Source: Barron's Chinese

Author: J. Dennis Jean-Jacques

Investing is by no means an easy task. Even when you believe that the market price of a company has long been undervalued, it may continue to fall to a point that makes you question your judgment. In such moments, rational judgment and meticulous calculations may no longer be sufficient to support your trading decisions; only conviction can help you navigate through the troughs.

J. Dennis Jean-Jacques, who once worked alongside legendary investors such as Peter Lynch and Michael Price, summarized seven tenets of value investing in his book 'The Five Key Principles of Value Investing.' During times of extreme market downturns, you may wish to revisit these beliefs. This article is excerpted from the first chapter, 'The Philosophy of Value Investors.'

Tenet One: No matter how the market changes, the world will not come to an end because of it.

Tenet One: No matter how the market changes, the world will not come to an end because of it.

From the short to medium term, investor sentiment has a far more significant impact on stock prices than fundamentals. However, in the long term, fundamentals are the key factor. Throughout the history of American capitalism, capital markets have always survived repeated economic crises and continued to thrive. Since World War II, the U.S. economy has experienced several recessions and setbacks, yet the market has always managed to recover promptly from these crises. History shows that the vast majority of economic recessions are, in essence, normal, and as long as the government responds appropriately, these downturns will be short-lived.

On October 1, 2001, following the '9/11' incident, capital markets were plunged into a state of heightened uncertainty. Peter Lynch made the following comments regarding the market turmoil at the time: 'Despite having worked in this industry for over 30 years and having witnessed numerous challenging periods, including the 1987 stock market crash (when the Dow Jones Industrial Average plummeted by 23% in a single day) and five other major recessions, I still cannot answer this question, and perhaps never will. No one can make definitive predictions about where the next 1,000 points will go. Market volatility is the norm, and it is certainly no place for comfort.'

What is important for us is that we must not lose focus on the market under any circumstances, as that is the key to succeeding in the stock market.' Peter Lynch went on to say that this series of events would hurt the market in the short term, affecting corporate earnings and the broader economic environment. 'But in the long run, I believe that corporate returns ten years from now will be higher than they are today, and those 20 years from now will be significantly higher, with the market following this upward trend.'

As we can see from the data in Figure 1, in 15 out of 18 financial collapses, the stock market recovered its losses within just three months, with growth exceeding the event-driven declines.

Note: 1. The periods of 22 days, 63 days, and 126 days are calculated starting from the last day listed in the 'Event Occurrence' column. 2. The start date in the 'Event Occurrence' column refers to the time when the market began reacting to the event or the nearest trading day after the event occurred.

3. Between 1914 and 1916, the Dow Jones Index incorporated a new set of 20 stocks for calculation purposes and used them to compute the value upon reopening on December 12, 1914. The NDR analysts conducting this study adjusted the Dow Jones Index data for December 12, 1914, to ensure continuity. This data is sourced from the Dow Jones Industrial Average compiled by Phyllis S. Pierce for the period 1885–1990. 4. 'Days' refer to market trading days.

Tenet Two: Investors are always driven by fear and greed, causing fluctuations in the overall market and stock prices.

Volatility is simply a necessary cost of engaging in stock investment. As previously mentioned in this chapter, the two most common emotional responses in the stock market are fear and greed. Fear drives stock prices far below intrinsic value, while greed pushes them far above intrinsic value. Investors, fearing that company stock prices will become worthless, frantically sell off their stocks and mutual funds on the market. This leads to high redemption rates for these funds, forcing professional investors, especially value investors, to sell stocks against their will at prices far below the company's true value. This fuels the spread of fear, ultimately creating a vicious cycle. Normal economic cycles or sudden stock market crashes are often caused by these vicious cycles.

Greed, on the other hand, has the opposite effect. Investors inflate stock prices, refuse to sell overvalued securities, and hope to extract as much potential profit as possible. Excessive optimism and fear are the enemies of rational investors. Therefore, value investors feel fear when the market is filled with greed, and the framework of value investing seeks to prevent one from falling into excessive fear or greed.

