Jeffrey Gundlach, founder and CEO of DoubleLine Capital and known as the "New Bond King," issued a stern warning in a recent in-depth interview: the 40-year cycle of declining interest rates in the United States has come to an end. Massive debt is pushing the economy to an unsustainable brink, while the overheated private credit market is brewing a major liquidity crisis akin to the subprime mortgage crisis of 2006.

On March 27, during an in-depth dialogue hosted by renowned financial presenter Julia, Jeffrey Gundlach, founder and CEO of DoubleLine Capital, delivered impactful insights on global macroeconomic trends, the Federal Reserve's monetary policy path, private credit risks, and future asset allocation strategies.

As one of the most influential fixed-income investors on Wall Street, Gundlach explicitly stated during hours of discussion that risks in the current financial environment are clearly accumulating. He not only overturned market consensus expectations of an "imminent rate cut" by the Federal Reserve but also proposed an extreme scenario where U.S. Treasury bonds could face "restructuring" or "soft default" in the future.

"Because of the debt burden we carry and the way we are financing the government with a $2 trillion deficit, this is entirely unsustainable. If something is unsustainable, it has to stop." Gundlach set an extremely cautious tone from the outset.

"Because of the debt burden we carry and the way we are financing the government with a $2 trillion deficit, this is entirely unsustainable. If something is unsustainable, it has to stop." Gundlach set an extremely cautious tone from the outset.

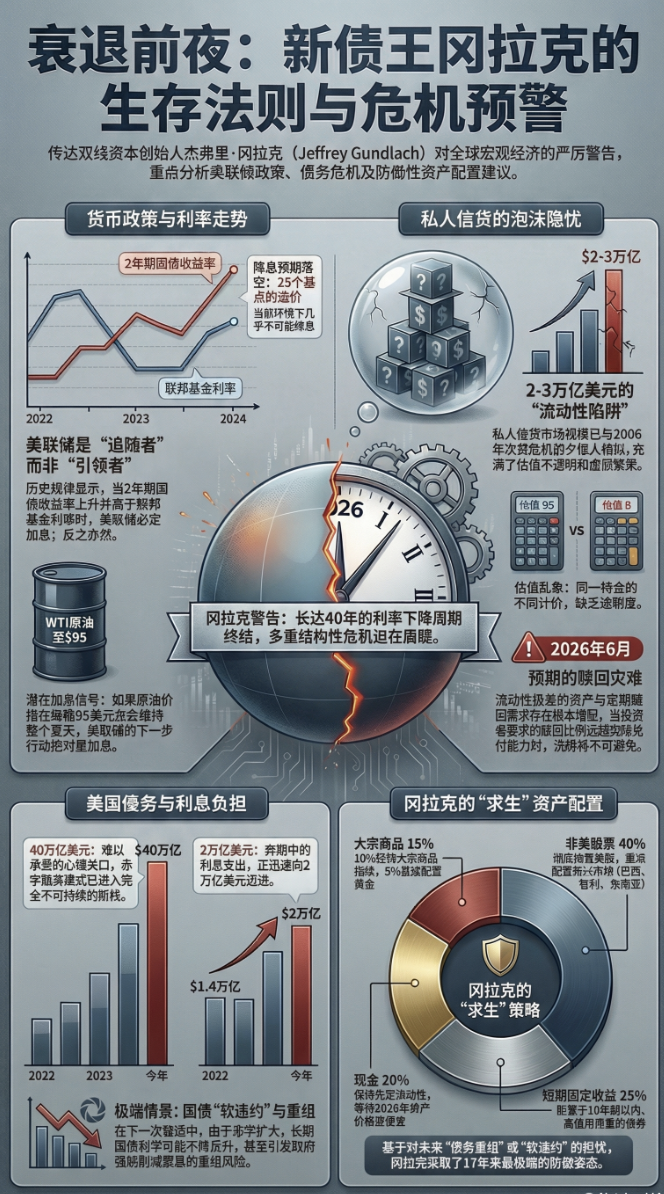

The Federal Reserve has no secrets; its next move will not be a rate cut but rather a "rate hike."

Regarding the current market's fervent expectation of rate cuts by the Federal Reserve within the year, Gundlach threw cold water on the notion. He bluntly pointed out that the Federal Reserve has never been a leader in interest rates but rather a follower.

"I think we should abolish the Federal Reserve and directly use the two-year Treasury yield as the short-term interest rate." Gundlach sharply noted that if one compares the federal funds rate with the two-year Treasury yield over the past 30 years, the pattern is obvious: when the two-year Treasury yield rises above the federal funds rate, the Fed inevitably raises rates; conversely, the same holds true.

He elaborated on recent market dynamics:

"Just before the Federal Reserve announced it would keep rates unchanged, everyone was saying, 'The Fed will cut rates twice this year.' I said, no, they won't. The two-year Treasury yield is higher than the federal funds rate. With the federal funds rate at its current level and the two-year Treasury yield more than 25 basis points above the upper limit of the federal funds rate, you cannot expect to see a decline in the federal funds rate."

Gundlach predicted that if crude oil prices remain high (for example, WTI crude at around $95 per barrel throughout the summer), "the Federal Reserve will absolutely raise rates. You'll hear more and more about this starting now. Perhaps the Fed's next move will be a rate hike."

Private Credit: A 'Thoroughly Disastrous' Replay of the 2006 Subprime Crisis

When discussing private credit, currently the hottest asset class on Wall Street, Gundlach used the harshest language in the room, directly comparing it to the subprime market that triggered the 2008 global financial crisis.

"Last year, I told people I felt like I was in 2006, surrounded by all kinds of bubbles." Gundlach stated that the current private credit market, valued at two to three trillion dollars, bears an uncanny resemblance to the size of the subprime market just before the onset of the global financial crisis in 2006.

He completely exposed the facade of private credit as a "low volatility, high return" investment, pointing out that its valuation is entirely an opaque false prosperity. He shared a shocking industry insider perspective:

"There is a major insurance company client who has eight managers holding identical positions. The same holdings, one valued at 95 and another at 8."

Gundlach pointed out that the essence of private credit lies in packaging highly illiquid assets for investors who require periodic redemptions, a fundamental mismatch that is bound to collapse. He warned:

"When you request a 14% redemption and they only give you 5%, what you will do next is demand a 40% redemption. By June 2026, you will see some rather wild redemption requests. Private credit must undergo a significant reshuffle."

Capital Preservation First: Selling U.S. Assets, Focusing on Emerging Markets and Gold

Based on concerns about rising long-term interest rates and a potential credit crunch, DoubleLine Capital’s current risk exposure has dropped to its lowest level in 17 years since its inception. Gundlach made it clear that times have changed, stating, "We have left the world of ambition and hype," with capital preservation now being the top priority.

