On Tuesday, a $69 billion auction of two-year U.S. Treasury notes encountered weak demand, recording the largest tail since March 2023, with nearly no participation from foreign investors. Rising oil prices fueled inflation expectations, leading to a complete reversal of market rate-cut forecasts, with some even beginning to price in rate hikes. A $70 billion auction of five-year Treasury notes is scheduled for Wednesday, followed by a $44 billion auction of seven-year Treasury notes on Thursday.

As the conflict between the US and Iran continues to escalate, Wall Street is issuing a direct warning to the market—the US Treasury auction has encountered weak demand.

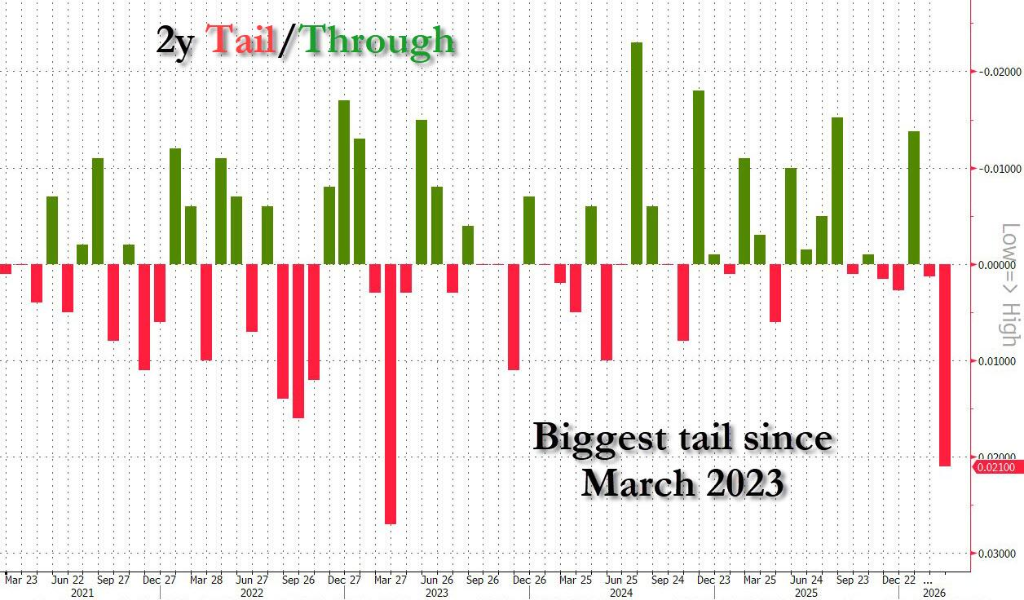

On Tuesday, March 24, the US Treasury's $69 billion two-year bond auction saw lackluster demand, far below expectations, with foreign investors nearly absent.

The two-year Treasury bonds were finally sold at a yield of 3.936%, higher than the secondary market's real-time trading yield just before the auction deadline, creating the largest tail difference since March 2023, reflecting weak market subscription interest.

The two-year Treasury bonds were finally sold at a yield of 3.936%, higher than the secondary market's real-time trading yield just before the auction deadline, creating the largest tail difference since March 2023, reflecting weak market subscription interest.

