Source: Shenwan Hongyuan Macro

Authors: Zhao Wei, Chen Dafei, Zhao Yu, Li Xinyue, Wang Maoyu

Export controls, futures market interventions, and tax cuts may be alternative measures.

Abstract

Facing the persistently rising oil prices, Trump's traditional policy tools are becoming insufficient. If oil prices continue their volatile climb, what tools does the Trump administration have left to suppress prices, and will it resort to 'TACO' again under market and inflation pressures?

I. Key Considerations: How Trump May Suppress Oil Prices — A High Probability of Resorting to 'TACO' Again

I. Key Considerations: How Trump May Suppress Oil Prices — A High Probability of Resorting to 'TACO' Again

A. Measures already taken by the U.S. government to control oil prices: releasing reserves and easing sanctions, but with limited effect

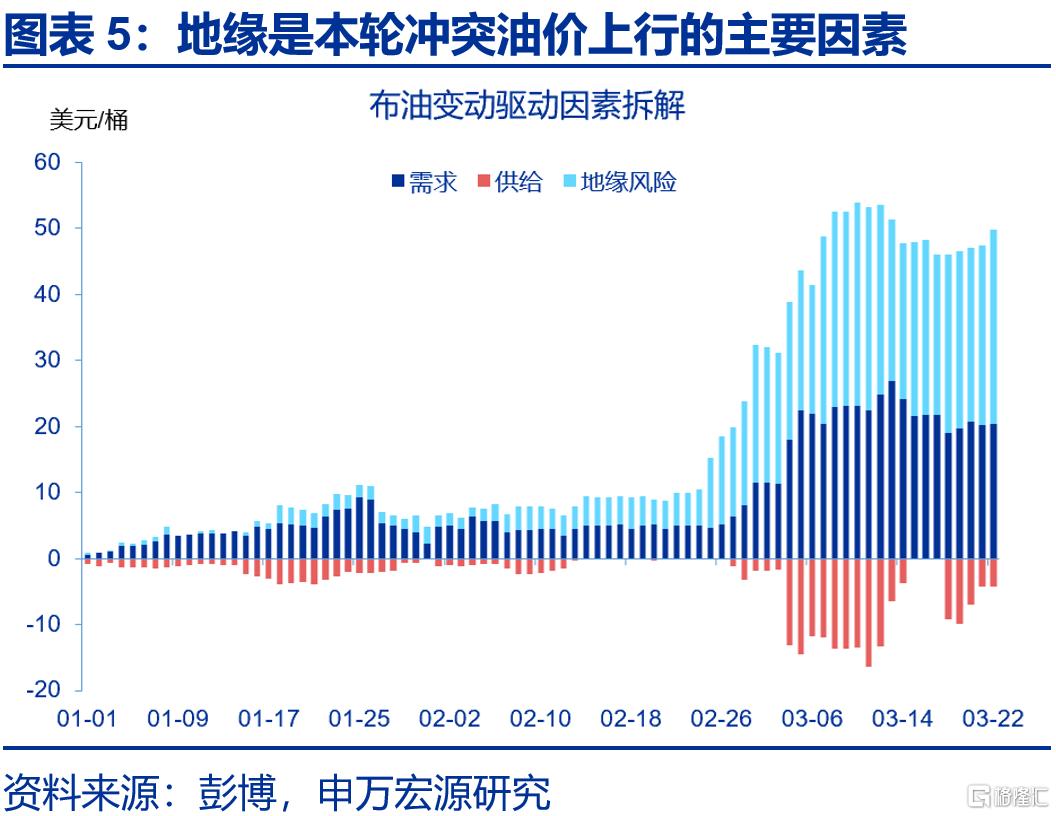

Geopolitical premiums accounted for 65% of this round of oil price increases. Even considering only supply and demand factors, oil prices are unlikely to return to pre-conflict levels. In this oil price rally, geopolitical premiums contributed $29.6, while supply and demand factors added $16. Considering only supply and demand factors, the midpoint of oil prices has reached $80 per barrel, surpassing pre-conflict levels. Future declines in oil prices may need to go through two stages: first, suppressing risk premiums, then rebalancing supply and demand.

