Source: Barron's Chinese

Author: Barton Biggs

The stock market possesses astute insight into turning points in wars, even more acute than frontline commanders.

Can we gain insights into history by observing stock market trends? Even at pivotal turning points during World War II, such as the Battle of Midway and the Dunkirk evacuation, frontline commanders often struggled to fully grasp their significance due to restricted information and the use of propaganda by both sides. However, stock market investors astutely identified these turning points. The British stock market began a slow recovery before the London Blitz, while the U.S. market bottomed out during the Battle of Midway. This excerpt is from Barton Biggs' book, 'Wealth, War & Wisdom: A Chronicle of the Role of Stock Markets in World War II.'

World War II was not only about freedom and democracy but also about the survival of capitalism and, to some extent, the future of stock markets. As suppliers of capital, stock markets autonomously determined prices. Despite occasional missteps, global stock markets in the early 1940s largely understood the ebbs and flows of the war. This must be attributed to the inherent wisdom of market participants, as all sides controlled war news and used propaganda as a weapon.

World War II was not only about freedom and democracy but also about the survival of capitalism and, to some extent, the future of stock markets. As suppliers of capital, stock markets autonomously determined prices. Despite occasional missteps, global stock markets in the early 1940s largely understood the ebbs and flows of the war. This must be attributed to the inherent wisdom of market participants, as all sides controlled war news and used propaganda as a weapon.

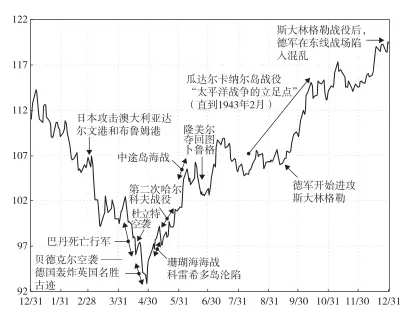

Stock markets demonstrated a strong ability to identify turning points in the war. The only major failure occurred in May and June 1942 when the Tokyo market failed to recognize the significance of two Pacific naval battles. As discussed in Chapter Seven, Japanese official battle reports and media portrayed the Battle of the Coral Sea as a great victory, and the Battle of Midway as a success rather than a defeat, despite admitting losses of aircraft and ships.

Casualties inevitably drew attention and mourning, but Japanese society at the time fully supported the war effort and blindly believed in the invincibility of the Japanese military, making it nearly impossible to imagine campaign failures or economic collapse. Selling stocks based on unconfirmed rumors of naval defeats would have been considered unpatriotic.

By mid-1942, Japan had effectively adopted a planned economy, with the government controlling labor, prices, wages, and industrial decisions. Prime Minister Hideki Tojo placed the Ministry of Munitions, led by Deputy Prime Minister Nobusuke Kishi, in charge of overall economic policy. While this simplified organizational structures and seemed theoretically effective, Japan's reliance on imported raw materials rendered U.S. naval blockades increasingly effective, preventing any rise in production. From autumn 1942 until Japan’s surrender in August 1945, industrial output steadily declined. Between 1940 and 1944, the U.S. economy grew by approximately two-thirds, whereas Japan’s economy expanded by only 25%.

However, not all Japanese investors misunderstood the significance of the Battles of the Coral Sea and Midway. Amid domestic food shortages and the dismantling of park fences around the Imperial Palace for scrap metal, the Nomura family and Nomura Securities began to suspect that Japan would ultimately lose the war by mid-1942. Despite newspapers and radio broadcasting only favorable war news, the Nomura family apparently gained information through social circles frequented by elite members of high society. Many naval officers and pilots who participated in the Battles of Midway and the Coral Sea had relationships with geishas, and when they failed to return, rumors spread. Sensing trouble, the Nomura family began gradually selling off their stock holdings, even short-selling. Later, they may have deduced that land and real estate would be the best assets to preserve value after the war, leading them to invest in property. These assets provided funding for Nomura Securities’ rapid post-war expansion, eventually establishing it as Japan’s leading securities firm.

1. The Insight of the U.S. and London Stock Markets

In contrast, the New York stock market almost immediately recognized the importance of the Battles of the Coral Sea and Midway. Initially, U.S. officials did not claim victory in the Battle of Midway because the War Department had faced severe criticism for falsely reporting earlier defeats as victories during the first months of the war.

In 1941, the New York stock market plummeted. As the situation worsened, the market continued to decline into the spring of 1942. German submarines prowled the U.S. East Coast, wreaking havoc on American shipping convoys and creating terrifying scenes. Churchill feared that Britain’s maritime supply lines might be severed. Meanwhile, in another part of the world, Singapore surrendered, Allied forces suffered a crushing defeat in the Battle of the Java Sea, Burma and the Dutch East Indies fell under Japanese occupation, and Corregidor, the last bastion in the Philippines, eventually capitulated. America’s war efforts stumbled, as repeatedly highlighted by the media, which criticized the ineffectiveness of U.S. military leadership.

