Morgan Stanley believes that Meta's current valuation of approximately 15 times earnings is at a decade-low level, trading at a discount of over 50% compared to its peers. Beyond cost-cutting measures such as layoffs, its core growth driver lies in the potential AI-powered product MetaClaw: This tool leverages the Llama large model and 3.5 billion active users to create a closed-loop 'agent-based shopping' experience by integrating merchant inventory and payment capabilities, which could shift Meta from ad display to transaction monetization.

Morgan Stanley believes that the market is…$Meta Platforms (META.US)$Morgan Stanley believes that market pessimism toward Meta has bottomed out, and the current valuation creates a rare tactical buying opportunity, while also listing it as a top pick.

In the latest research report released on March 29, Morgan Stanley analyst Brian Nowak maintained an overweight rating for Meta Platforms, lowering the target price from $825 to $775, which still represents an upside of approximately 50% from the current share price of around $526.

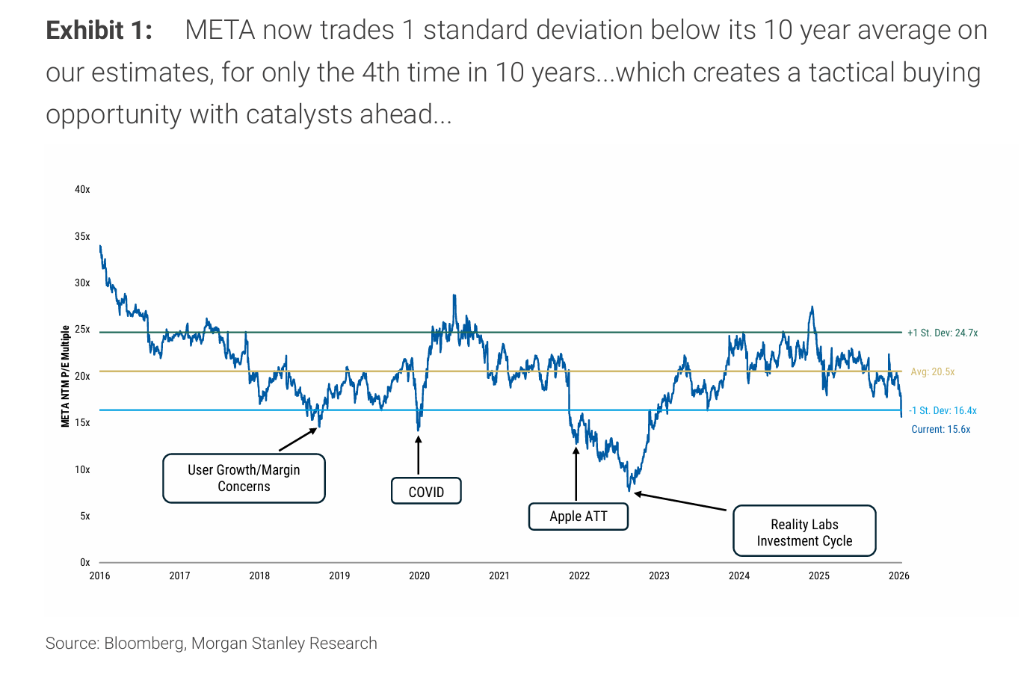

The report noted that due to concerns over GenAI investment returns, macroeconomic uncertainties, and regulatory shadows, Meta is currently trading at a valuation of approximately 15 times the expected earnings per share for 2027, which is 1 standard deviation below its 10-year average. This marks the fourth time such an undervaluation has occurred in the past decade. This position, combined with expectations of the company’s potential AI agent product rollout, forms the core logic behind Morgan Stanley’s bullish stance on Meta. Additionally, Meta is advancing a plan to reduce its workforce by about 20%, which Morgan Stanley estimates could save $3 billion to $10 billion annually, thereby contributing more than $1 to earnings per share (EPS) by 2027, providing a higher bottom support for EPS during reinvestment cycles.

The report noted that due to concerns over GenAI investment returns, macroeconomic uncertainties, and regulatory shadows, Meta is currently trading at a valuation of approximately 15 times the expected earnings per share for 2027, which is 1 standard deviation below its 10-year average. This marks the fourth time such an undervaluation has occurred in the past decade. This position, combined with expectations of the company’s potential AI agent product rollout, forms the core logic behind Morgan Stanley’s bullish stance on Meta. Additionally, Meta is advancing a plan to reduce its workforce by about 20%, which Morgan Stanley estimates could save $3 billion to $10 billion annually, thereby contributing more than $1 to earnings per share (EPS) by 2027, providing a higher bottom support for EPS during reinvestment cycles.

