Morgan Stanley stated that Tesla is building a 'flywheel effect' through Robotaxi and Optimus, accelerating its transformation into physical AI. As a key catalyst in the near term, Robotaxi leverages structural cost advantages and unsupervised testing in Austin, with mass production expected to commence in 2026; Optimus represents long-term growth potential.

Despite holding $44 billion in cash, Tesla may face a cash flow gap in 2026 due to over $200 billion in capital expenditures. The profitability of its core business will be the cornerstone of its transformation.

$Tesla (TSLA.US)$Tesla is constructing a mutually reinforcing growth logic around Robotaxi and Optimus—Robotaxi commercialization is the most important near-term catalyst for this year’s stock price, while Optimus represents the company's long-term bet on transitioning to physical AI. These two main lines together form what Morgan Stanley calls Tesla's 'flywheel.'

According to TradingView, after attending the TMT conference in San Francisco and visiting the Texas Gigafactory, Morgan Stanley analyst Andrew S Percoco expressed a "marginally more optimistic" outlook on the commercialization prospects of Robotaxi, particularly praising the progress made by the company in addressing edge cases such as passenger pick-up and drop-off. The report maintained an Equal-weight rating for Tesla with a target price of $415, while reaffirming the timeline for Cybercab mass production to commence in April 2026.

According to TradingView, after attending the TMT conference in San Francisco and visiting the Texas Gigafactory, Morgan Stanley analyst Andrew S Percoco expressed a "marginally more optimistic" outlook on the commercialization prospects of Robotaxi, particularly praising the progress made by the company in addressing edge cases such as passenger pick-up and drop-off. The report maintained an Equal-weight rating for Tesla with a target price of $415, while reaffirming the timeline for Cybercab mass production to commence in April 2026.

Ask Futubull AI: How does Tesla look recently? What key business developments should be closely watched??

Ask Futubull AI: How does Tesla look recently? What key business developments should be closely watched??

