As the conflict in Iran enters its second month and oil prices surpass $100 per barrel, U.S. Treasury yields have moved inversely lower, signaling a key decoupling between bonds and oil. Market logic has shifted from inflation fears to concerns about recession and expectations of fiscal stimulus. Goldman Sachs predicts that bond yields will ultimately trend downward, while Morgan Stanley points out that the market is pricing in fiscal stimulus following an energy shock.

As the conflict in Iran enters its second month, the market is shifting from short-term inflation fears to forward-looking pricing of fiscal stimulus.

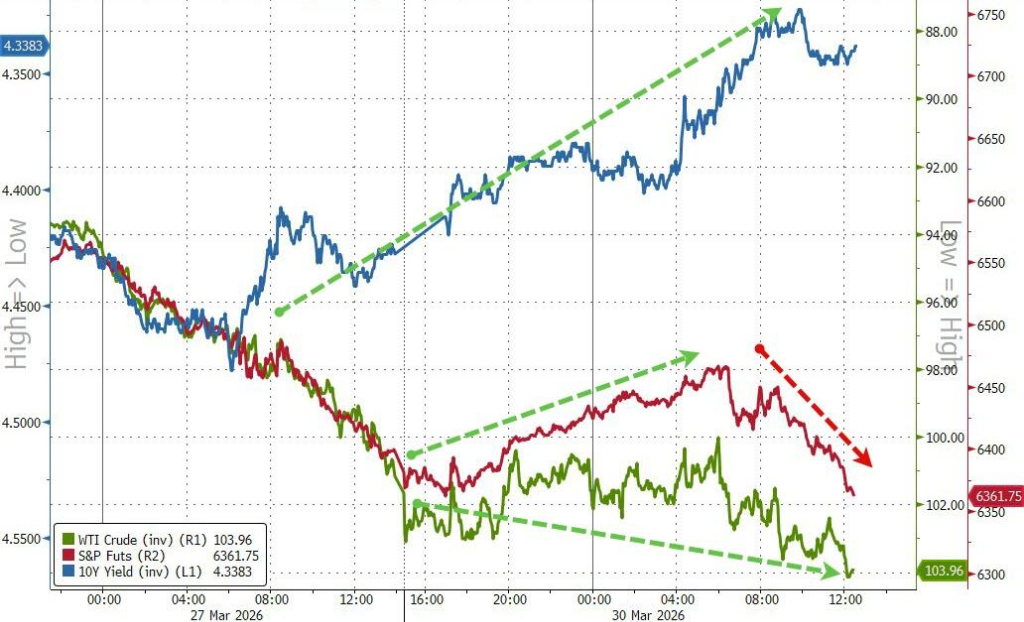

On Monday, as $Crude Oil Futures (MAY6) (CLmain.US)$ crude oil surged above $100 per barrel, U.S. Treasury yields unexpectedly moved in the opposite direction, $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ falling nearly 8 basis points to 4.348%.