Faced with the S&P 500 index trading at more than twice the price-to-book ratio of the rest of the world, Gundlach provided a highly disruptive contrarian asset allocation recommendation: completely divest from U.S. stocks.

40% allocated to non-US equities: "I have been advising US investors that their equity allocation should be 100% in non-US stocks, particularly emerging market stocks denominated in local currencies. For instance, Brazil, Chile, and Southeast Asia."

25% allocated to short-term fixed income: Entirely invested in bonds with maturities of less than ten years and higher credit quality.

15% allocated to commodities: Of which 10% is linked to the Bloomberg Commodity Index and 5% directly allocated to gold.

20% held in cash: Waiting for asset prices to become cheaper by 2026 before taking action.

Regarding gold, Gundlach is extremely optimistic:

"Gold is real money. Central banks will remain a significant source of ongoing demand for gold... Gold is no longer just for survivalists or eccentric speculators. It is a genuine asset class."

Endgame Scenario: $40 Trillion Debt Burden Pressures U.S. Treasury Bonds, Potentially Facing 'Direct Interest Rate Cut' Restructuring

Concerning the deepest worries about the macro environment, Gundlach attributes them to the growing debt black hole in the United States. The current U.S. national debt has reached $39 trillion, and Gundlach believes that "when it reaches $40 trillion, it may become a psychological threshold."

He challenges the long-standing market assumption—that economic recessions lead to lower interest rates. Gundlach warns that during the next recession, due to the sharp expansion of deficits, long-term government bond yields will not decline but instead rise. Currently, the annual interest payments by the U.S. Treasury have already reached $1.4 trillion, “heading toward $2 trillion in interest expenses.”

When asked about the likelihood of a recession, he noted:

I certainly think there is a high probability that those in power will announce the onset of a recession at some point in 2026. I would assign it at least a 50% likelihood.

If long-term interest rates rise to around 6%, interest expenditures will spiral out of control. Gundlach outlined two ultimate approaches to resolving this crisis: inflationary devaluation or soft default (debt restructuring).

More shockingly, he believes the possibility of the U.S. government mandatorily revising treasury bond rules to directly lower coupon rates is far higher than market expectations.

I believe investors need to consider the idea that the creditworthiness of U.S. Treasuries might come into question. People don't like hearing this. They think it's too radical an idea.

To avoid this 'interest rate cut' restructuring risk, Gundlach's team has implemented extreme defensive measures: shorting all long-term treasuries and converting all mandatory holdings into bonds with the lowest possible coupons (e.g., 1.5%) within the same maturity period, to prevent principal from plummeting due to forced government reductions of high-coupon bonds (e.g., 6%).

At the end of the interview, Gundlach predicted that a 'restructuring' or large-scale 'reset' (i.e., the Fourth Turning) of the American system will occur around 2030. Until then, his strategy consists of just four words: 'Wait for the perfect opportunity.'

The full transcript of the interview is as follows:

Jeffrey Gundlach

Because of the debt burden we carry and our current method of financing the government through a $2 trillion deficit, which is entirely unsustainable, change is necessary. If something is unsustainable, it must come to an end. This situation must stop. And politicians, of course, have shown no willingness to rein in spending. Therefore, the market will ultimately have to enforce discipline. So, risks are clearly accumulating in the current environment, and I am very interested in adopting a low-risk strategy for the coming months and quarters.Julia

Founder and CEO of DoubleLine Capital, Jeffrey Gundlach. We are deeply honored to have you on our program today. Thank you very much for taking the time to speak with me.Jeffrey Gundlach

Thank you for having me, Julia. It's been a while since we last spoke.Julia

Indeed, it has been a long time. It’s been five years since our last conversation. You are one of my favorite people to talk to in the investment world. Again, it is an honor to have you here, Jeffrey. A lot has happened so far this year. I can hardly believe we’re about to close out the first quarter. I’ve been telling my guests that so much has happened, and there have been so many changes. And indeed, there have been. Since it’s been a while since your last appearance on the show, let’s start with the big picture. Talk to us about your framework for viewing the world today, your assessment of the economy and markets, and what you’re focusing on. Jeffrey, one of the hallmarks of this program is that when explaining the big picture, you have free rein to go as long as you’d like.Jeffrey Gundlach

Alright. Well, the economy seems to be slowing down. Interestingly, bond yields are rising, and Treasury yields are climbing. One core idea I’ve been developing, especially over the past five years or so, is that we are no longer in a long-term declining interest rate environment, particularly for long-term rates. I came to this conclusion around four or five years ago. At that time, I faced significant opposition. Many believed that rates would remain low for generational reasons. However, I think there are long cycles in interest rates, typically lasting about 40 years. Rates bottomed out around 1945 and then began rising in the 1950s, continuing to climb until, I would say, 1984. After that, rates started declining, and that trend persisted until around 2000. I’ve always believed that the long-term decline in long-term rates must have ended due to Treasury interest payments. The interest burden has skyrocketed due to the persistent $2 trillion annual budget deficits, compounded by higher rates. You know, the Federal Reserve raised short-term rates from zero to 5.375%, which caused a substantial increase in interest costs. As a result, the U.S. Treasury now pays about $300 billion annually in interest, whereas now it’s closer to $1.4 trillion, with seemingly no end in sight.Jeffrey Gundlach

Deficit spending. So, we continue to add about $2 trillion in debt annually, and the average interest rate on Treasury bonds maturing now is around 3.8%. Therefore, given that the current two-year Treasury yield is approximately 4% and the 30-year Treasury yield is nearing 5%, if we maintain the status quo, those maturing bonds will be replaced by new bonds issued at higher rates.Jeffrey Gundlach

I find it very interesting to look back at the 'taper tantrum' and the 'tariff tantrum' that occurred about a year ago. Interestingly, during the 'tariff tantrum,' the S&P 500 fell by 18%. If you review the past few decades of the S&P 500’s 13 corrections or bear markets, in each of the first 12 instances, the dollar rose by about 8% to 10%. What I found particularly thought-provoking was that last year, when the stock market dropped by 18%, the dollar actually fell. This confirms my belief that when markets are weak or the economy is soft, interest rates do not decline.Jeffrey Gundlach

