As tensions in the Middle East push oil prices to multi-year highs, the trading logic in the U.S. bond market is undergoing a fundamental shift. Traders are abandoning bets on a rebound in inflation and instead focusing on the potential impact of high energy prices on economic growth in the United States and globally.

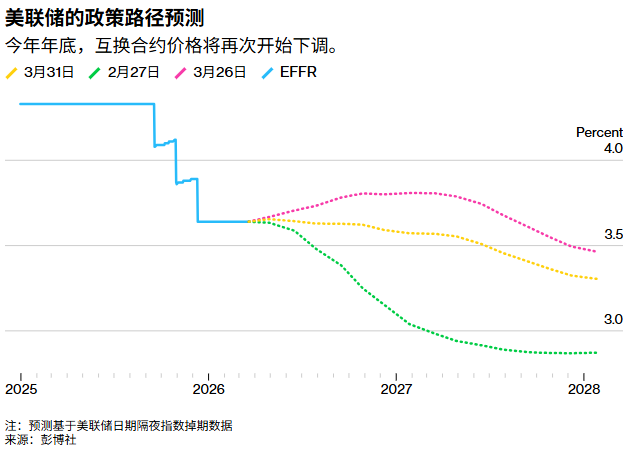

This shift in sentiment has been particularly pronounced in the interest rate market: as recently as the beginning of last week, futures prices were confidently pricing in an interest rate hike by the Federal Reserve before the end of the year; now, expectations reflected in the interest rate swaps market have completely reversed – cumulative Fed rate cuts of about 6 percentage points are expected by the end of 2026, implying an approximately 25% probability of rate cuts priced into the market.

Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, noted that investors now widely believe that the threat posed by the energy shock to global economic growth is on par with, or even surpasses, concerns about inflation.

This dramatic change in perspective was quickly reflected in the options market linked to the Secured Overnight Financing Rate (SOFR). Data released on Monday showed that changes in open interest positions sent a clear signal: previously large hawkish positions hedging against rate hikes had been unwound and incurred losses.

This dramatic change in perspective was quickly reflected in the options market linked to the Secured Overnight Financing Rate (SOFR). Data released on Monday showed that changes in open interest positions sent a clear signal: previously large hawkish positions hedging against rate hikes had been unwound and incurred losses.

On Tuesday, a notable trade emerged in the market, employing a strategy of selling put options to generate funds, aiming to profit from the ongoing dovish shift at the front end of the curve in futures markets. The market has now fully priced in a 25-basis-point rate cut at the December policy meeting.

This shift in strategy reflects investors' reassessment of the economic impact of the Iran conflict. Early market interpretations suggested the Fed would need to raise rates to curb anticipated inflationary rebounds, but concerns about economic growth have now taken center stage, driving a rally in U.S. Treasuries and other major economies' sovereign bonds. Jerome Powell, Chair of the Federal Reserve, further solidified this market consensus in his speech on Monday, hinting that the central bank is inclined to overlook the impact of rising oil prices rather than adjust interest rate policies accordingly.

In the middle section of the Treasury yield curve, the reallocation of capital is also evident. On Monday, when the price of 5-year Treasury futures rose, the open interest positions increased rather than decreased. This conveys a key message: the rise was not driven by short covering (price increases due to short covering typically coincide with a decline in open interest) but rather by new long positions being established. This indicates that investors are not being forced to stop out but are proactively entering bullish positions.

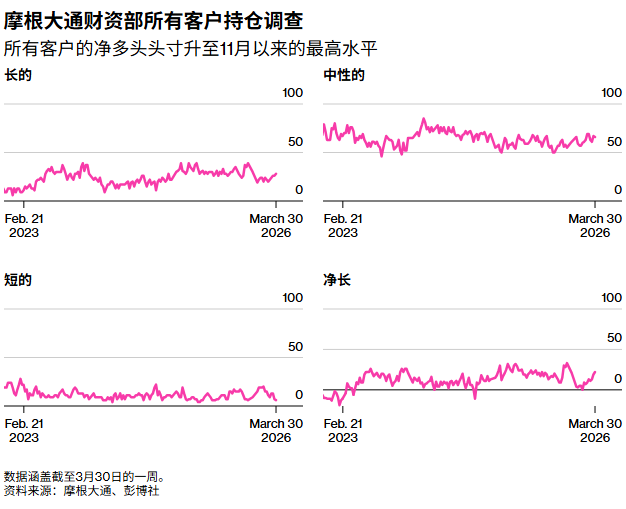

It is understood that this sector had undergone a prolonged period of deleveraging (investors reducing positions and lowering risk exposure), and this behavioral pattern is now reversing, with demand for 'bottom fishing' or 're-entering long positions' returning. Additionally, the spot market is also showing bullish momentum, with JPMorgan’s Treasury client survey released on Tuesday indicating that net long positions among clients have reached their highest level since November of last year.

