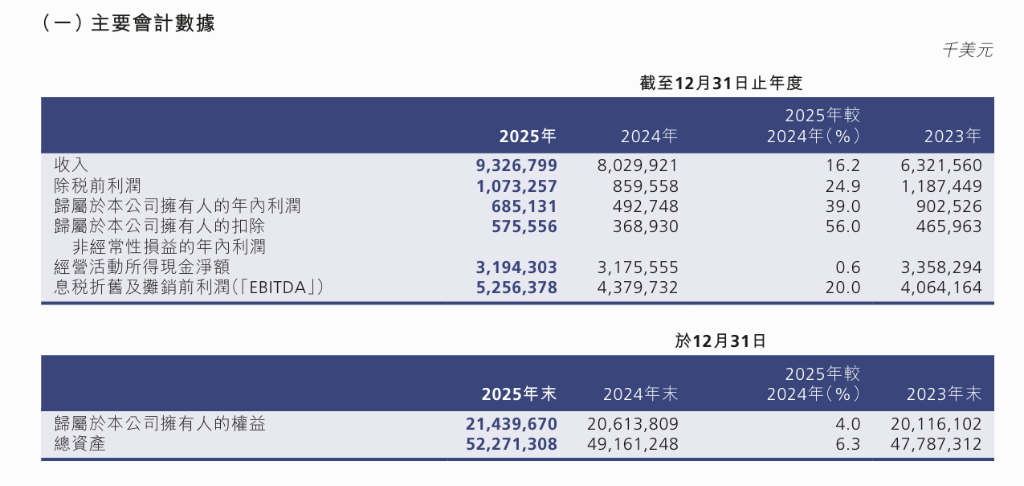

SMIC reported revenue of $9.327 billion and a net profit of $685 million in 2025, both reaching record highs. Monthly capacity exceeded one million wafers, with capacity utilization rising to 93.5%, driving gross margin recovery.

The company remains the world's second-largest foundry and is advancing the integration and capital increase of SMIC Northern and Southern operations. It forecasts that its revenue growth for 2026 will exceed the industry average, with capital expenditure remaining roughly flat compared to 2025.

$SMIC (00981.HK)$Revenue and profit in 2025 hit all-time highs. Despite increasing depreciation pressures, significant improvements in capacity utilization drove gross margin back onto an upward trajectory, maintaining the company’s position as the second-largest pure-play foundry globally.

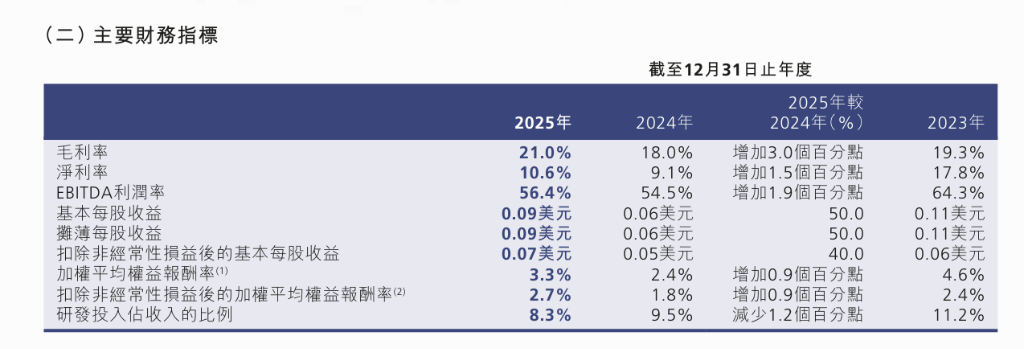

According to the company's announcement on the 26th, SMIC achieved annual revenue of $9.327 billion in 2025, representing a year-on-year increase of 16.2%. Net profit attributable to shareholders of the parent company was $685 million, up 39.0% year-on-year. Despite substantial growth in depreciation, gross margin rose to 21%, increasing by three percentage points year-on-year.

According to the company's announcement on the 26th, SMIC achieved annual revenue of $9.327 billion in 2025, representing a year-on-year increase of 16.2%. Net profit attributable to shareholders of the parent company was $685 million, up 39.0% year-on-year. Despite substantial growth in depreciation, gross margin rose to 21%, increasing by three percentage points year-on-year.

