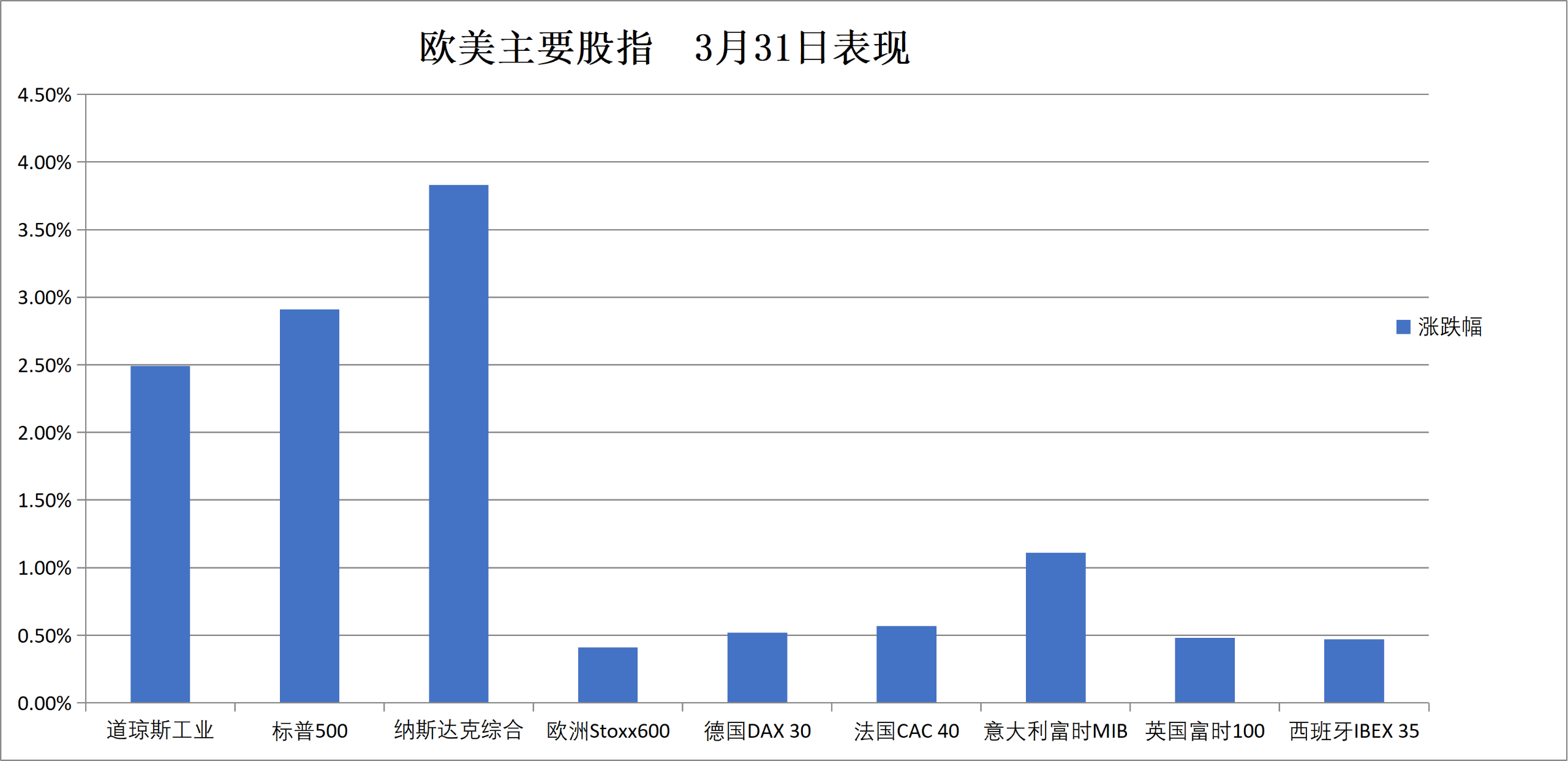

On Tuesday, the S&P 500 surged by 2.9%, the Nasdaq Composite climbed 3.8%, and the Dow Jones Industrial Average rose 2.5%. Year-to-date, the S&P 500 has fallen by 4.6%, the Nasdaq by 7.1%, and the Dow by 3.6%, marking the worst quarterly performance since 2022. One of the hardest-hit sectors in Q1 was the software industry. SaaS stocks declined for the third consecutive month, recording their worst quarterly performance since the second quarter of 2022.

