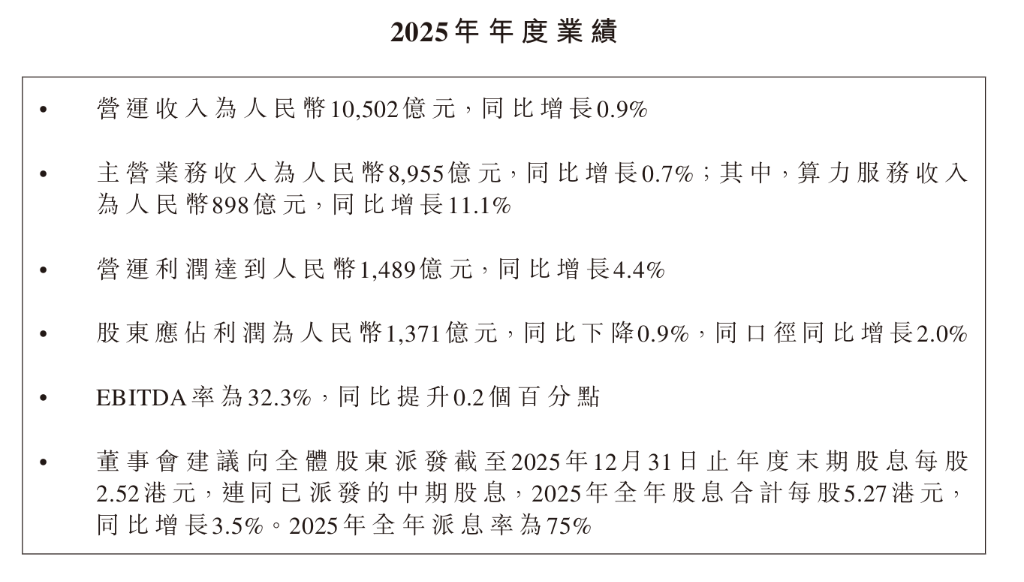

China Mobile's total operating revenue for the full year of 2025 exceeded the trillion-yuan mark, reaching RMB 1,050.2 billion, representing a year-on-year increase of 0.9%; core main business revenue amounted to RMB 895.5 billion, up by 0.7% year-on-year.

Revenue from the computing power services segment reached RMB 89.8 billion, marking an 11.1% year-on-year growth, with intelligent computing services showing an impressive growth rate of 279%.

$CHINA MOBILE (00941.HK)$On March 26, 2026, the company released its full-year 2025 financial results, presenting a report card that demonstrated steady progress.

For the full year of 2025, total operating revenue surpassed the trillion-yuan threshold, reaching RMB 1,050.2 billion, representing a year-on-year increase of 0.9%; core main business revenue was RMB 895.5 billion, up by 0.7% year-on-year. Facing pressure from slowing growth in traditional telecommunications businesses, the company relied on strong contributions from computing power services and intelligent services to maintain its overall profitability at the level of top-tier international operators.

For the full year of 2025, total operating revenue surpassed the trillion-yuan threshold, reaching RMB 1,050.2 billion, representing a year-on-year increase of 0.9%; core main business revenue was RMB 895.5 billion, up by 0.7% year-on-year. Facing pressure from slowing growth in traditional telecommunications businesses, the company relied on strong contributions from computing power services and intelligent services to maintain its overall profitability at the level of top-tier international operators.

On the profitability front, operating profit reached RMB 148.9 billion, reflecting a year-on-year increase of 4.4%, with EBITDA margin rising to 32.3%; however, net profit attributable to shareholders was RMB 137.1 billion, down slightly by 0.9% year-on-year. This decline did not stem from deteriorating core business operations; management specifically noted that excluding the one-time impact of changes in tax policies related to package revenue allocation, net profit under comparable terms actually increased by 2.0% year-on-year. The significant reduction in other gains in 2024 (from RMB 4.97 billion in 2024 to a loss of RMB 0.426 billion in 2025) and a decrease in interest and other income (from RMB 23 billion to RMB 18.3 billion) were the primary factors pressuring net profit.

From a strategic perspective,$CHINA MOBILE (00941.HK)$The company is at a critical juncture in transitioning from a 'telecommunications operator' to a 'communication + computing power + intelligence' integrated technology service enterprise. Combined revenue from computing power services and intelligent services now accounts for 20.2% of main business revenue, up by 1.4 percentage points from the previous year. With continued explosive demand for AI infrastructure, the computing power business is expected to become the core narrative supporting the company’s future valuation.

Traditional Telecommunications Business: Maintaining Scale Amid Value Pressure

Telecommunication services remain$CHINA MOBILE (00941.HK)$the cornerstone of the company’s revenue, contributing RMB 714.9 billion in 2025, but showing a slight year-on-year decline of 1.0%, with its share of main business revenue dropping to 79.8%.