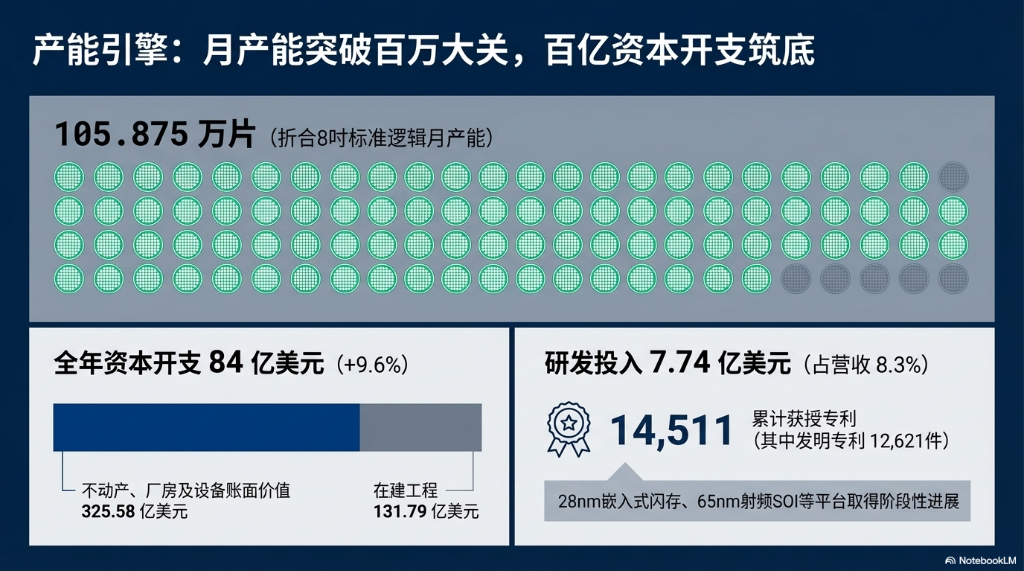

In 2025,$SMIC (00981.HK)$The company maintained high R&D investment at $774 million, accounting for 8.3% of sales revenue. Monthly capacity, in terms of equivalent 8-inch standard logic wafers, surpassed one million units during the year, with capacity utilization rising to 93.5%, up 8 percentage points year-over-year. Annual wafer shipments grew by 20.9% year-over-year to 9.697 million units.

For 2026, the company provided guidance in its annual report: assuming no major changes in the external environment, revenue growth will exceed the industry average for comparable peers, while capital expenditure is expected to remain roughly level with 2025. Meanwhile, the company is advancing two major transactions: acquiring 49% of SMIC Northern through an A-share issuance and increasing SMIC Southern’s registered capital from $6.5 billion to approximately $10.08 billion via a capital increase. No cash dividends were declared, as the company expects capital expenditure in 2026 to still exceed 20% of audited net assets.