What is truly interesting now is that it is difficult for people to discern the real reasons behind the rise in interest rates. Everyone tends to blame oil prices, and certainly, there is some truth to that. But it's a pattern. Many patterns are being broken. In the past, when Treasury yields rose, spreads on credit products typically narrowed. However, in March this year, it was one of the worst months in a long time. I mean, the two-year Treasury yield increased by 60 basis points this month, yet the spreads on credit products widened instead of narrowing. So we are beginning to see financial conditions genuinely tighten. Therefore, I have consistently believed that we are heading into an environment that will be highly unfavorable for financial assets. I sometimes listen to replays of your Saturday morning show, I believe it’s with Chris Whalen. I think I started tuning in. Perhaps it’s just confirmation bias because I agree with much of what he says. But last year, I told people that I felt like I was living in 2006, with all the bubbles, and all that—digital technology driven by artificial intelligence, and the narrowness of the market. Last year, making money was incredibly easy. I mean, even bonds—investment-grade bonds—rose by about 8%, while the S&P 500 Index climbed around 17% or 18%. European stocks performed stronger, and emerging market stocks showed the strongest performance.Jeffrey Gundlach

But this year is a year of caution and reflection. I noticed that although gold rose by about 70% over the entire year last year, Bitcoin actually fell. The conclusion I drew from this is that we have left the world full of aspirations. We have exited the world of hype where everyone thought 'you only live once' and similar notions. We are entering a realistic world because of Bitcoin. It feels like something from three or four years ago, and I think one of the biggest insults to it is that millennials would tell baby boomers that now only baby boomers care about Bitcoin, as it has ceased to be cool. So we are entering a world composed of tangible and real things, leaving behind the world of hype. I believe this will become a theme. I was reading financial news today, and as we approach the end of March, they mentioned that this has been the worst quarter for the stock market since 2022. That’s quite a long time. I mean, the stock market has fallen significantly. Some indices might have dropped by 2% or 3%, and others perhaps by 3% or 4%. But this implies that we haven’t experienced a single quarter where the stock market declined by 5% in the past four years, which seems overdue. Entering 2026, the valuation of the stock market reminds me of the situation at the end of 2021, which led to a terrible year that followed.Jeffrey Gundlach

In 2022, so I believe we are in a world where capital preservation takes precedence. At DoubleLine Capital, we have continuously reduced risk for over two years, particularly in terms of credit risk, and have been upgrading the quality of our investments. In fact, within funds that can invest in BBB-rated corporate bonds, our current holdings are at the lowest level in the history of DoubleLine Capital, which has been established for nearly 17 years. We are not very optimistic about the outlook for financial assets because I believe that even if we fall into a recession, long-term Treasury rates will rise rather than decline, breaking the pattern of the first 40 years of my career. I think this is what is going to happen. Therefore, we will face an environment where there is growing concern about interest expenses and, fundamentally, the interest costs associated with massive debt burdens.Jeffrey Gundlach

I hear a lot of people saying that if national gasoline prices exceed $4 per gallon, it will have a psychological impact on the economy. I think there might be some truth to that. This morning here in California, our gas prices are among the highest. Hawaii may be higher, but our prices are quite high—I currently spend six dollars and seventy cents to fill up my tank. That’s really…Julia

Regular gasoline?Jeffrey Gundlach

Yes, it's just regular gasoline. So the price is already high. But I also think these psychological thresholds are important. Most people don't realize that national debt has surpassed $39 trillion. I have a feeling that when it hits $40 trillion, it may become a psychological threshold where people start thinking, you know, by 2030 or 2031, it could reach $50 trillion.Jeffrey Gundlach

This is a very big issue. I think much of what investors believe they know has been shaped by falling interest rates and the experience of always being able to refinance their way through cycles, but that era is over. So, what happens when the yield on the 30-year Treasury bond actually starts rising in a weak economy? Think about it. If the economy is weak and bond yields rise, think about what that means. It means interest expenses grow faster. Of course, when the economy is weak, budget deficits expand, taking up a significant portion of GDP. In the past, during recessions, budget deficits typically expanded by 4% of GDP. Of course, the last two recessions were very severe. You know, there was the global financial crisis, and then there were pandemic lockdowns, where budget deficits expanded by 8% and 12% of GDP respectively. So if this really happens, one message I’ve been telling forward-thinking investors is that we might see some fairly aggressive measures needing to be taken to address this interest expense problem. One idea was proposed in a white paper at the end of 2024. Then Scott Bessent, who wasn’t yet the Treasury Secretary at the time, commented that perhaps we should restructure U.S. Treasuries held by foreign investors. What he meant was extending maturities and lowering coupons. It was interesting that he said this because it’s an idea I’ve been contemplating, and I think it’s more likely than most people are willing to believe. Perhaps one way to handle this issue is not only to do this for foreign investors but potentially for all Treasuries. So you go ahead and say, I know we’re going to directly lower the coupon on Treasuries so we can reduce interest expenses. Think about it: the average coupon on Treasuries is about 3.8%. If you lower it to, say, 1%, you could cut nearly 75% of interest expenses. This way, we could return to spending levels from five years ago, thus creating more room to push the problem further down the road. Because you can’t afford, if we head toward $2 trillion in interest expenses, which is exactly where we're heading, it will really become unsustainable.Jeffrey Gundlach

So I think investors need to consider the idea that the creditworthiness of U.S. Treasuries could become an issue. People don’t like to hear this. They think it’s too radical an idea.Jeffrey Gundlach

But let me tell you. You know, federal income tax used to be illegal. So they passed an amendment to make it legal. You know, according to its charter, the Federal Reserve is not allowed to purchase corporate bonds, but after the pandemic lockdowns, they did so on a small scale.Jeffrey Gundlach

So that was illegal. You know, in 2006, there were prospectuses for $2 trillion worth of unsecured mortgage-backed securities. It clearly stated in plain English that these mortgages must not be modified under any circumstances. That’s what was written in the prospectus, but millions of U.S. mortgages were modified anyway. So rules can be changed.Jeffrey Gundlach

Therefore, I am very uneasy about the risks of holding long-term government bonds. In our portfolio, our exposure in this area is essentially close to zero. For the small amount we do hold, over a year ago, I went to my government bond team and said that I wanted us to maintain the duration structure of our government bond holdings. But at every maturity level, I want you to swap out the bonds we hold for those with the lowest coupon rate within that maturity bracket. By doing this, we reduced the coupon rates on our 10-year and longer-dated government bonds from 4.75% to 1.5%. This way, in case they decide to modify these bonds to reduce the coupon rate. Well, if you hold a government bond with a 6% coupon, which was issued ten years ago as a 30-year bond with a 6% coupon, and if they lower the coupon to 1.5%, you will suffer a loss of more than 50 points.Jeffrey Gundlach