Following signals of a ceasefire negotiation between the US and Iran, US stocks recorded their largest single-day gain since May 2025. Meanwhile, international oil prices retreated from their highs, the dollar weakened, and gold rebounded.

Market optimism stemmed from overnight news—President Trump had previously indicated to his aides that he was willing to end military action against Iran even while the Strait of Hormuz remained largely closed.

It is reported that U.S. government officials assessed that forcibly reopening the waterway would extend military operations beyond the originally planned timeframe of four to six weeks. Based on this, Trump decided to gradually conclude the current military operation after achieving key objectives such as weakening Iran's naval and missile capabilities.

By midday Tuesday, Iranian President Pezeshkian stated that Iran was willing to end the war, provided its demands were met, particularly assurances that it would not be subjected to aggression again. This conciliatory statement triggered a sharp rally in gold and risk assets.

Bill Northey, Senior Investment Director at Bank of America Wealth Management, commented: 'Today's capital markets are reflecting expectations of an early end to the conflict or a ceasefire.'

According to CCTV News, the Iranian President, via official media, expressed Iran's 'necessary willingness to end the war,' but stressed the need for 'guarantees to prevent future aggression.' Oil prices plunged immediately thereafter, with Brent crude falling even more sharply, widening the spread between the two benchmarks to its widest level since December 2013.

However, caution remains widespread in the market. Bloomberg macro strategist Brendan Fagan pointed out that Tehran’s definition of 'basic guarantees,' especially if tied to previously proposed ceasefire conditions, could pose a high bar for the Trump administration to accept.

The S&P 500 surged 2.9% on Tuesday, the Nasdaq climbed 3.8%, and the Dow rose 2.5%.

