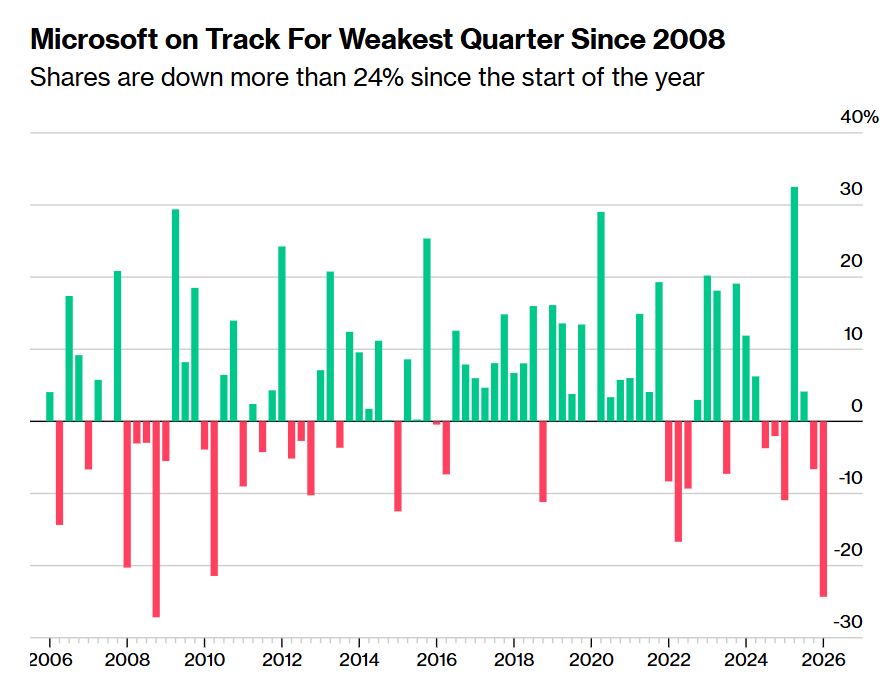

Microsoft is on track to record its worst quarterly performance since 2008, with artificial intelligence impacting the company's growth prospects from two directions. Due to market concerns over investments in AI infrastructure and competition from AI startups, Microsoft's stock price is heading towards its poorest quarterly showing since the global financial crisis.

The American technology giant $Microsoft (MSFT.US)$ appears to be at the intersection of two unsettling trends roiling the technology sector, which could result in its stock experiencing the worst quarterly performance since the global financial crisis nearly two decades ago.

First, this software behemoth with a market value close to $3 trillion globally is doubling down on AI capital expenditure. However, an increasing number of investment institutions on Wall Street are questioning when the growing investment in artificial intelligence computing infrastructure will yield more significant returns in revenue and profit growth. Secondly, the pessimistic narrative of “AI disrupting everything” has led global investors to continuously sell off software stocks because they fear that AI startups like Anthropic and OpenAI are developing AI agents focused on highly efficient workflows that could completely replace Microsoft’s SaaS software products.

Jonathan Cofsky, portfolio manager at Janus Henderson Investors, stated: 'There is indeed a concern in the market that customers will no longer pay Microsoft but instead turn directly to large AI model providers, which could impact Microsoft's core growth business, or at least put pressure on the company's pricing and profit margins.' Nevertheless, Jonathan Cofsky remains firmly committed to holding Microsoft shares.

Jonathan Cofsky, portfolio manager at Janus Henderson Investors, stated: 'There is indeed a concern in the market that customers will no longer pay Microsoft but instead turn directly to large AI model providers, which could impact Microsoft's core growth business, or at least put pressure on the company's pricing and profit margins.' Nevertheless, Jonathan Cofsky remains firmly committed to holding Microsoft shares.

From a bet worth hundreds of billions of dollars to signs of weakening moats, the company’s stock price fell by 24% in the first quarter, putting it on track for the largest quarterly decline since the 27% drop in the fourth quarter of 2008. This year, among the Magnificent Seven—tech companies that have seen the highest market investment enthusiasm in recent years—Microsoft has been the weakest performing tech giant so far. A benchmark index tracking this group (Magnificent Seven benchmark index) fell by 13% over the same period.