In 1942, despite the strong resolve of the British and American people, they also felt despair about the future. Matthew Arnold’s famous poem 'Dover Beach' became widely circulated. He wrote: 'Ah, love, let us be true to one another! For the world, which seems so full of no joy, no love, no light, no certitude, no peace, nor help for pain; but only a darkling plain swept with confused alarms of struggle and flight, where ignorant armies clash by night.'

During the war years, so many lives were lost at sea, on land, and in the air that a short poem was frequently posted on bulletin boards in British officers’ mess halls.

There is an old belief:

On distant shores,

Far from despair and sorrow,

Old friends will meet again.

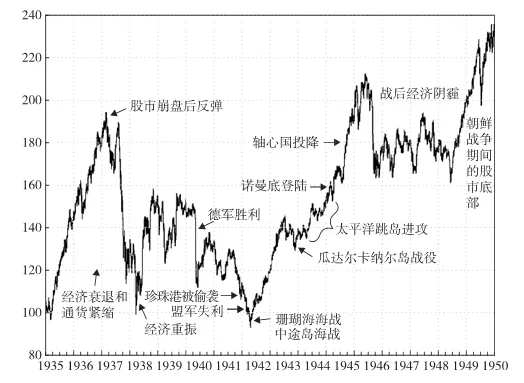

In early winter and spring of 1942, Japan's threat to invade Australia and its overwhelming victories in Southeast Asia caused sharp declines in stock prices in New York and London. The Allies suffered consecutive defeats, the Japanese forces appeared invincible, Germany successfully launched a new offensive against the Soviet Union, and Britain experienced continuous losses on the desert battlefield, all of which deeply unsettled investors. Although the Dow Jones Industrial Average briefly rose after Tokyo was bombed, by the end of April, it had fallen 20% for the year, reaching a low of just 92 points on April 30, 1942, down 30% from 132 points at the start of 1941.

As 1942 began with more losses and defeats, the stock markets in London and New York remained depressed. In fact, as Robert Sobel (who wrote the authoritative history of the New York Stock Exchange titled 'The Big Board') noted, February 1942 was the month with the lowest trading volume since the founding of the New York Stock Exchange in 1915. On February 14, trading volume amounted to only 320,000 shares, with only 30,000 shares traded in one hour. The price of a seat on the New York Stock Exchange fell to $17,000, the lowest since 1897, representing a 97% drop from the record high of $625,000 in 1929.

The moribund stock market also dealt a blow to the real estate market. Hotels in New York City sold for less than their annual earnings, while office rents on Wall Street dropped to as low as $1 per square foot. James Grant, in his masterpiece 'The Trouble with Prosperity,' described this phenomenon as what some called 'a drought panic.' Bear in mind, the slump in the stock and real estate markets occurred during a period of surging war production, massive budget deficits, and robust corporate profits.

However, concerns in the stock market went beyond this. The U.S. Treasury proposed setting the corporate income tax rate at 60%, and the Reaffirmation Committee intended to impose taxes on excess corporate profits, making corporate earnings and dividends unpredictable. For personal incomes exceeding $50,000, the income tax rate reached 85%. The Roosevelt administration seemed determined to balance income and wealth through mobilization. These tax policies, along with the poor performance of U.S. troops on the battlefield, further eroded investor confidence.

At the time, all rational forecasters held a pessimistic view of the future. In 1939, a prominent Harvard University professor (whose name is withheld out of respect) published an influential article. He pointed out that due to low birth rates and the lack of additional land for development, the U.S. economy was bound to enter a prolonged recession. Moreover, he stated there was a scarcity of new industries and inventions. However, at the time he wrote this article, the U.S. birth rate was rising, and the war had spawned thousands of new industries and technologies.

In early 1942, the poor performance of the U.S. military in the Pacific theater contributed to a degree of pessimism in the stock market. Initially, American media falsely reported the disastrous defeat of U.S. forces at Pearl Harbor, the complete annihilation of MacArthur's air force, and the setbacks of Anglo-American troops on the Asian battlefield. When the general public, especially investors, learned that these optimistic reports were either false or misleading, they lost faith in both the military and the press.

In early February 1942, Admiral Bill Halsey, nicknamed “Bull,” launched a surprise attack on Japanese forces in the Marshall Islands and the Gilbert Islands. A U.S. Navy pilot claimed during the battle to have sunk 16 Japanese warships. Halsey’s telegram described this great victory, recounting radio communications from U.S. pilots.

