This article is from Golden Finance, authored by Taozhu.

Over the past month, $Bitcoin (BTC.CC)$ an extremely unusual phenomenon has emerged in the market.

Compared to the cryptocurrency treasury boom a few months ago, BTC has now exited the collective buying phase.

The buyers driven by treasury demand are almost entirely limited to $Strategy (MSTR.US)$ 。

The buyers driven by treasury demand are almost entirely limited to $Strategy (MSTR.US)$ 。

First, only Strategy continues to buy.

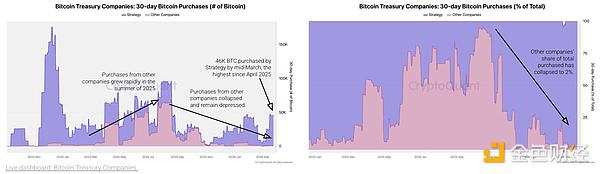

According to an analysis by CryptoQuant, Bitcoin treasury demand is currently fully driven by Strategy. Over the past 30 days, Strategy purchased 45,000 Bitcoins, while other companies collectively bought only about 1,000, marking a 99% decrease from previous levels and reducing their share of total purchases to just 2%. This indicates that new demand has almost completely vanished. Strategy now holds approximately 76% of the Bitcoin treasury share, reflecting a highly concentrated industry with a lack of broad corporate demand.

Strategy made four Bitcoin purchases in March, with the most recent purchase occurring on March 23.

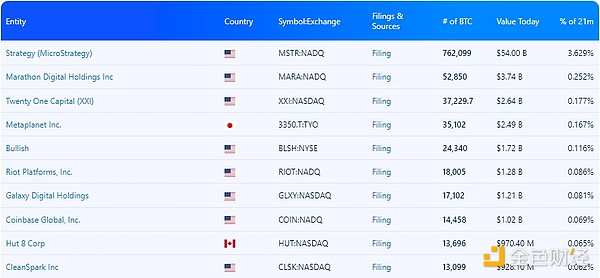

It currently holds 762,099 Bitcoins, maintaining its position as the largest holder, accounting for 3.629% of the total 21 million supply.

Moreover, seemingly to continue increasing its Bitcoin holdings, Strategy announced on March 23 the launch of a new 21 billion USD STRC equity issuance plan and a new 21 billion USD MSTR equity issuance plan, bringing the total financing scale to 42 billion USD.

The revised ATM equity plan by Strategy enables it to gradually sell more shares in the open market rather than raising less capital from external investors through convertible bonds as before. Strategy's preferred shares, such as STRC and STRK, pay dividends to investors monthly while allowing Strategy to increase its Bitcoin holdings without issuing additional MSTR common stock.

Corporate buying of BTC has evolved from being conducted by multiple companies to almost solely by Strategy, with corporate demand for BTC treasury essentially vanishing overnight.

Julio Moreno, Director of Research at CryptoQuant, pointed out earlier this year: 'Most new corporate Bitcoin buyers only made one or two purchases before ceasing trading, failing to provide sustained price support.' Compared to the expansion phase of 2023-2024, year-on-year demand growth for BTC has significantly slowed. Currently, this indicator is below the historical trend line, indicating that capital is contracting rather than being driven by the adoption waves that typically fuel bull markets.

II. Why Are Other Companies No Longer Buying?

1. Decreased Risk Appetite

The expectation that the Federal Reserve will continue to cut interest rates remains uncertain. In the current environment of higher interest rates, the cost of capital is high, and stable returns can be obtained through U.S. Treasuries. Therefore, allocating funds to crypto assets has become a less preferred option.

Coupled with a sluggish global economy and frequent geopolitical conflicts, most companies are adopting conservative financial strategies under these circumstances.

2. Bear Market in Cryptocurrencies

In 2025, a surge of cryptocurrency treasury companies emerged, providing Wall Street investors with alternative avenues to invest in cryptocurrencies. As Bitcoin continued to climb and reached its peak in October, many companies' stock prices rose accordingly. However, the subsequent overall decline in the crypto market has impacted the valuations of these companies.