So, even if you think the probability of these risks materializing is low, there is no reason to take them. I believe everyone in the investment community agrees that if you are taking on risk without any reward, don't take it. The flip side of the same coin is that if you can eliminate a risk at zero cost, or even at a negligible cost, you should eliminate that risk.Jeffrey Gundlach

This is how I view things. Because of our debt burden and the way we finance the government through a $2 trillion deficit, it is completely unsustainable and must change. If something is unsustainable, it has to stop, and this situation must come to an end. And politicians, of course, have shown absolutely no willingness to control spending. Therefore, ultimately, the market will have to enforce it. That’s why I believe the path of least resistance for long-term government bond yields is upward. And this is somewhat concerning because we are now seeing some credit pressures emerge, as interest rates experienced one of the largest single-month increases in March 2026. The spreads on high-yield bonds have widened by approximately 75 basis points. So, risks are clearly accumulating in the current environment, and I am very interested in adopting a low-risk strategy in the coming months and quarters.Julia

Hey everyone, I hope you enjoyed this interview. If you could take a moment to hit the subscribe button, we’re working towards our next goal of reaching 100,000 subscribers, and your support can really help us get there.Julia

Thank you so much, and please continue to enjoy the rest of the interview. Wow, Jeffrey, you’ve set such a great framework for our discussion. As you pointed out, the first time you and I met for an interview was seven years ago. At that time, the debt was $22 trillion, and you noted that it is now $39 trillion. That $40 trillion mark may indeed become a real psychological threshold. And your argument is that during the next recession, interest rates will rise, and the dollar will fall. Wow, you really got my attention because this sounds like it could be a very painful awakening. I wonder, do you think investors intellectually understand this? Are their positions appropriately aligned? Because I also hear from you...Jeffrey Gundlach

No. Yes, the position is appropriate. Most American investors, especially their positions are in very bad shape. For more than a year, I have been advising American investors that their stock holdings should be 100% non-U.S. stocks and held in foreign currencies. This worked very well last year and is also effective this year. My primary advice is that American investors should buy emerging markets, not emerging market stocks, but emerging market stocks denominated in local currencies.Jeffrey Gundlach

This is the only thing that has actually risen this year. If you look at the situation so far this year, there is almost nothing that has risen. I just checked. What has risen this year includes gold, which rose by a few percent, the U.S. Dollar Index, which rose by 1.7%, the commodity index, with the Bloomberg Commodity Index rising by 21%. The only other thing that has risen is emerging market stocks, which rose by 1.4%. In contrast, you know, the U.S. stock market has fallen. I think it's time. This is rare for investors. So many people have been advising American investors to invest overseas, but this hasn’t worked for years, and now it’s starting to work. What excites me most about the investment market is when something makes perfect sense fundamentally but eventually starts happening in reality, and that’s what’s happening now. These overseas investments are outperforming the U.S., and there is still a long way to go. If you look at the Morgan Stanley World Equity Index, you can split it into two parts: the Morgan Stanley U.S. Index and the Morgan Stanley Rest of the World Index. About 15 to 20 years ago, the price-to-book ratio of U.S. stocks versus the rest of the world (excluding the U.S.) was the same. Now, the price-to-book ratio of the S&P 500 is more than double that of the rest of the world (excluding the U.S.). This is an extreme overvaluation. Everyone seems to be saying one word, 'American Exceptionalism.' This makes no sense to me. All they mean is that the U.S. outperforms other regions. When people say 'American Exceptionalism,' they mean the U.S. market, especially the stock market, outperforms foreign markets. I think we are in a multi-year phase. We might be in the second inning of a nine-inning baseball game metaphor, at most at this stage, where foreign markets will outperform the U.S. Therefore, I have an unusual asset allocation recommendation. I basically recommend 40% investment in stocks, all non-U.S. stocks. Some of these include Brazil, Chile, some Southeast Asian stocks, etc. I only suggest about 25% investment in fixed income, all within ten years, and all in the higher credit quality segment. Then I suggest about 15% investment in commodities. I might put 10% in the Bloomberg Commodity Index and 5% in gold because I think gold is currently very attractive, having surged last year to a very frothy level of $5,500, but earlier this week it fell to $40,100. So I think gold will continue to be a strong performer. Then I think investors should hold the remaining portion of their portfolio in cash, as asset prices will become cheaper as we move through 2026. Of course, one thing everyone is talking about, and I have been very vocal about, is the situation with private credit. Yes. Its scale is strikingly similar to the subprime and unsecured mortgage loans of 2006. People say it’s not big, only two to three trillion. Well, that was exactly the size of that market in 2006, leading into the global financial crisis. I think this will be a very long, drawn-out story and won't spread as quickly as the subprime issue did because the subprime problem was priced every day, every minute, due to something called the ABX Index for AAA-rated subprime products. You could see it start falling like a rock in early 2007. So you could see it drop from 100 to 93, then to 80. But this private credit issue is evaluated only about once a quarter. So data points will be few and far between.Julia

Yes, Jeffrey, when you mentioned that, it... reminded me of how you see similarities between today’s private credit market and the subprime market of 2006? Because in the summer of 2007, at a conference, you said that subprime would be an outright disaster and would only get worse.Jeffrey Gundlach

That’s right. It was at the Morningstar Conference in June 2007. Yes. I was invited to speak at the Morningstar Conference this year. Unfortunately, I couldn’t attend due to scheduling conflicts. But as I was thinking about giving the keynote speech at the Morningstar Conference, I said to myself, maybe I should open with 'Private credit is an outright disaster and will only get worse,' because that’s exactly what I improvised about the subprime issue in 2007. I didn’t plan to say that. It just came out, and I said it. But I’m glad I did. I mean, obviously, the issue is that everyone is becoming increasingly aware of the private credit market, those valuations aren’t real valuations. I think the head of Apollo also said that. Valuations aren’t real. So everyone knows that, at best, you’re dealing with a moving average situation. I mean, it was only about a year ago that I really started paying attention to private credit when a client from an insurance company visited, a very large insurance company client deeply involved in private credit. They said they had several managers, and eight of them held the exact same position, identical. That’s typical; it used to be a bit like club-style private credit, though there are now some minor disputes within families, but not long ago, it was a harmonious big family. He said, I have eight managers holding the exact same position. One of them is priced at 95, another at 8. What? Wait, what?Julia