“Jack, stay away from that cruiser, it’s my target!” “Fantastic! Look at that bastard burning.” The Herald Tribune enthusiastically reported, “Bull’s Revenge!” “Pearl Harbor avenged!” Evan Thomas recounted that when Halsey’s flagship, the aircraft carrier Enterprise, returned to Pearl Harbor, sirens blared, and sailors and workers on the damaged docks cheered until they were hoarse. In reality, most of Halsey’s report was exaggerated. Only one Japanese transport ship and two small barges were sunk.

In February 1942, Leon Henderson, head of the Office of Price Administration, confidently predicted that the war would reduce Americans’ living standards to those of the Great Depression era. High-quality corporate bonds yielded 2.75%, while stocks yielded 8% to 9%. The chairman of MetLife declared that life insurance portfolios should not include stocks. The New York State Insurance Commission deemed stocks as “inappropriate investments” and prohibited insurers from investing in equities. This costly regulation was not repealed until the mid-1950s, by which time the post-war bull market was in full swing.

However, no one realized how cheap stocks were. Not only did dividend yields reach three times that of bond yields (whereas today the opposite is nearly true), but also, in April 1942, 30% of the stocks listed on the New York Stock Exchange traded at less than four times their 1941 earnings per share, with many stocks selling below net cash value. Over two-thirds of the stocks had price-to-earnings ratios between 4 and 6. W.E. Hutton quipped in aristocratic tones that President Roosevelt might “do well to pay more attention to those stock investors who live in poor housing, lack clothing, and sufficient food, who account for one-third of the total stock market population.” The average price-to-earnings ratio of 600 representative stocks was 5.3, and only 10% of all stocks had ratios exceeding 10.

Nevertheless, the bull market was slow to arrive. On April 13, 1942, Harry Nelson of Barron’s wrote:

In late 1928 and early 1929, some could foresee the impending sorrow, yet the market seemed indestructible. Logically, today’s market conditions favor buyers, but the market appears perpetually stagnant.

2. The Wise Timing of the U.S. Stock Market Bottom

Then, in May 1942, just before the U.S. military fortunes improved in the Pacific theater, the outlook seemed exceedingly bleak, and the U.S. stock market hit a historic low. Bad news from other parts of the world continued to pour in, yet the stock market sensed a turning point in the war against Japan. Although the Battle of the Coral Sea in early May was more of a draw than a victory for the United States, the Japanese offensive was halted for the first time, preventing them from capturing Port Moresby and losing a stepping stone for invading Australia. The U.S. Navy demonstrated that it could hold its ground even against the stronger Japanese Navy. Subsequently, the United States achieved a significant victory at the Battle of Midway. Despite fluctuations in the stock market when Rommel captured Tobruk in June 1942, the chart below shows that the lows in late April to early May marked the trough of the long bear market of the 1930s and early 1940s.

The stock market bottom in April to May 1942 was epic, giving birth to a new cyclical bull market. This bull market lasted for four years with only minor corrections and peaked on May 29, 1946. The year 1945 was extraordinary, with large-cap stocks rising 36.4% and small-cap stocks surging 73.6%. This was an incredible rally from the bottom of 1942. According to Ibbotson Associates, small-cap stocks rose 44.5% in 1942, 88.4% in 1943, 53.7% in 1944, and 73.6% in 1945. Once pessimism dissipated, stocks rebounded rapidly like a compressed spring being released.

In fact, the first major pullback in the U.S. stock market occurred in February 1946, when the Dow Jones Industrial Average experienced a typical "warning crack" decline, falling by 10%. The Dow Jones Industrial Average surged 14.2% over 78 trading days (when the market operated six days a week) starting from the low on February 26, forming a classic V-shaped reversal pattern and reaching its highest point since 1930 on May 29. Subsequently, the stock market declined for several months, including one month where it plummeted nearly 20%.

Afterward, the U.S. stock market fell into a severe post-war slump, undergoing nearly three years of sideways consolidation. This situation arose as the European economy struggled, the Cold War erupted, and the U.S. economy faced challenges adjusting. It was widely believed that without the stimulus of defense spending, the United States would fall into stagflation characterized by high unemployment. Inflation soared to 18% in 1946, 9% in 1947, but suddenly dropped toDeflation, reaching 1.8%. As shown in the chart below, both stocks and bonds remained sluggish until mid-1949, when the post-war global economic downturn began to dissipate.

Futubull【机会页】Celebrity portfolio tracking opportunities have been launched! Multiple celebrity portfolios are available for selection, allowing you to follow the strategies of major players with one click, accurately locking in high-quality investment targets, and investing with greater confidence!

Futubull【机会页】Celebrity portfolio tracking opportunities have been launched! Multiple celebrity portfolios are available for selection, allowing you to follow the strategies of major players with one click, accurately locking in high-quality investment targets, and investing with greater confidence!

Editor/Rice