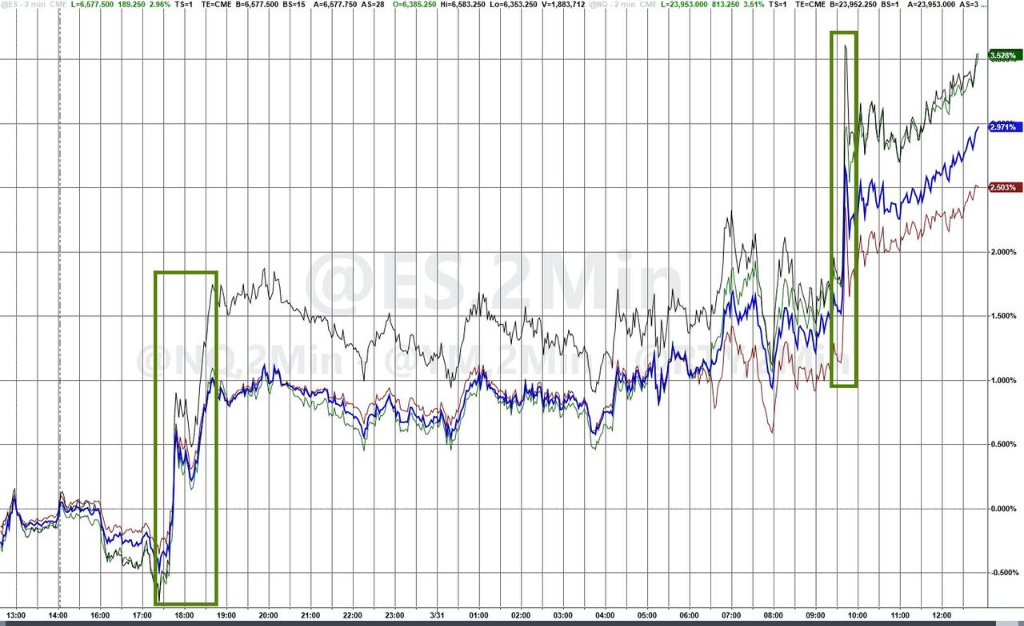

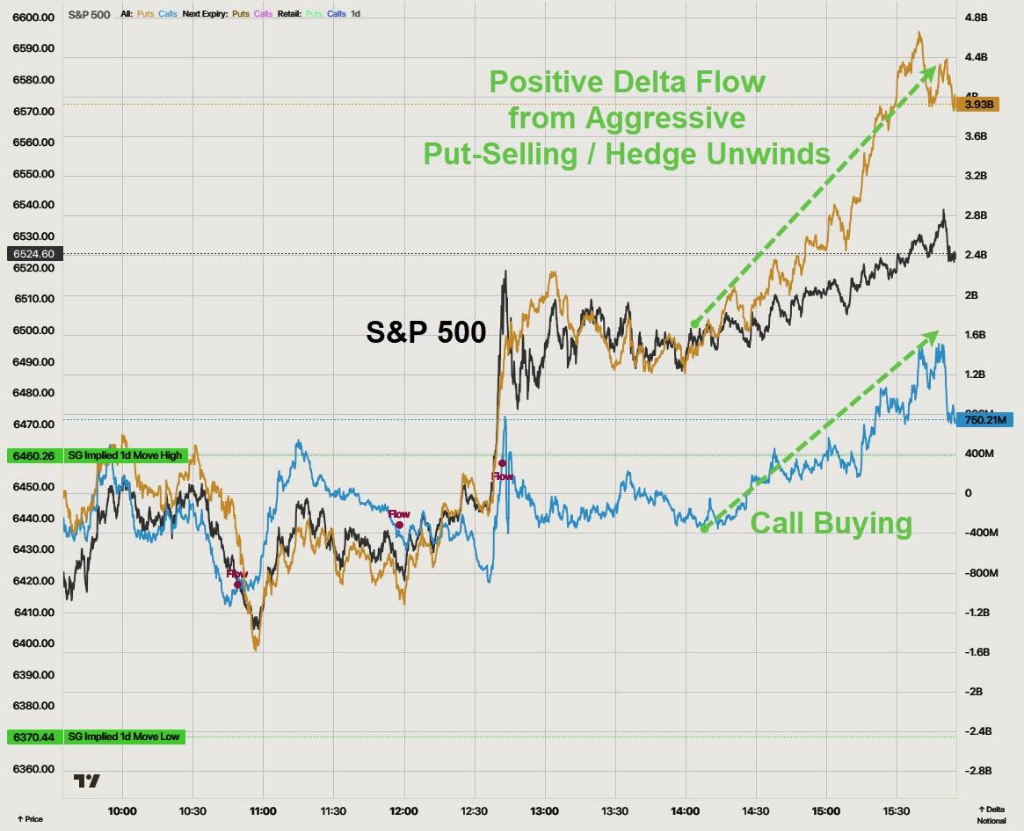

The robustness of Tuesday’s rally warrants scrutiny. According to feedback from Goldman Sachs traders, trading activity remained relatively subdued, with gains primarily driven by hedge unwinding rather than proactive capital inflows chasing the rally.