Since the conflict began, Trump has mainly suppressed oil prices by releasing reserves, easing sanctions, and rerouting pipelines. First, IEA member countries released 400 million barrels of crude oil, increasing reserves by an average of 3.33 million barrels per day; second, temporarily easing maritime crude oil sanctions on Russia and Iran; third, rerouting oil pipelines from countries such as Saudi Arabia. These measures can provide 6.83 million barrels per day of supply within 30 days, but are insufficient to fully suppress risk premiums.

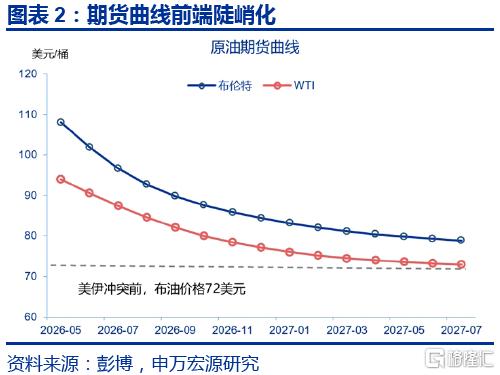

The existing measures have failed to reverse the upward trend in oil prices, leading to greater divergence in global oil prices. At the regional level, segmentation in the global market has deepened. Asia is the most strained, Europe is moderate, and America enjoys a relative buffer. In terms of term structure, the front end of the futures curve has steepened, with near-term prices significantly higher than long-term ones. Along the industrial chain, refining spreads have widened, with the apparent spread between gasoline and crude oil expanding to $27.6 per barrel.

B. Future measures that the U.S. government may adopt: export controls, futures market interventions, and tax cuts could be alternative options

If the U.S. implements crude oil export controls, oil prices may not fall but instead further increase upward pressure on international oil prices. In 2025, U.S. crude oil exports ranked just behind those of Saudi Arabia and Russia. If the U.S. reduces exports, the available global crude oil supply will contract further, potentially driving international oil prices even higher. Additionally, U.S. gasoline prices are benchmarked against Brent crude oil, so restricting crude oil exports is unlikely to lower domestic gasoline prices.

If the US Treasury directly trades crude oil futures, it may create a short-term impact on prices, but the capital constraints would be extremely high. To achieve a visible effect on WTI, the Treasury would need to establish a short position of 100,000 to 150,000 contracts, corresponding to a notional scale of 100 million to 150 million barrels of crude oil. Once floating losses reach the margin line, additional funds must be injected immediately. After exhausting available funds, the Treasury would need to seek special appropriations or coordination with the Federal Reserve.

If oil prices continue to spiral out of control, the US might shift toward direct interventions on the consumer side, with tax cuts and temporary regulatory relaxations potentially entering the policy toolkit. Possible measures include: 1) Temporarily exempting the federal fuel tax, which could directly lower gasoline prices by 18.4 cents per gallon; 2) Reducing refining costs, with an average impact of 0-1 cent per gallon; 3) Relaxing summer gasoline environmental formulation restrictions, with an average impact of 3-10 cents per gallon.

(III) The possibility of Trump initiating TACO again: The downside in oil risk premium is limited, making TACO a high-probability option.

The decline in oil risk premiums faces three major obstacles. First, negotiations may experience setbacks, and even if a ceasefire agreement is reached, the market might retain expectations of a 'second conflict.' Second, there is a lag in the recovery of physical crude oil supply. Third, the Strait remains an important negotiating lever for Iran, which may enter a new normal of selective passage—retaining influence over shipping while reducing the risk of full-scale conflict with neutral countries.

