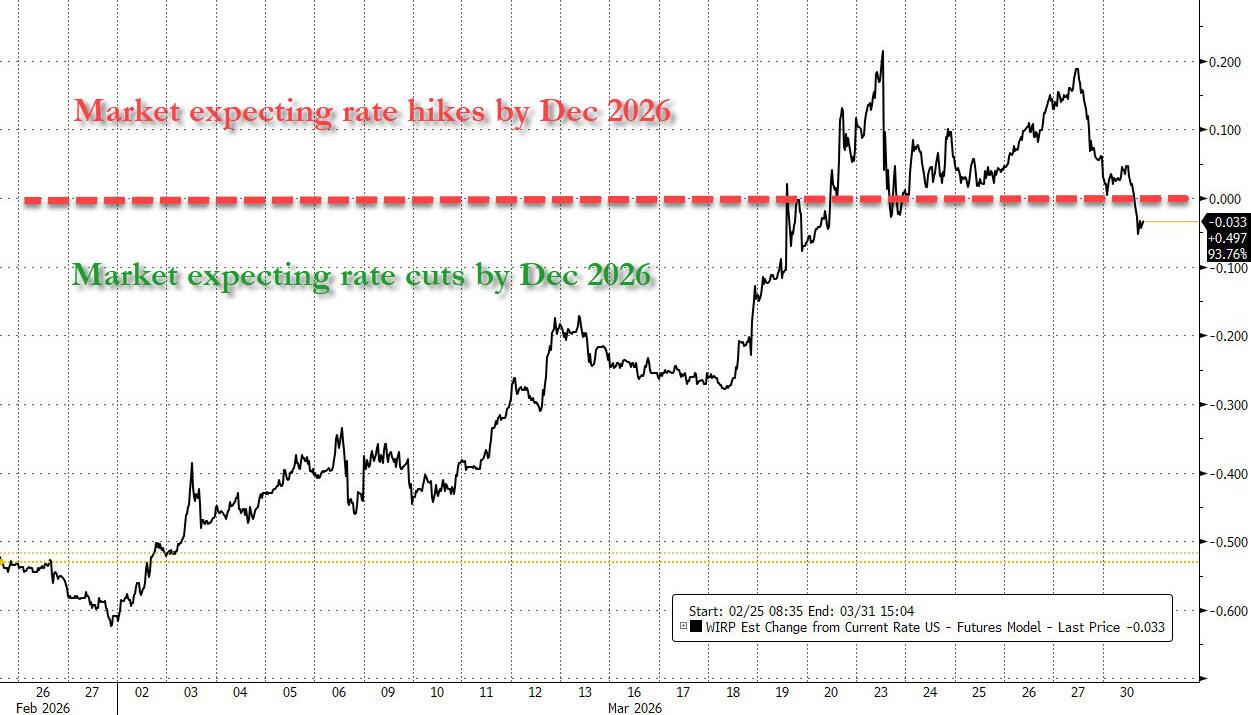

①At the beginning of last week, it was a foregone conclusion in the futures market that interest rates would rise before the end of the year, and this view was still considered highly likely until last Friday; ②However, on Monday, sentiment underwent a dramatic shift, to the point where traders once believed there was a 20% chance of a rate cut by the end of the year.

The U.S. Treasury market rebounded on Monday (March 30) from its worst sell-off in 17 months as traders unwound bets on interest rate hikes by the Federal Reserve, with market focus shifting to speculation that a potential U.S.-Iran conflict could exacerbate a global economic slowdown.

Federal Reserve Chair Powell stated on Monday that against the backdrop of the energy shock caused by the U.S.-Israel conflict with Iran, the Fed is inclined to maintain interest rates unchanged and temporarily 'ignore' the impact of this shock. These remarks further fueled the rally in the bond market. Many industry insiders noted that Powell's speech at Harvard University alleviated market concerns that the Fed would be forced to tighten monetary policy to curb accelerating inflation, prompting traders to re-price the slight possibility of a rate cut this year.