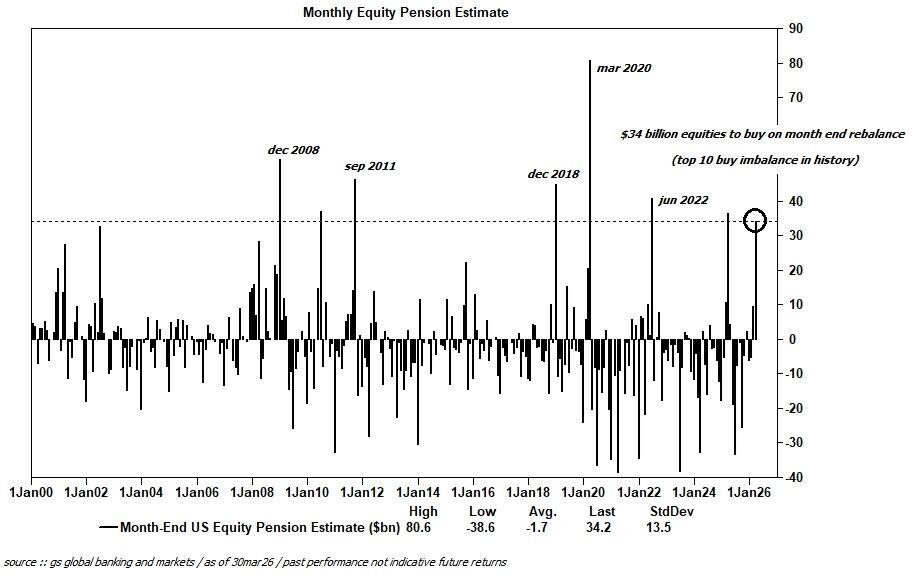

Another factor that cannot be overlooked is the quarter-end pension rebalancing. Estimates suggest that US pensions needed to purchase approximately $34 billion worth of American stocks at the end of the month, marking the eighth-largest buy imbalance since 2000 and one of the top ten historical imbalances.

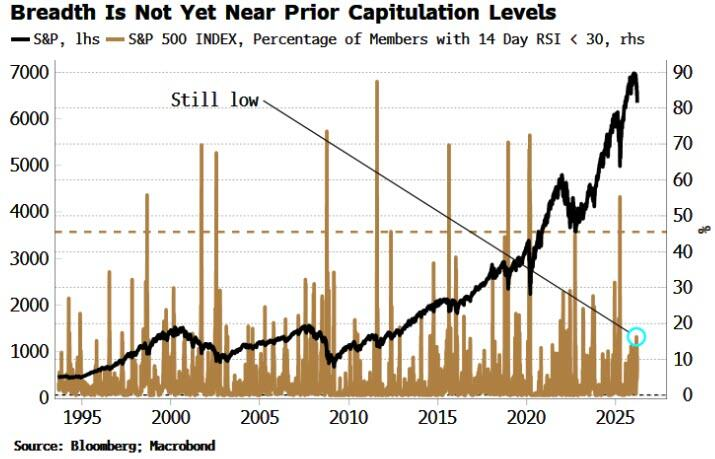

Bloomberg strategist Simon White noted that the market has yet to exhibit technical signs of a bottom. The net number of NYSE-listed stocks hitting new 52-week lows was only slightly negative, whereas historically tradable bottoms often coincide with deeply negative values.

Less than 20% of the stocks in the S&P 500 have an RSI below 30, a level that historically tends to indicate a mature rebound opportunity when it reaches 40% to 50%.

Moreover, Tuesday's sharp rally could not mask the brutal end to the first quarter. The S&P 500 is down 4.6% year-to-date, Nasdaq has fallen 7.1%, and the Dow Jones has dropped 3.6%, marking the worst quarterly performance since 2022.

From the energy crisis to concerns about an AI bubble, from stress in the credit markets to looming stagflation, every trading day in Q1 tested investors' nerves.

One of the most brutal battlegrounds in Q1 was the software sector. SaaS stocks fell for the third consecutive month, posting their worst quarterly performance since Q2 2022, with existential threats posed by AI disruption being the core pressure point.