Under the baseline scenario, the Strait will struggle to fully restore passage, with oil prices remaining above pre-conflict levels but below their peak. In the fourth quarter, Brent crude prices may hover around $85 per barrel, and by September, the Strait's traffic volume may recover to 70% of its prior level. Under an optimistic scenario, passage through the Strait gradually recovers, and risk premiums diminish but are unlikely to fully dissipate. In an extreme scenario, oil prices surge to a high in the second quarter but cannot sustain elevated levels over the long term.

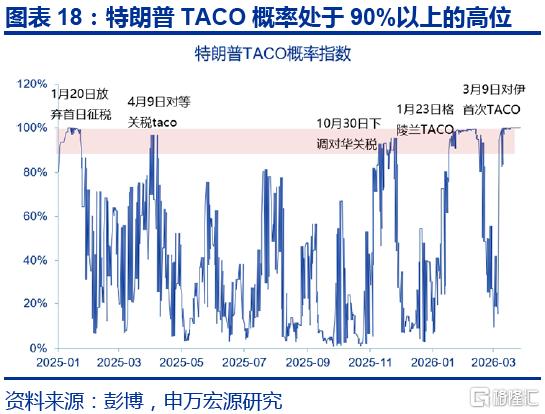

Although the Trump administration has adopted a tough stance, the likelihood of making greater concessions is increasing. Based on the characteristics of Trump’s policies, this article constructs the TACO Index, which has performed exceptionally well in historical backtests, accurately predicting four key concessions since Trump 2.0. Currently, the probability of TACO stands at a high of 95%, and the likelihood of Trump making larger concessions may be underestimated given the limited effectiveness of the aforementioned measures.

Risk warnings: Escalation of geopolitical conflicts; Unexpected slowdown in the US economy; The Federal Reserve unexpectedly turning more 'hawkish.'

Main Body of the Report

Facing persistently rising oil prices, Trump’s conventional policy tools have become insufficient. If oil prices continue to climb erratically, what price suppression tools remain in the Trump administration’s arsenal, and will Trump 'TACO' again under market and inflation pressures?

Hot Topic Analysis: How else can Trump suppress oil prices?

What measures has the US already taken to control oil prices? Releasing reserves and easing sanctions—conventional measures with limited effects.

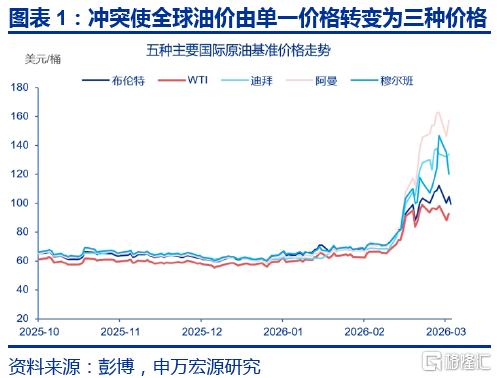

Following the escalation of geopolitical tensions between the US and Iran, global oil prices have exhibited stronger divergent characteristics. At the regional level, the segmentation of the global market has deepened. Asia is the most strained, Europe is in the middle, and the Americas have a relatively greater buffer. The Oman and Dubai crude oil benchmarks saw larger increases, reflecting spot shortages in Asia.$Brent Last Day Financial Futures (JUN6) (BZmain.US)$Prices higher than$Crude Oil Futures (MAY6) (CLmain.US)$, reflecting the higher premium brought to Brent crude by geopolitical risks. The release of strategic reserves by the US, coupled with rising inventories at Cushing, suppressed WTI oil prices, leading to an expansion of WTI’s discount to Brent. In terms of the term structure, the front end of the futures curve steepened, with near-term prices significantly higher than long-term ones. The May Brent crude contract was priced at $108, while the September contract had retreated to $89.8, expanding the four-month spread to $18, indicating that the core market issue remains short-term flow disruptions. On the industry chain level, refining margins widened. The May RBOB gasoline futures were priced at $3.07 per gallon, equivalent to $128.8 per barrel, compared to $101 per barrel for May WTI crude. This implies that the apparent spread between gasoline and crude oil had expanded to approximately $27.6 per barrel.