Different marked-to-market values. Oh my, one...Jeffrey Gundlach

The same position, one valued at 95 and the other at 8. It really opened my eyes because I hadn’t previously understood so clearly what was happening there. But then, suddenly, you notice that later last summer or early last autumn, you started to see strange things, like bonds dropping from 100 to zero within a few weeks. What really struck me was a fund managed by a highly respected sponsor, which just a few months ago announced one day that they were adjusting the valuation of the fund from 100 to 81. That is a significant markdown for a fund overnight. But what many people didn’t fully realize was that it’s unlikely they marked every single bond, every single credit position, down from 100 to 81. That probably didn't happen. So you have to ask yourself, what exactly is the delta of some of these valuation changes? If half the fund was completely rock solid and they only wrote down the other half, that means they marked that half down by 38 points. If three-quarters of the fund was absolutely rock solid and then I wrote down 25% of the fund, that means that 25% of the fund went from 100 to 24 overnight. So what exactly is going on here? It certainly sounds like there's a lot of opacity in these valuations.Jeffrey Gundlach

I’ve always emphasized that private credit is a candidate for potential issues in the future because it’s such a rapidly growing market. I made an analogy that anything that goes from a small market to a booming market and becomes extremely popular—I said it’s like a small town in the Wild West. Okay, imagine you’re in a frontier area in 1820, with a farming population, all God-fearing, and you have a sheriff like Gary Cooper in 'High Noon,' who is kind-hearted, and everything works well. But then one day, someone discovers gold three miles outside of town. Suddenly, all these opportunists, some of whom are rogues, flood into the town because they want to get rich. So suddenly, the population explodes with massive growth, and some of them are unethical people. So you end up seeing a lot of crime, and everything starts to deteriorate. That’s what happens. That’s what happened in the CLO market in the early 2000s, and that’s what happens in any market. There’s nothing special about private credit. It’s just a booming market. So suddenly, you have a few companies that are doing well, they have good risk controls, etc., and they're getting decent returns.Jeffrey Gundlach

Then, for some reason, the sector becomes super-hot, like private credit did in 2021. Why did private credit become so hot in 2021? Because interest rates were still at zero. Then the government injected $7 trillion into the economy. So anyone with even a rudimentary understanding of basic economics should have known that inflation was going to rise significantly, and zero interest rates would become a huge losing proposition. So of course, interest rates rose from about 1% to over 5% on the 30-year Treasury, meaning a loss of 50 points. And of course, the stock market, when entering 2022 with extremely high price-to-earnings ratios, suffered huge losses due to such a sharp rise in interest rates.Jeffrey Gundlach

So when you know that subordinated debt and public bonds will deteriorate, and you know that traditional equities will deteriorate, you start looking for something else. Remember how SPACs suddenly became popular? Yes, like blind pools. Like, I don’t want stocks, I don’t want public equities, I don’t want public bonds because I know they will deteriorate. So give me something where I can’t map the risks of public bonds and public equities onto it, because if I can map the risks of public bonds and equities onto some new asset class, then I won’t like that new asset class because it will carry the risk mappings I want to avoid.Jeffrey Gundlach

So give me something where I don’t know what it is, and better yet, don’t mark it to market, so I don’t have to worry about volatility. That’s the private credit market. It’s a non-mark-to-market, completely opaque market. I’ll feel better because I don’t know what it is. So the argument for private credit became, hey, this is a low-volatility asset, which it isn’t, or, hey, it has performed well over the past four or five years. Well, that’s because the private markets... the public fixed-income markets fell 12% in 2022, and the stock market fell even more.Jeffrey Gundlach

So, of course, something that doesn't mark-to-market outperforms. It's like saying a CD outperforms a 30-year Treasury bond. That’s because you don’t mark it to market. So, it’s a fundamental flaw in the asset class. And there are a lot of them. You know, it has come to the point where now there are even advertisements on financial shows saying that, in the good old days, ordinary blue-collar Americans could buy a small piece of great American companies like General Motors and Boeing. But now, companies are staying private longer. So poor, ordinary Americans don’t have the chance to invest in these incredibly great private investment opportunities. So now we’re doing an ETF that invests in private credit. The problem now is that for endowments, it’s fine if the money is locked up in such products, but these funds now allow people to withdraw quarterly. Of course, we saw that in March, in some cases, redemption requests were three times what the fund prospectus allowed. So they allow 5%, and they have to deal with 15%.Jeffrey Gundlach

I heard today that, in an effort to soften people's perception of this issue, there is now a sponsor discussing launching a fund that would allow people to withdraw 7.5% quarterly instead of 5%. Then they say, in fact, we might even look at whether we can get approval to offer monthly liquidity so people can withdraw 2% per month instead of 5% quarterly. This starts to blur the line between public and private offerings in a very unsettling way. I mean, if these private products are going to offer monthly liquidity, why not make it weekly? Why not daily?Jeffrey Gundlach

Well, at some point, you do violate the notion that 'private' means you don’t have liquidity. In exchange for that, you have a longer investment horizon and perhaps a higher return. But once you start turning what is supposed to be an alternative to liquid investments (and their mark-to-market drawbacks) into essentially... a public market product, because now there is a fundamental mismatch between what is inherently a private product and liquidity. It simply cannot coexist. They cannot coexist. These are two different worlds. So when you distort something to expand the buyer base or appease holders who are already frustrated by the lack of liquidity, you end up with something that doesn’t work. It has no potential. It can't even function theoretically, which is why private credit must undergo a major shakeout.Julia

Do you think, um, if they talk about 'cockroaches,' does that mean it's a full-blown outbreak? Are we heading towards a crisis? How do you see this evolving?Jeffrey Gundlach

I think this space is overinvested. When I give speeches sometimes with audiences of 2,000 people, from around 2023 onwards until now, during the Q&A session, the first question is always, 'What do you think about private credit?' This question has been asked so many times that I started answering it this way: 'I guess you're asking me because you own a lot of private credit, right?' And they all say, 'Yes.' Everyone, they all own private credit. Everyone is involved. So, there are no new buyers left. There are only new sellers. So we got a glimpse of illiquidity with Harvard's endowment fund, which had to enter the bond market to raise cash to pay for maintenance and salaries because their donors stopped donating when protests and trouble occurred on campus. Harvard, with more than $50 billion in its endowment, didn’t have enough liquidity to cover several billion dollars in expenses, showing how tightly individuals, institutions, and pension plans are locked in. Another thing that isn’t discussed enough, but if you really want to delve into the details, there are podcasts made by former insurance examiners with 40 years of experience. They discuss how private equity owns private credit, acquires insurance companies, and then guides those insurers to buy private credit. They then transfer some of the insurance company’s risk to reinsurers located in Bermuda, Barbados, or the Cayman Islands, where U.S. regulators have no oversight. In some cases, private credit firms owning insurance companies transferred reinsurance risks to these islands, but they didn’t fully fund them. So they transferred, say, $50 billion in risk to reinsurers but didn’t back it with $50 billion in assets. They should actually have backed it with $55 billion in assets to maintain a 10% surplus as a prudent measure, but instead, they underfunded these reinsurers. I’m sure not 100% of companies do this, but again, it’s like the Wild West. You know, if they found gold in this reinsurance model, it’s like, you know, Apollo owns Athena, so they have these captive insurers, somewhat learned from Warren Buffett, who started doing it long ago and made a fortune, and they eventually claimed to transfer risks that weren’t actually transferred. So, some of these insurance companies or reinsurers don’t have 10% surplus to liabilities. They are more like 1% surplus.Jeffrey Gundlach