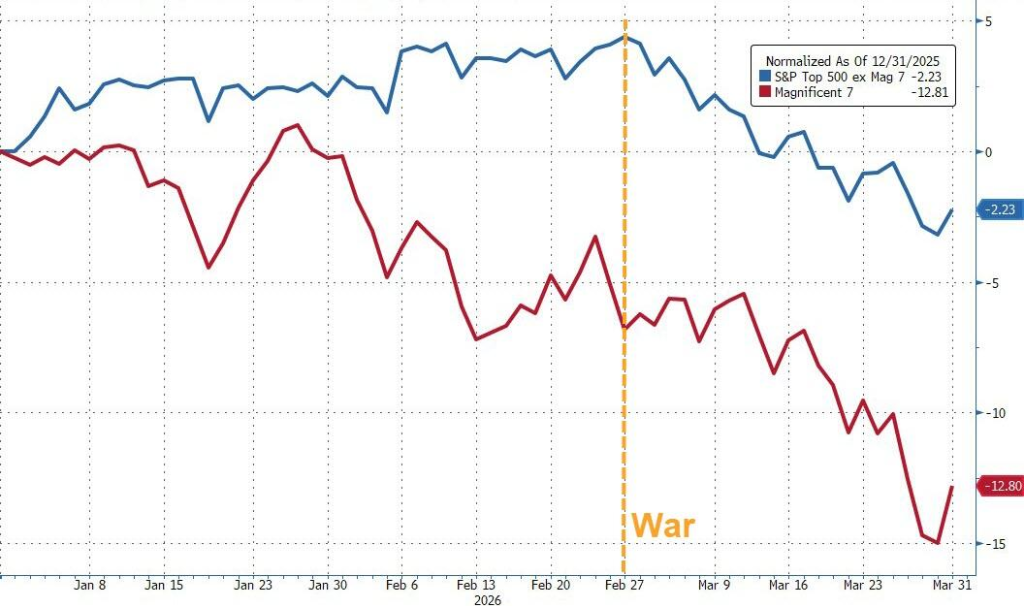

The Mag 7 tech giants significantly underperformed relative to the other 493 components of the S&P 500 in Q1.

Meme stocks recorded their largest drop since December 2022 in March and have now declined for five consecutive months.

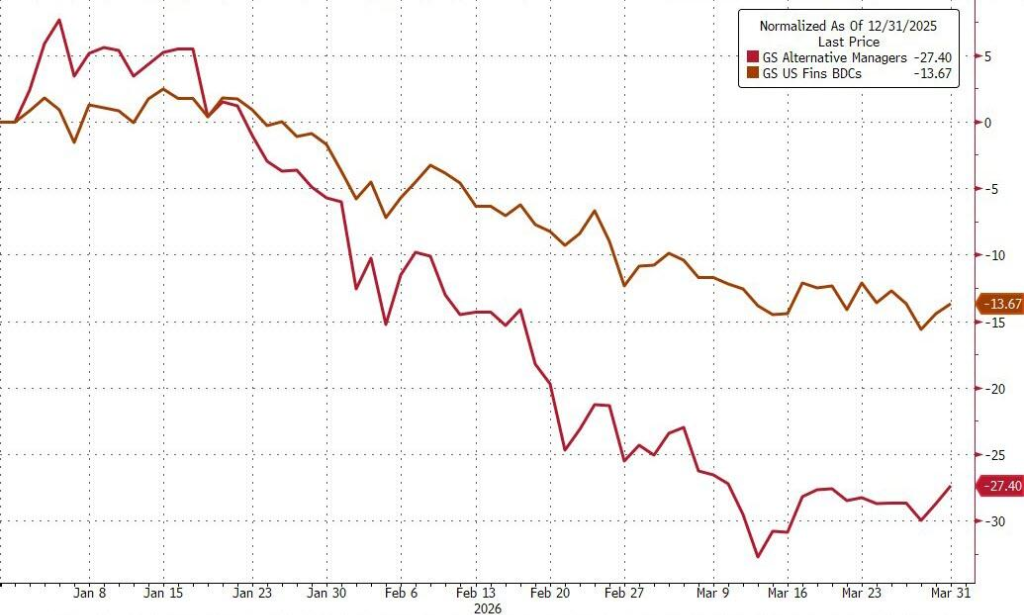

Meanwhile, cracks in the private credit market are becoming increasingly apparent. The mark-to-market valuation of BDC loans, affected by redemption restrictions, is bringing the private credit crisis from behind the scenes to the forefront. Investment-grade and high-yield credit spreads widened sharply in March, reaching their highest levels since April last year.

