This article is from Chuanyue Global Macro, authored by Wu Shuo and Lin Yan.

In just a few weeks, the market's liquidity expectations for the remainder of the year have made a complete 180-degree turn. Under pressure from persistently heightened tensions in the Persian Gulf and elevated international oil prices, inflation risks have resurfaced. Major central banks generally held steady this month, with some even issuing hawkish signals, leading to a rapid reversal of previous easing expectations. Currently, the risk of a renewed global tightening cycle has significantly increased, intensifying pressures of liquidity tightening, causing most asset classes, except crude oil and the US dollar, to experience sharp corrections.

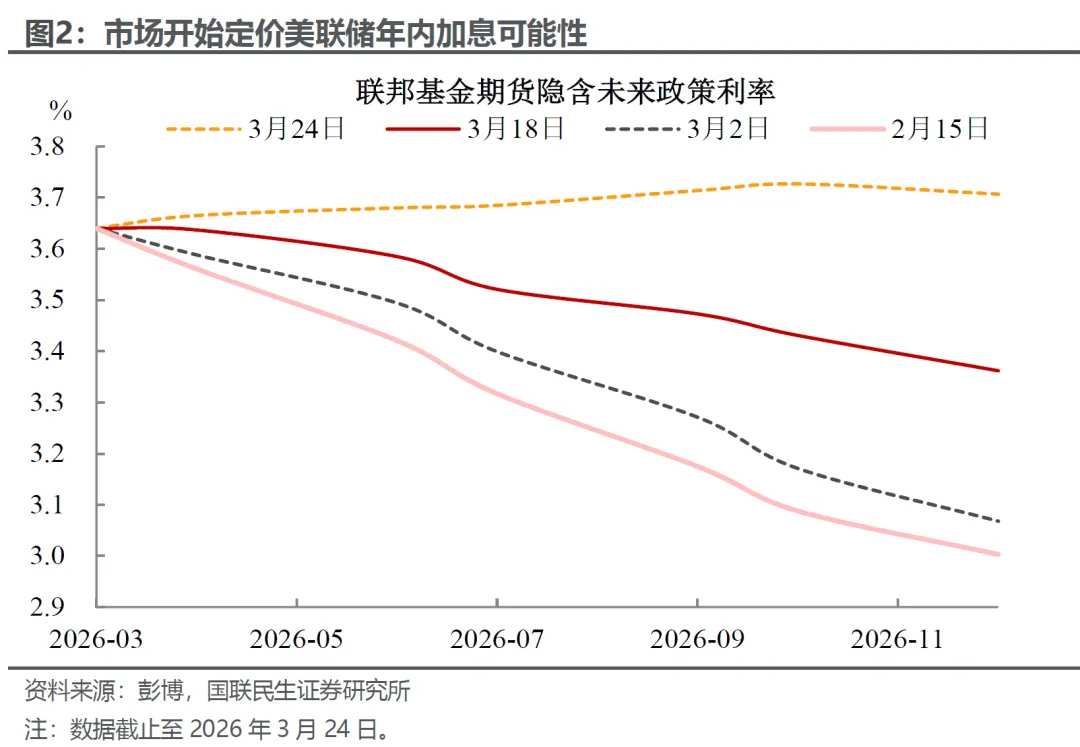

Similarly, the Federal Reserve is no exception. At the beginning of the year, the market widely expected about two rate cuts in the U.S. within the year; however, as concerns over inflation re-emerged, policy expectations have notably shifted, with markets even starting to price in the possibility of renewed rate hikes.

Nevertheless, market expectations often exhibit an inertia of linear extrapolation, leaving room for potential back-and-forth adjustments. As seen with the recent surge in rate hike expectations, any subsequent correction could trigger a strong countermovement in the market.

Nevertheless, market expectations often exhibit an inertia of linear extrapolation, leaving room for potential back-and-forth adjustments. As seen with the recent surge in rate hike expectations, any subsequent correction could trigger a strong countermovement in the market.

So, does the Fed have the possibility of raising rates again this year? We believe this probability is low. The threshold for the Fed to resume rate hikes is currently high, with multiple constraints making maintaining the current interest rate levels likely its policy baseline. Against the backdrop of economic weakness and impeded inflation transmission efficiency, continuing rate cuts within the year remain a plausible scenario. Specifically,

1. Learning from history: How did the Federal Reserve enter a rate hike cycle?

First, reviewing past rate hike cycles reveals that the Fed typically initiates rate hikes based on the following typical characteristics tied to its dual mandate of employment and inflation:

1) A sustained recovery in the job market, alongside tight labor supply and demand, often constitutes an important prerequisite for the Fed to commence rate hikes. In the rate hike cycles since 1970, the three-month average of new non-farm payrolls in the U.S. prior to rate hikes was mostly maintained around 200,000, with unemployment showing a general downward trend. Strong employment performance provided solid fundamental support for the Fed's monetary tightening.

2) Inflation levels are an important consideration for rate hikes, but inflation expectations are equally crucial, directly determining the urgency and intensity of the Fed’s tightening policies. Rate hikes do not always follow a significant rebound in inflation; after economic stabilization, even with mild short-term inflation, the Fed may still adopt preemptive rate hikes due to concerns over wage stickiness and future inflation rebounds, making future inflation expectations more critical. During periods of major supply shocks such as the oil crises in 1973 and 1977, and disruptions in global supply chains and energy in 2022, the Fed often demonstrated lagged responses, with the pace of interest rate increases frequently aligning or even lagging behind rising prices.