Meta’s core growth driver lies in the potential AI agent product MetaClaw: this tool leverages the Llama large model and 3.5 billion active users, integrating merchant inventory and payment capabilities to create a 'proxy shopping' closed loop, which is expected to push Meta from ad display toward transaction monetization. Morgan Stanley also slightly reduced its advertising revenue forecasts for 2026 and 2027 by about 1% each to reflect conservative macro assumptions, but even so, the expected EPS for 2027 remains at $36.31, preserving significant upside potential.

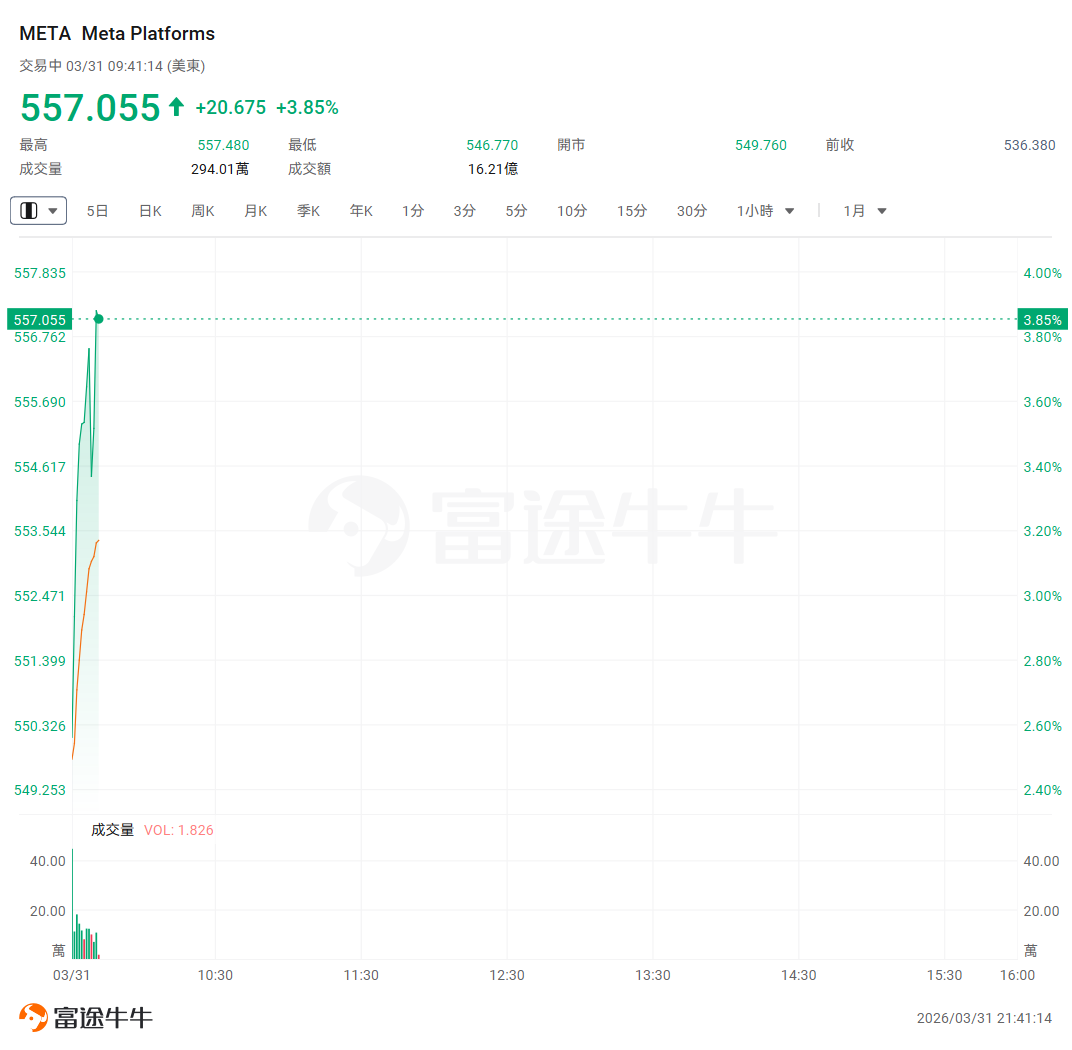

As of now, $Meta Platforms (META.US)$The stock surged nearly 4% at the opening.