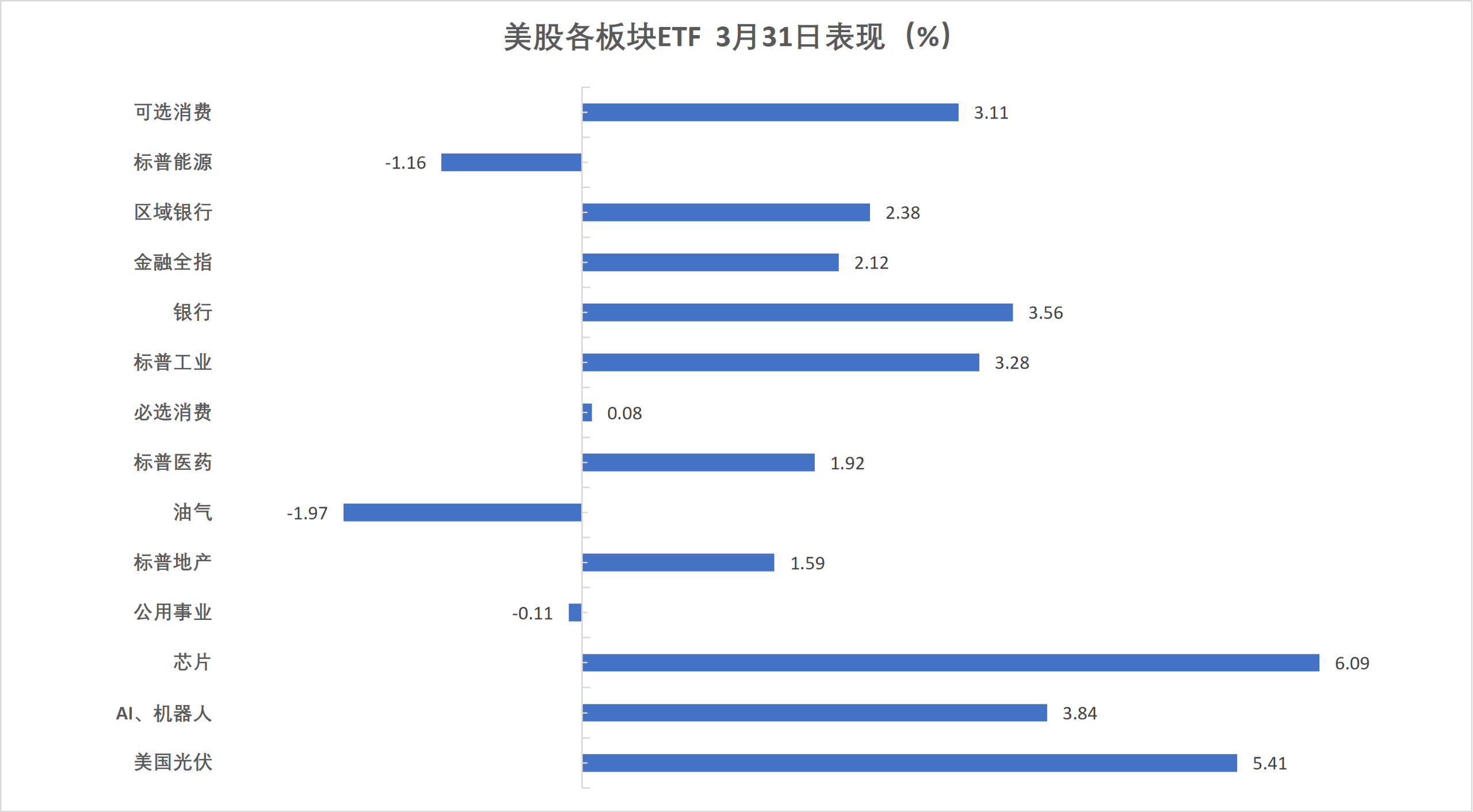

U.S. stocks rose broadly on Tuesday, with the semiconductor ETF closing up more than 5.7%, leading U.S. sector ETFs on the final trading day of March. The energy sector ETF gained 37.9% in Q1.

U.S. Equity Benchmark Indices:

The S&P 500 Index closed up 184.80 points, or 2.91%, at 6,528.52.

The Dow Jones Industrial Average closed up 1,125.37 points, or 2.49%, at 46,341.51.

The Nasdaq Composite Index rose by 795.988 points, or 3.83%, closing at 21,590.629 points. The Nasdaq 100 Index surged by 786.811 points, or 3.43%, marking its largest single-day gain since May 2025, and closed at 23,740.189 points.

