①No borrower worldwide can escape the surge in market interest rates triggered by the Middle East war and the resulting energy supply shock; ②For U.S. tech companies planning to invest over $600 billion in the artificial intelligence arms race this year, the sharp rise in borrowing costs may come at an especially inopportune time...

No borrower worldwide can escape the surge in market interest rates triggered by the Middle East conflict and its resulting energy supply shock. For U.S. technology companies planning to invest over $600 billion this year in the artificial intelligence arms race, the sharp rise in borrowing costs could not have come at a worse time.

The surge in artificial intelligence capital expenditure is unprecedented. Tech giants are expected to allocate $630 billion in capital expenditure this year, primarily directed toward artificial intelligence data centers, chips, and cloud computing, a figure exceeding 2% of U.S. GDP; next year’s projected spending will exceed $800 billion, approaching 3% of GDP.

Admittedly, U.S. tech giants have historically funded expansions with cash, and they still hold substantial reserves: some estimates indicate that the combined cash and equivalents held by the five largest 'hyperscalers' exceeds $350 billion. This partly explains why Apple and Microsoft still enjoy credit ratings higher than that of the U.S. government.

Admittedly, U.S. tech giants have historically funded expansions with cash, and they still hold substantial reserves: some estimates indicate that the combined cash and equivalents held by the five largest 'hyperscalers' exceeds $350 billion. This partly explains why Apple and Microsoft still enjoy credit ratings higher than that of the U.S. government.

However, they are also rapidly depleting these cash reserves.

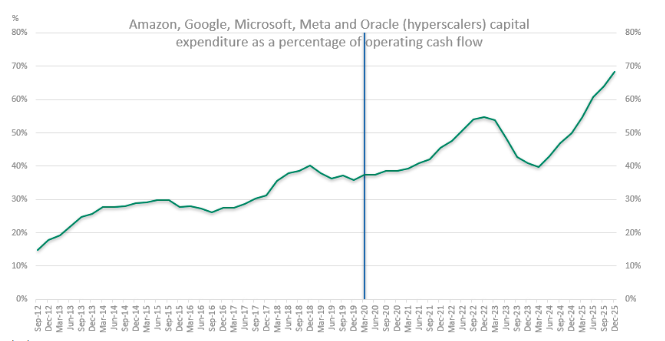

According to Apollo Global Management, as of the end of last year, approximately 60% of the operating cash flow of these AI-focused companies was allocated to capital expenditures—this ratio may now be nearing 70%. At this rate, it won’t be long before every dollar earned by these AI giants is designated for capital expenditure.

Analysts at Morgan Stanley stated that cumulative capital expenditure by tech giants over the next two years is expected to reach approximately $1.4 trillion, nearly 90% of the projected $1.6 trillion in operating cash flow.

As a result, tech giants will increasingly turn to credit markets. Analysts at Bank of America estimate that total debt issuance by hyperscalers this year will reach $175 billion, up from $121 billion last year, more than six times the annual average of $28 billion over the previous five years.

On a broader scale, borrowing across the entire industry is even larger. Analysts at Mitsubishi UFJ Financial Group estimate that investment-grade bond issuance by technology and artificial intelligence companies last year totaled $245 billion—a figure not far from the cumulative $298 billion over the previous decade.

AI concept stocks start to face pressure

Despite many industry insiders still firmly believing that tech giants are relatively capable of withstanding external shocks such as geopolitical conflicts. For instance, according to Capital Economics, since the outbreak of the Middle East war four weeks ago, the growth expectations for earnings in the technology sector have outpaced those of any other sector, including energy.

However, it is undeniable that after several years of substantial increases driven by the AI boom, technology stocks now appear particularly vulnerable, as concerns about excessive spending and overvaluation were raised at the beginning of the year. Some investors clearly have doubts about whether current AI-related investments and borrowings can generate sufficient returns.

In fact, as concerns grow over the impact of an Iran war on potential oil supply disruptions, investors in the U.S. stock market have recently shifted towards defensive stocks. This has led to a decline in some technology stocks, represented by chipmakers, which have started to lead losses in the U.S. equity market.

Billy Leung, investment strategist at Global X Management, stated, 'Rising oil prices and continued volatility in interest rates are driving a broader trend of risk aversion, with investors selling off crowded trades in growth and artificial intelligence sectors.'

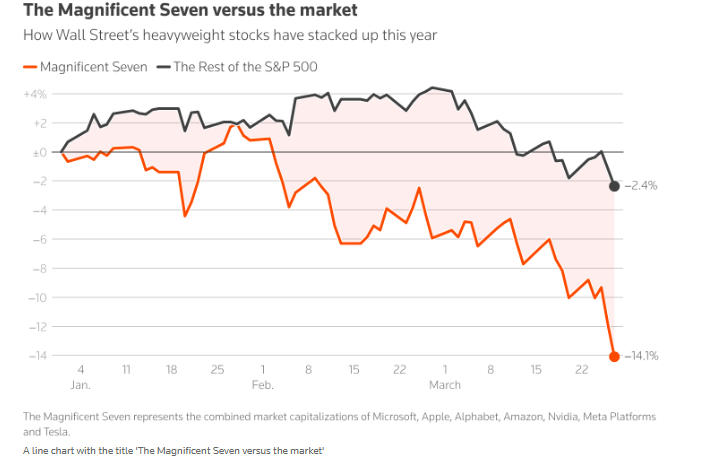

Market data shows that Roundhill's ETF tracking the 'Magnificent Seven' fell 5% last week, bringing its monthly decline to approximately 10%, with a nearly 20% drop since the October high last year.

Jim McCormick, Chief Global Macro Strategist at Citigroup, stated that the early belief that the technology sector would remain unaffected was incorrect. The market has now realized, 'We are facing a world of persistently rising yields and energy costs, which is unfavorable for the AI industry.'

Let’s take a look at the soaring borrowing costs worldwide.

While stock prices fluctuate dramatically, more concerning is the rise in borrowing costs, which will add additional pressure to the balance sheets of major AI companies leveraging debt to finance their AI projects. Meanwhile, the scale of massive investments will make achieving incremental profits per dollar increasingly difficult. If market interest rates continue to rise, this pessimism will only intensify.

This month, the yield on the 10-year U.S. Treasury bond has risen by approximately 40 basis points, marking the largest monthly increase since October 2024.

Similar surges in yields are also occurring in Europe and Japan. The yield on Italy’s 10-year government bond rose to 4.14% at one point this month, with the cumulative increase reaching about 80 basis points at its peak, matching the scale of sell-offs during the previous round of the energy crisis in 2022. Japan’s 10-year government bond yield also hit 2.39% on Monday, the highest since February 1999, while the 40-year yield briefly touched 4.02%.

Despite the aforementioned turmoil in the government bond market, it has not yet triggered significant repercussions in the investment-grade corporate bond market — the widening of spreads during the same period was a relatively moderate 15 basis points. However, this situation may change.

Tech giants face a potential double whammy: on one hand, higher interest rates and growing debt burdens; on the other, the prospect of squeezed profits and falling stock prices.

For the broader market and economy, given these companies' central role in overall U.S. earnings and growth, the implications could be even more significant.

If the tech giants' staggering capital expenditure spree — one of the largest collective investments in a single industry in history — ultimately comes to fruition, it would indeed be difficult for the U.S. economy to fall into a recession. However, if rising bond yields and falling stock prices hinder these plans, the resulting 'perfect storm' of escalating inflation, tighter borrowing costs, and an already sluggish job market might be more than the U.S. economy can bear.

Editor/Rice