UBS Group has warned that the current oil price shock is far more disruptive than the period between 2011 and 2014. Shale oil, once regarded as a 'shock absorber,' has largely lost its effectiveness—investment elasticity has significantly diminished, and supply-side expansion is no longer replicable. More troubling is the fact that year-over-year oil price increases are approaching 100%, compounded by a weak labor market, tightening household liquidity, and elevated inflationary pressures. These multiple headwinds leave the U.S. economy with almost no buffer, and the net impact may be severely underestimated.

The fundamental difference between the current oil price shock and the high oil price cycle from 2011 to 2014 is that the shale oil industry's responsiveness to price signals has significantly weakened, and what was once the most important supply-side buffer mechanism for the U.S. economy has essentially disappeared.

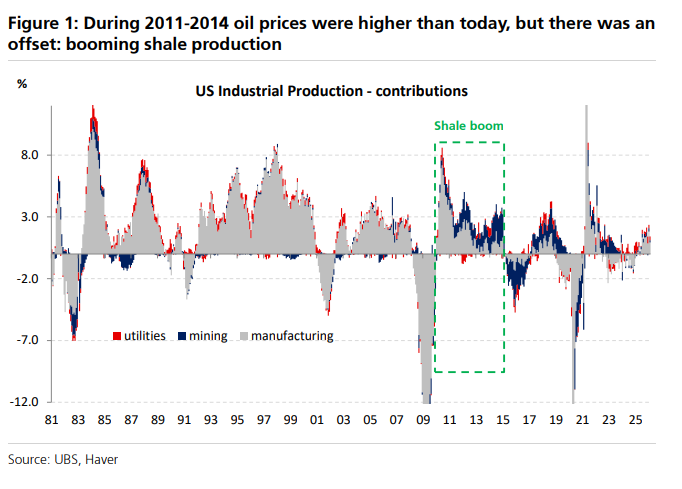

According to Zhui Feng Trading Platform, UBS Group economist Arend Kapteyn noted in a report on March 19 that although the average Brent crude oil price from 2011 to 2014 was approximately $110 per barrel (equivalent to about $145 in today’s terms, roughly 23% higher than the current spot price), U.S. GDP growth at the time remained above 2%. The key reason was that the booming shale oil industry provided strong hedging. This buffer has now largely disappeared, making the net impact of the current rise in oil prices on the U.S. economy harder to offset.

The report emphasized that the destructive nature of the current oil price shock also lies in the speed of the price increase—should the current oil price level persist, year-on-year growth will approach 100%, far exceeding the peak annual increase of no more than 55% during 2011 to 2014. At the same time, the U.S. labor market is weaker, household liquidity is tighter, and inflationary pressures are sharper. These compounding adverse factors make it even harder to offset the erosion effect on consumer income.

The report emphasized that the destructive nature of the current oil price shock also lies in the speed of the price increase—should the current oil price level persist, year-on-year growth will approach 100%, far exceeding the peak annual increase of no more than 55% during 2011 to 2014. At the same time, the U.S. labor market is weaker, household liquidity is tighter, and inflationary pressures are sharper. These compounding adverse factors make it even harder to offset the erosion effect on consumer income.

Shale oil was once the 'shock absorber' of the U.S. economy.

At the beginning of the 2010s, the U.S. shale oil revolution was in full swing, and its supportive role for the economy was undeniable. According to the UBS Group report, in early 2010, the U.S. mining sector (primarily the oil and gas industry) accounted for about 14% of industrial production value. By 2012 to 2013, this sector contributed more than half of the total growth in U.S. industrial production, and during certain periods, it almost accounted for all increments in industrial output.

It was this robust expansion on the supply side that provided strong support to the U.S. economy despite high oil prices—the loss of consumer purchasing power caused by high oil prices was, to some extent, offset by employment, capital expenditure, and industrial output growth driven by the shale oil investment boom.

The elasticity of shale oil investment has significantly declined.

Following the collapse in oil prices from 2015 to 2016, although U.S. mining output rebounded from a low base, the investment intensity and drilling density of the shale oil industry have never returned to pre-2014 levels. The UBS Group report pointed out that oil production still marginally responds to price changes through increased well completions, improved capacity utilization, and enhanced production efficiency—but overall investment elasticity has notably decreased.

In other words, if the market views the current oil price as a temporary phenomenon, the U.S. will struggle to see any supply-side expansion response akin to that driven by shale oil from 2011 to 2014, leaving no way to offset the erosion of real consumer income caused by rising oil prices.

With multiple headwinds compounded, the current shock is harder to absorb.

The UBS Group report outlined several key differences between the current macro environment and the previous high oil price cycle. First, the current U.S. labor market is weaker compared to the period from 2011 to 2014; second, household sector liquidity is tighter, leaving limited buffer space to withstand external shocks; third, the inflation shock has been more severe, with a stronger transmission effect of rapidly rising oil prices on overall prices.

These factors collectively imply that, in the absence of a counterbalancing expansion in shale oil supply, the net drag effect of this round of oil price increases on U.S. economic growth could far exceed the judgment derived from the market's simplistic analogy with historical experience from 2011 to 2014.

Editor/Lee