Trump simultaneously curbed oil prices through supply releases, easing sanctions, and rerouting exports. Prior to the US-Iran conflict, the global crude oil market was in a relatively loose balance, with supply slightly exceeding demand by an average increase of 1.9 million barrels per day in inventory, and the Strait of Hormuz transporting an average of 20.3 million barrels per day. Following the conflict, measures taken by the US and other countries to suppress oil prices included: first, the release of crude oil inventories.

On March 11, 32 IEA member countries announced the release of 400 million barrels of crude oil. Among them, the US contributed 172 million barrels, making it the largest contributor. Over a 120-day period, this would add an average of 3.33 million barrels per day to supply; second, temporary relaxation of crude oil sanctions. A 30-day exemption was granted for Russian crude sanctions, allowing Russian crude stranded at sea before March 12 to be sold, filling a gap of 1.8 million barrels per day; a 30-day exemption was also granted for Iranian oil exports, permitting Iranian crude loaded before March 20 and unloaded before April 19 to enter the market, addressing a shortfall of 1.7 million barrels per day; third, Saudi Arabia and others rerouted pipelines. Collectively, these measures could provide an additional 6.83 million barrels per day of crude oil supply.

From the composition of oil prices, geopolitical premiums accounted for 65% of the total price increase in this cycle. Even when considering only supply-demand factors, oil prices are unlikely to return to pre-conflict levels. As of March 22,$Brent Last Day Financial Futures (JUN6) (BZmain.US)$The price stood at $110.7, of which the long-term central price of oil was $64, with geopolitical risk premiums contributing $29.6 to the rise and supply-demand factors accounting for $16.1 of the increase. Geopolitical risks have been the main driver of the rise in oil prices since the start of the conflict, contributing 65% of the increase, with supply-demand factors accounting for the remaining 35%.

Even when considering only supply-demand factors, the corresponding central oil price has reached $81, suggesting that even if geopolitical risks decline in the future, oil prices may struggle to return to pre-conflict levels. Further extrapolation suggests that any future retreat in oil prices may occur in two phases: the rollback of risk premiums and the rebalancing of supply and demand. The first phase decline may occur quickly, but the subsequent phase of retreat is likely to slow down significantly.

In the future, possible measures that the US government may adopt include export controls, futures market intervention, or tax cuts.

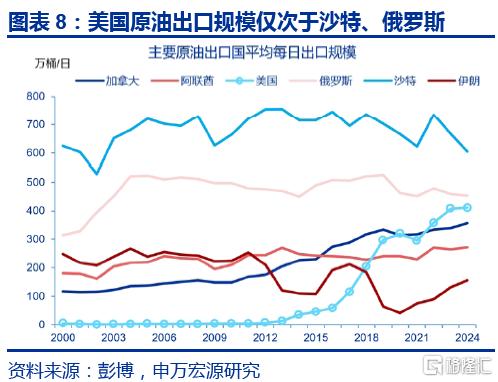

If the US introduces measures to restrict crude oil exports, oil prices may not fall but instead face further upward pressure. Limiting US oil exports could produce several effects: First, restricting exports cannot lower international oil prices but may instead push up Brent crude prices. In 2025, US crude exports averaged about 4 million barrels per day, second only to Saudi Arabia and Russia, mainly destined for Europe and Asia. It is one of the few sources capable of replacing Middle Eastern crude supplies. If the US reduces exports, the global availability of crude oil will further contract, potentially driving international oil prices higher. Restricting exports may also reduce incentives for future US production increases, diminishing long-term global supply expectations.

Secondly, restricting crude oil exports is unlikely to significantly reduce domestic gasoline prices in the United States. The refining hubs of the U.S. are concentrated along the Gulf Coast, where crude costs are linked to Brent oil prices rather than the inland WTI prices. The global spot market for gasoline primarily uses Brent crude as its pricing benchmark. Therefore, U.S. gasoline prices exhibit a stronger correlation with Brent crude than with WTI. Ultimately, restrictions on exports may primarily benefit U.S. refineries, as domestic crude retention could lower WTI prices, potentially widening the Brent-WTI spread and increasing refining margins for existing facilities.