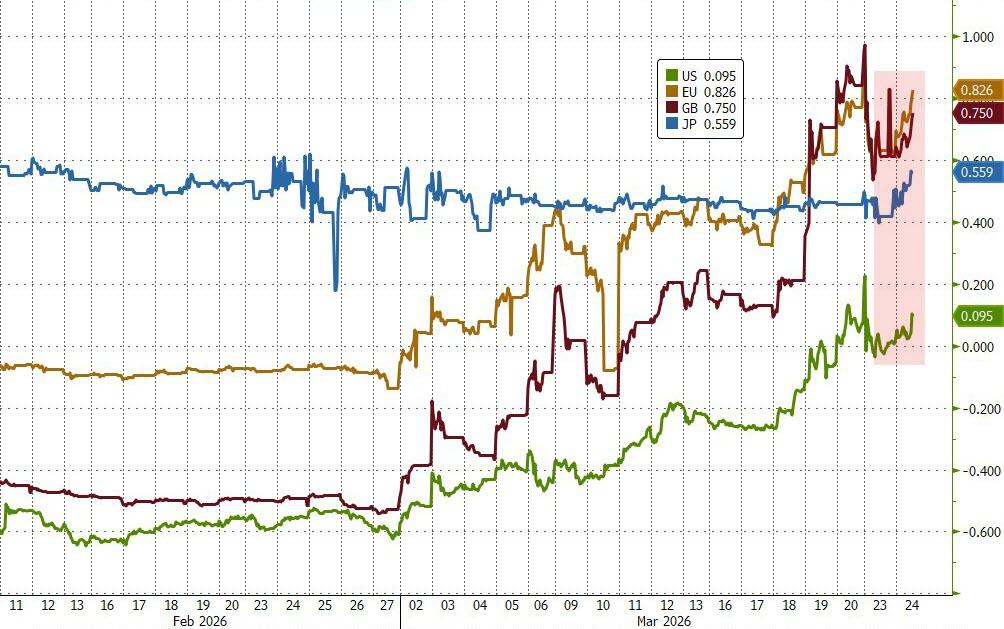

In addition, according to CCTV reports, part of the US 82nd Airborne Division is about to be deployed to the Middle East region. These dual factors pushed the two-year Treasury yield up by as much as 10 basis points to 3.96%, hitting an eight-month high, and drove yields across all maturities temporarily higher.

David Robin, an interest rate strategist at TJM Institutional Services, attributed the outcome to an extremely uncertain market environment:

Today’s auction unfortunately launched during a very difficult, volatile, and uncertain period. Why enter now? The risk-reward ratio is heavily skewed towards risk.

Notably, after the US stock market closed on Tuesday, according to CCTV News, Trump stated that US-Iran negotiations were 'likely quite close to reaching an agreement,' with Iran agreeing never to possess nuclear weapons. The report mentioned that the US intended to propose a one-month ceasefire and presented 15 peace negotiation clauses.

Treasury yields briefly retreated, partially erasing the day’s gains, while oil prices also fell in post-market trading. However, this did not fundamentally alter the market's cautious tone. A $70 billion five-year Treasury auction is scheduled for Wednesday this week, followed by a $44 billion seven-year Treasury auction on Thursday.

Oil price-driven inflation concerns have completely reversed expectations of interest rate cuts.

This auction result marked the highest yield for a two-year Treasury auction since May, whereas just a month ago, the previous two-year Treasury auction held on February 24 produced the lowest yield since 2022.

Ultimately, the persistent rise in oil prices driven by Middle East conflicts has reignited inflation expectations, nearly extinguishing hopes for a Fed rate cut this year. The market has even begun pricing in the possibility of a rate hike.

John Canavan, Chief Analyst at Oxford Economics, noted:

High oil prices have sustained modest market pricing for a potential Fed rate hike this year, while uncertainty has also temporarily dampened underlying auction demand.

He further stated:

The sell-off in U.S. Treasuries is partly an instinctive reaction to poor auction results, but the weak auction demand itself is also partly attributable to high oil prices.

Anthony Saglimbene, Chief Market Strategist at Ameriprise, pointed out:

High oil prices have exerted tangible pressure on the U.S. economy through rising prices and declining employment. Until there is greater clarity regarding the situation in the Middle East, particularly around the Strait of Hormuz, the stock market will remain under pressure.

The across-the-board rise in U.S. Treasury yields also implies higher borrowing costs and tighter financial conditions, posing a direct drag on both businesses and consumers. It is projected that approximately $10 trillion of U.S. debt will mature and require refinancing over the next year, making the pressure from rising borrowing costs significant.

Two-year Treasury bonds are typically the most sensitive instruments to market expectations of monetary policy and should theoretically attract safe-haven capital during a Fed rate-cutting cycle. However, the current rise in yields, coupled with a notable decline in auction demand, precisely indicates a shift in investors' outlook on policy prospects.

As Anthony Saglimbene remarked:

The market is beginning to question whether the issue will be that easily resolved.

Editor/Rocky