In contrast, the current macroeconomic environment differs markedly from historical rate hike cycles:

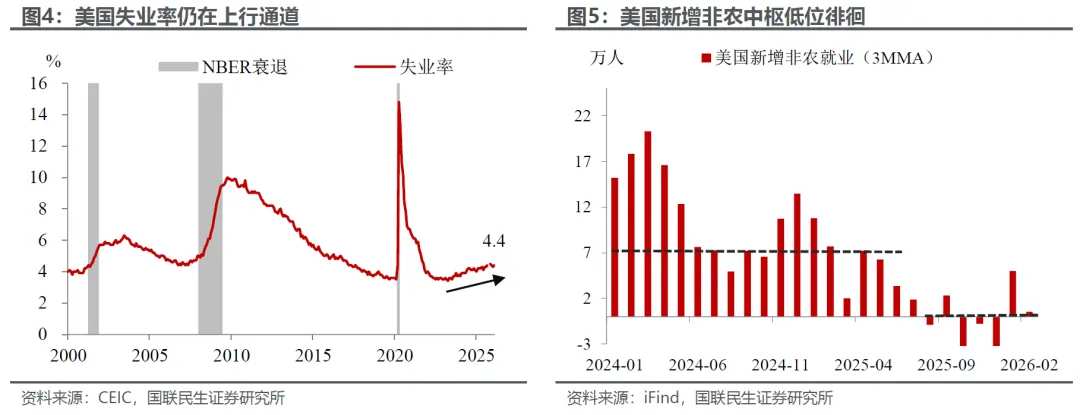

On the one hand, the US labor market has shown a sustained weakening trend, and the foundation for employment recovery remains unstable. At present, the center of new non-agricultural jobs in the US remains around zero, and the unemployment rate is also showing an upward trend. Against this backdrop, if the Federal Reserve prematurely initiates an interest rate hike, it would not only fail to provide policy support but could further impact the already fragile job market, exacerbating downward economic pressures.

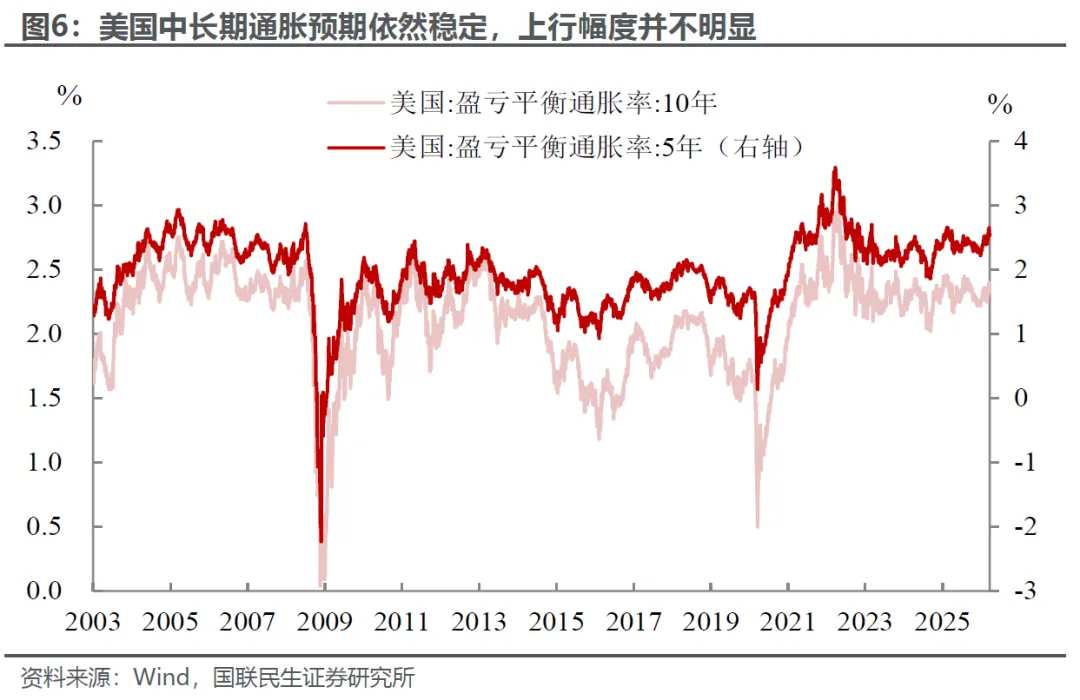

On the other hand, although there are short-term inflation concerns, inflation expectations remain relatively stable. We believe the core reason is that the recent rise in international oil prices lacks the critical foundation for sustained inflation transmission on both the supply and demand sides. Comparing the two major energy price shocks caused by the oil crisis in the 1970s and the Russia-Ukraine conflict in 2022, their ability to continuously spread to the inflation side essentially relied on the unique supply patterns and strong demand stimulus policies at those times. These key conditions are absent in the current environment.

