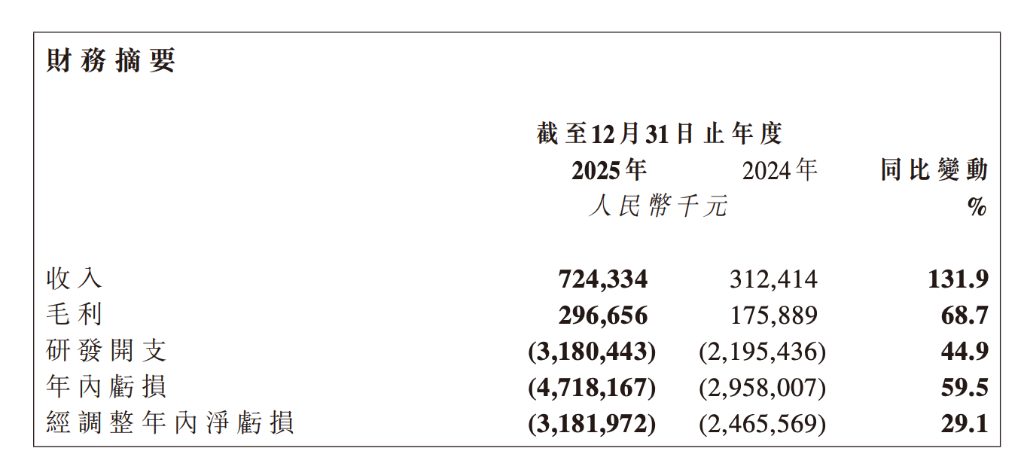

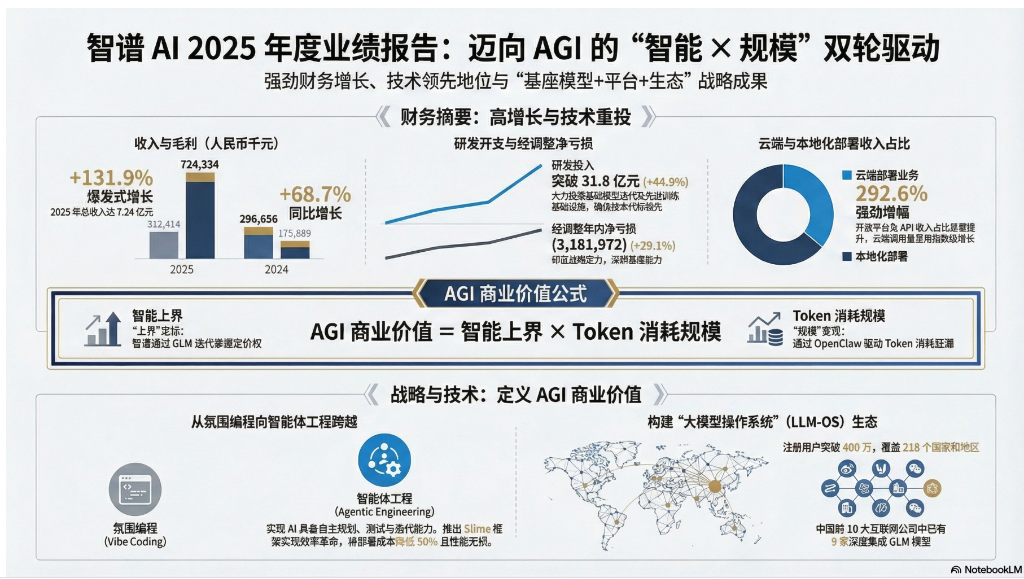

Zhipu's revenue reached 724 million yuan in 2025, representing a year-on-year increase of 131.9%. Revenue from the open platform and API (cloud services) surged by 292.6% year-on-year to 190 million yuan, while revenue from the enterprise-grade intelligent agent business grew by 248.8% year-on-year to 166 million yuan. The company invested 3.18 billion yuan in R&D, marking a 44.9% year-on-year increase, resulting in a net loss that widened by 59.5% year-on-year to 4.718 billion yuan.

On March 31, $KNOWLEDGE ATLAS (02513.HK)$ AI released its financial report for the year 2025. The report showed that the company continued its rapid growth in its first year post-IPO, but alongside strategic heavy investment in R&D, losses also expanded significantly.

In 2025, the company achieved total revenue of 724 million yuan, representing a year-on-year increase of 131.9%. Cloud services and intelligent agent businesses became the core drivers of growth. However, during the same period, the company's net loss amounted to 4.718 billion yuan, widening by 59.5% from 2.958 billion yuan in the previous year. The main reason for the expanded loss was the significant increase in R&D expenditures, which reached 3.180 billion yuan, marking a year-on-year increase of 44.9%, reflecting the company’s strategy of driving long-term development through technological investment.

Boosted by positive earnings news, Zhipu's Hong Kong stocks surged 15% at the opening on April 1st, currently trading at HKD 797.5, once again setting a new all-time high.