If, if the market valuation issues they face today turn into actual defaults, and if the U.S. economy falls into a situation worse than a mild recession—something more severe than a light downturn—then we could be facing a very significant problem.Jeffrey Gundlach

So I am extremely cautious now. I have been reducing risk for two years, and our current risk level is at its lowest in DoubleLine Capital’s 17-year history, and I am far from considering increasing risk. We need credit product spreads to widen significantly before we can prudently decide to start investing in, say, single-B-rated securities or lower. So we are focused on capital preservation and waiting for better opportunities, which will almost certainly arise as we move into 2026. It’s just that it probably won’t happen this year, because, as I said, with private credit, you don't get continuous information—it only comes once a quarter. So we'll see. There's one thing I believe. Anyone who has been in this space for even half as long as I have knows that redemption requests for private credit in June will be much higher than in March. Because when you request 14% redemption and they only give you 5%, what you do next is request 40%. Maybe you'll get a little more that way. It's like bond allocations. You know, I've been trading bonds for over 45 years, and when the market is good, and a company's credit is highly sought after, if they issue $500 million in bonds and you want $50 million, you don’t just subscribe for $50 million because demand will exceed $500 million. So you subscribe for $200 million to ensure you get your $50 million. Redemptions will work the same way. They aim for a certain percentage. If they don’t get it this time, they know there will be greater demand next time. So by June 2026, you will see some pretty wild redemption requests.Julia

I know you're right, Jeffrey. Okay, I’d like to bring up another area you've been closely watching. I find it fascinating, the point you made—that the Federal Reserve follows the two-year Treasury yield rather than leading it.Jeffrey Gundlach

No doubt. Yes, absolutely no doubt.Julia

Okay, could you explain that to the audience?Jeffrey Gundlach

Well, I would tell anyone else, if they can use charting tools, just go back 30 years, and if you want, plot the federal funds rate, the official federal funds rate, and the two-year Treasury yield. What you'll see is that when the federal funds rate stabilizes for a period of time, you start to see movements in the two-year Treasury yield. If it starts to decline, it means the Federal Reserve is about to start cutting rates. If the two-year Treasury yield rises, it means the Federal Reserve is about to start raising rates. When the Fed started cutting rates in September 2024, we had a huge gap. The two-year Treasury yield was about 175 basis points lower than the federal funds rate, and they finally started cutting rates. Then, when they started raising rates in 2021 and 2022, the two-year Treasury yield was far above the federal funds rate. When the Fed eventually raised rates, I remember it was by 25 basis points. That was at a meeting in February, and immediately after the Fed press conference, I appeared on a financial program and said they should have raised rates by 200 basis points because they were so far behind the two-year Treasury yield. The Fed simply follows the two-year Treasury yield.Jeffrey Gundlach

Indeed, you can really see this in the market behavior over just the past six trading days because the Fed press conference and the unchanged federal funds rate happened last Wednesday, which was yesterday a week ago. Interestingly, before the Fed's announcement, I was watching financial programs where all the stock-focused individuals were saying, 'Yes, you know, things are becoming less convincingly good, but we do have one thing going for us. The Fed will cut rates twice this year.' They said, 'The Fed will cut rates twice this year.' And I said, 'No, they won't.' The two-year Treasury yield is higher than the federal funds rate. Well, since then, the two-year Treasury yield has surged and is now around 4%. So with the federal funds rate where it is now and the two-year Treasury yield more than 25 basis points above the upper limit of the federal funds rate, you cannot expect to see a decline in the federal funds rate. Therefore, you're increasingly going to hear that it's already begun. You’ll hear people discussing that maybe the next move by the Fed is a rate hike, which would be such an aggressive shift in rhetoric compared to the consensus (two rate cuts) just six trading days ago, although I didn’t believe it at the time. I, I, I. Because the two-year Treasury yield was already higher than the federal funds rate at that point. But that’s only because the Fed doesn’t have any super-secret information. They’re just looking at everything we’re all looking at. And the two-year Treasury yield reflects the collective wisdom of all those investing in safe assets, investing in relatively short-term funding, which is the level they think rates should be at. That’s where the federal funds rate should be. I think we should eliminate the Fed and directly use the two-year Treasury yield as the short-term interest rate.Julia

Okay, so what do you think? Okay, the next step is a rate hike. Why do you think that? Okay, most likely it's a rate hike. What do you think?Jeffrey Gundlach

Certainly. It looks like that. Okay. If, if, certainly, if West Texas Intermediate crude oil stays at $95 a barrel, and if that persists throughout the summer, the Fed will absolutely raise rates.Julia

Alright. And as you pointed out again in your argument, during the next recession, interest rates will rise and the dollar will fall. Regarding the recession, do you have a probability in mind? For example, how likely is it that we will enter a recession soon, or what’s the timeline? I, I, I.Jeffrey Gundlach

No, this is not the framework I think within, because there is no scientific basis behind such matters. But I, I, I, I, I, I believe, I believe that the continuously rising interest rates are facing upward pressure due to supply and still high inflation. What I mean is, I think, for example, mortgage rates have returned to 6.5%. If this situation continues, mortgage rates will reach 7% again. The real estate market cannot even withstand mortgage rates at a high of 5%. What I mean is, even if mortgage rates are below 6%, the real estate market is still more ample. Now it's at 6.5%? If this high inflation framework continues, they will continue to rise. So, yes, I, I certainly think that there is a high possibility that the authorities will announce a recession starting at some point in 2026. I would give it at least a 50% probability.Julia

Um. Alright. I want to return to our financial situation because you also wrote an article in The Economist, and I will provide a link for the readers. I believe it was in December 2024 that you outlined two possible outcomes in that article. Do you think we are heading towards currency devaluation? Or the restructuring you mentioned earlier? I guess my question is what do you think the consequences will be? And what might be the triggering factors?Jeffrey Gundlach