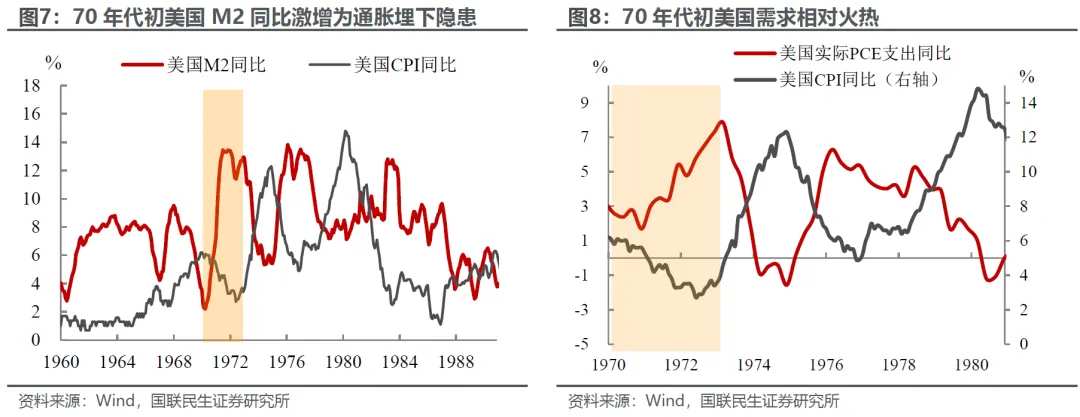

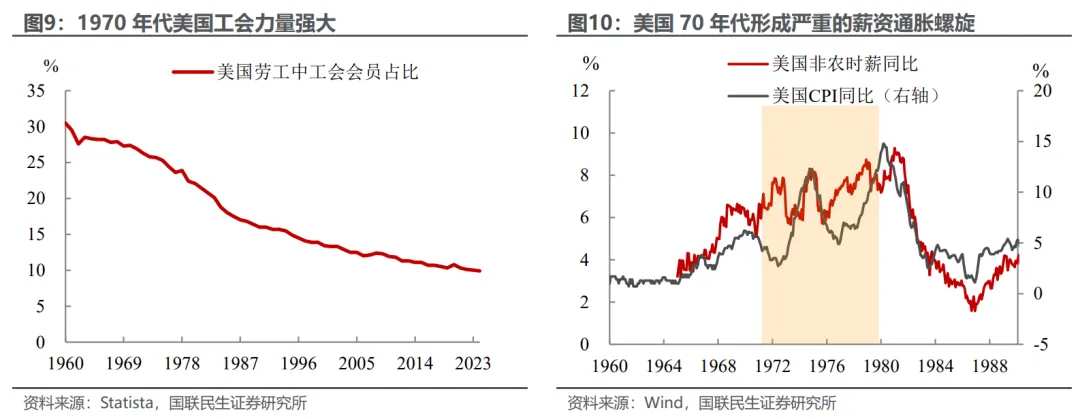

Specifically, the stagflation pattern in the US during the 1970s was due to supply shocks compounded by insufficient policy resolve, which eventually led to the de-anchoring of inflation expectations. In fact, even before the oil crisis, signs of inflation risks had emerged in the US under the long-standing Keynesian stimulus framework adopted after World War II. To sustain high economic growth and full employment, the government continuously implemented expansionary fiscal and monetary policies: on one hand, the 'Great Society' welfare program significantly expanded fiscal expenditures, causing the overall deficit rate in the US to rise in the late 1960s; on the other hand, the Federal Reserve maintained loose liquidity for an extended period, leading to excessive growth in the money supply, which pushed aggregate demand into overheating and consistently raised inflation expectations. The Federal Reserve failed to promptly tighten policies to curb this, and its subsequent anti-inflation efforts lacked sufficient resolve.

Ultimately, under a series of supply shocks in the 1970s, inflation expectations became completely de-anchored. After the Middle East War triggered OPEC's oil embargo, severe shortages of international crude oil occurred. As the US was highly dependent on overseas supplies as a net importer with weak energy self-sufficiency, rising oil prices directly increased production costs across all industries in the US. Companies were forced to raise prices, becoming the core trigger for widespread inflation. Additionally, the strong influence of US labor unions at the time, where wages were prone to rise but resistant to fall, further increased corporate costs and drove prices higher, forming an inflationary spiral.

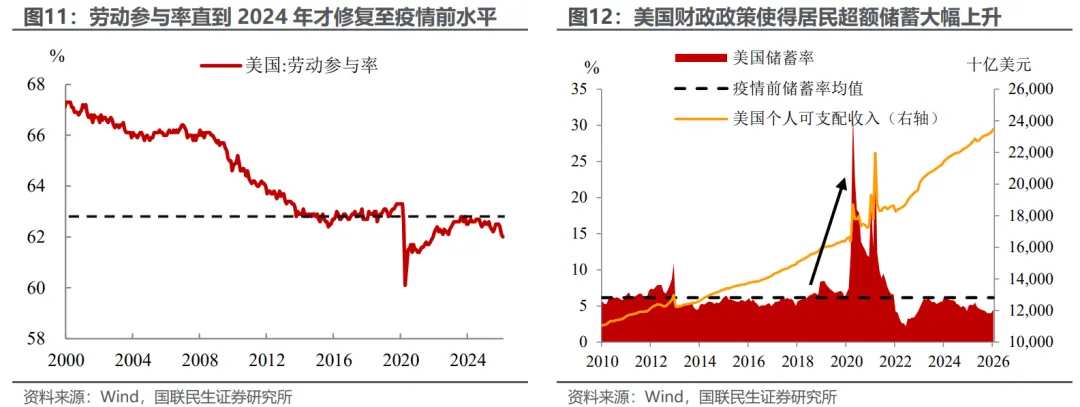

In contrast, the high inflation in the US in 2022 was largely the result of post-pandemic overheated demand and a tight labor market. Of course, the Russia-Ukraine conflict disrupted global energy supplies, serving as a significant external catalyst for the inflation surge; however, the more fundamental driving factor was the unprecedented scale of fiscal and monetary stimulus policies implemented during the pandemic, which provided demand-side support for cost pressures to be continuously transmitted downstream. The concentrated release of excess household savings fueled a temporary overheating of consumer demand, while tight labor market conditions (caused by a sharp decline in labor participation rates due to the pandemic) led to elevated wage growth. Cost pressures rapidly spread across goods, services, and rental housing sectors, ultimately triggering broad-based high inflation unseen in nearly four decades.