Boosted by positive earnings news, Zhipu's Hong Kong stocks surged 15% at the opening on April 1st, currently trading at HKD 797.5, once again setting a new all-time high.

Under the guidance of its core strategy, 'Intelligence Upper Limit × Token Consumption Scale,' the company has achieved significant progress. Its GLM series models continue to maintain a leading position in multiple international evaluations. On the commercialization front, the number of registered users on the MaaS platform has surpassed 4 million, and the GLM-5 model was quickly adopted by top domestic internet companies shortly after its release. Notably, in February 2026, the company implemented an active price increase for its programming package products, which was well-received by the market, signaling recognition of its technological value. Additionally, the company’s business operations now cover 218 countries and regions globally, actively exploring global cooperation models such as 'Sovereign AI.'

At Zhipu's 2025 earnings briefing, Zhipu CEO Zhang Peng introduced that the pricing for Zhipu's API calls would increase by 83% in the first quarter of 2026. Despite this, the market still exhibits strong demand, with call volumes surging by 400%. Currently, Zhipu has become one of the domestic vendors with the highest paid token consumption. According to reports, Zhipu's GLM model has been fully deployed on leading global cloud service providers such as Google Vertex AI, AWS Bedrock, Fireworks, and Cerebras.

Cloud service revenue tripled, with intelligent agent business emerging as a new growth engine.

A breakdown of business operations revealed diverse growth drivers. During the reporting period, the company optimized its revenue classification disclosure to better reflect its strategic layout. Among these, the open platform and API business performed most impressively, with revenue soaring from 48.48 million yuan to 190 million yuan, a year-on-year increase of 292.6%, primarily due to enhanced model capabilities and a surge in usage volume. This marks an acceleration in the scaling process of its MaaS (Model-as-a-Service) platform.

Enterprise-level intelligent agent business, as an emerging growth pole, saw its revenue rise from 47.49 million yuan to 166 million yuan, representing an increase of 248.8%. This product line aims to build autonomous intelligent systems for complex enterprise scenarios, and the explosive market demand validates the trend of AI applications evolving towards greater depth and automation.

The traditional stronghold business of enterprise-level general large models (mainly deployed locally) saw revenue grow from 215 million yuan to 366 million yuan, an increase of 70.5%, still constituting half of the revenue (accounting for 50.4%).

In terms of deployment methods, cloud services grew faster than localized services. Revenue from cloud deployment surged by 292.6% year-on-year, increasing its share of total revenue from 15.5% to 26.3%. This reflects the growing market acceptance of standardized, agile AI services and aligns with the company’s long-term strategy of promoting model servitization.

Cost Structure: R&D Investment Exceeds 3.1 Billion Yuan, Gross Margin Under Pressure

Behind the rapid revenue growth lies equally astonishing investment and temporary pressure on profitability. In 2025, the company's gross profit reached 297 million yuan, growing by 68.7% year-on-year. However, the overall gross margin declined from 56.3% in 2024 to 41.0%.

The earnings report explains that this is mainly due to the increase in the proportion of cloud deployment business and the local deployment business investing more delivery resources to meet customer demands, resulting in a temporary decline in gross margin. Notably, the gross margin of enterprise-level general large models decreased from 69.6% to 47.0%, marking a significant change.

Meanwhile, the company's cost of sales increased by 213.3% year-on-year to 428 million yuan, consistent with the pace of business expansion. The real major expense, however, lies in research and development. In 2025, the company’s R&D expenditure reached 3.18 billion yuan, a year-on-year increase of 44.9%, accounting for 439% of total revenue.

The driving factors behind this are clear: rising employee costs (due to team expansion and share-based payment expenses), as well as surging expenditures on third-party computing power services required for iterating foundational models and investing in advanced training facilities. The company is continuing to intensify its efforts during the final sprint phase of this technological marathon.

Technological Barriers: The Leap from Vibe Coding to Agentic Engineering

In the business review, management outlined a clear path of 'intelligent evolution': from atmosphere programming to agentic engineering, and ultimately to future 'digital engineers' capable of executing long-term tasks. In 2025, Zhipu claimed to have achieved the leap from Vibe Coding to Agentic Engineering ahead of its competitors.

To achieve this leap, the company tackled multiple challenges at the technical foundation. Through optimization strategies such as Muon Split and improvements in MLA-256, it reduced the GPU memory usage for model training while maintaining performance; the dynamic sparse attention mechanism addressed computational challenges in long-sequence reasoning, reportedly cutting deployment costs by 50%.

Particularly crucial is the introduction of the Slime asynchronous reinforcement learning framework, aimed at solving the 'idle spin' pain point when agents execute long-duration tasks, achieving decoupling of generation and training. Paired with an innovative direct double-sided importance sampling algorithm, the model can now efficiently learn from over 10,000 real-world software engineering environments.

Editor/KOKO