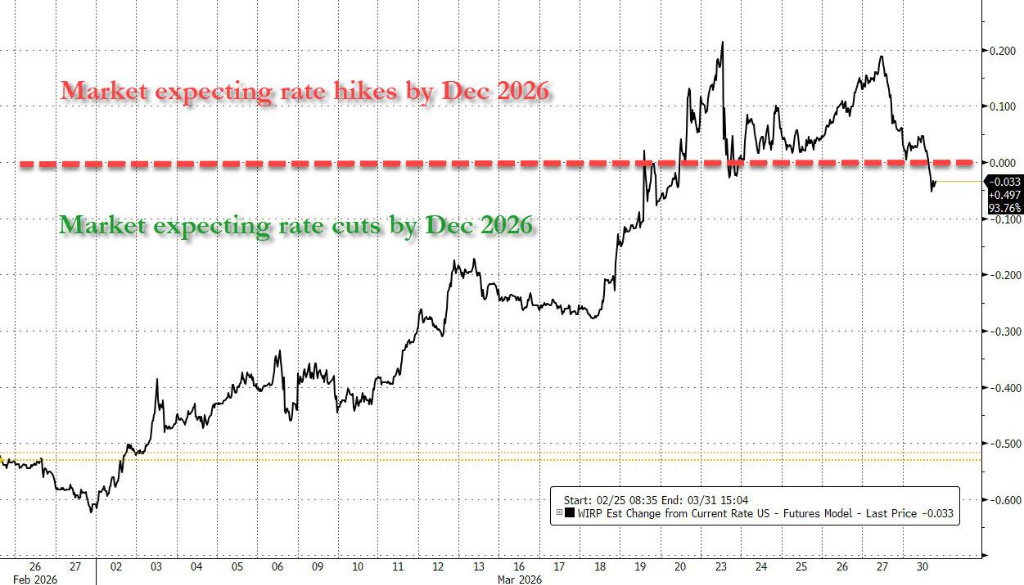

Market pricing shifted simultaneously. The money market reduced the probability of a Federal Reserve rate hike in 2026 from about 35% on Friday to around 20%, while repricing expectations for mild interest rate cuts within the year.

Market pricing shifted simultaneously. The money market reduced the probability of a Federal Reserve rate hike in 2026 from about 35% on Friday to around 20%, while repricing expectations for mild interest rate cuts within the year.

This 'decoupling' trend marks a shift in the market from short-term inflation fears to concerns about a mid-term economic recession, as well as preemptive positioning for the next round of fiscal stimulus.

Goldman Sachs analyst Chris Hussey pointed out that the core of the market this week remains the tug-of-war between growth and inflation:

On the inflation side, prices of crude oil, natural gas, aluminum, and derivatives have spiraled upward, threatening to spill over globally, particularly into Asia.

On the growth side, the persistent uncertainty in the Middle East, coupled with energy price shocks, has dimmed the outlook for labor demand.

Although the short-term trajectory may still be complex, Goldman Sachs' assessment is that bond yields will eventually decline and long-term stock market volatility will rise across various scenarios, leading to 'growth panic' rather than 'persistent inflation panic.'

Matthew Hornbach, Chief Interest Rate Strategist at Morgan Stanley, went further to suggest that the U.S. interest rate market may increasingly reflect an expectation that fiscal stimulus will follow after energy-driven demand destruction.