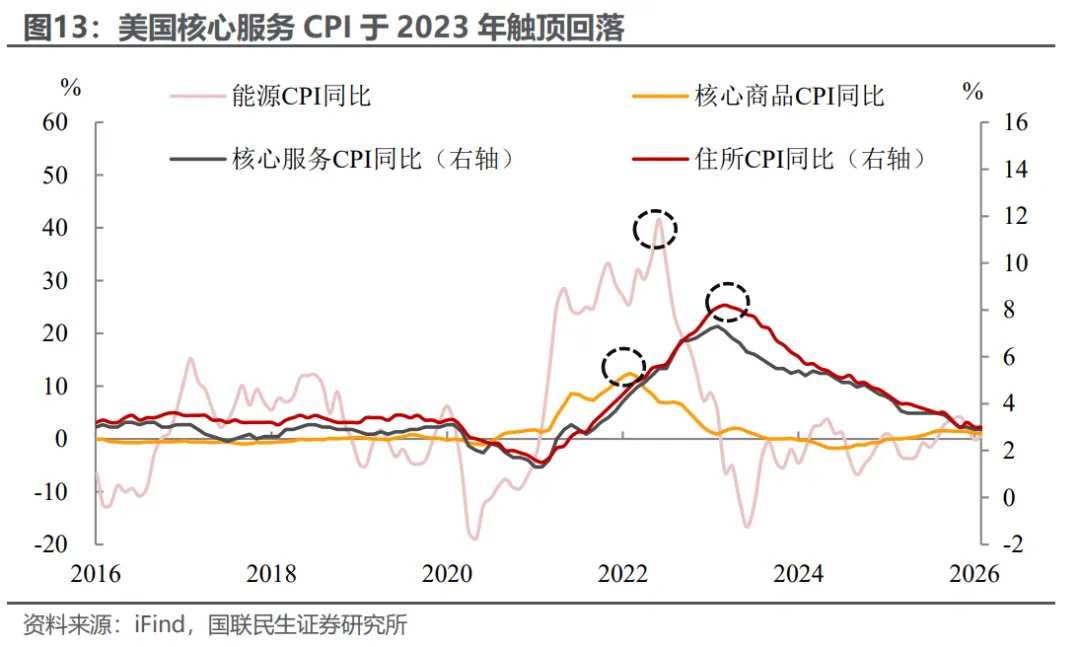

The trajectory of inflation components also confirms that US energy inflation peaked and quickly retreated in 2022, leading to a weakening in commodity prices. However, core CPI components such as housing did not enter a downward channel until mid-2023. The overheating of service demand driven by fiscal stimulus was a key reason for the persistence of this inflation cycle.

At present, both the shock resistance on the supply side and the transmission momentum on the demand side differ fundamentally from the previous two cycles:

On the supply side, the shift in the US's role within the global energy supply landscape has fundamentally reduced the extent to which rising oil prices can transmit to broader inflation. On one hand, the shale oil revolution increased US crude oil self-sufficiency and turned the country into a net exporter, significantly enhancing its resilience to geopolitical supply disruptions, making it difficult to form sustained energy gaps. Simultaneously, crude oil export revenues help offset rising corporate costs, to some extent suppressing price increase momentum. On the other hand, the rapid promotion of renewable energy and continuous improvements in industrial efficiency have decreased the overall dependence of the US economy on crude oil, reducing the weight of the energy component in the CPI basket and moderating its impact on overall inflation.

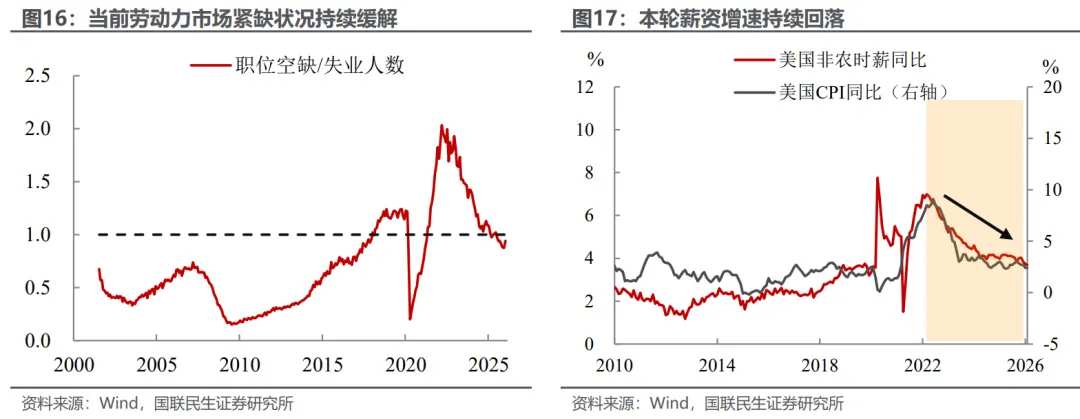

Additionally, the absence of a wage-inflation spiral mechanism has become a crucial factor in curbing the sustained diffusion of inflation on the cost side. The continued cooling of the US labor market, coupled with a gradual reduction in job vacancies and declining union power and wage stickiness, has prevented a significant positive feedback loop between wages and inflation, effectively blocking the possibility of spiraling cost pressures pushing up prices across the board.

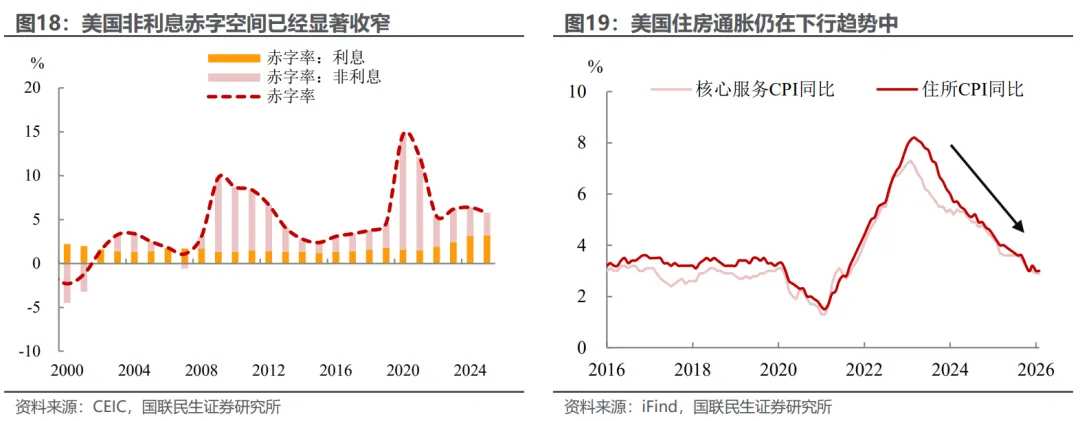

On the demand side, the weak economic outlook makes it difficult to smoothly pass on the pressure of rising oil prices downstream. Although the Federal Reserve has initiated a rate-cutting cycle, the policy rate remains significantly above the neutral level, maintaining a generally tight monetary environment that continues to suppress durable goods consumption, investment, and the real estate market. Meanwhile, the high level of US government debt and limited fiscal space have led to a gradual withdrawal of large-scale demand stimulus policies, significantly weakening fiscal support for aggregate demand.