Tenet Three: Inflation is the only true enemy, and any attempt to predict economic changes or trends in the market or economy is futile.

Focus on companies and their value, then keep Tenet One in mind. Inflation refers to the general increase in the prices of consumer goods and services. The federal government compares the current prices of a basket of consumer goods with historical prices to measure the inflation rate. If current prices rise, investors will demand higher returns on the stocks of the companies they have invested in to offset the decline in the purchasing power of their investment capital. The Federal Reserve typically intervenes to control inflation.

During periods of inflation, the Federal Reserve raises the discount rate, leading to an increase in interest rates. As interest rates rise, the cost of borrowing money increases, reducing the demand for money. The prices of goods and services purchased with money also decrease, eventually leading to downward pressure on product prices. For companies, inflation means an increase in the cost of borrowing funds, and economic indicators such as interest rates and unemployment rates are influenced by inflation expectations.

Inflation can have catastrophic impacts on investors, leaving them with very limited options to mitigate its effects. Buffett once said, "The math makes it all clear: inflation is a heavy tax, far heavier than any tax currently stipulated by law. The inflation tax has the magical power to erode capital." Buffett warned, "If you think you can skillfully outmaneuver inflation in the securities market, I would be happy to be your broker, but not your partner."

Do not waste time; while accurately predicting economic changes such as interest rates or stock market trends might be highly profitable for investors, it is not feasible and likely never will be. Thus, value investors do not burden themselves with anxiety chasing these illusory mirages; instead, they focus on more substantive issues.

Tenet Four: Good ideas are hard to come by, but even in bear markets, there are always good ideas to be found in the market.

The term 'stock market' is actually inaccurate; a more appropriate description would be a market with numerous stocks, where individual investors can perform well regardless of overall market trends. Disciplined value investors can identify top-tier companies and purchase their shares at the most reasonable prices.

In fact, many value investors firmly believe that the best investment ideas often stem from bear markets, as companies that perform exceptionally well during bear markets tend to have attractive valuations. Since the market is always forward-looking, it often discounts the current economic environment. Prudent investors understand that a bear market is merely a natural phase in the economic and market cycle, and ample evidence shows that every bear market will eventually come to an end after a period of time.

Therefore, we should acknowledge that a bear market is only a temporary phenomenon, and stock prices become more appealing during such periods. It must be recognized that even if one cannot find a once-in-a-lifetime deal during a bear market, there will always be investment opportunities available. In summary, the best time to buy high-quality companies from a long-term perspective is often during a bear market.

Tenet Five: The primary purpose of a publicly listed company is to convert its existing resources into shareholder value.

As a shareholder, your role is to ensure this transformation takes place. A company's purpose is not merely to achieve 'sustained operation'; they are organizations that transform resources and have a responsibility to convert their existing resources into shareholder value. If public companies fail to achieve this goal, they might as well shut down or delist to go private. For a company to truly convert resources into wealth, it usually requires the impetus of one or a series of specific events. These events are called catalysts, which could range from the launch of new products to corporate spin-offs.

The management teams of the best companies are the most efficient at converting resources into shareholder wealth. Corporate resources include personnel, capital, brands, property, plants, and equipment. By transforming these resources into shareholder value, shareholder wealth can be expanded. Any increase in real earnings will be added to shareholders' equity. If management cannot effectively convert free cash flow into shareholder wealth, it should reinvest the free cash flow or distribute dividends to shareholders. In short, management holds the key to success.

Tenet Six: 90% of successful investing comes from buying the right stocks.

On the other hand, selling stocks at the optimal price is not as easy, so value investors tend to buy early and sell early. Given the market’s continuity, value investors can purchase stocks at lower prices, expecting to achieve their desired value without taking excessive risks. To buy stocks correctly, investors need a framework to determine the timing of purchases and sales.

As some professionals have noted: 'There are always fools appearing who buy stocks at higher prices than you initially paid, and as long as someone is willing to pay more, prices can continue to rise. Undoubtedly, this is merely the effect of mass psychology. All astute investors will take preemptive action at the beginning.'