Record-high revenue and profit

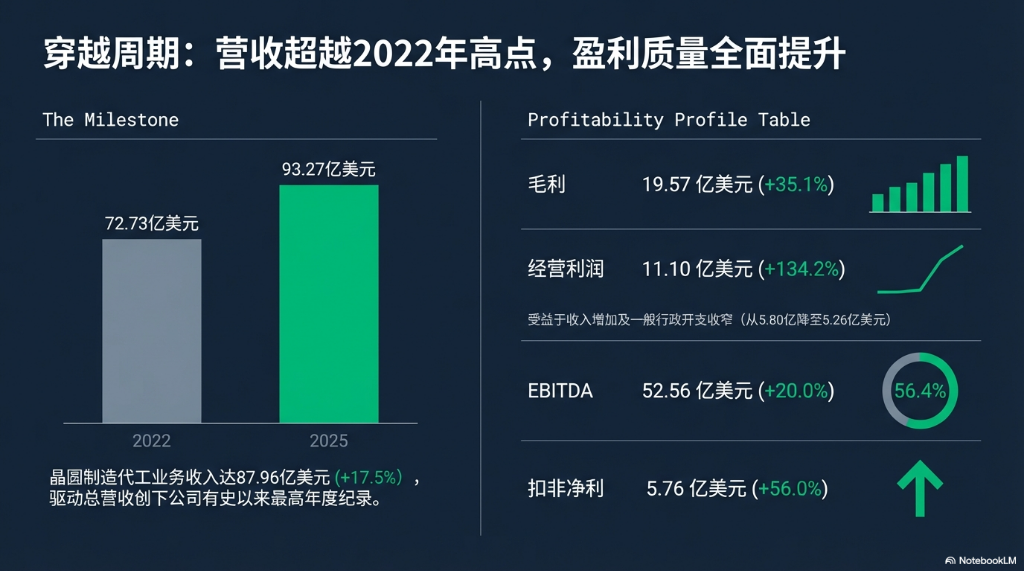

$SMIC (00981.HK)$Revenue in 2025 totaled $9.327 billion, surpassing the previous high of $7.273 billion in 2022, marking the highest annual revenue in the company’s history. The growth in revenue was primarily driven by shipment volume: wafer shipments increased by 20.9% year-on-year, while the average selling price slightly decreased from $933 per unit in the previous year to $907. Revenue from wafer manufacturing and foundry services amounted to $8.796 billion, up 17.5% year-on-year.

Profitability improved across the board. Gross profit increased from $1.448 billion in the previous year to $1.957 billion, a rise of 35.1%. Operating profit surged by 134.2% year-on-year from $474 million to $1.11 billion, mainly due to higher revenue and reduced general administrative expenses (from $580 million to $526 million). Net profit attributable to shareholders of the parent company, excluding non-recurring items, was $576 million, up 56.0% year-on-year, outpacing the growth rate of net profit including non-recurring items, reflecting enhanced earnings quality. EBITDA reached $5.256 billion, up 20.0% year-on-year, with the EBITDA margin rising to 56.4%.

Notably, depreciation and amortization for the full year amounted to $3.81 billion, an increase of approximately 18% compared to $3.223 billion in the previous year, indicating continued upward pressure on depreciation. Against this backdrop, the improvement of three percentage points in gross margin underscores the positive impact of capacity utilization and product mix optimization on profitability.

Accelerated capacity expansion, monthly capacity exceeding one million units

By the end of 2025,$SMIC (00981.HK)$Monthly capacity reached 1.05875 million units in terms of equivalent 8-inch standard logic wafers, with annual capacity utilization hitting 93.5%, an increase of 8 percentage points year-over-year. The company incurred cash expenditures on property, plant, and equipment amounting to approximately $8.4 billion during the year, a year-over-year increase of 9.6%. By year-end, the book value of property, plant, and equipment rose to $32.558 billion, while the book value of construction in progress stood at $13.179 billion, reflecting substantial ongoing capacity expansion.

The structure of the balance sheet was adjusted accordingly. The company's total interest-bearing debt increased from USD 11.596 billion at the end of the previous year to USD 12.596 billion, with borrowings amounting to USD 12.588 billion. The weighted average effective interest rate was 1.74% for RMB-denominated debt and 3.84% for USD-denominated debt. The net debt-to-equity ratio shifted from -10.6% (i.e., a net cash position) at the end of the previous year to 1.9%, indicating that the company moved slightly from a net cash position to a net debt position. Net cash flow generated from operating activities amounted to USD 3.194 billion, remaining largely unchanged from the previous year.