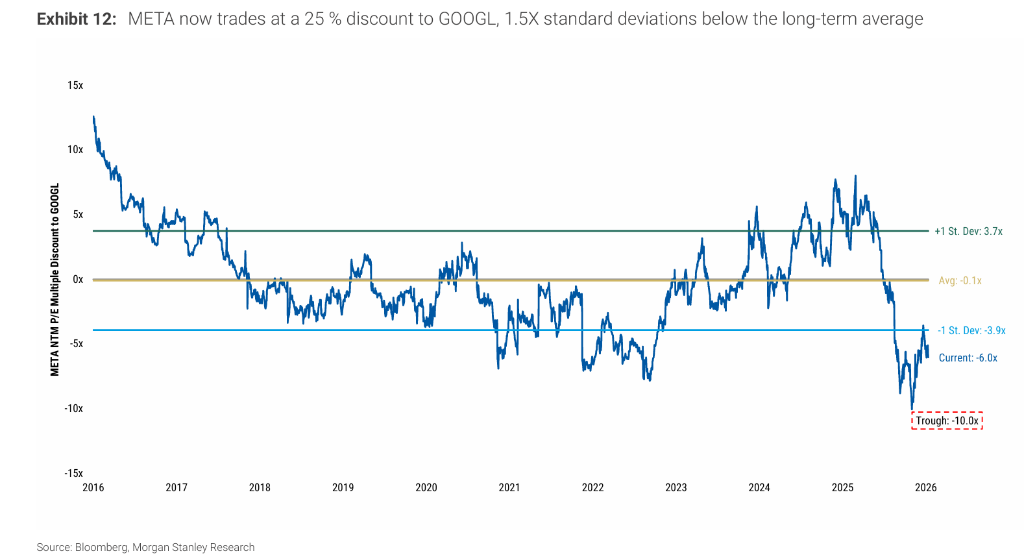

Valuation Bottom: Discount Reaches Rare Decade-Low Levels

Meta’s current valuation level is already in a significant discount range compared to other large-cap tech stocks covered by Morgan Stanley.

From a longitudinal perspective, Meta’s forward price-to-earnings ratio is approximately 15 times, lower than its 10-year average of 20.5 times and further breaking below the 1-standard-deviation lower bound of 16.4 times. This has only occurred four times in the past decade, including during the 2018 user growth and margin crisis, the impact of Apple’s ATT privacy policy, and the revaluation triggered by the Reality Labs investment cycle.

From a cross-sectional perspective, Meta’s 2027 PEG valuation is approximately 0.9 times, while the median PEG for Apple, Microsoft, Alphabet, Amazon, and Netflix during the same period is about 2.0 times, representing a discount of over 54%. Even when calculated based on Morgan Stanley’s $775 target price, Meta’s PEG remains approximately 33% below the peer average, while its compound annual growth rate for EPS from 2025 to 2027 is projected at 16%, higher than the peer median of 10%.

Morgan Stanley’s base-case target price of $775 corresponds to a 2027 price-to-earnings ratio of approximately 21 times, roughly in line with the historical average; the bull-case target price is $1,000, and the bear-case target price is $450, implying potential upside of approximately 90%.