If you plan to buy stocks, you should do so as early as possible. Buying early allows you to make full use of dollar-cost averaging. According to this method, you can purchase more shares of a specific company when the stock price is low. Assuming the fundamental factors that initially led you to buy the stock remain unchanged, dollar-cost averaging can become a powerful tool. For knowledgeable value investors, this method reduces the average cost per share, thereby enhancing returns. It enables investors to acquire shares at more favorable prices.

Tenet Seven: Market volatility is not risk; it represents opportunity. The real risk lies in the reversal and permanent change of a company’s intrinsic value.

The volatility of stock prices is not directly related to risk. Value investors are indifferent to the daily fluctuations of the general market, as a company's fair value and intrinsic value do not frequently fluctuate with stock prices. Benjamin Graham pointed out that the market serves investors rather than guiding their decision-making. Therefore, market fluctuations only provide value investors with opportunities to buy or sell at specific price levels.

Stock prices always fluctuate around a company’s intrinsic value. Value investors should consistently focus on the direction of change in a company’s intrinsic value. The true risks lie in cash flow risks and the economic environment in which the target enterprise operates. The actual level of risk also depends on the purchase price of the stock, specifically the difference between the purchase price and the company’s intrinsic value.

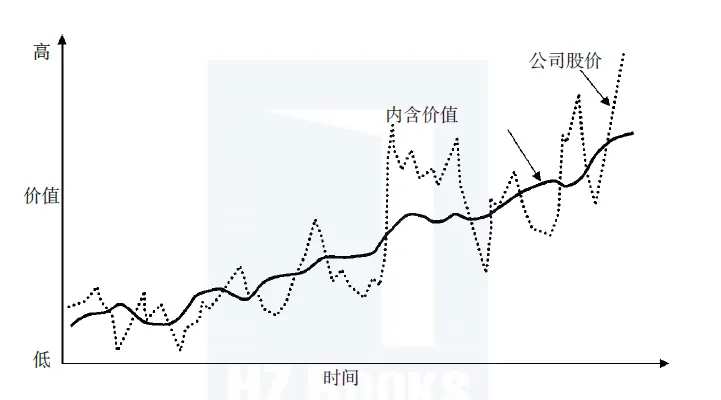

Figure 2 illustrates the relationship between the stock price and intrinsic value of a well-managed, high-quality company. The solid line in the figure represents the company’s intrinsic value, while the dashed line represents the fluctuations in the company’s stock price.

From Figure 2, we need to understand three key points: First, stock prices oscillate up and down around the company’s intrinsic value. Due to market participants attempting to predict market trends, stock price behavior becomes highly variable. These variables stem from financial news, industry data, market movements, portfolio allocations by mutual fund managers, and the actions of major shareholders that must also be considered. These factors cause stock price volatility, but the company’s intrinsic value does not fluctuate as a result.

Second, the focus. Knowledgeable investors wish this kind of stock price volatility would occur across all securities. Value investors need to concentrate on the company’s intrinsic value, asking themselves questions like, “Have the company’s fundamentals changed?” By thoroughly analyzing the solid line in the graph, investors can take full advantage of stock price fluctuations to identify when the market is overly speculative or excessively pessimistic about the target company.

Third, Figure 2 also highlights the issue of timing. Each company and industry exhibits different levels of volatility. For instance, technology companies experience far greater volatility than most manufacturing firms. Therefore, investors who purchase technology-backed companies below their intrinsic value lines may choose to exit their positions earlier due to the higher volatility of these companies’ stock prices. The key question is how to buy stocks below the company’s intrinsic value, which is often the most challenging aspect for tech company investors—a topic we will explore further later in this book.

In summary, value investors tend to avoid high-tech companies. Warren Buffett never touches tech stocks. Similarly, Michael Price, though more speculative than Buffett, admitted, “I am not a tech stock investor unless they plummet... with stock prices below net cash flow per share.” These masters emphasize buying the right stock at the right time. The key point is that the market often signals individual investors when to buy or sell.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Rice