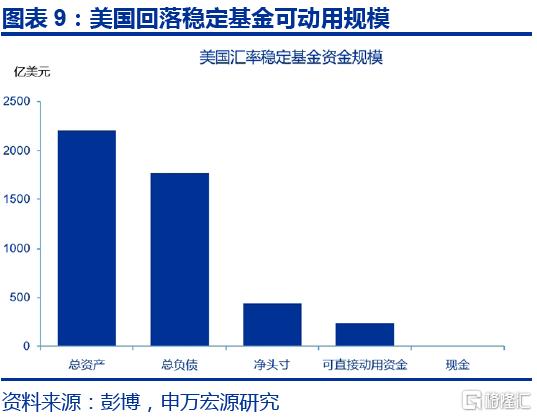

If the U.S. Treasury directly intervenes in the crude oil futures market, it may create a short-term impact on price expectations, but the financial constraints and political costs would be extremely high. Direct buying or selling of crude oil futures contracts by the Treasury to stabilize speculative activity and price volatility would involve uncertain operational details and outcomes. If the Treasury were to trade crude oil futures, funding would likely come from the Exchange Stabilization Fund (ESF). As of January 2026, the ESF holds total assets of $220.8 billion, total liabilities of $176.7 billion, and a net position of $44.2 billion. Only about $23.8 billion is readily available, of which merely $200 million is in cash.

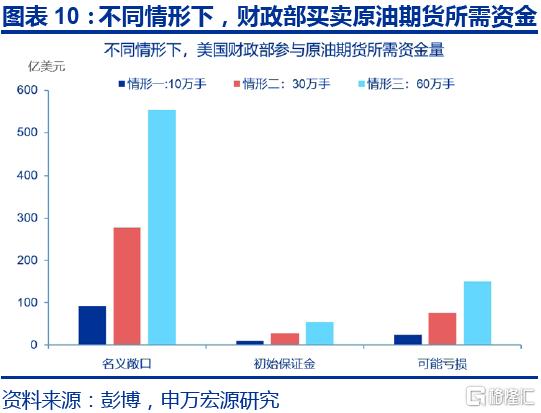

Trading futures may temporarily lower oil prices, but sustainability could be limited. In terms of required capital, each WTI contract represents 1,000 barrels, with average daily trading volume of 1 million contracts and open interest of 4 million contracts, equivalent to approximately 4 billion barrels of crude oil. To achieve a noticeable impact on WTI prices, the Treasury would need to establish a short position of 100,000 to 150,000 contracts, corresponding to a nominal scale of 100 to 150 million barrels of crude oil (comparable to the recent release of 170 million barrels from the Strategic Petroleum Reserve). A smaller scale might fail to register in the market. A 100,000-contract position represents only 10% of daily trading volume and 2.5% of open interest.

If oil prices continue to rise due to geopolitical factors, the Treasury’s short positions could face significant losses. If the Treasury shorts WTI futures, it would be exposed to unlimited downside risk. For instance, a $10 increase in oil prices could result in daily paper losses of $1 billion for 100,000 contracts. At a position size of 300,000 contracts, a $25 increase in oil prices could lead to cumulative losses of $7.5 billion upon liquidation. Once losses breach margin requirements, the Treasury would need to immediately inject additional funds. After exhausting available resources, the Treasury would have to seek special appropriations from Congress or coordination with the Federal Reserve, incurring substantial political costs.

If oil prices continue to spiral out of control, the U.S. is more likely to shift toward direct intervention on the consumer side, with tax cuts and temporary relaxation of fuel formulation standards potentially entering the policy toolkit. Following the conflict, several countries have introduced measures to stabilize oil prices, primarily through price caps and gasoline subsidies. Japan launched a new round of fuel subsidies on March 19, aiming to cap the national average retail gasoline price at 170 yen per liter. South Korea has expanded fuel tax reductions and raised price ceilings.