MetaClaw: AI Agent Capabilities Expected to Reshape Platform Growth Logic

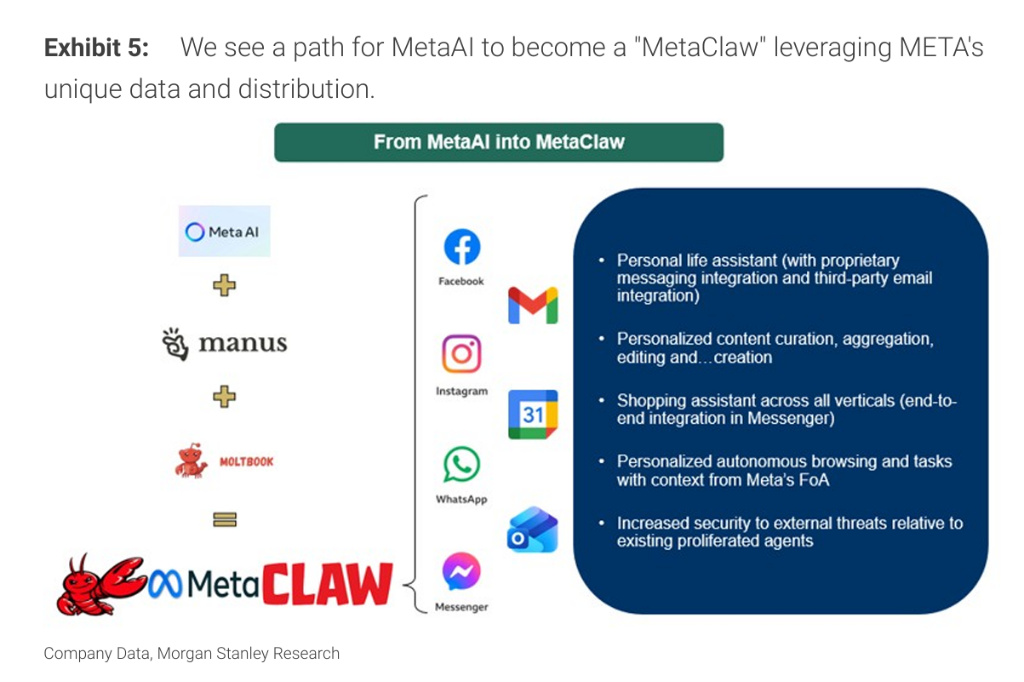

Amid the current valuation divergence, the market's core skepticism lies in whether Meta's approximately USD 190 billion in effective capital expenditure (including procurement of hyperscale computing power) can generate visible commercial returns. Morgan Stanley believes the answer lies in Meta’s potential AI agent product—"MetaClaw."

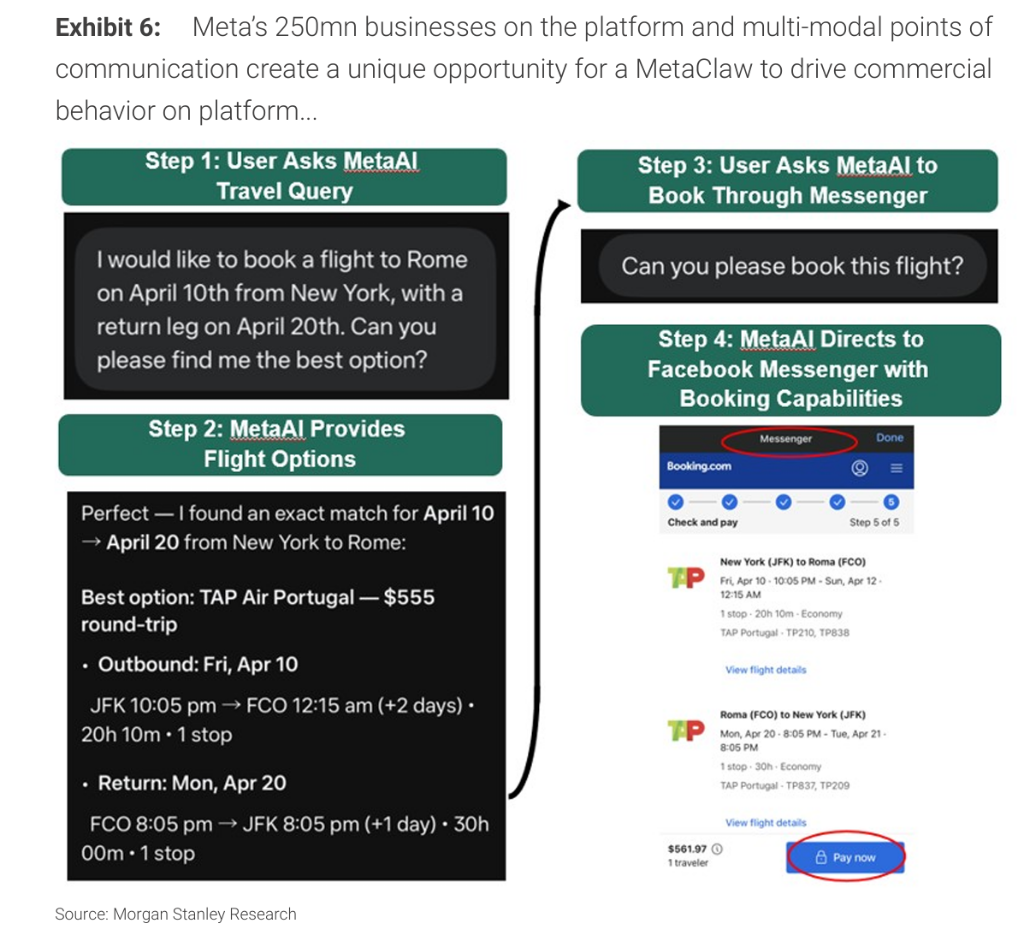

The MetaClaw framework outlined by Morgan Stanley is built on Manus and an enhanced version of the Llama large language model, with Moltbook serving as the intermediary layer connecting individual user proxies. This framework is further augmented by Meta’s multimodal commercial ecosystem, which spans over 3.5 billion daily active users, 250 million merchants, and more than 10 million advertisers across Facebook, Messenger, Instagram, and WhatsApp, forming a potential closed-loop AI agent shopping and service platform. Reports indicate that Meta is already testing the integration of Gmail and Google Calendar into its agent product.