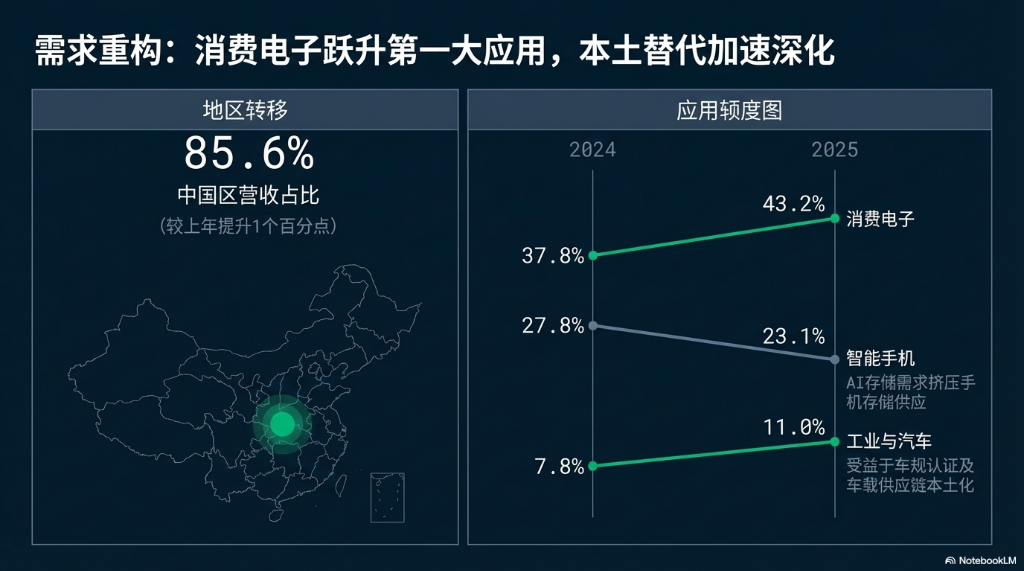

Domestic demand structure diverged, with consumer electronics gaining a larger share.

In 2025, revenue from China accounted for 85.6% of the total, up from 84.6% in the previous year, reflecting the ongoing trend of localization substitution. In terms of application structure, the share of wafer sales for consumer electronics expanded from 37.8% to 43.2%, becoming the largest application category. The share for smartphones declined from 27.8% to 23.1%, while the share for industrial and automotive applications increased from 7.8% to 11.0%, benefiting from the implementation of automotive certifications and the accelerated localization of domestic vehicle electronics supply chains.

Management noted in the annual report that strong demand for storage driven by artificial intelligence has squeezed the supply of memory chips available for other consumer electronics sectors such as mobile phones, potentially suppressing end-user demand through price increases. However, the company's technological expertise in areas such as BCD, analog, MCU, and mid-to-high-end display drivers allows it to maintain a favorable position.

In terms of R&D, investment in 2025 reached USD 774 million, accounting for 8.3% of revenue, down from 9.5% the previous year, mainly reflecting an increase in the revenue base. The company achieved phased progress across multiple platforms, including its 28nm embedded flash platform and 65nm RF-SOI. By the end of the year, the company had been granted a cumulative total of 14,511 patents, of which 12,621 were invention patents.

M&A integration advanced: acquisition of SMIC Northern and capital increase for SMIC Southern.

September 2025,$SMIC (00981.HK)$In September 2025, the company signed agreements with five counterparties, including the National Integrated Circuit Fund, to acquire a 49% stake in SMIC Northern through the issuance of new ordinary A-shares denominated in Renminbi. In December, the parties finalized the consideration and number of shares to be issued. The extraordinary shareholders' meeting approved the transaction in February 2026. The application has been accepted by the Shanghai Stock Exchange. Upon completion of the transaction, the company will own 100% of SMIC Northern, which is expected to enhance asset quality and streamline corporate governance.

Meanwhile, in December 2025, SMIC Southern completed a capital increase, raising its registered capital from USD 6.5 billion to USD 10.0773 billion, with participation from multiple investors including Phases I, II, and III of the National Integrated Circuit Fund and the Shanghai Integrated Circuit Fund. After the capital increase, the company holds a 41.561% stake in SMIC Southern through SMIC Holdings, retaining control. The company stated that the capital increase aims to reduce SMIC Southern's debt-to-asset ratio and optimize the group's financial structure.

2026 Outlook: Growth guidance outperforms peers, but external risks remain.

In its annual report, the company expressed a positive outlook for 2026, anticipating that the trend of overseas supply chain reshoring and the replacement of older products with new ones by domestic customers will continue, creating incremental opportunities for local supply chains. The company provided guidance indicating that revenue growth would exceed the industry average, while capital expenditures are expected to remain broadly in line with 2025 levels.