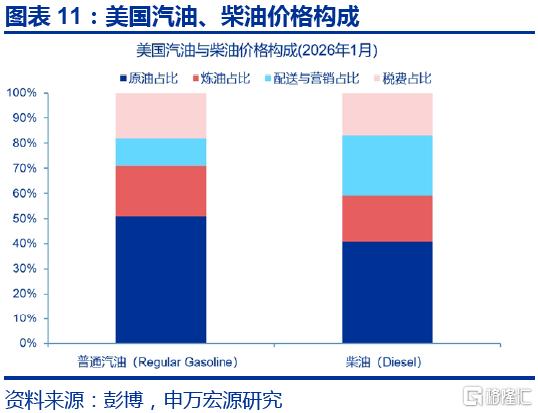

In 2026, crude oil costs accounted for 51% of the U.S. average retail gasoline price, taxes 18%, refining 20%, and distribution and marketing 11%. Tools to reduce domestic gasoline prices can be divided into four categories: lowering crude oil costs, reducing refining costs, cutting distribution costs, and decreasing taxes. Aside from reducing crude oil prices, potential measures the U.S. government might adopt include: 1) Tax relief—temporarily suspending the federal fuel tax, which could directly lower gasoline prices by approximately 18.4 cents per gallon, though congressional approval would be required; 2) Reducing refining costs—easing pollution standards for refineries, which could cut production costs by an average of 0-1 cent per gallon; 3) Relaxing summer gasoline environmental formulation restrictions—allowing E15 (15% ethanol-blended gasoline) and conventional gasoline sales during summer months, with an average impact of 3-10 cents per gallon. Overall, price control tools may more directly lower domestic gasoline prices but are unlikely to alter the global crude oil supply-demand dynamics.

Will Trump TACO again? The decline in crude oil risk premium is limited, making TACO a high-probability option.

Oil prices may struggle to return to pre-conflict levels in the short term, with the decline in risk premium facing three key obstacles. First, negotiations are prone to setbacks, as both sides find it difficult to quickly concede on core issues. Even if a ceasefire agreement is reached, the market may retain expectations of a 'second conflict.' On March 24, ceasefire expectations briefly pushed WTI down to $90. However, on March 25, renewed negotiation challenges caused WTI to rebound to $94, indicating that geopolitical premiums may not fully dissipate. Second, there is a lag in the recovery of physical supply.

Crude oil shipments from the Middle East to refinery processing typically experience a lag of 30-40 days. Even if the conflict ends immediately, full supply restoration may take an additional 1-2 months. Third, the Strait remains an important negotiating lever for Iran, which may enter a new norm of selective passage—retaining influence over shipping while reducing the risk of full-scale conflict with neutral countries.

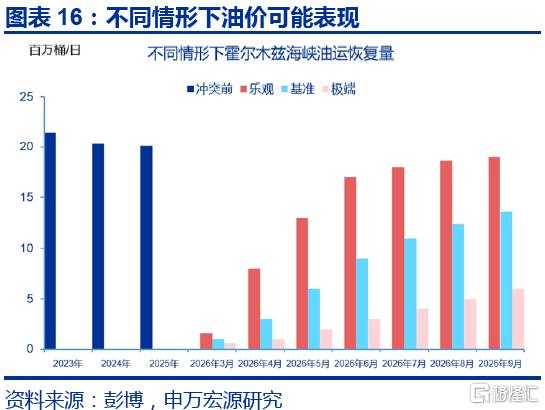

Future oil prices may fluctuate within a range higher than pre-conflict levels but below panic-induced peaks.

In the baseline scenario, the Strait is unlikely to be fully restored, with oil prices higher than pre-conflict levels but lower than the peak. In this scenario, negotiations between the two parties may experience fluctuations, and while the Strait is not completely closed, only selective passage is permitted. Alternative crude oil routes can alleviate some pressure. Crude oil prices remain higher than pre-conflict levels but below the panic peak. Brent crude is projected to reach $108 per barrel by the end of Q2, $97 by the end of Q3, and hover around $85 in Q4. By September, the Strait may restore about 70% of its shipping volume.