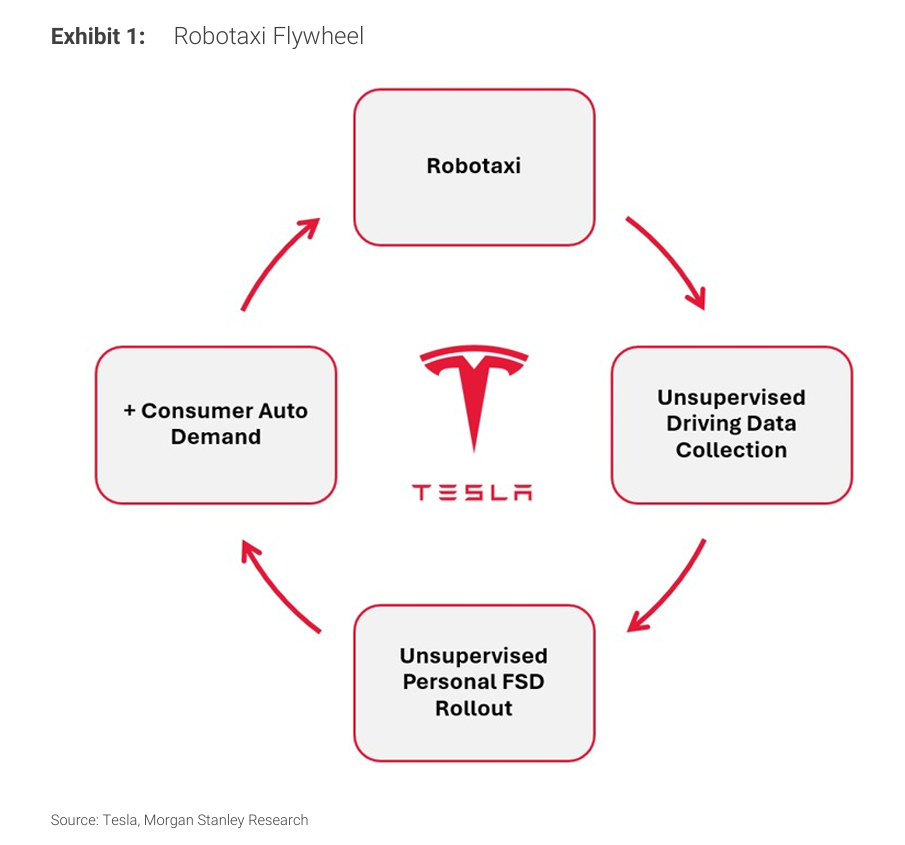

The "Robotaxi flywheel" logic proposed by Morgan Stanley suggests that every mile driven by unsupervised Robotaxis will continuously optimize the underlying autonomous driving model, thereby accelerating the unsupervised adoption of personal FSD (Full Self-Driving), boosting FSD adoption rates, improving automobile demand, and enhancing free cash flow growth. This implies that the success of Robotaxi commercialization will not only serve as a source of mobility service revenue but also act as a significant lever to boost Tesla’s core automotive business.

However, this strategic layout comes with significant short-term financial pressures. Morgan Stanley estimates that Tesla’s capital expenditure in 2026 will exceed $20 billion, more than double year-on-year, with a free cash flow deficit of approximately $8 billion for that year. Tesla’s cash reserves of around $44 billion provide some buffer in the near term; however, if the recovery of its automotive business falls short of expectations, Morgan Stanley does not rule out the possibility of the company seeking opportunistic financing in 2027.

Robotaxi: Austin is the true testing ground for unsupervised deployment.

At$Tesla (TSLA.US)$In the current Robotaxi deployment, hundreds of vehicles have been deployed in the San Francisco Bay Area. However, California regulations still require safety monitors in the driver's seat, making Austin the primary test site for unsupervised real-world deployment. Morgan Stanley expects Tesla’s Robotaxi fleet to reach approximately 1,500 vehicles by the end of 2026.

Tesla has deliberately slowed down its rollout pace in Austin to refine operational strategies, planning to expand Robotaxi services to seven additional cities in the first half of 2026. The company stated that transitioning from supervised to unsupervised operations in new cities is expected to take less time than the approximately six months experienced in Austin. In the short term, fluctuations in NHTSA accident data are considered normal model stress tests, with issues primarily concentrated on edge cases unique to ride-hailing scenarios, such as passenger pick-up and drop-off processes—scenarios where Tesla’s existing FSD mileage data struggles to provide sufficient coverage.

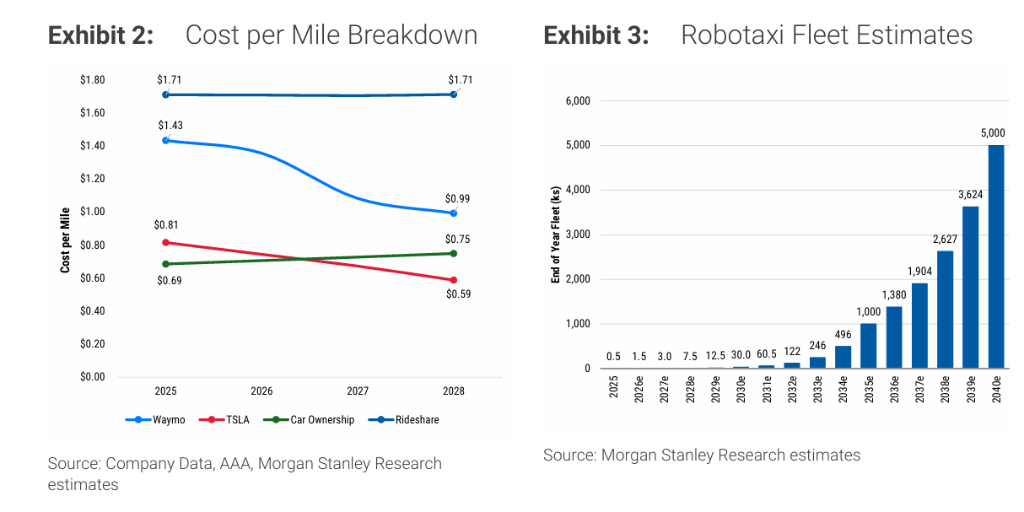

In terms of cost structure, Morgan Stanley believes Tesla holds a significant structural advantage. Based on Model Y estimates, Tesla’s all-in cost is approximately $0.81 per mile, lower than Waymo’s $1.43 and traditional ride-hailing services’ $1.71. With the ramp-up of Cybercab production, Morgan Stanley projects costs could further decrease to $0.37 per mile by 2035, approaching management’s long-term target of around $0.30 per mile for Cybercab.