In terms of user scale, the total number of mobile customers has reached 1.005 billion, with the market structure remaining fundamentally stable; the net increase in 5G customers reached 89.6 million, accumulating to 642 million, with a penetration rate rising to 63.9%. The number of 5G network base stations exceeds 2.77 million, taking the lead in introducing 5G-Advanced core network intelligence. The number of broadband internet customers hit a record high of 329 million, driving a 7.1% year-on-year increase in broadband network revenue, effectively offsetting the downward pressure on mobile traffic ARPU. The number of IoT card connections reached 1.48 billion, making the AIoT platform the world's largest connection management platform.

It is worth noting that voice service revenue dropped from 70.09 billion yuan to 66.63 billion yuan, and wireless internet service revenue fell from 385.9 billion yuan to 369.1 billion yuan, indicating that traditional incremental services have entered the stage of stock competition. The company was granted a license for satellite mobile communication business operations, marking the entry of satellite communications into commercial operation, which could pave the way for new traffic entry points in the future.

Computing Power Services: AI-driven computing power demand ignites growth engine

Computing power services have become$CHINA MOBILE (00941.HK)$the growth pole with the most potential. In 2025, revenue from this segment reached 89.8 billion yuan, representing an 11.1% year-on-year increase, with intelligent computing services growing by an impressive 279%, becoming the true "primary engine," driving overall cloud computing services to grow by 13.9% year-on-year.

At the infrastructure level, the company's total intelligent computing capacity reached 92.5 EFLOPS (FP16), covering full-scale computing capabilities from hundreds to over ten thousand cards, with more than 1.5 million standard IDC racks available for external services. Revenue from AIDC (AI Data Centers) grew by 35.4% year-on-year, significantly outpacing the overall data center revenue growth of 8.7%, demonstrating that AI-dedicated computing power is rapidly replacing general-purpose computing as the primary demand driver.

On the network side, the company has established a three-tiered computing power latency circle of 1 millisecond within metropolitan areas, 5 milliseconds within provinces, and 20 milliseconds nationwide. The inter-provincial backbone 400G OTN network has achieved near-complete national coverage, forming a differentiated competitive barrier through "integrated computing and networking." The monthly active users of the cloud drive reached 210 million, with cloud video users surpassing 86.7 million. The consumer penetration of the Mobile Cloud brand is also accelerating.

Intelligent Services: Large model applications transition from R&D to commercial implementation

The intelligent services segment generated revenue of 90.8 billion yuan in 2025, representing a 5.3% year-on-year increase, emerging as the third growth curve beyond communications and computing power.

$CHINA MOBILE (00941.HK)$The layout in this track has become quite comprehensive: the Jiutian foundational large model has been upgraded to version 3.0, topping the OpenCompass ranking; over 100 AI+ products and application solutions and 29 vertical-specific intelligent agents have been launched; a self-built high-quality dataset of 3,500 TB has been created; and more than 50 proprietary industry-focused large models have been developed, concentrating on vertical fields such as energy, water conservancy, and agriculture, collaborating with industry leaders to co-build industry-specific large models.

In terms of implementation data, revenue from data algorithms increased by 12.6% year-on-year, and revenue from digital intelligence culture grew by 13.3% year-on-year. The AI-powered assistant 'Lingxi' has surpassed 100 million monthly active users, with the capability platform being invoked over 1.4 trillion times, and more than 80,000 active digital intelligence employees. AI has also begun to demonstrate initial success in reducing costs and improving efficiency in internal operations. In the area of embodied intelligence, the company has independently developed a large VLA model with 3 billion parameters, and its quantum computing cloud platform exceeds 2,000 qubits, establishing an early-mover advantage in emerging fields.

Behind the profit decline: One-off factors dominate, while operational fundamentals remain intact

The net profit decrease of 0.9% year-on-year appears concerning at first glance, but a deeper analysis of the financial report reveals that the decline was primarily driven by three types of non-recurring factors.

Firstly, the 'Other (Loss)/Gain' item plummeted from RMB 4.97 billion in 2024 to a loss of RMB 426 million in 2025, including the negative impact of tax adjustments related to bundled revenue. Secondly, interest and other income fell from RMB 23 billion to RMB 18.3 billion, mainly due to a reduction in net gains from holding/disposing financial assets from RMB 16.73 billion to RMB 13.01 billion. Thirdly, financing costs slightly increased to RMB 3.66 billion.

After excluding these factors, operating-level net profit on a comparable basis grew by 2.0% year-on-year, consistent with the 4.4% increase in operating profit, indicating stable profitability in core businesses. The effective corporate tax rate also declined, with the actual tax burden in 2025 standing at approximately 21.8%, slightly lower than 22.3% in 2024.

Editor/Melody