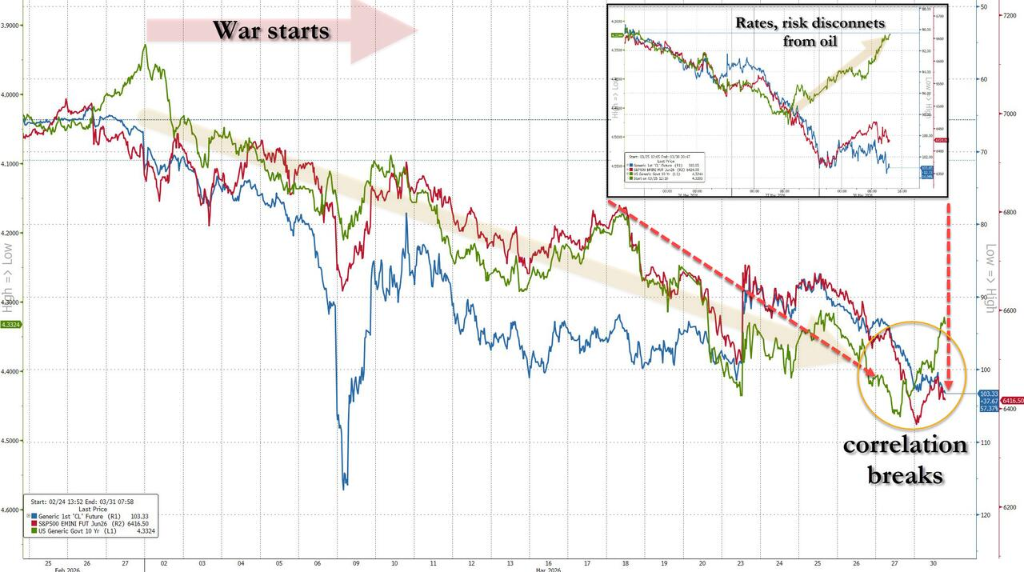

Decoupling of correlations: divergence between bond and oil market trends

Since the outbreak of the Iran conflict, the market's pricing logic has been quite singular: go long on energy and short everything else.

However, cracks have emerged over the past week. Despite the surge in energy prices, long-term inflation expectations have hardly moved significantly. As measured by five-year inflation swaps, the market’s expectations for inflation over the next five years have fallen by about 20 basis points from their January peak, retreating to levels seen during last April’s period of turmoil.

Francisco Simón, Head of European Strategy at Santander Asset Management, stated:

Although inflation remains a latent concern, the potential drag on growth and confidence should begin to form a hedge, limiting further upside in yields.

He added that the bond market is currently one of the clearest tools for pricing the macroeconomic impact of the conflict.

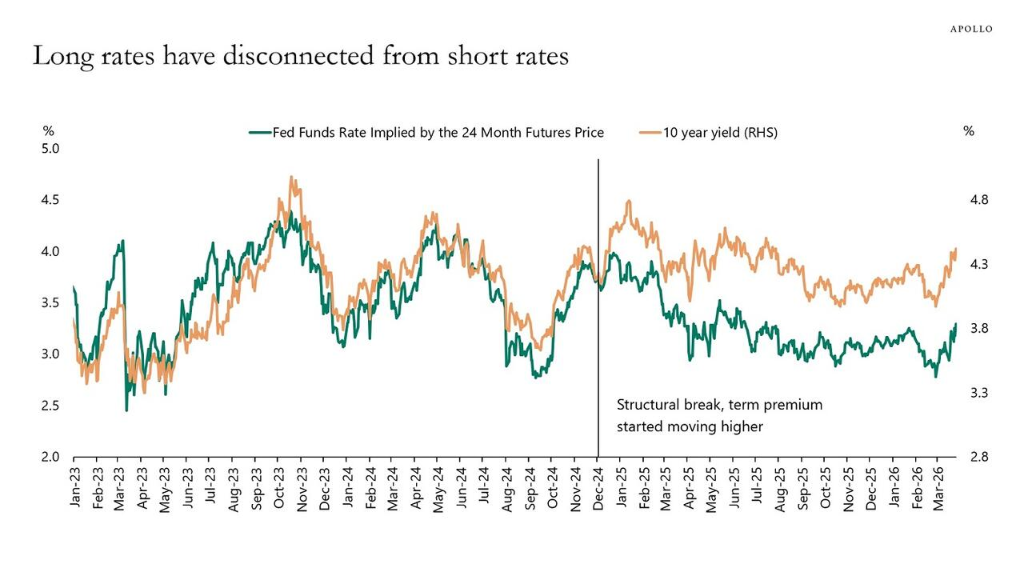

Torsten Slok, Chief Economist at Apollo, also pointed out that there is a noticeable premium embedded in the current 10-year rate. Under normal Federal Reserve expectations, the 10-year rate should be around 3.9%, not the current 4.4%, implying an "excess premium" of approximately 55 basis points.

The sources of this premium may include fiscal concerns, quantitative tightening, reduced foreign demand, and doubts about the independence of the Federal Reserve. Slok remarked:

Investors need to seriously consider what these 55 basis points really signify.