As shown in the chart above, Microsoft’s stock is set to record its weakest quarterly performance since 2008—its share price has fallen by more than 24% since the beginning of the year.

Cofsky stated: 'Microsoft has become more capital-intensive.' 'For the stock to perform better in the future, we need to be more confident that there will not be a substantial slowdown in the growth of its core software business.'

As leading artificial intelligence model companies like Anthropic and OpenAI recently launched a series of AI agent products focused on high-efficiency proxy workflows, these innovations are highly likely to replace certain functional software services at a much lower cost. Global software stocks have suffered heavy sell-offs. The iShares Expanded Tech-Software Sector ETF (IGV.US), which tracks the U.S. software industry, has plummeted approximately 40% from its record high in September, firmly entering deep bear market territory.

Since February, the pessimistic tone of “AI disrupting everything” has been driven primarily by growing concerns that AI agent workflows like Claude Cowork and OpenClaw (formerly known as Clawdbot and Moltbot), which have gained immense popularity and spread virally, could undermine the entire software empire built on the SaaS seat subscription revenue model. This triggered a rare wave of sell-offs that quickly spilled over into industries such as insurance, real estate, trucking, and any other sectors perceived to rely on seat-based revenue models or labor-intensive business models — areas the market believes will be thoroughly disrupted by AI.

Microsoft Stands at the Most Dangerous Crossroads Since the AI Super Bull Market

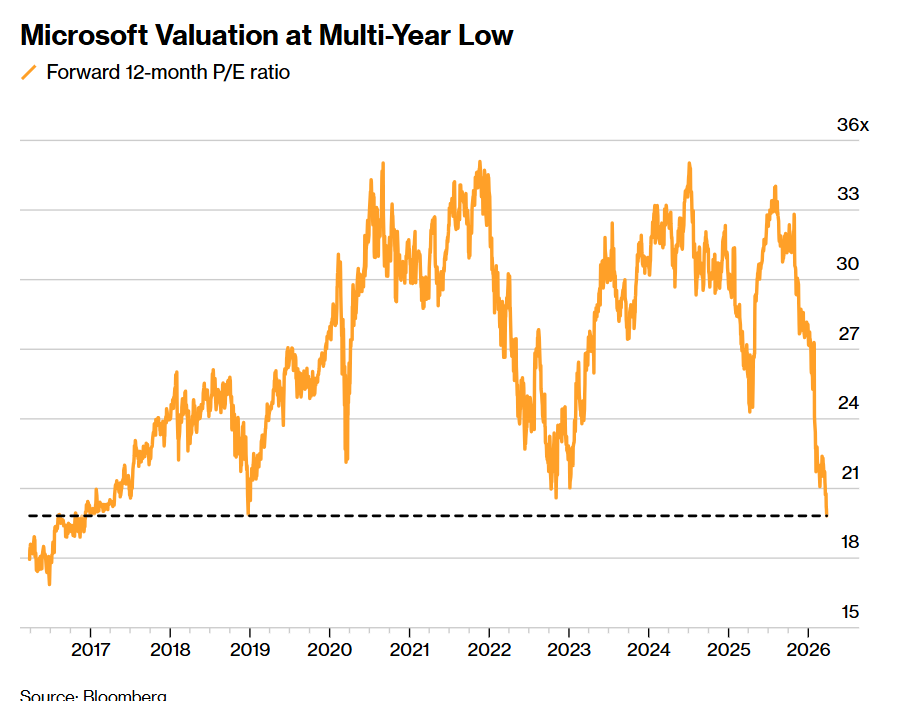

This selloff has even made the stock appear relatively cheaper compared to other tech giants and the Nasdaq Index, with its forward price-to-earnings ratio for the next 12 months falling below 20 times, the lowest since June 2016. As shown in the chart below, Microsoft’s valuation is at a multi-year low.