Altan Tutar, Co-founder and CEO of MoreMarkets, made a pessimistic prediction about crypto treasury companies last year: 'Most Bitcoin treasury companies will disappear just like other DATs.'

After October last year, the cryptocurrency market entered a downward trend, with new demand slowing and even showing signs of 'demand exhaustion.' For most companies, holding cryptocurrency reserves is no longer a favorable option, as volatility and the declining trend have directly undermined confidence in purchasing.

Previously, many companies hoarded various cryptocurrencies because it created a positive feedback loop: issuing stock to buy a certain coin; gaining more market attention by holding that coin, which boosted stock prices; then using raised funds to buy more coins...

This self-reinforcing model requires the market to remain in a bull phase. However, when the cryptocurrency market falters, this model fails. Declining prices lead to shrinking book profits for companies, which in turn erodes investor confidence, pressures stock prices, further impacts companies' financing capabilities, and ultimately leaves them without surplus funds to continue buying.

For example, at the end of February, Ethereum treasury FG Nexus reduced its holdings by another 7,550 ETH, worth approximately $14.06 million. The reason for the sale was losses: the company had purchased 50,600 ETH between August and September 2025 during the DAT company boom at an average price of about $3,940 per ETH, totaling $200 million. To date, FGNexus has incurred cumulative losses of $86.98 million from its Ethereum investment.

As BTC prices continue to fluctuate downward, many cryptocurrency treasury companies have stopped purchasing cryptocurrencies and shifted their preference toward more conservative cash and low-risk asset management.

Companies rush into the market en masse during bull markets and disperse just as quickly during bear markets. Stable buyers have become cyclical participants.

Section Three: Why is Strategy Still Dominating Among Veteran Players?

While most companies are choosing to exit, Strategy stands out as a notable exception.

For most companies, BTC and other cryptocurrencies represent part of their asset allocation. For Strategy, however, BTC serves as the foundation of the company's valuation logic, its core asset, and the cornerstone of its narrative—Strategy has consistently played the role of a Bitcoin bull through both bull and bear markets.

Moreover, for Strategy, BTC has become a matter of belief. Michael Saylor positions Bitcoin as 'Digital Capital,' referring to it as the ultimate reserve asset of the 21st century. On March 22, Saylor stated, 'The orange march continues.' Despite a 10% loss on the company’s Bitcoin investments due to the market crash last weekend, the company still increased its Bitcoin holdings.

Finally, Strategy has become deeply tied to Bitcoin. When investors purchase shares of Strategy, they are effectively gaining exposure to Bitcoin. Strategy has transformed itself into an ETF-like product with leverage. Therefore, during unfavorable market conditions, Strategy must continue to increase its holdings.

In summary, even though the overall cryptocurrency market may be underperforming, Strategy continues to buy Bitcoin due to long-term conviction, counter-cyclical accumulation, and ongoing enhancement of Bitcoin exposure.

Bernstein analysts noted: 'Strategy plays the role of Bitcoin’s ultimate safe haven bank, while Bitcoin ETFs are attracting more resilient (and less speculative) sources of capital. The robust capital base of Bitcoin is continuously expanding.'

IV. Implications of Strategy's Unique Dominance

In the short term, Strategy's continuous purchases will have a positive impact on Bitcoin prices. When other companies stop buying, Strategy’s steady acquisitions can ease market selling pressure and prevent a sharp decline in Bitcoin prices. However, this support also depends on Strategy: factors such as lower-than-expected financing or slower accumulation may weaken Strategy’s ability to increase holdings, which could further lead to downward pressure on Bitcoin prices.

In the long run, the increasing concentration of Bitcoin in the hands of one company reduces the market's risk resilience. Should Strategy adjust its strategy, it could significantly impact confidence in the cryptocurrency market.

Strategy is no longer just a participant but a key variable influencing the stability of the cryptocurrency market.

Editor/KOKO