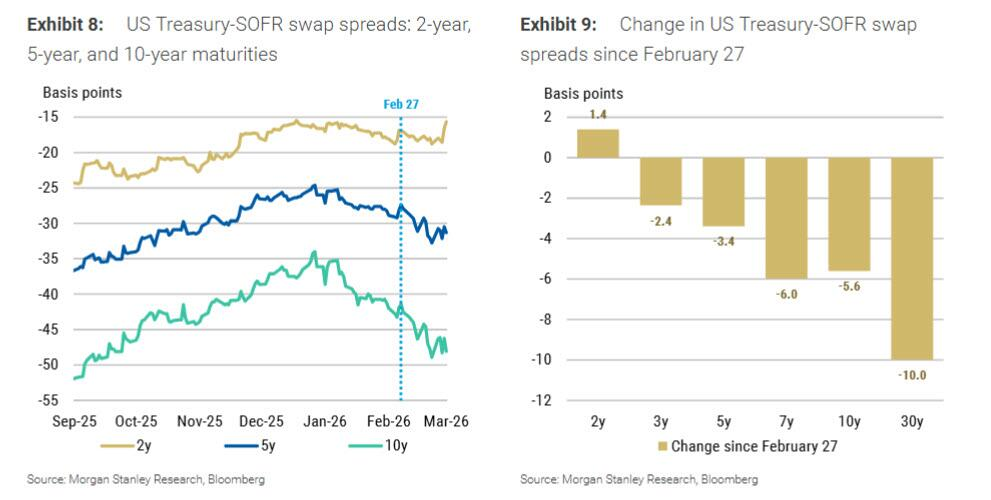

Meanwhile, U.S. Treasuries have continued to underperform relative to SOFR swaps since February 27, with even 2-year Treasury notes starting to lag behind SOFR swaps, suggesting the market is already pricing in the risk of increased Treasury supply.

The true pricing in the bond market reflects fiscal stimulus, not monetary easing.

Hornbach of Morgan Stanley proposed a deeper interpretive framework in the report.

He believes that the current pricing logic in the U.S. bond market may no longer merely reflect the path of monetary policy but is instead anticipating the fiscal response by the government to energy shocks.

From a historical perspective, the COVID-19 pandemic has profoundly altered investors' perceptions of crisis-response mechanisms.

Before the pandemic, markets assumed that the primary tool for addressing crises came from central banks; now, however, investors seem to believe that the main force for addressing growth crises has shifted to government fiscal measures, while central bank responses are constrained by persistent inflationary pressures.

Regarding the current situation, Hornbach pointed out that if investors are indeed pricing in a fiscal stimulus significant enough to force the Federal Reserve to pivot, its scale must far exceed the supplementary military appropriations related to the conflict with Iran and must address the private sector most severely impacted by rising energy costs.

Morgan Stanley’s public policy strategists believe that the political bargaining path for supplementary appropriations is already fraught with challenges, and whether additional stimulus measures can be implemented largely depends on the duration of the conflict.

There are precedents. The Spanish government has proposed an energy price relief plan totaling 5 billion euros, encompassing VAT reductions and subsidies, while the Portuguese government has enacted legislation allowing for temporary electricity price caps during energy crises.

Potential risks of Gulf states selling U.S. Treasuries

Amid heightened expectations of fiscal stimulus, a potential hedging risk is emerging.

