regions are most likely to achieve large-scale autonomous driving deployment first and the role of regulatory consistency in commercial success, we believe that the United States and China will be the first markets to achieve scaled implementation. In the U.S., due to regulatory authority being vested at the state level, it has become one of the first markets to allow large-scale testing and the commercialization of Robotaxis. China also places significant emphasis on the opportunities presented by autonomous driving, with local companies demonstrating substantial economies of scale. Additionally, the Middle East is an attractive market, especially for Chinese companies seeking higher profit margins.

In terms of regulation, as Ms. Wood mentioned, autonomous driving platforms have proven to be much safer than human drivers. Years ago, we estimated that Robotaxis could bring about an 80% improvement in safety, and now statistics from platforms like Waymo and Tesla's Full Self-Driving (FSD) have confirmed this. The technology has matured, and while regulation is critical to promoting widespread adoption, driverless vehicles are already on the roads, and we foresee full adoption occurring within the next five to ten years.

Currently, technology is no longer a barrier; the real challenge lies in how to move Robotaxis beyond initial pilot programs in a few cities to achieve genuine fleet-scale expansion. This requires companies like Tesla, which can deploy a large number of vehicles on the road, as well as deep cooperation between Waymo and automakers, along with the hardware-software synergy demonstrated by Chinese companies. Low-cost vehicle platforms will play a crucial role here, as only then can fleet sizes expand and appealing products be offered to consumers. As scale increases, the per-mile cost will continue to remain lower than existing ride-hailing prices, which is the key to expanding market size and represents the top priority for major companies in execution moving forward.

5. The cost of reusable rockets is decreasing significantly.

Host: Next, let’s talk about reusable rockets.

Researcher: The reusability of rockets is indeed ushering in a new era for the space economy. The year 2025 is highly symbolic, with annual orbital payload mass reaching its highest level in history, largely thanks to SpaceX. Currently, SpaceX operates over 9,000 active Starlink satellites in orbit, accounting for more than two-thirds of all satellites currently in space. Their dominance stems from a decade-long head start in the industry. In 2015, SpaceX successfully recovered its first orbital-class booster, executing partial reuse nearly flawlessly, while its strongest competitor only achieved its first successful recovery late last year. While other companies are still striving to master partial reuse, SpaceX is pushing ahead with full reuse, directly translating into a dramatic reduction in launch costs.

Our research centers on Wright's Law, which, in the context of launch costs, states that every doubling of cumulative payload mass sent to orbit results in a 17% reduction in launch costs. SpaceX’s Falcon 9 rocket has already demonstrated this. By our estimates, since 2008, they have reduced launch costs by approximately 95%. This has unlocked vast new opportunities in the space age, including orbital data centers and medical microgravity testing that greatly advances multi-omics in the context of technological convergence. Currently, launch prices have dropped to around $1,000 per kilogram. When SpaceX successfully deploys its fully reusable Starship rocket at full capacity, we expect costs to fall below $100 per kilogram. This is why orbital data centers are becoming highly attractive. Once this scale threshold is reached, orbital data centers may become 25% cheaper than ground-based computing.

The reduction in costs from approximately $700 per Falcon 9 launch to about $100 for Starship will directly catalyze an explosion in vehicle-based AI and space-based computing. The demand for satellites in space-based computing will be at least ten times greater than current levels, far surpassing the scale of Starlink and existing communication constellations. This alone could expand the market by an order of magnitude. If we establish a lunar base in the future, the cost of satellite constellations could drop to around $10 per kilogram, but this would require extensive infrastructure development on the Moon beforehand. In summary, the reduction in launch costs is absolutely the core driver behind all orbital infrastructure development.

Ms. Wood: Many people are extremely concerned that AI and automation will destroy existing jobs. But I want to say that we are now witnessing the dawn of a new world. Space exploration is one aspect, and another is the online world built on blockchain technology and immutable digital property rights. I believe these fields will experience explosive growth. Therefore, we are very excited about the AI era, and we firmly believe it will ultimately lead to a net increase in employment opportunities.

Researcher: Regarding net job creation and long-term trends, short-term cash flow generation opportunities within the reusable rocket ecosystem are primarily concentrated in the satellite connectivity sector. For example, the well-known Starlink recently surpassed 10 million active subscribers.

This explosive growth also validates Wright's Law. We believe that every time the cumulative orbital gigabits per second transmission rate doubles, satellite costs will decrease by approximately 44%. This steep cost reduction curve has triggered an explosive growth in the industry. Once scaled, this could represent an annual revenue opportunity of up to $160 billion, which is why many aerospace companies are rushing to enter the public markets to seize a share of the pie.

