Bank of America's latest report: Market sentiment has cooled, the sell signal has ended, but neither a concentrated capitulation of bulls nor macro panic has emerged, and the buy signal has yet to be triggered. Recently, stocks and gold have been heavily sold off, with funds flowing into short-term bonds as a safe haven. Bank of America predicts that policymakers will be forced to act to avoid a recession, triggering a 'policy panic-driven easing,' with oversold assets such as gold and software worth monitoring.

The latest fund flow report from Bank of America shows that market sentiment has notably cooled from extreme optimism, but key buy signals have yet to be triggered, and the timing for contrarian investors to enter remains premature.

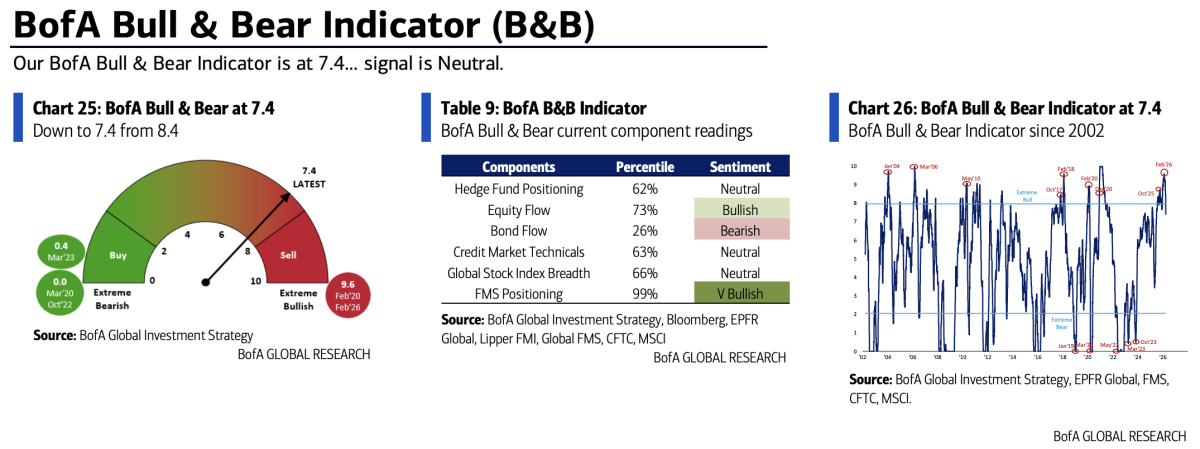

According to Storm Chaser Trading Desk, Bank of America strategist Michael Hartnett released the latest report on March 27. The Bank of America Bull & Bear Indicator dropped sharply from 8.4 to 7.4. Since the sell signal was issued on December 17 last year, the S&P 500 Index has fallen by 5% cumulatively, with the maximum peak-to-trough drawdown reaching 7%.

Although the sell signal has officially ended, several trading rules at Bank of America indicate that the market has not witnessed either a concentrated capitulation of bulls or macro-level panic (i.e., significant downward revisions in GDP and earnings-per-share forecasts), meaning conditions for contrarian buying are insufficient.

Although the sell signal has officially ended, several trading rules at Bank of America indicate that the market has not witnessed either a concentrated capitulation of bulls or macro-level panic (i.e., significant downward revisions in GDP and earnings-per-share forecasts), meaning conditions for contrarian buying are insufficient.

Bank of America believes that policymakers will be compelled to take action to prevent a recession, leading to 'policy panic-driven easing.' Additionally, once the Middle East conflict is resolved, Trump may push for certain measures to protect American consumers from the impact of a recession and consolidate his support among voters.

Bull & Bear Indicator retreats, sell signal ends but no buy signal emerges

The Bank of America Bull & Bear Indicator plummeted this week from 8.4 to 7.4, its lowest level since July 2025, mainly due to deteriorating breadth in global equity indices, outflows from high-yield bonds and emerging market debt, and widening credit spreads.