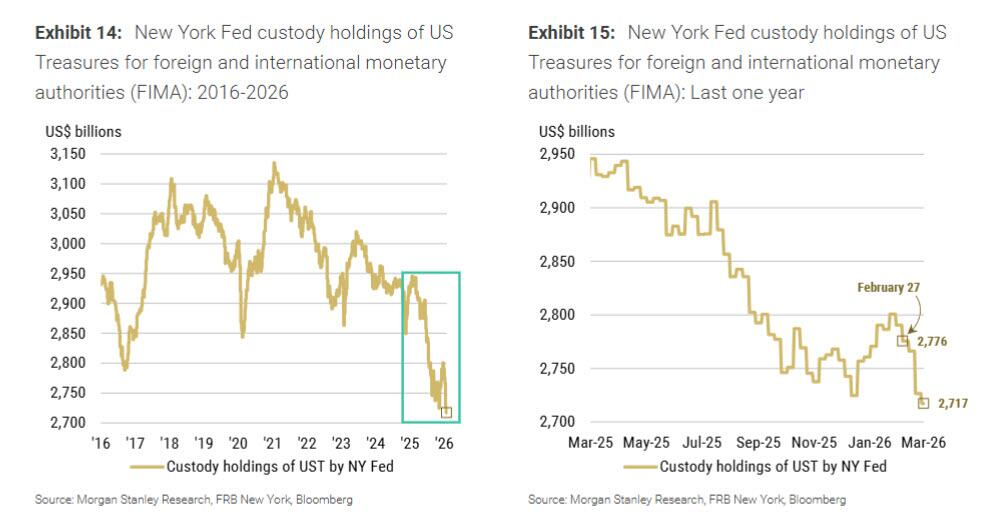

Data from Morgan Stanley shows that holdings of foreign official institutions in the New York Fed's custodial accounts have decreased by approximately $58 billion since February 25, while the reverse repurchase accounts (FIMA RRP) of foreign currency authorities have only increased by about $3 billion during the same period, implying that proceeds from related sales may have been repatriated rather than retained within the dollar system.

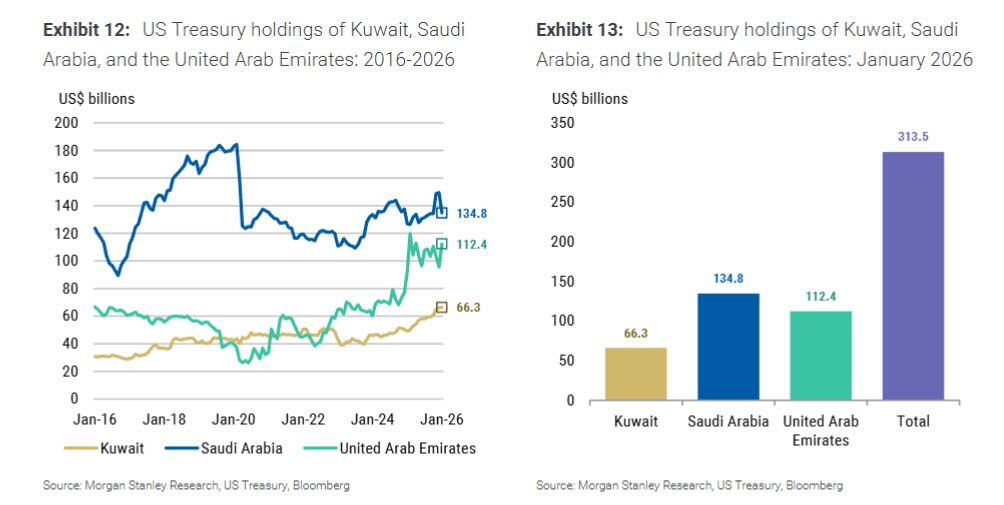

Kuwait, Saudi Arabia, and the UAE collectively held approximately $313 billion in U.S. Treasury bonds in January this year, with their holdings having increased since 2022.

Against the backdrop of ongoing conflict, whether more Gulf nations will reduce their holdings of U.S. Treasuries to cope with domestic military and economic pressures remains highly uncertain. This variable, combined with expectations of fiscal stimulus, creates a current dilemma for the bond market.

On one hand, expectations of fiscal stimulus are depressing yields.

On the other hand, potential continued selling pressure from Gulf nations could push long-term yields higher again and, in the event of prolonged U.S. Treasury selloffs, force the Federal Reserve to act more quickly.

Hornbach admitted that it remains unclear how this contradiction will ultimately be resolved. However, the recent synchronized sharp rise in gold, precious metals, and crypto-assets clearly indicates that the market is actively positioning itself for one of the aforementioned scenarios.

Editor/Doris