Cybercab: Disruptive manufacturing processes underpin cost competitiveness.

The cost advantage of Cybercab partly stems from its innovative manufacturing process.$Tesla (TSLA.US)$At the Austin Gigafactory, a modular 'unboxed' architecture replaces the traditional white body, painting, and sequential assembly processes. The vehicle consists of five major components: the front module, the central battery module, the rear cargo module, and two side modules. These parts are produced in parallel and then assembled. The exterior panels are made entirely of plastic material using reaction injection molding, with color directly injected into the plastic. This process eliminates the need for a traditional paint shop, significantly reducing factory footprint.

Morgan Stanley believes that whether Cybercab can start mass production as planned in April 2026 is a critical milestone for verifying the achievement of the aforementioned cost targets and will also directly impact the scaling process of Robotaxi.

Optimus: A long-term narrative with implementation still requiring time

Compared to the relatively clear progress of Robotaxi, Optimus remains in an earlier stage. Morgan Stanley expects the release of Optimus Gen 3 to be postponed until the second quarter of 2026, but considers the more critical milestone to be the start of mass production (SOP) in the second half of 2026.

Humanoid robots rolling off the production line in 2026 are expected to have relatively limited functionality. Tesla has even proposed establishing an 'Optimus Academy,' dedicated to data collection, model optimization, and robot training. Additionally, the majority of new computing power from the Cortex 2 supercomputing center will be allocated to Optimus training. Elon Musk disclosed on the X platform that Tesla is developing 'Digital Optimus' — a task orchestration tool aimed at Optimus and potentially Cybercab.

Among the five components contributing to Morgan Stanley's $415 target price, Optimus (humanoid robot) contributes $60 per share, albeit discounted by 50% to reflect market pricing of high uncertainty regarding its commercial implementation. By contrast, network services (including FSD subscriptions) contribute $145 per share, and Tesla's mobility business contributes $125 per share, forming the two core pillars of the target price.

Energy Business: Growth logic remains solid, but near-term margin pressures persist

$Tesla (TSLA.US)$The energy business remains an important growth driver, with strong demand on both the front-end grid side and the back-end user side. The company is adding 50 GWh of Megapack capacity in Houston while advancing a 7 GWh domestic lithium iron phosphate battery production line.

However, Morgan Stanley cautions that attention should be paid to gross margin pressures in the energy business in the near term — intensified pricing competition coupled with lagging tariff impacts are expected to compress this year’s energy business gross margin to the mid-20% range. Regarding Tesla’s core automotive operations, although production of the Model S/X has been halted, the possibility of introducing new models has not been ruled out, including derivatives based on the Cybertruck platform, launching the Model YL in new regions, and the Roadster.

Morgan Stanley points out that during Tesla’s transformation into physical AI and robotics, maintaining profitability in its core automotive (including FSD) and energy businesses is a fundamental prerequisite for supporting its current valuation (corresponding to approximately 40 times EBITDA by 2030).

Peak capital expenditure phase: Ample cash reserves, but financing risks cannot be overlooked

Morgan Stanley forecasts that$Tesla (TSLA.US)$Capital expenditure in 2026 (excluding the Terafab project) will exceed $200 billion, doubling from the previous year, resulting in a free cash flow deficit of approximately $8 billion for that year. Capital expenditure in 2027 is expected to slightly decrease to about $16 billion. With anticipated recovery in EV demand and improved profit margins, the company’s free cash flow is expected to gradually approach breakeven.

Key variables influencing the direction of capital expenditure include: the scale of Optimus robot procurement for internal training at Tesla (cost per unit exceeding USD 250,000); the pace of expansion of the Robotaxi fleet (Morgan Stanley estimates that by 2027 Tesla will deploy approximately 3,000 vehicles through its own assets); incremental computing power investments required for FSD and Optimus training; and the scale of construction of Tesla's self-developed chip manufacturing plant—Morgan Stanley estimates the total investment for this project could reach USD 35 billion to USD 45 billion.

Tesla's cash reserves of approximately USD 44 billion provide near-term support for the above extensive capital plan. However, Morgan Stanley explicitly stated that if high capital expenditure persists and improvements in the automotive business fall short of expectations, the possibility of the company pursuing opportunistic financing by 2027 cannot be ruled out.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Melody