Some of Wall Street's top bond fund managers have indicated that financial markets are significantly underestimating the risk of a military strike by the United States against Iran, which could lead to a sharp slowdown in an already weak U.S. economy.

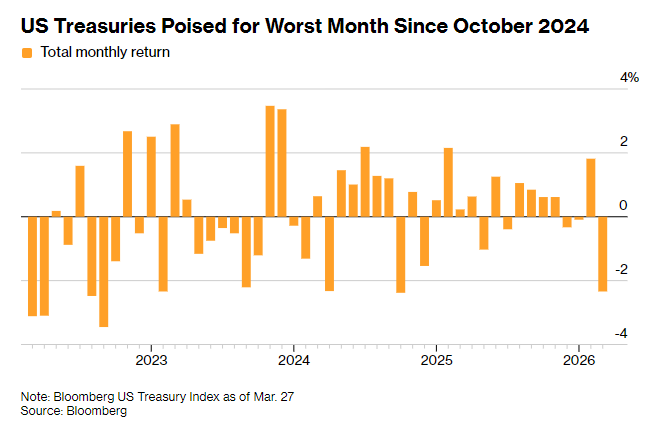

Currently, international oil prices have broken through $110 per barrel, and with no signs of conflict abating, market trading remains focused on inflationary pressures. This has driven the U.S. Treasury market to suffer its worst monthly selloff since October 2024, with investors increasingly betting that the Federal Reserve will raise interest rates again within the year.

However, asset management giants such as Pacific Investment Management Company (PIMCO), JPMorgan, and Columbia Threadneedle Investments have begun positioning for a potential economic downturn—anticipating that weakening growth will eventually trigger a rebound in the bond market, driving yields significantly lower.

Kelsey Berro, fixed-income portfolio manager at JPMorgan Asset Management, stated: "With each passing day of the conflict, the market moves closer to being forced to confront the negative impact on economic growth, which will ultimately push U.S. Treasury yields lower. Current yield levels have risen to become quite attractive overall."

Kelsey Berro, fixed-income portfolio manager at JPMorgan Asset Management, stated: "With each passing day of the conflict, the market moves closer to being forced to confront the negative impact on economic growth, which will ultimately push U.S. Treasury yields lower. Current yield levels have risen to become quite attractive overall."

As surging energy prices, rising borrowing costs, and steep stock market declines begin to squeeze businesses and consumers, economists are revising growth forecasts downward while raising the probability of a recession. Goldman Sachs estimates the likelihood of a U.S. economic recession over the next 12 months has risen to about 30%, while PIMCO believes this probability exceeds one-third.

Typically, pessimistic economic expectations benefit bonds, as they increase the likelihood of the Federal Reserve cutting interest rates to stimulate the economy. However, the current situation is markedly different—traders believe that skyrocketing energy prices will further constrain the Fed, which is already grappling with stubbornly high inflation, making rate cuts unlikely.

The resulting sharp sell-off in the bond market has driven yields across the board to soar. Since the U.S. launched airstrikes at the end of last month,$U.S. 2-Year Treasury Notes Yield (US2Y.BD)$and$U.S. 5-Year Treasury Notes Yield (US5Y.BD)$has surged by more than 50 basis points; the 30-year yield is approaching 5%, just a step away from its peak when the Federal Reserve pushed rates to a more-than-two-decade high in 2023.

This trend primarily reflects concerns that rising energy prices will push up costs across various goods. The Organization for Economic Co-operation and Development (OECD) warned last week that the U.S. consumer price index (CPI) could soar to 4.2% this year. Investors are thus demanding higher bond returns to hedge against inflationary erosion.

However, seasoned bond investors believe the current selloff has created a prime opportunity to lock in high yields—the focus on inflation risks is overshadowing threats to economic growth.

Daniel Ivascyn, chief investment officer of PIMCO, which manages over $2 trillion in assets, stated: "Shocks originating from inflation often rapidly evolve into growth shocks. We are now at a tipping point where the economy is poised for a significant weakening."

In fact, risks in the U.S. economy had been accumulating even before the outbreak of the war. Since Trump's return to the White House, the imposition of additional tariffs and disruption of global trade have led to a continued cooling in the job market. In February, U.S. employers cut 92,000 jobs, and the March data, to be released on Friday, is expected to show only a mild rebound with an estimated increase of just 60,000 jobs. Additionally, markets have been volatile due to concerns over artificial intelligence (AI) and localized pressures in the private credit sector.

Now, the conflict that has lasted for four weeks has essentially halted oil shipments through the Strait of Hormuz. This shock has already reached end consumers, driving U.S. gasoline prices to their highest levels since the surge in inflation following the pandemic.

Rick Rieder, head of fixed income at Blackrock, which manages over $2 trillion in assets, believes that the Federal Reserve should still cut interest rates to cushion the impact. He stated that once the economic outlook becomes clearer, he will increase his purchases of short-term bonds.

“In the coming weeks, we will monitor how the situation evolves, and then I will enter the market to buy,” he said during an interview.

As of Friday, futures markets indicate that traders have fully ruled out the possibility of a Fed rate cut in 2026, expecting it to maintain rates unchanged while pricing in about a one-third probability of a 25-basis-point hike within the year.

As$U.S. 30-Year Treasury Bonds Yield (US30Y.BD)$Amid the rise, Ed Al-Hussainy, portfolio manager at Columbia Threadneedle, has started to increase holdings of long-term bonds. He predicts that if the Federal Reserve raises interest rates further, adding new pressure to the economy, long-term yields will eventually retreat.

“The more aggressive the Fed’s tightening policy, the greater the downward pressure on the long end of the bond yield curve as it needs to price in total demand and inflation premium,” he remarked.

Editor/Melody