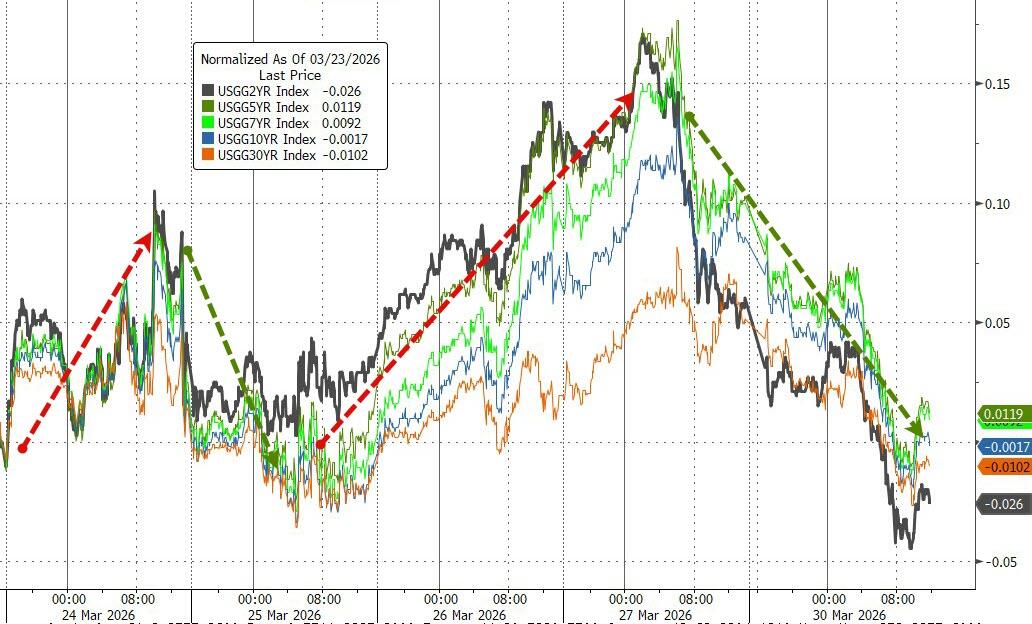

This shift in stance once caused short-term U.S. Treasury yields to fall more than 10 basis points during the session, before paring some losses. By the close of the New York trading session, U.S. Treasury yields fell across the board, with the 2-year yield down 8.19 basis points to 3.830%, the 5-year yield falling 8.21 basis points to 3.986%, the 10-year yield declining 7.76 basis points to 4.350%, and the 30-year yield dropping 5.35 basis points to 4.913%.

This shift in stance once caused short-term U.S. Treasury yields to fall more than 10 basis points during the session, before paring some losses. By the close of the New York trading session, U.S. Treasury yields fell across the board, with the 2-year yield down 8.19 basis points to 3.830%, the 5-year yield falling 8.21 basis points to 3.986%, the 10-year yield declining 7.76 basis points to 4.350%, and the 30-year yield dropping 5.35 basis points to 4.913%.

It is worth noting that the rebound in U.S. Treasury prices on Monday also marked the second consecutive day that yields fell alongside rising oil prices. This contrasted with much of March, when Treasury yields climbed amid surging energy prices as markets worried that the Iran war could trigger higher inflation.

The market has shifted from worrying about inflation to worrying about the economy.

In this regard, analysts pointed out that this round of bond market rebound reflects growing market anxiety that the conflict erupting in the Middle East will hit the U.S. economy, as rising fuel costs have pushed up costs for businesses and consumers, slowing U.S. job growth.

“Before last Friday, investors seemed more focused on the inflationary impact of rising oil prices, so they began pricing in expectations of a Federal Reserve rate hike, pushing up Treasury yields,” said John Briggs, head of U.S. interest rate strategy at Natixis. “Then, sentiment shifted, and despite higher oil prices, the focus of concern turned to economic growth.”

This marks a significant shift for the bond market, where concerns about an inflation shock—which would tie the central bank’s hands—largely overshadowed worries about economic growth.

Gennadiy Goldberg, head of U.S. interest rate strategy at TD Securities, said, “The market is uncertain how to respond to recent geopolitical events—whether it should focus on first-order inflation impacts or second-order economic growth effects.” Not only is the geopolitical situation full of uncertainties, but the market is also undecided on how the Fed will respond to these developments.

As shown in the chart below, it was considered a foregone conclusion in the futures market early last week that interest rates would rise before the end of the year, and this remained highly likely until Friday. However, on Monday, sentiment shifted dramatically, leading traders to briefly believe there was a 20% chance of a rate cut by year-end.

Recession risks cannot be ignored.

Some large U.S. bond funds, including PIMCO, had previously warned that financial markets were underestimating the risks of an economic slowdown as inflation concerns intensified. Goldman Sachs also stated that the probability of the U.S. economy falling into a recession within the next year has risen to about 30%.

Currently, the U.S.-Iran conflict has entered its fifth week, with no signs of abating even after the U.S. extended the deadline for Iran to agree to reopen the Strait of Hormuz. This has led to Brent crude, the international benchmark, hovering above $110 per barrel on Monday, while U.S. WTI crude broke through the $100 mark for the first time since 2022.

Although Trump earlier posted on social media that the U.S. government was engaged in "serious consultations" with the Iranian regime, he also reiterated the threat to attack Iran's oil and electricity infrastructure if no agreement is reached. Meanwhile, Iran has consistently indicated that peace talks have not made progress and suggested its ability to sustain the conflict for a longer period, increasing the risk of a protracted conflict that could disrupt key energy supplies to most parts of the world.

Jim Barnes, head of fixed income at Bryn Mawr Trust, said that the conflict situation does not seem to have improved significantly. "Investors originally thought that since the war has lasted this long, we should be closer to the end, but reality suggests otherwise. This has led investors to reconsider incorporating a longer-term perspective, which, given the current situation, is what is driving yields lower."

"U.S. Treasury markets rallied Monday morning as investors focused on the potential risks to global economic growth posed by the situation in the Middle East, rather than trading the conflict purely from the perspective of an inflation shock," said Ian Lyngen, head of U.S. interest rate strategy at BMO Capital Markets.

Stan Shipley, a fixed-income strategist at Evercore ISI, said, "Over the past two months, the U.S. Treasury market has been too narrowly focused on inflation, and now people are beginning to worry that if oil prices rise high enough, the economy will fall into a recession. This is good news for the U.S. Treasury market."

Editor/Doris