In the optimistic scenario, the Strait gradually resumes operations, and risk premiums recede but are unlikely to fully disappear. In this scenario, substantial progress is made in the April ceasefire talks between the US and Iran, with the Strait of Hormuz progressively reopening, and Gulf ports and refineries returning to normal operations. The average price for Q2 remains elevated due to high oil prices from March to early April, but Brent crude may drop to $96 by the end of Q2 and $76 by the end of Q4. By September, the Strait may restore over 90% of its shipping volume.

In the extreme scenario, crude oil prices surge in Q2 but cannot be sustained at high levels for an extended period. In this scenario, the Strait approaches long-term closure, and infrastructure such as ports, oil fields, and power facilities may be targeted. Brent crude prices may spike to around $140 in Q2, but the inability to sustain high prices, coupled with demand destruction and growing recession expectations, could lead to a gradual decline in oil prices. By September, the Strait may only restore approximately 30% of its shipping volume.

There remains a significant probability that Trump will TACO again in the future. TACO essentially represents Trump's marginal concessions on previously hardline policies under rising market pressures. Regarding oil prices, in the event that various measures fail to yield quick results, there is a possibility that Trump may use TACO to suppress oil prices or even make greater concessions. On March 9, Trump stated that the war with Iran was "coming to an end," causing Brent crude to fall by $14.9. On March 23, Trump postponed a plan to strike Iranian power facilities by five days, leading to a $7 drop in Brent crude.

Based on Trump's policy characteristics, this article constructs a TACO Probability Index, yielding a TACO probability ranging from 0% to 100%. The TACO Probability Index has performed exceptionally well in historical backtesting, accurately predicting key concessions since Trump’s second term, including: the reciprocal tariff TACO on April 9, 2025; the reduction of tariffs on China on October 30, 2025; the Greenland TACO on January 23, 2026; and the first Iran-related TACO on March 9. The TACO Probability Index rose to above 90% prior to each of these events. Currently, the TACO index remains at a high of 90%, indicating that despite Trump's administration's tough rhetoric, the likelihood of future concessions remains substantial.

Crude oil prices have become the "anchor" for pricing major asset classes. While the market closely monitors battlefield developments, negotiation prospects, or the impact of the Strait of Hormuz’s navigation on oil prices, it is also important not to overlook the reflexivity of the "oil price-inflation-financial markets-economy" relationship. There may be multiple paths for conflict evolution, but from a macroeconomic and capital markets perspective, they might be summarized into two scenarios: First, if the conflict escalates further, stagflationary pressures on the economy will intensify simultaneously, prompting financial markets to continue risk-off behavior. Financial stress would reinforce "stagnation" and weaken "inflation," eventually crossing a critical threshold to shift the market into "recession trading," thereby suppressing the oil price center and creating conditions for the Fed to "pivot dovish." Second, if the conflict unexpectedly eases, the geopolitical risk premium for crude oil may rapidly narrow, but supply-demand gaps will still keep the oil price center elevated. Considering that oil prices were higher in early 2025 and lower later, even if the oil price center falls to around $80 per barrel by the end of 2026, the year-on-year increase would still be as high as 27% (with the average Brent crude price in December 2025 being $63 per barrel). Therefore, Fed policy may act as a medium-term constraint.

Risk Warning

1. Escalation of geopolitical conflicts. The Russia-Ukraine conflict has yet to conclude, and geopolitical tensions may intensify volatility in crude oil prices, disrupting the global disinflation process and expectations for a soft landing.

2. U.S. economic slowdown exceeds expectations. Attention should be paid to the risks of weakening employment and consumption in the United States.

3. The Federal Reserve shifts to a more hawkish stance than expected. If U.S. inflation demonstrates greater persistence, it could impact the pace of future interest rate cuts by the Federal Reserve.

Editor/Melody