Below is an overview of the latest positioning indicators in the interest rate market:

JPMorgan Client Survey

As of the week ending March 30, JPMorgan's clients increased their long positions by 2 percentage points, while short and neutral positions each fell by 1 percentage point, shifting the net position to the largest long position since November of last year.

SOFR Options

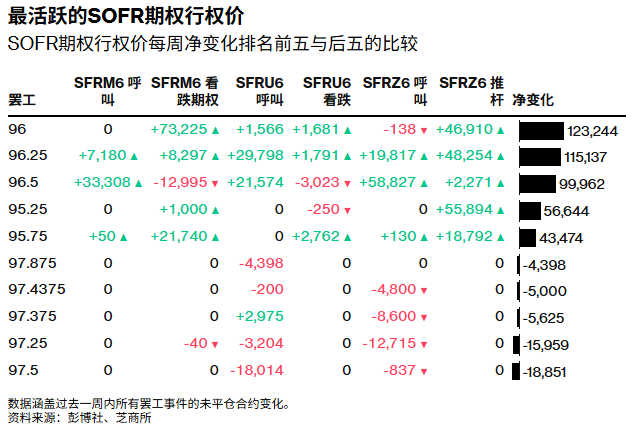

The microstructure of the SOFR options market further confirms this pricing shift. Over the past week, traders have heavily established new risk exposures in put options expiring in June and December 2026 with a strike price of 96.00 to hedge against potential rate hike risks within the year. Recent fund flows around this strike price include buying SFRM6 96.3125/96.00 put spreads and purchasing SFRM6 96.25/96.00/95.75 put butterfly structures. The 96.25 strike price was also active last week, with one notable trade involving the sale of 25,000 straddle contracts expiring in September 2026, generating premium income of up to $30 million.

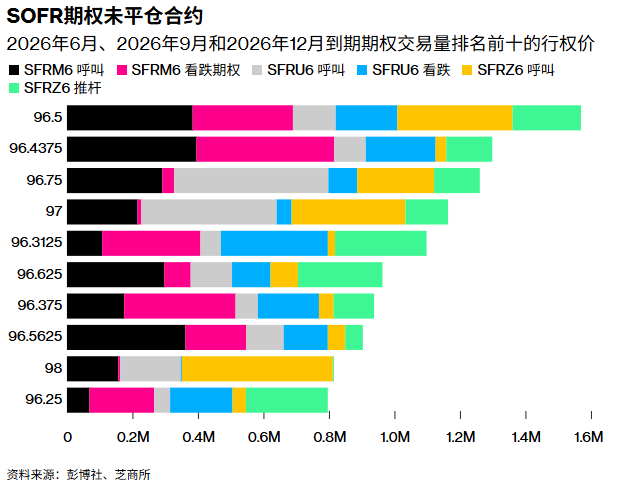

In terms of strike price distribution, the most concentrated open interest remains at the 96.50 strike price for the June, September, and December 2026 contracts, which aggregates significant risks from call and put options expiring in June as well as call options maturing in December. Notably, the June SOFR option will expire on June 12, a week ahead of the policy statement scheduled for June 17.

Additionally, the open interest volume near the 96.4375 strike price for the June option has risen significantly recently. Related trading flows include buying SFRM6 96.4375/96.50 call spreads while selling 2QM6 97.375 calls, forming a ratio bullish steepener structure with a transaction size of approximately 100,000 contracts against 50,000 contracts.

Treasury Option Premium

The risk premium structure in the Treasury options market has also undergone significant adjustments. Over the past few weeks, the hedging premium for front-end yield curve options had favored puts but has now retreated to near-neutral levels, reflecting dovish repricing in the front-end market on Friday and Monday, as well as recalibration of market expectations for rate cuts from year-end to next year. On the longer end of the curve, option premiums remain skewed toward puts, indicating that traders are more willing to pay insurance costs for potential selloffs rather than rallies in long-term bond futures.

Editor/Melody