Well, I think my basic scenario is that long-term government bond yields will rise until they reach a level that is hard to ignore in terms of its impact, which I would say is around 6%. I believe that if long-term interest rates rise to about 6%, people will start to calculate and realize that they are heading towards over $2 trillion in interest payments, which is unsustainable. So at that point, you might have this concept of restructuring come up. Or we might say, well, let's just go for a soft default; we won't pay the coupons, right? What will happen is that we will have generations during which we cannot borrow money because the prices of these long-term bonds will collapse. No one will trust us to issue long-term debt anymore, which ironically will become part of the solution. Because if we cannot issue any debt, we will actually have to balance our budget. And that is what we should really be doing. We should not run a debt-driven economy. You know, the $2 trillion in our economy is just borrowed money at the federal government level. Just at the federal government level. So the trigger will be that you cannot ignore the impending interest payments, and you must take action on this. Another option is currency devaluation, where you simply use, you know, cheaper dollars to pay it back. You pay it back with inflation, relative to...Julia

Inflation.Jeffrey Gundlach

You will allow for inflation, by the way, Julia, this is exactly what they did after World War II. The debt-to-GDP ratio at that time was about the same as it is now. Inflation was expected to be much higher after the war, and it indeed was. But they kept interest rates at extremely low levels, with government bond yields at 2.5%, while inflation rose to high single digits. So basically, you ultimately erode debt through inflation and experience very severe negative real interest rates. This led to a 40-year bear market in government bonds. This is also what will happen here.Jeffrey Gundlach

If we devalue. If we devalue, you will be living in a high-interest-rate environment for a long time. But the alternative is this soft default. I can't think of any other tools available, basically some combination of devaluation and soft default.Julia

I think, equally concerning is that, technically, we are still in, if you will, 'good times,' and we haven't faced a major emergency yet. And this is our fiscal situation.Jeffrey Gundlach

Yes, exactly. Well, that's the whole problem. You know, we, we, we. You don't have a 'rainy day fund' at all. You know, it's not raining right now, and we're already spending the 'rainy day fund.'Julia

You know, listening to you, one thing caught my attention. You mentioned several times in this conversation that you are in a capital preservation mode, and you are reducing risk. It's kind of like, when someone like you says that, it piques my interest.Julia

What worries you the most? Like, what is the risk you face today? Yes, I know you are at DoubleLine Capital, and you don’t cross the double-line risk threshold. So, what is the risk that worries you the most or keeps you up at night now? Or if you’re not, you know, not really losing sleep over it.Jeffrey Gundlach

I, I, I, I really believe that the interdependent relationship between private credit and private equity will not end well. I think it is unhealthy. So, I, I really, I have been saying this since around May of last year. It has been almost 10 months now, and the next question will be about these private markets. Of course, the headlines about the private credit market are already out there. The alarm bells are ringing quite loudly. Very loudly. And this is not a natural state.Jeffrey Gundlach

So I believe that defaults in certain areas of the private credit market will lead to significant repricing, reducing credit risk at that level, such as single-B or lower ratings.Jeffrey Gundlach

So, I, regarding investments, I rarely take risks. I want an excellent opportunity. Only then will I take risks, and I believe that the expansion of high-yield bond spreads by 50 to 70 basis points from historically low levels is far from an excellent opportunity. I think, you know, high-yield bond spreads were at 350. Now they are around 425. You know, call me when they reach 700. That's when I start taking risks.Jeffrey Gundlach

Most people do not realize that the bank loan market, the triple-C bank loan market, has already become a disaster. Prices have fallen significantly, and the spreads on triple-C bank loans, generally speaking, at the index level, are nearly 2,000 basis points. This means that no one believes they will be repaid. So defaults are imminent.Julia

Yes, I like this. "Waiting for an excellent opportunity." Okay, you mentioned another thing during your conversation, and your prediction was very accurate. In fact, it was named, I think, one of the best market predictions of the year by Business Insider, but in your webcast in March 2025, you said gold, which was around $2,915 at the time, might rise to $4,000, and indeed it did in October. Of course, we saw earlier this year it touched $5,500. Now it has returned to, I think I saw today. I hold gold. So I checked today, it's above $4,300. But you said now is an opportunity; are you buying gold now? Or how are you managing your gold positions?Jeffrey Gundlach

I actually bought some. I purchased some gold mining stocks last June, which was my last gold-related move, and I was extremely fortunate. It was pure luck because that was exactly when they started to take off, you know. But there's an interesting story about my gold prediction. I was on a TV show when gold was at $2,970. The interviewer asked me if I thought it would break through $3,000. I said, what kind of prediction is that? Predicting a 1% increase? Yes, so, I didn’t mean to say this, but given the way the question was posed, I said, you know what, it will exceed $4,000 this year. Forget $3,000; it will surpass $4,000. And it made me look like an honest person. I mean, it eventually rose to around $4,500 in the fourth quarter of last year. It even went above $5,000 later. So, I believe gold is real money. I think people are starting to realize that. Central banks will continue to be a significant source of demand for gold. Before Nixon abandoned the gold standard, about 70% of central bank reserves were in gold, then it dropped to 20%. At that time, everyone turned to the US dollar as the preferred reserve. Well, now gold is rising again. It has increased to about 30% of central bank reserves. I think it’s entirely reasonable to expect that the proportion of gold in reserves could reach 50%, which would generate enormous gold demand. So here, gold is no longer just for survivalists or eccentric speculators. It is a legitimate asset class being reintroduced into the central banking world as a real asset class, worthy of holding one-third of your reserves. So, I just don’t see any reason for anyone to sell.Jeffrey Gundlach

Gold. I’m not a silver enthusiast. I know many people like silver because, you know, it multiplies wealth. When gold’s beta operates positively, silver rises more. But silver is more of an industrial metal. I think gold is the real deal, so I’ll stick to the standard rather than derivatives.Julia

You’ve been in the investment industry for 45 years. No. This is, from your perspective, a relatively challenging environment, right? For instance, is it harder to make money?Jeffrey Gundlach

No, the most difficult environment for me was in 2021 when the bond market offered no yield. There was a moment when the only way to get 5% from US fixed income was to buy the junk bond index with 50% leverage and hope there were no defaults, since the junk bond index yielded 3.5%, hoping there would be no defaults. Believe it or not, if you actually did that, if you bought the index yielding 3.5% with 50% leverage to achieve that 5% return, you’d go bankrupt because your financing costs rose to 5.375%, while your coupon remained at 3.5%. So you had nearly a 2% negative arbitrage, bleeding every day, every moment, and your junk bond prices were far below cost. So you’d face margin calls.Jeffrey Gundlach