Amid the K-shaped economic divergence in the United States, the current rise in oil prices lacks broad-based demand support, making it difficult for inflationary pressures to spread from the energy sector into a comprehensive and sustained increase in overall prices. Particularly under high interest rates, core inflation components such as housing remain on a downward trajectory, further weakening upward momentum in overall inflation. This also provides critical demand-side support for keeping inflation expectations stable.

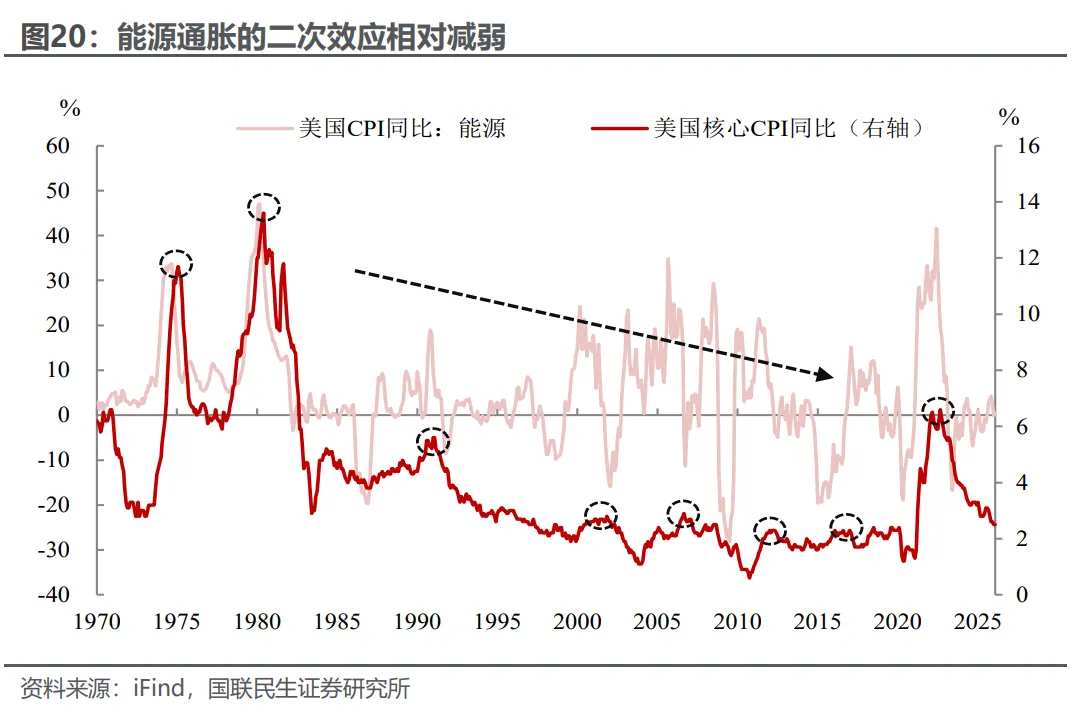

A review of historical patterns reveals that, since the Great Stagflation of the 1970s, the secondary pull effect of oil price fluctuations on core inflation has significantly diminished. This is due to factors such as the transition in energy structures, stronger Federal Reserve discipline, and greater flexibility in labor market adjustments. Especially in the absence of robust demand-side support, oil price shocks are even less likely to generate sustained inflationary transmission momentum.

Therefore, when faced with such supply shocks, the traditional policy logic of the Federal Reserve is typically to disregard temporary inflation spikes in the short term, waiting until inflation transmission becomes more evident, core inflation steadily recovers, or inflation expectations show clear signs of rising—indicating a pronounced 'second-round inflation' effect—before considering rate hikes. The core consideration here is the uncertain sustainability of short-term supply-side transmission and the fact that economic slowdowns often offset inflationary pressures to some extent.

Certainly, this time is no exception. Whether considering the weak performance of the labor market mentioned earlier or the efficiency of inflation transmission, the United States does not meet the conditions for raising interest rates this year. Moreover, significant uncertainties persist in the short-term geopolitical situation in the Middle East, making the sustainability and trajectory of rising international oil prices unclear. Coupled with Trump's fluctuating policy stance, if the Federal Reserve were to raise rates prematurely, any subsequent decline in oil prices could lead to frequent adjustments in Fed policy, exacerbating market expectation disorder and triggering substantial financial market volatility, which would ultimately be detrimental to economic stability.