This indicator previously triggered a sell signal on December 17, when the reading was above 8.0. Since then,$S&P 500 Index (.SPX.US)$it has fallen by 5% cumulatively, with the maximum peak-to-trough drawdown reaching 7%.

Based on Bank of America's historical statistics since 2002 covering 32 sell signal periods, the average returns for the S&P 500 and MSCI World Index in the subsequent three months were only 1%, lacking strong rebound appeal.

Compared to previous major market bottoms, the current indicator reading remains significantly high. During the 'equivalent tariff' sell-off in April 2025, the indicator fell to 3.4; at the height of the COVID-19 pandemic panic in 2020, it once dropped to 0.0, far from the extreme levels seen during historical market bottoms.

Global Breadth Rule: Further declines still needed to trigger buy signal

Bank of America believes that the most likely indicator to first trigger a buy signal is the 'Global Breadth Rule' – which generates a buy signal when 88% of global stock indices simultaneously fall below their 50-day and 200-day moving averages.

Currently, this indicator reads at -16%, having once touched -39% on Monday (March 23), but has since recovered somewhat. According to Bank of America calculations, triggering a buy signal would require an additional decline of approximately 2% in the Asia-Pacific stock market, about 3% in emerging markets, and roughly 14% in Latin American markets.

Other indicators also remain below buy thresholds: cash positions in global fund manager surveys stand at 4.3%, with the buy threshold being 5.0%; the Global Flow Trading Rule requires outflows exceeding 1% of assets under management from global equities and high-yield bonds within four weeks to trigger a signal, while the current reading is only -0.8%.