Although Meta lacks an independent browser entry point, the inventory information and payment capabilities of its 250 million merchants already constitute the underlying infrastructure driving "agent-based shopping." Less than a month ago, Meta initiated testing of a GenAI-powered shopping feature. Once MetaClaw takes shape, it is expected to drive multi-year sustained revenue growth akin to search functionalities, extending Meta’s monetization capabilities from ad display to transactional closed loops.

On the advertiser side, Meta has begun developing fully automated creative generation and ad placement tools for small and medium-sized enterprises (SMEs), further expanding its share of advertisers’ budgets.

Core Advertising Business: Growth Trajectory Remains Underestimated

Morgan Stanley’s core advertising assumptions are not aggressive but remain slightly above market consensus expectations.

Morgan Stanley forecasts that Meta’s advertising revenue will grow by approximately 28% in 2026 and 21% in 2027, corresponding to revenue projections of about USD 257.5 billion and USD 311.6 billion, respectively—about 3% to 5% higher than market consensus. The key logic supporting this view is that the average daily usage time of Meta’s applications (approximately 40 minutes for Facebook and 60 minutes for Instagram) continues to expand, while the increasing proportion of video content enhances the monetization potential of traffic quality.

At the product pipeline level, Meta disclosed in its Q4 2025 earnings report that it plans to launch ten additional features in 2026, including large-model-driven content recommendation optimization, the expansion of WhatsApp ad placements, and the rollout of Threads ads to the UK, EU, and Brazilian markets. The company maintains clear forward visibility for 1-2 years of growth in its core business, with the next major growth milestone anticipated in 2027—when large language models will be used to analyze Meta’s native data to further enhance the quality of contextual advertising signals.

Workforce Reduction Dividend: Potential 20% Staff Cut to Raise EPS Floor

Morgan Stanley characterizes the reported potential 20% workforce reduction as a positive signal, arguing that this move will establish a higher margin of safety for EPS.

If Meta reduces approximately 157,730 positions, with an estimated annual cost per employee ranging from $200,000 to $600,000, the corresponding annualized operating expenditure savings would be approximately $3.15 billion to $9.46 billion, equivalent to 3% to 9% of Morgan Stanley's 2027 EBIT forecast for Meta. In terms of earnings per share (EPS), this move could provide an additional boost of over $1 to the 2027 EPS beyond the base case scenario, or serve as a buffer in the event of a weakening advertising market.

Notably, the base case model does not yet incorporate the savings from the above-mentioned layoffs — the model already assumes a significant increase in depreciation and amortization for 2026 and 2027, at approximately $31.9 billion and $51.3 billion respectively, reflecting Meta's continued heavy investment in infrastructure. If the layoffs are implemented, they could effectively offset upward cost pressures, making the $36.31 EPS forecast for 2027 more certain.

Catalyst Calendar: May and September Are Key Time Windows

Morgan Stanley has identified May and September 2026 as two potential key catalyst windows for Meta.

In May, Meta hosted its inaugural LlamaCon AI Developer Conference last year, and Morgan Stanley expects it may continue in 2026, with Meta likely to announce the latest model and product updates. Media reports have also mentioned the possibility of a new model being released in May. Regarding September, Meta typically holds its annual Connect Developer Conference during this month, which has historically been a concentrated venue for product roadmaps and technical milestones.

The release of products and models at these two时间节点 — particularly the implementation of MetaClaw-related capabilities — will be a key variable driving the market to reassess Meta’s ROIC visibility and thereby facilitate valuation recovery. Currently, the implied probability from market options shows that the likelihood of Meta’s stock price exceeding the $775 target within the next 12 months is approximately 13.6%, while the probability of reaching the $1,000 bullish scenario is about 0.9%. Conversely, the probability of falling to the $450 bearish scenario is approximately 31.7%.

Editor/Jayden