2. The Cost of Raising Rates? From 'Stagflation' to 'Recession' Trading

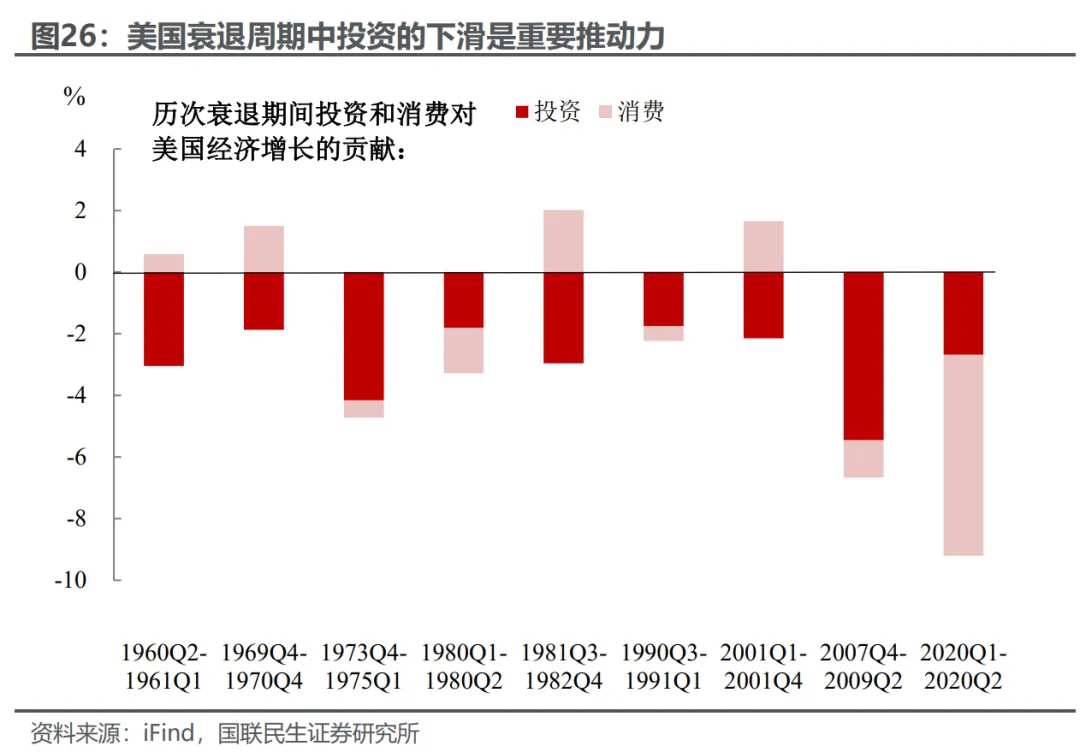

In addition to the stringent conditions for raising rates, the cost of doing so is something the U.S. economy and the Trump administration cannot easily bear. Against the backdrop of an increasingly fragile U.S. economy and financial markets (except for AI), a hasty rate hike could cause significant negative impacts on the economy. The sustainability of the current market pricing for 'stagflation' trading may be weak, with a non-negligible likelihood of eventually evolving into 'recession' trading.

As we previously noted, the core issue facing the U.S. economy today is the 'K-shaped' divergence, a fundamental problem that Trump must address during this midterm election year. On one hand, he needs to sustain the role of AI investment in supporting the economy and the boost that rising stock markets provide to consumption; on the other hand, he must maintain fiscal expansion to 'secure livelihoods.' However, once interest rates rise, the adverse impacts on both objectives will be obvious:

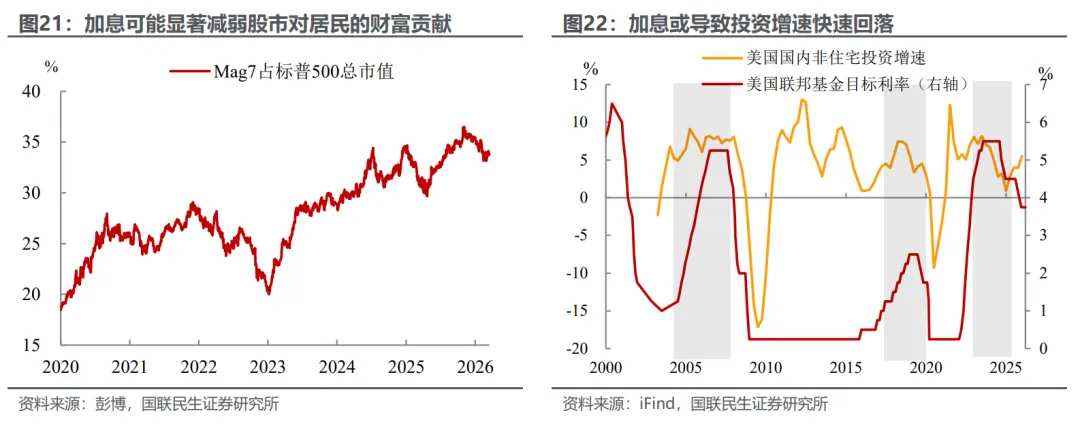

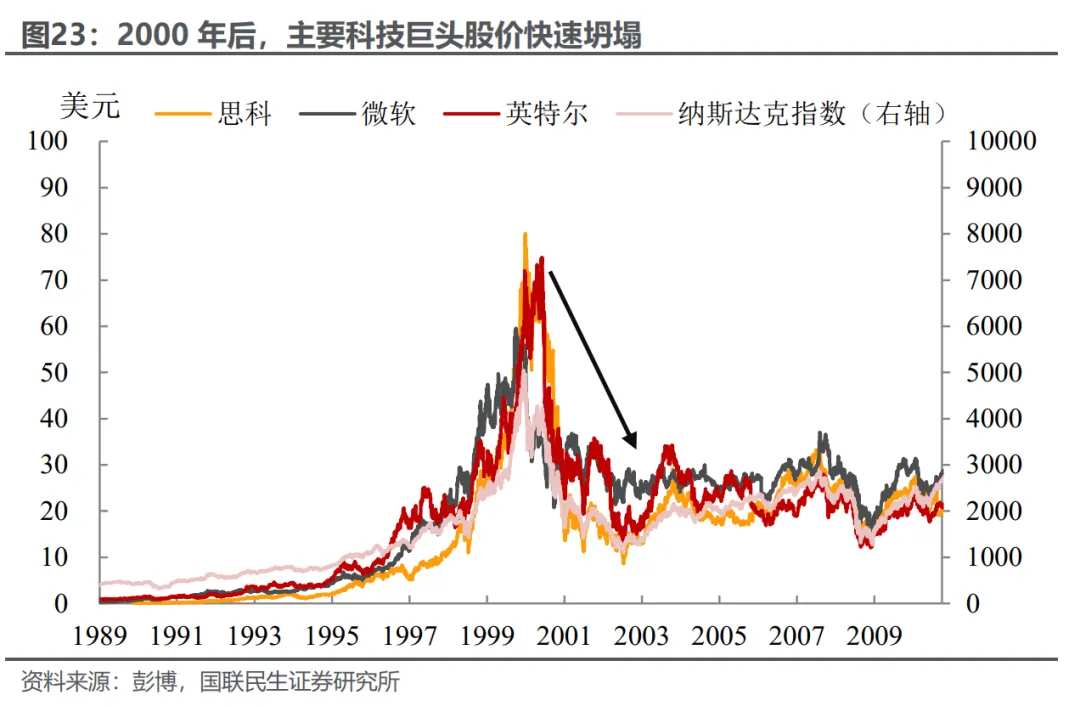

First, looking at AI investment, although the AI industry is still in a phase of deepening implementation and may not yet have reached the level of forming asset bubbles, concerns over high valuations and overly rapid increases have arisen multiple times in the market. The overall fragility of tech stocks has risen significantly, making them extremely sensitive to changes in policy and liquidity. Any minor fluctuations can easily trigger sharp volatility. Once a rate hike is implemented, it could lead to ongoing negative expectations in the market, resulting in a rapid decline in risk appetite. This would not only prompt a correction in tech stock valuations (with MAG7 accounting for over 30% of total market capitalization) and directly reduce the wealth effect on households but might also cool down investment and financing in the AI sector, leading to a contraction in capital expenditures. $S&P 500 Index (.SPX.US)$ This logic is not an isolated case. Historical lessons from the dot-com bubble in 2000 are highly instructive: during periods of tightening liquidity and rising interest rates, high-valuation growth sectors are often hit first. Valuation expansions driven by capital inflows become unsustainable, and if profit realization falls short of expectations, it can easily trigger a 'double whammy' of valuation and earnings declines, leading to simultaneous cooling in capital markets and industrial investment. In 2000, as the Federal Reserve raised rates consecutively, valuations of tech giants like Cisco, Microsoft, and Intel collapsed rapidly, and their stock prices plummeted. The market quickly revised its growth narrative for the new economy, causing a significant contraction in capital expenditures. Declining risk appetite and slowing industrial investment reinforced each other, creating a strong negative feedback loop.

This logic is not unique. The historical experience of the dot-com bubble in 2000 serves as a stark warning: during periods of tightened liquidity and rising interest rates, high-valuation growth sectors are often the first to be impacted. The previous valuation expansion driven by capital inflows becomes unsustainable, and if profit realization fails to meet expectations, it can easily trigger a 'double whammy' of declining valuations and earnings—a phenomenon known as the 'Davis Double Kill.' This results in simultaneous cooling in capital markets and industrial investments. In 2000, as the Federal Reserve continued to raise interest rates, the valuations of tech leaders like Cisco, Microsoft, and Intel collapsed rapidly, leading to significant declines in stock prices. The market swiftly adjusted its growth narrative for the new economy, causing a marked reduction in capital expenditures. Declining risk appetite and slowing industrial investment mutually reinforced each other, creating a significant negative feedback loop.

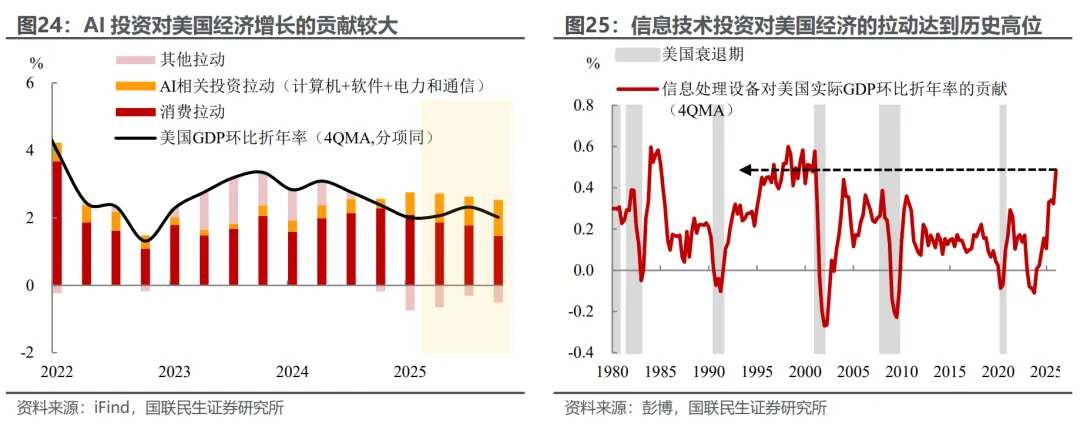

Similarly, the current investment in AI is crucial for the growth of the U.S. economy, becoming an indispensable component. By Q4 2025, AI-related investments in the U.S. contributed 1.07% (4QMA) to the annualized quarter-on-quarter economic growth, accounting for approximately half of the total growth. If rising interest rates trigger a rapid contraction in corporate investment, it could significantly amplify downward economic pressure, serving as a key driver pushing the economy toward recession.

Secondly, the 'double squeeze' effect of rate hikes and rising oil prices will significantly exacerbate living costs and debt repayment pressures for middle- and low-income groups, potentially leading to deeper livelihood challenges. In fact, the economic situation of middle- and low-income groups in the U.S. is already more fragile, as we have previously revealed that these groups are clearly lagging behind in economic growth, with livelihood pressures becoming a core pain point for the U.S. economy.

