As the financial markets, battered by various shocks, enter the second quarter, the shadow of regional conflict-related news continues to loom over the global landscape. This backdrop may drive stock markets to further lows, while significant sell-offs in the bond market could attract buyers to re-enter.

As the financial markets, battered by various shocks, enter the second quarter, the shadow of regional conflict-related news continues to loom over the global landscape. This backdrop may drive stock markets to further lows, while significant sell-offs in the bond market could attract buyers to re-enter.

Investors generally believe that even if the conflict is resolved and short-term market sentiment receives a boost, the damage to Middle Eastern energy infrastructure and persistently high oil prices will still weigh on economic growth and drive up inflation. Against this backdrop, equities are likely to undergo further corrections; if the conflict escalates further, concerns over economic growth may overshadow inflation anxieties, potentially leading to a recovery in the bond market.

Seema Shah, Chief Global Strategist at Principal Asset Management, which oversees approximately $594 billion in assets, stated: 'When the market is filled with noise, it’s hard to cut through the fog and discern direction. We have consistently advised increasing allocation to international equities, a rationale that remains valid, but that doesn’t mean completely exiting the U.S. market.'

Seema Shah, Chief Global Strategist at Principal Asset Management, which oversees approximately $594 billion in assets, stated: 'When the market is filled with noise, it’s hard to cut through the fog and discern direction. We have consistently advised increasing allocation to international equities, a rationale that remains valid, but that doesn’t mean completely exiting the U.S. market.'

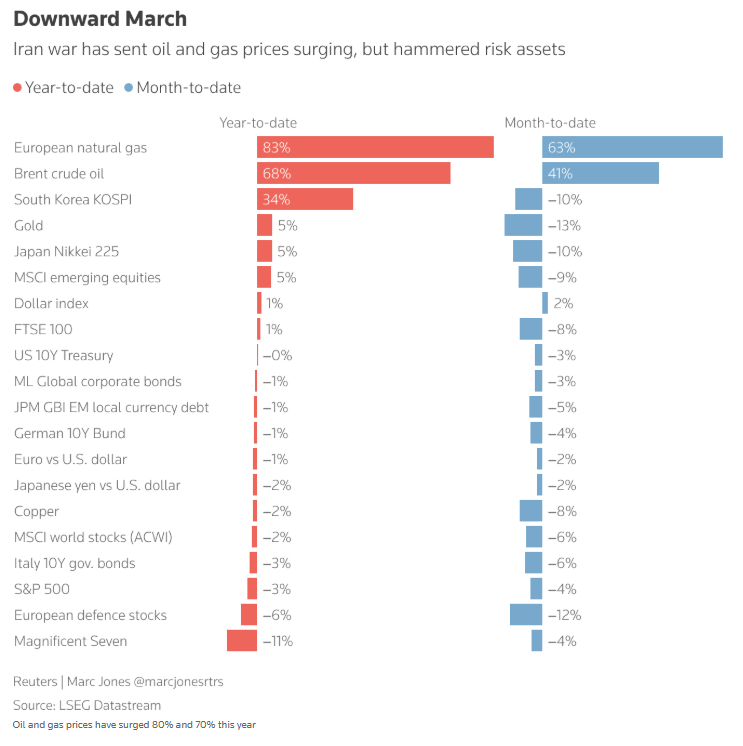

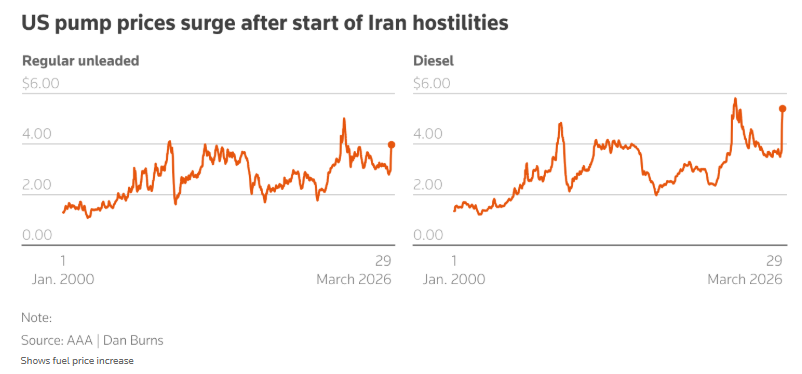

A turbulent first quarter kicked off with conflicts in the Middle East, further roiled by Trump's intervention in Venezuela, threats related to Greenland, and dramatic disruptions from advancements in artificial intelligence (AI) technology. Crude oil emerged as the standout asset of the quarter, with prices surging about 90% to surpass the $100-per-barrel mark. This move caught bond investors off guard, leading to a sharp rise in expectations for interest rate hikes.

Analysts surveyed predict that as long as the current supply disruptions persist, oil prices will fluctuate between $100 and $190 per barrel, with an average forecast of $134.62. Data from the online prediction market Polymarket shows a 36% probability of the war ending by mid-May and a 60% chance of it concluding by the end of June.