6. Technology Development Trends for the Next Five Years

Host: So from 2026 to 2030, how will the development arguments around the convergence technology stack in AI, robotics, energy systems, and public blockchain evolve? What are the most critical bottlenecks?

Researcher: From the perspective of diversified investment, extensive exposure to various cutting-edge technologies is crucial. You can fully invest in AI enterprise software, as short-term setbacks in this field will not affect the successful development and pricing of new therapies in the multi-omics market. Although AI serves as the underlying accelerator for all these technologies, each sub-sector faces vastly different commercialization resistance and market opportunities. We need to build momentum across all technological fields, anticipate, and capture the kinetic energy that converts into cash flow for reinvestment.

Regarding bottlenecks, we believe there is indeed a global need for more computing power. Whether it’s the orthogonal expansion of computing power through space-based data centers or the continuous expansion of chip wafer fabs in the United States, both contribute to enhancing computational infrastructure. For instance, Boom, a supersonic civilian aircraft company, has carved out an enormous new business focused on providing electricity for computing power due to its engine technology perfectly aligning with the immense power demands of AI data centers. Currently, capital markets are flocking to provide resources for these infrastructure opportunities, which is the most significant industry catalyst at present.

Cathie Wood: As mentioned multiple times, unit growth is crucial, which is at the core of Wright's Law. If one must point out what might impede development, extreme disasters such as global wars would certainly pose major obstacles. However, interestingly, even during the toughest times, businesses and consumers remain willing to change their ways of doing things to seek better, cheaper, more efficient, more streamlined, and more creative solutions. The COVID pandemic serves as an excellent example. At that time, global supply chains were once paralyzed, and work was severely disrupted, but this instead accelerated the deployment of technology. Now, not only have we overcome these challenges, but we are moving forward at an even faster pace.

Researcher: The biggest competitor to disruptive technologies is actually inertia and the status quo. The collective concern about AI in today’s society is driving people to take more proactive actions to understand and embrace this technology. This is why companies are confident they need to invest hundreds of billions more to expand computing capacity because existing computing power cannot meet the demand for AI-integrated applications.

Regarding the future of enterprise software and SaaS in the Agentic AI era, we believe that AI's transformation of software does not necessarily mean a complete destruction of the current landscape. AI is making software development easier than ever before. Some companies may choose to develop or enhance internal software capabilities independently, but it is more likely that we will see a group of emerging competitors with stronger AI-native attributes, greater agility, and tailored solutions for specific industries emerge. Rather than having every company build its own CRM system, opting for these highly efficient next-generation tools would make more sense. This paradigm shift undermines expectations regarding the revenue growth and pricing power of traditional software giants, leading to their continued sell-off in the capital markets.

Currently, many outstanding AI-native companies are still incubating in private markets. Examples include Sierra for customer service, Harvey for legal affairs, and Cursor for software development assistance. Taking Cursor as an example, within just three years of its establishment, its revenue run rate surpassed $2 billion. In the traditional cloud computing era, reaching a $100 million run rate was considered a significant milestone, like$Twilio(TWLO.US)$Such leading companies spent six years and employed 500 people to achieve this. However, Cursor accomplished the same feat in half the time and with half the workforce, generating 20 times the revenue of a traditional SaaS giant. This vividly demonstrates the tremendous leap in productivity brought by Agentic AI. In the future, these next-generation software enterprises will exhibit astonishing commercial explosiveness.

Cathie Wood: I believe it is crucial to emphasize that, precisely because AI has significantly lowered the technological barrier, we are confident that an unprecedented wave of entrepreneurship is on the horizon. Now, all of us can program directly using natural language. So, go ahead and start your ventures!

Host: On the exciting topic of the entrepreneurial boom, our meeting today concludes here. Thank you very much for your participation, and we hope you enjoyed the in-depth discussion on Big Ideas 2026. If you have not yet downloaded the relevant report, please be sure to read and review it. After the meeting, you can contact us via our website or social media platforms. Wishing you all the best, and let us work together to advance innovation.

Futubull【机会页】Celebrity portfolio tracking opportunities have been launched! Multiple celebrity portfolios are available for selection, allowing you to follow the strategies of major players with one click, accurately locking in high-quality investment targets, and investing with greater confidence!

Futubull【机会页】Celebrity portfolio tracking opportunities have been launched! Multiple celebrity portfolios are available for selection, allowing you to follow the strategies of major players with one click, accurately locking in high-quality investment targets, and investing with greater confidence!

Editor/Rice