Microsoft’s valuation multiples are only slightly higher than those of the S&P 500 Index. However, during this recent downturn, Microsoft once briefly became cheaper than the S&P 500, meaning its valuation multiples temporarily dropped below that of the S&P 500 for the first time since 2015, underscoring how the market has unusually driven Microsoft’s valuation to near-market or even briefly below-market levels.

Although Wall Street remains optimistic that Microsoft will emerge as a long-term winner in the AI technology field, the company still needs to keep up with the unprecedented AI computing power spending arms race among hyperscale cloud vendors like Google and Amazon, a stance that may complicate any short-term sentiment reversal. According to compiled market consensus data, including leasing, Microsoft’s capital expenditures are expected to reach $146 billion in the fiscal year ending June 2026, a significant increase of about 66% from $88 billion in fiscal year 2025. This figure is projected to rise further to $170 billion in fiscal year 2027 and continue to grow to $191 billion in fiscal year 2028.

Investors are increasingly scrutinizing such large-scale expenditures, especially in the absence of a more pronounced acceleration in growth. In the most recent quarterly results, the growth rate of Microsoft's highly watched Azure cloud computing division even slightly decelerated compared to the previous quarter. Meanwhile, Microsoft’s Copilot AI application has gained limited traction among users, prompting the company to adjust its operational model for AI applications to enhance this AI software service.

Accumulating headwinds

Ben Reitzes, a senior analyst at Melius Research, rates the stock as “Hold.” He stated that all these combined issues reflect mounting headwinds for Microsoft. On March 23, he wrote in a note to clients: “Microsoft’s upside potential in operating its Azure cloud platform is very limited as it is preoccupied with repairing the growth momentum of its Copilot business and its own model ecosystem — a challenge that will not resolve itself within just one quarter.”

Of the 67 Wall Street analysts covering Microsoft, 63 have assigned a “Buy” rating, three a “Hold” rating, and one a “Sell” rating. The analysts’ average 12-month price target for the stock stands at $592, implying over 60% upside potential over the next year based on the average price target. According to compiled institutional data dating back to 2009, this represents the highest implied return on investment on record. The stock’s decline relative to its 200-day moving average is also the largest since 2009.

In Reitzes' view, the overwhelming “Buy” rating for the stock reflects severe complacency among his peers on Wall Street. He believes that Microsoft's Productivity and Business Processes segment, as well as its More Personal Computing division, also face additional growth risks.

On the other side is Tal Liani, an analyst from Bank of America, who has become increasingly bullish on Microsoft. Earlier this week, he resumed coverage of the stock with a “Buy” rating, citing Microsoft’s “durable multi-year growth potential” in cloud computing and AI as the core rationale.

These two contrasting market perspectives touch on the tension surrounding Microsoft’s stock. The long-term growth outlook is indeed promising, but there are very real execution risks between now and then. Whether these concerns are prescient or represent a significant buying opportunity depends on the observer’s judgment.

Jake Seltz, a senior portfolio manager at Allspring Global Investments, stated: “I believe this stock holds significant long-term investment value. Its AI strategy will ultimately prove to be correct, and I think it will largely remain insulated from the most severe fears of AI disruption. At the same time, these concerns are creating opportunities for long-term holdings, especially if you’re willing to exercise a bit more patience.”

Microsoft is currently experiencing what can be described as 'two squeezing forces' stemming from the AI technology on which it pins its growth hopes: on one side, defensive measures such as heavy capital investment, margin pressures, and a widespread hiring freeze; on the other, external upstarts and AI agent workflows challenging the medium- to long-term growth prospects and pricing power of Office, Copilot, and even Azure.

Thus, some Wall Street analysts view Microsoft’s current downturn not merely as a routine valuation correction, but as the market’s first systematic questioning: Will AI amplify Microsoft, or will it first weaken the company’s long-standing critical software business model? Microsoft’s stock is heading toward its worst quarterly performance since Q4 2008, signaling that Wall Street is repricing Microsoft from being “the first beneficiary under the AI wave” to “the most capital-intensive tech giant with still unproven returns on investment in AI.”

Editor/Doris