①At the start of this week, the national average retail price of gasoline in the United States officially exceeded $4 per gallon, reflecting ongoing supply shocks in the energy market; ②Interestingly, while this might seem to signal that the Federal Reserve should raise interest rates to curb inflation, the answer, at least for now, may be quite the opposite…

At the start of this week, the national average retail price of gasoline in the United States officially surpassed $4 per gallon, reflecting ongoing supply shocks in the energy market. Interestingly, while this might seem to be a signal for the Federal Reserve to raise interest rates in order to curb inflation, the answer, at least for now, may be quite the opposite…

On Tuesday, investors instead anticipated that the Federal Reserve would keep benchmark interest rates unchanged, and might even pivot to cutting rates later this year, as policymakers are likely to weigh the risks posed by rising energy prices—an increase that could weigh more on economic growth than trigger lasting inflation.

In a speech delivered on Monday that could influence market movements, Federal Reserve Chair Powell hinted that raising interest rates at this moment might not be the right remedy for an economy already facing a weakening labor market and growing concerns on Wall Street about a potential recession—when asked whether he believed policymakers should consider a rate hike now, Powell responded, “By the time the effects of monetary tightening become apparent, the oil price shock may have long passed, and you would be putting undue pressure on the economy at an inappropriate time. Therefore, our inclination is to ignore any form of supply shock.”

In a speech delivered on Monday that could influence market movements, Federal Reserve Chair Powell hinted that raising interest rates at this moment might not be the right remedy for an economy already facing a weakening labor market and growing concerns on Wall Street about a potential recession—when asked whether he believed policymakers should consider a rate hike now, Powell responded, “By the time the effects of monetary tightening become apparent, the oil price shock may have long passed, and you would be putting undue pressure on the economy at an inappropriate time. Therefore, our inclination is to ignore any form of supply shock.”

These remarks were made at a pivotal moment for the markets, which had been struggling to discern the Fed’s true intentions amid a series of conflicting and ever-changing economic signals. Just last week, traders were seriously contemplating the risk that the Fed’s next move might involve a rate hike.

However, Powell’s comments—though couched in the Fed’s characteristic diplomatic style, suggesting both a rate hike or cut remains possible—helped steer the market away from its hawkish stance. Bond traders quickly abandoned bets on rising inflation, shifting their focus to the potential impact of high oil prices on economic growth.

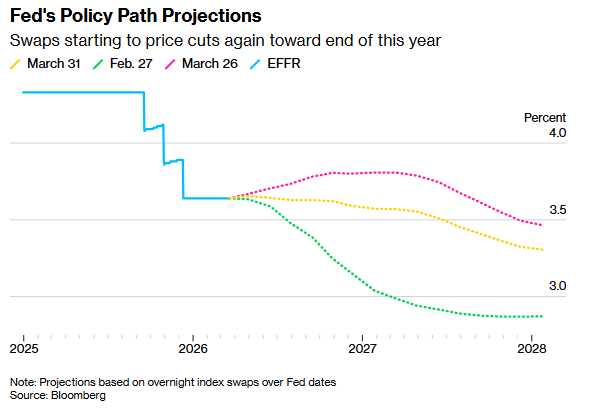

As shown in the chart below, at the start of last week, futures markets widely expected a rate hike before the end of the year to be a foregone conclusion. Now, the interest rate swaps market reflects expectations of about 6 basis points in rate cuts by the end of 2026, equivalent to roughly a 25% probability. Ian Lyngen, head of U.S. interest rate strategy at BMO Capital Markets, stated that investors “now view the risks to global economic growth posed by the energy shock as equal to, or even greater than, inflation concerns.”

This dramatic shift was unmistakably evident in the options market linked to the Secured Overnight Financing Rate (SOFR), which is closely tied to central bank policy expectations. Data on open interest (i.e., traders’ exposure) released on Monday showed that a large number of hawkish positions, previously established to hedge against expectations of an imminent Fed rate hike, appeared to have been liquidated—and at a loss.

Abandon Inflation Concerns, Stabilize the Economy?

Rob Subbaraman, head of global macro research at Nomura Securities, wrote in a recent report that when it comes to addressing high prices, central bankers may ultimately be “strong in words but slow in action.”

He added, "Currently, with the overall inflation rate surging, it makes sense for central banks to adopt a wait-and-see approach while maintaining a hawkish stance, which helps stabilize inflation expectations. However... the pass-through effect of rising oil prices on wage growth and core inflation may be limited. On the contrary, the conflict in the Middle East could quickly escalate into a global economic growth shock."

In fact, recent concerns among industry insiders about the impact of soaring oil prices on economic growth have surpassed worries about inflation itself, aligning with Powell’s view that raising interest rates now will not address energy cost issues but may instead lead to more problems in the future. Policymakers are more concerned about the risk of price increases undermining consumer demand and employment rather than the direct impact of energy-driven inflation.

Joseph Brusuelas, Chief Economist at RSM, stated that central bank policymakers should be wary of 'demand destruction' triggered by energy shocks.

"Time is not on the side of the U.S. economy," he wrote in the article. "The greater risk lies in what comes next: demand destruction. This is the term in economics for the phenomenon where high prices force individuals and businesses to cut back on spending. It sounds abstract, but it is very concrete – meaning fewer car sales, fewer home purchases, fewer dining outings, reduced business investments, and ultimately fewer jobs."

Brusuelas added that the Federal Reserve is caught in a policy dilemma: raising interest rates now could further drag down economic growth, while standing pat risks worsening oil price conditions.

"This is a classic stagflation dilemma with no perfect solution," he said. "If the situation deteriorates further, the Federal Reserve will take action. But we believe the Fed is more likely to remain patient, and when it eventually acts, it tends to lag behind the curve, putting further pressure on demand before making significant rate cuts."

Jason Thomas, Head of Global Research and Investment Strategy at Carlyle Group, expressed similar concerns, stating that the Fed may not only be forced to cut rates but also do so by larger increments than its usual 25 basis points per move.

This dynamic highlights a shift in the Fed's approach to shocks – moving away from focusing on temporary price spikes to paying more attention to broader economic impacts. Thomas wrote, "Faced with a temporary supply shock severely impacting the labor market, the Federal Reserve will not stand idly by. In this economic downturn scenario, rate cuts could begin as early as September, and the magnitude of the cuts is likely to exceed 25 basis points."

Editor/Doris