So if you, in the fixed-income space, we all know in broad investing there’s fear and greed driving people. But fear becomes stronger than greed. However, the most dangerous thing isn’t fear or greed—it’s 'demand'.Jeffrey Gundlach

"I need to earn X% in returns," because, back in 1993, I was in the office of a major university's treasurer when the president happened to come by. He said, the president asked the treasurer, how can we get our endowment fund to yield 6%? Well, the endowment needs to generate 6%. The treasurer said it’s impossible, given that Treasury yields were at 3%, and nothing could produce 6% returns. The president told the treasurer, wrong answer. I want to know how we can achieve 6%. He didn’t want to hear "we can't do it." He said, no, you must achieve 6%. What are you going to do about it? Well, the result was that people ended up doing crazy things. For instance, Orange County, and some strange Mae bonds with odd characteristics, which eventually fell from 100 to around 40 during the bond bear market of 1994—and that wasn’t even a particularly severe bear market. So, in trying to achieve 6%, they lost 60%. Therefore, investing based on 'need' is the most unwise approach. You can only say, this year we will fall short of the target return, we will earn this amount this year, and that amount next year, averaging out to 6%. Never invest based on 'need,' because you will always take on unwise risks.Julia

That’s a very good lesson. Jeffrey, that’s why you’re the 'Bond King.' You truly are the 'Bond King.' I know you might not say that yourself, but you're the one who has stood firm through it all.Julia

So, can I ask you about... can I ask you about California? You recently posted a tweet. Or an X post, since people often ask you about municipal bonds, and you usually don’t have much to say. But looking at the deficits caused by absurd spending and tax policies, as well as accelerating revenue erosion, I’ll just say, avoid all general obligation municipal bonds in California, Illinois, and New York. I’ve never bought a general obligation bond.Jeffrey Gundlach

We can...Julia

As someone living in California, what’s the situation there? Are they doomed?Jeffrey Gundlach

I hold California municipal bonds, but I do not hold general obligation bonds. I only hold bonds that are tied to a specific revenue source, such as water projects, where you know there is a revenue stream. I only buy bonds rated investment-grade single-A or higher. This is not because they are insured, but because the underlying revenue stream actually exists. As for general obligation bonds, I...Jeffrey Gundlach

I, I think, I, if, so what I would most want to avoid, I think, are Chicago municipal bonds. I, I just can't imagine why anyone would be willing to take the risk of legislative changes. I mean, anything could happen. The rules can be changed. They could say, if your income exceeds a certain level, municipal bonds become taxable. They could say, if your income exceeds this amount, we will cut the coupon on your bonds. Anything could happen. And with such enormous wealth inequality, which increasingly manifests itself in political activities, you have to be extremely concerned about these issues.Jeffrey Gundlach

Yes, California may try to impose a billionaire tax. I think it will be stalled in court for many years before it is actually implemented, because there will be huge interest groups wanting to drag it into litigation. So I'm not too worried about the issue of the billionaire tax, but it is indeed an unsettling trend. I know Bernie Sanders wants to propose this nationwide.Julia

Do you think California will go bankrupt?Jeffrey Gundlach

In a way, it already has gone bankrupt. I mean, we have... We're supposed to have a balanced budget, but we're nowhere near a balanced budget. You know, we, we, we started projects like the high-speed rail project. It was supposed to run between San Francisco and Los Angeles. It was originally scheduled for completion in 2020. The last time I checked, it's 2026, and they haven't laid an inch of track. So we are far behind schedule. The budget was originally $30 billion. Now they say that if they want to complete the high-speed rail from Los Angeles to San Francisco, it will exceed $130 billion. That’s a $100 billion cost overrun. Therefore, instead of saying we’re going to spend $130 billion, they decided to use around $30 to $35 billion to build between Merced and Bakersfield. That’s a stretch absolutely no one has demand for.Jeffrey Gundlach

It's absurd. So, yes, I think as California raises taxes, you talk about a billionaire tax, all they're doing is depleting the tax base. In the past 12 months, we've already seen the five wealthiest individuals in California leave the state, and it's only going to accelerate. California thinks that if you leave, they can impose a wealth tax on you. Good luck. Good luck trying to track down those who live in Tennessee because you're going to send them a bill.Julia

Oh my God, what are you going to do?Jeffrey Gundlach

What can you do? Not move back?Julia

Yes, you'll drive so many people away. They'll come to North Carolina where I am and drive up our housing prices.Jeffrey Gundlach

If they impose a wealth tax, the cost of collection will exceed the tax revenue.Julia

That's also a good point. Jeffrey, before I let you go, can I ask you one final question? Sure. I don't know if you're in a rush. I'm happy to chat more, but I also need to be mindful of your time.Julia

Oh, the question is: What do you think is something right now where, if you made a prediction, it might not seem like the consensus and is absolutely not obvious. But maybe a year from now, if we have this conversation again, it will be more widely accepted?Jeffrey Gundlach

I think there will be three parties fielding candidates in the next presidential election?Julia

Do you think that candidate will be viable? Because...Jeffrey Gundlach

It will be interesting. The Democrats and Republicans have created significant barriers for third parties, making it difficult for them to succeed. However, interest in a third party will be high enough to overcome these obstacles.Julia

I wonder if this means we are entering the 'Fourth Turning'?Jeffrey Gundlach

I, I, I spoke with Neil Howe about 16 or 17 years ago. It was interesting because I didn't know who he was and had never heard of the 'Fourth Turning.' But as we talked, we shared exactly the same perspective, albeit expressed slightly differently. I fully understood what he meant by the 'Fourth Turning.' I said that I believe a major transformation, a big 'reset,' or if you will, a 'reorganization' of our system is long overdue. I mentioned that I think it will happen around 2030, and he agreed. I still think it’s around 2030. I believe Neil still considers that a reasonable timeframe. Yes, so we are very much in sync on this concept.Julia

Yes, we also really like Neil Howe on our channel, and we might see that climax soon. I must say, Jeffrey Gundlach, it's such an honor to have you back on the show again. I always enjoy our conversations. Again, you are one of my favorite people to interview, and having you on this program is truly a pleasure. It means a lot to me, and as a podcast host, it's a significant milestone—I'm incredibly grateful. I hope this isn’t our last conversation. I’d be more than happy to welcome you back anytime you’re willing to spare us some time. Thank you so much. Jeffrey Gundlach, founder and CEO of DoubleLine Capital, the 'Bond King,' I’m deeply grateful to you. Thank you again.Jeffrey Gundlach

Thank you, Julia. I really enjoyed our conversation.

Editor/KOKO