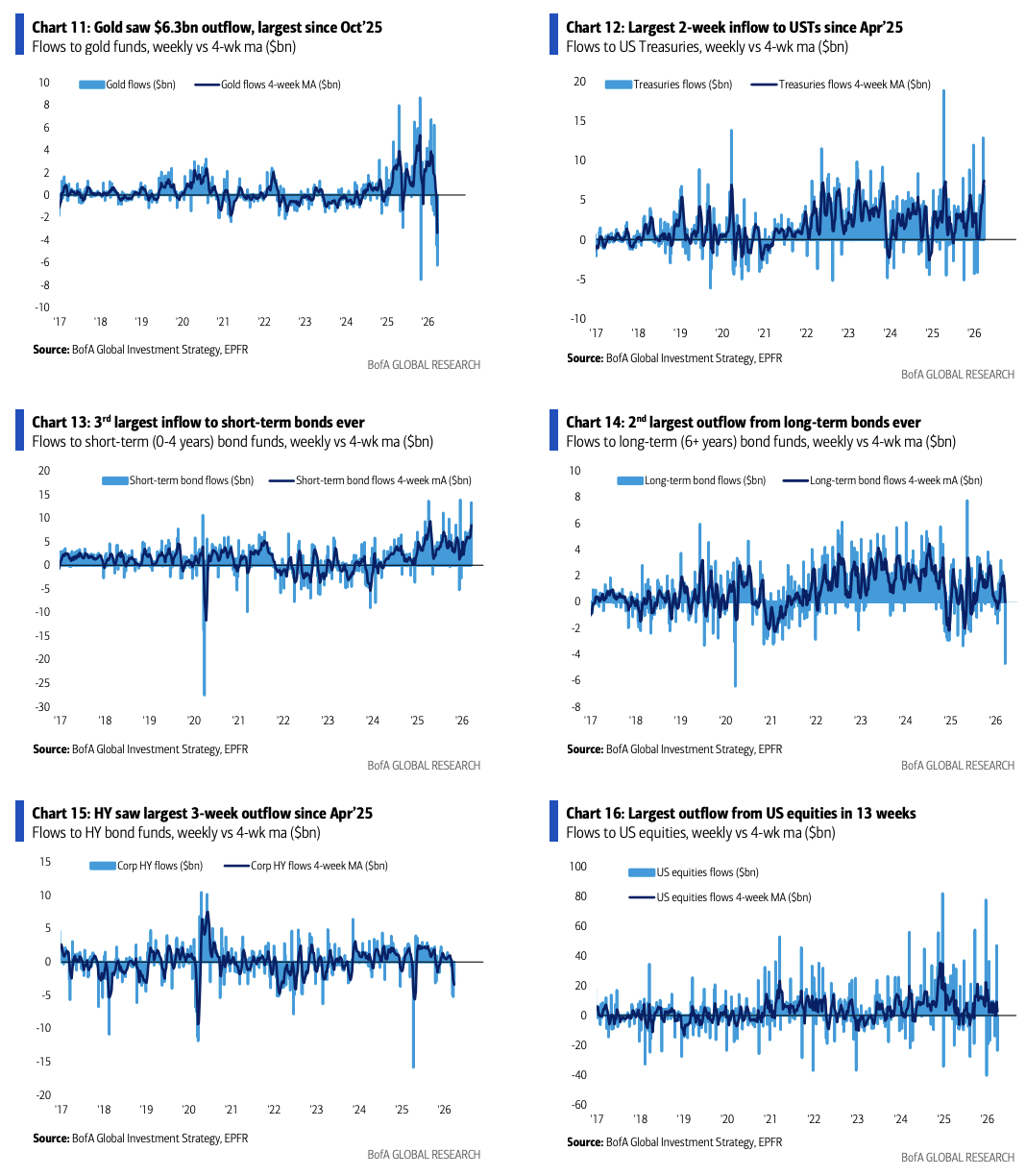

Massive capital exodus: Equities, high-yield bonds, and gold all experience net outflows

This week's capital flows exhibited clear risk-averse characteristics. U.S. equities recorded a weekly outflow of $23.5 billion, the largest in nearly 13 weeks; European equities saw an outflow of $3.1 billion, marking the largest weekly outflow since April 2025; outflows from the materials sector reached $10.5 billion, setting a new historical record.

High-yield bonds have experienced net outflows for five consecutive weeks, with this week's outflow reaching $3.3 billion. Over three weeks, cumulative outflows amounted to $13.5 billion, representing the largest three-week outflow since April 2025. Gold funds recorded a weekly net outflow of $6.3 billion, the largest single-week outflow since October 2025.

Capital primarily flowed into short-term fixed-income assets: U.S. Treasuries attracted inflows of $6.8 billion this week, with cumulative inflows over two weeks totaling $19.7 billion, the largest two-week inflow since April 2025. Short-term bonds (with maturities of four years or less) recorded inflows of $13.3 billion, marking the third-largest weekly inflow in history.

In contrast, long-term bonds (with maturities exceeding six years) experienced outflows of $4.7 billion, the largest single-week outflow since March 2020 and the second-largest in history.

Bank of America's baseline outlook: Policy panic looming, awaiting better buying opportunities

Based on a comprehensive assessment of various indicators, Bank of America’s basic outlook is that policymakers will be compelled to take action to prevent an economic recession, thereby triggering a "policy panic-driven easing."

However, prior to this, the market may continue to experience wide-ranging fluctuations—a trend that began in October to November last year when liquidity peaked, optimism surrounding AI capital expenditure reached its zenith, and following Trump's electoral defeats in New York, New Jersey, and the Virgin Islands. Bank of America believes this pattern is highly likely to persist until the November 2026 midterm elections.

Bank of America strategists recommend that, at this stage, there is no need to rush into the market, nor is it advisable to chase gains greedily.

Against the backdrop of a bear market in the US dollar and fiscal expansion trends in other parts of the globe, opportunities for gold bulls are expected to gradually return. Meanwhile, Bank of America identifies software, private equity, and consumer finance as the most contrarian long positions in Q2—these assets are currently in oversold ranges relative to their 50-day and 200-day moving averages.

Editor/Melody