The Russell 2000 Index climbed by 3.41%, ending the session at 2,496.374 points.

The VIX volatility index, often referred to as the 'fear gauge,' dropped by 17.45% to close at 25.27.

U.S. sector ETFs:

The semiconductor ETF rebounded by 5.76% at the close. The global technology stock index ETF, biotech index ETF, tech sector ETF, and global airline industry ETF all gained up to 4.40%, while the energy sector ETF fell by 1.13%.

In the first quarter, the energy sector ETF surged by 37.91%, while the utility ETF, semiconductor ETF, regional banking ETF, and biotech index ETF gained up to 8.20%.

Mag 7:

The Wind US Tech Magnificent 7 Index rose by 4.40%.

$Meta Platforms (META.US)$Up 6.67%,$NVIDIA (NVDA.US)$Up 5.62%, with Google A up 5.14%.$Tesla (TSLA.US)$ Up 4.64%, Amazon up 3.66%, Microsoft up 3.12%, $Apple (AAPL.US)$ Up 2.90%.

Semiconductor stocks:

The Philadelphia Semiconductor Index closed up 6.24% at 7588.196 points.

$Micron Technology (MU.US)$ Up 4.98%, Taiwan Semiconductor ADR up 6.78%, AMD up 3.77%.

Chinese concept stocks:

The Nasdaq Golden Dragon China Index closed up 2.80% at 6753.34 points, with a cumulative decline of 7.20% in March and a cumulative drop of 10.31% in the first quarter.

Other individual stocks:

Circle up 6.25%.

European stock markets fell 8% in March, as the war on Iran initiated by Trump wiped out the gains from January to February. The German stock market dropped over 10% in March, while the Norwegian stock market rose about 11.6% in March and 27% in the first quarter.

Pan-European Index:

The European STOXX 600 Index closed up 0.41% at 583.14 points, with a cumulative decline of 8.00% in March. Following the Iran war launched by the US and Israel at the end of February, the index continued to fall overall, with a cumulative drop of 1.53% in the first quarter after continuous increases in January and February.

The Eurozone STOXX 50 Index closed up 0.50% at 5569.73 points, with a cumulative decline of 9.26% in March and 3.83% in the first quarter.

National indices:

The German DAX 30 Index closed up 0.52% at 22680.04 points, with a cumulative decline of 10.30% in March and 7.39% in the first quarter.

The French CAC 40 Index closed up 0.57% at 7,816.94 points, with a cumulative decline of 8.90% in March and 4.08% in the first quarter.

The UK FTSE 100 Index closed up 0.48% at 10,176.45 points, with a cumulative decline of 6.73% in March but a cumulative increase of 2.47% in the first quarter.

Sector and Stock Performance:

Among Eurozone blue-chip stocks, Germany's Rheinmetall (RHM) rose 2.48%, Adidas gained 2.24%, and Deutsche Boerse Group climbed 2.20%, marking the third-best performance.

Among all components of the European STOXX 600 Index, Hensoldt surged 6.63%, Hochschild Mining rose 5.57%, Abivax advanced 5.41%, Alstom gained 5.39%, and Antofagasta increased by 5.25%, ranking fifth in performance.

In terms of sectors for March, the STOXX 600 Personal & Household Goods Index fell 15.05%, the Real Estate Index dropped 14.53%, the Automobiles & Parts Index declined 12.66%, the Construction & Materials Index fell 12.33%, and the Retail Index dropped 12.00%.

Middle East Abu Dhabi Murban crude oil futures fell 1.58% to $109.03 per barrel, with a cumulative increase of 48.72% in March and 78.10% in the first quarter.

Crude Oil:

WTI May crude oil futures settled at $101.38 per barrel.

Brent May crude oil futures settled at $118.35 per barrel.

The Abu Dhabi Murban crude oil futures in the Middle East fell by 1.58%, closing at USD 109.03 per barrel, with a cumulative increase of 48.72% in March and a total rise of 78.10% in the first quarter.

Natural Gas:

The NYMEX April natural gas futures settled at USD 2.8840 per million British thermal units.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Stephen