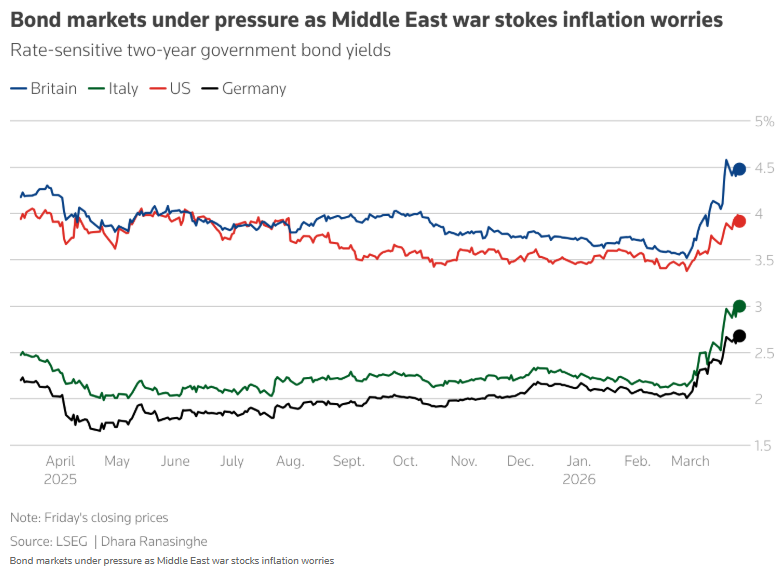

Similar to the inflation surge seen in 2022, short-term borrowing costs in the UK and Italy each spiked by 75 basis points this quarter, while significant volatility was also observed in the U.S., German, and Japanese bond markets.

Manish Kabra, Multi-Asset Strategist at Societe Generale, noted: 'Looking back at past oil shocks, only two factors matter: the duration of the shock and the central banks' response, which determines overall risk appetite.'

Following the outbreak of the Iran conflict, traders have fully ruled out the possibility of the Federal Reserve cutting interest rates within the year; Eurozone markets now expect three rate hikes, while the UK is expected to raise rates at least twice, reversing previous expectations of rate cuts in these economies. The monetary easing process in emerging markets has also been interrupted as a result.

Kabra believes that the Memorial Day weekend in May in the U.S. could become a focal point for markets—it marks the start of the summer travel season when consumers might pressure policymakers to control energy costs. Following the outbreak of hostilities, he raised his commodities allocation from 10% pre-conflict to 15%, reflecting the increasingly tight correlation between geopolitics and commodities.

Under pressure, the bond market may soon be followed by equities.

In the bond market, investors previously sold off heavily in response to expectations of rising inflation and interest rates, causing bond prices to plummet and yields to soar. However, some investors have begun to focus on opportunities following the market's correction.

Francesco Sandrini, Head of Multi-Asset Strategy at Amundi, stated that the institution has increased its allocation to short-term eurozone government bonds and maintained exposure to 5-year U.S. Treasuries, based on the rationale that once a resolution to the crisis emerges, fixed-income assets are likely to perform well. 'In short, we expect central banks to attempt to overlook short-term price pressures.'

Paul Eitelman, Global Chief Investment Strategist at Russell Investments, noted that compared to several months ago, bonds have become significantly more attractive, and he believes the dollar's strength is unlikely to be sustained in the medium term. In March, the dollar once again demonstrated its safe-haven characteristics, rising over 2%. Analysts pointed out that prior to the conflict, investors had shifted from U.S. assets to other markets, pressuring the dollar; should the conflict end, this trend could re-emerge.

At the same time,$XAU/USD (XAUUSD.CFD)$ Prices fell by 4% in March. Although safe-haven assets typically rise amid heightened inflation concerns, gold prices weakened as investors liquidated profitable positions to offset losses in other assets.

Thanks to strong earnings and a tech stock boom, equity markets had previously performed relatively robustly, but recent selling pressure has notably intensified. $S&P 500 Index (.SPX.US)$ The Stoxx Europe 600 Index has declined by 9%-10% from its recent historical peak, while Japan’s Nikkei index has fallen nearly 13% from its February all-time high.

Guy Miller, Chief Market Strategist at Zurich Insurance Group, stated that with the deteriorating economic outlook, he has reduced his equity position from an 'overweight' stance before the conflict to an 'underweight' position.

U.S. consumer confidence in March dropped more than expected, and German investor confidence deteriorated sharply. S&P Global’s March Purchasing Managers' Index (PMI), a forward-looking indicator of business activity for both the Eurozone and the U.S., hit multi-month lows. Analysts believe that although the U.S. economy is relatively resilient and is an energy exporter, if the conflict continues to push energy prices higher, the U.S. economy will still be impacted. The OECD warned last Thursday that the global economy has deviated from its originally stronger growth trajectory.

Miller of Zurich Insurance emphasized: 'This conflict is different from the geopolitical and political突发事件 we have experienced over the past year. Those earlier events had minimal impact on corporate profits, profit margins, and market valuations.'

Editor/KOKO