Against this backdrop, if rising oil prices and the rate hike cycle resonate, it would undoubtedly be 'adding insult to injury.' Rising oil prices directly increase basic living expenses such as transportation and heating, eroding already diminished disposable income; meanwhile, rate hikes mean increased interest payments on mortgages, credit card debt, and further squeezing household financial flexibility. The combination of these factors could not only force middle- and low-income families to cut necessary consumption and delay large expenditures but may even push them to the brink of debt default, posing a substantive threat to their quality of life and balance sheets, which would be highly unfavorable for Trump in handling midterm elections.

According to estimates by the Dallas Federal Reserve, the closure of the Strait of Hormuz would cause a significant impact on the economy in Q2 2026, with a single-quarter drag potentially reaching 2.9 percentage points. Although short-term resumption of shipping may allow for economic activity recovery, substantial supply chain shocks have already taken place, and the decline in global supply chain efficiency along with subsequent inventory disruptions will inevitably weigh on the magnitude and timing of economic recovery. At this juncture, if compounded by the effects of rate hikes, the resonance of supply shocks and tightening financial conditions might plunge the U.S. economy into a severe slowdown.

Therefore, whether due to downward economic pressure or political considerations by Trump, the cost and resistance faced by this administration from rate hikes are undoubtedly enormous.

3. Potential 'roadmap' for restarting rate hikes within the year?

So, what conditions might trigger a Fed rate hike this year? We believe that for the Fed to restart rate hikes this year, it would likely require a convergence of factors from inflation origins, demand transmission mechanisms, and policy constraints:

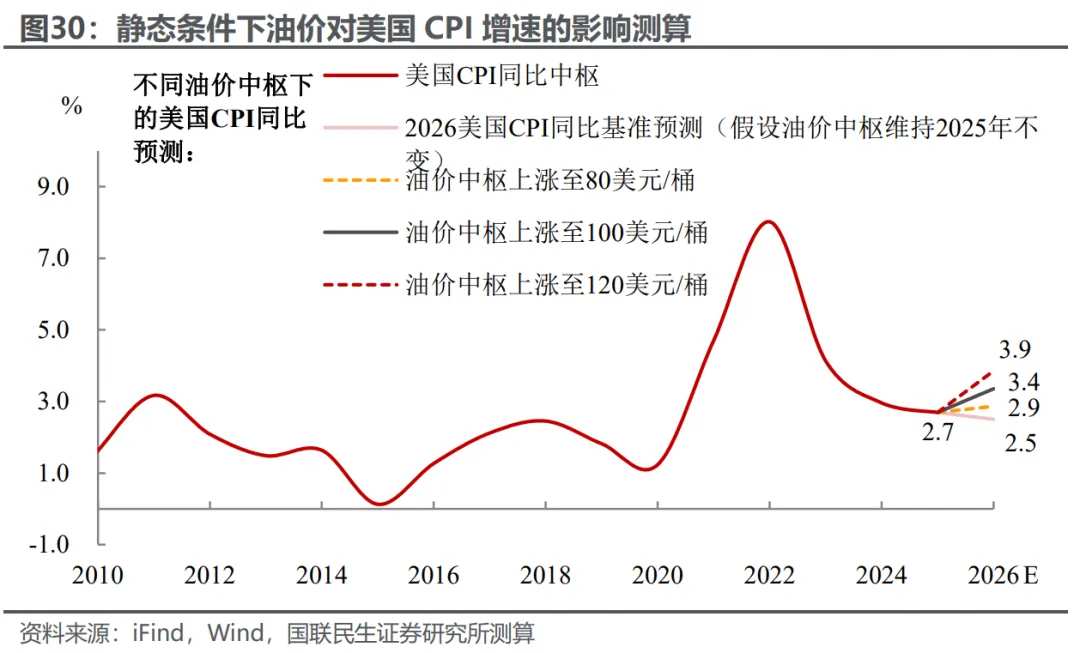

In terms of inflation sources, a prolonged stalemate in the Middle East situation could keep oil prices at $100-120 per barrel or even higher throughout the year. According to our previous calculations under a static model, U.S. inflation will rebound to above 3.5% this year. More importantly, if geopolitical conflicts continue to escalate and supply disruptions remain unresolved, persistently rising energy prices will ignite medium- to long-term inflation expectations, which is more critical for the Fed's policy pivot than a mere rebound in inflation readings.

In terms of transmission mechanisms, Trump may need to implement more aggressive fiscal expansion policies to unclog demand bottlenecks. In the midterm election year, if Trump follows the example set during Biden’s tenure by launching large-scale fiscal stimulus—through direct resident subsidies, tax cuts, and previously promised affordability support policies—it could quickly boost disposable income and activate end-user demand. This might complete the chain of oil price transmission to downstream investment and consumption, potentially becoming the biggest risk source for secondary inflation within the year.

In terms of policy constraints, whether Kevin Warsh can uphold policy independence is another critical condition that cannot be ignored. Compared to Powell, Warsh currently holds a notably dovish stance, publicly expressing intentions during his campaign to lower interest rates to around 3%, showcasing relatively weaker resolve in combating inflation. Under White House pressure, the likelihood of him shifting to a tightening stance is debatable. Additionally, the leadership transition process at the Fed itself poses potential risks. If Warsh fails to secure Senate confirmation, Powell will continue presiding over decisions as acting chair, potentially increasing the probability of restarting rate hikes within the year.

Therefore, based on the above three key conditions, we believe that the important indicators to watch for within the year include: marginal changes in inflation expectations (the sustainability of oil prices), the pace and effectiveness of fiscal policy implementation, and Wash’s subsequent policy statements and decision-making tendencies. These variables will collectively influence whether the Federal Reserve pivots its policy this year, as well as the timing and magnitude of such a pivot.

However, at least for now, considering the difficulty in achieving the aforementioned conditions, the hurdle for the Federal Reserve to raise interest rates within the year remains high.

Risk warnings: Unexpected stickiness in U.S. inflation and tariff pass-through; escalation of geopolitical conflicts and significant increases in oil prices; unexpected shifts in U.S. fiscal policy; potential discrepancies in data calculations.

Editor/KOKO