Trump expressed willingness to end the war while the Strait of Hormuz remains largely closed, shifting responsibility for reopening the strait to allies.

Deutsche Bank warned that there has been no significant improvement in actual transit volume data through the strait. If the blockade persists until November, Brent crude oil prices could average $177 per barrel. Multiple obstacles, such as the absence of U.S. minesweepers, potential intervention by the Houthis, and IEA reserves sufficient for only one month, have cast uncertainty over the timeline for reopening the strait.

The latest developments indicate that both the United States and Iran have expressed a willingness to end the conflict in the Middle East. However, if the war concludes, a critical question will inevitably arise: who will secure the Strait of Hormuz?

On March 31 local time, U.S. President Trump stated at the White House that the United States would conclude its military operations against Iran within "two to three weeks," adding that "the hardest part has already been completed." On the same day, he posted on social media: "You need to start learning to fight for yourselves; America won’t help you anymore. Go get your own oil."

On March 31 local time, U.S. President Trump stated at the White House that the United States would conclude its military operations against Iran within "two to three weeks," adding that "the hardest part has already been completed." On the same day, he posted on social media: "You need to start learning to fight for yourselves; America won’t help you anymore. Go get your own oil."

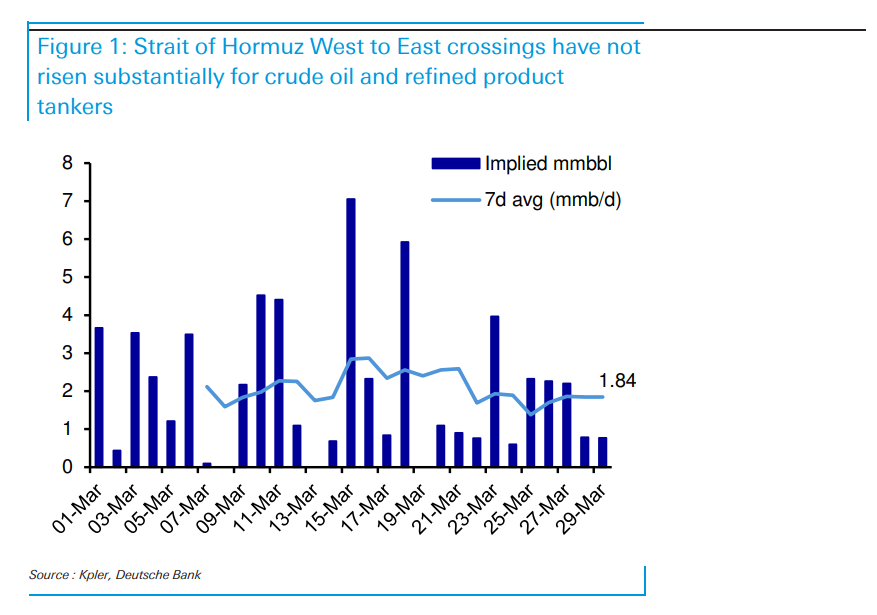

These remarks fundamentally altered market expectations regarding the situation in the Strait of Hormuz. Shipping data for the strait showed that as of March 29, the seven-day average transit volume remained at just 1.8 million barrels per day, equivalent to Iran’s crude oil exports, with no substantial improvement.

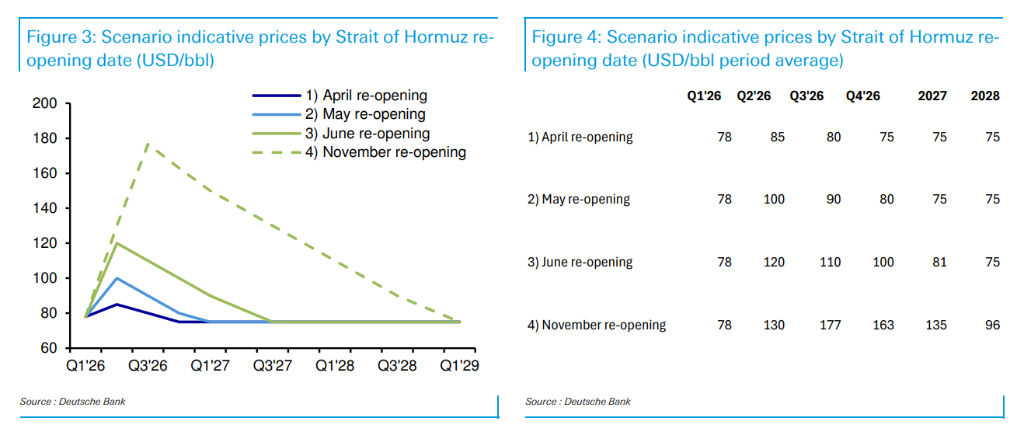

Deutsche Bank outlined four scenarios: if the strait reopens in April, Brent crude prices would quickly retreat to $90 per barrel and subsequently stabilize around $75 as the IEA releases reserves. However, if the blockade persists until November (spanning two quarters), the average Brent crude price would reach $177 per barrel, fluctuating between $170 and $190.

U.S. 'Passing the Buck,' Reopening of the Strait Remains Unresolved

According to information obtained by CCTV reporters on March 30 local time, U.S. officials revealed that Trump had informed aides of his willingness to end military operations even if the Strait of Hormuz remains largely closed.

U.S. government officials assessed that forcibly reopening the waterway would extend military operations beyond the originally planned timeframe of four to six weeks. Based on this, Trump decided to gradually conclude current operations after achieving key objectives such as weakening Iran's naval and missile capabilities, shifting instead to diplomatic pressure to push Iran to restore shipping access. Should diplomacy fail, Washington will urge European and Gulf allies to take the lead in reopening the strait.

According to Xinhua News Agency reports, Trump also singled out the UK on social media, stating it "refused to participate in strikes against Iran," and suggested: "First, buy from us—we have plenty; second, muster the courage to seize control of the strait yourself."

Data Shows: Virtually No Improvement in Transits Through the Strait of Hormuz

According to Storm Chaser Trading Desk, Deutsche Bank analyst Michael Hsueh noted in a research report published on March 31 that since Trump described Iran’s "goodwill gesture" (i.e., increased commercial transit permits) on March 25, there has been no material increase in the west-to-east flow of crude oil and refined products through the Strait of Hormuz.

As of March 29, the seven-day average transit volume was only 1.8 million barrels per day, nearly equivalent to Iran's crude oil exports (approximately 1.5 million barrels per day).

This implies that there is a significant gap between official statements and independently verifiable facts.

Moreover, “the blockade of the Strait may persist beyond the end of the war.”

Michael Hsueh believes that Trump’s remarks implicitly halted the escalation of threats by the U.S. military against Iran’s power generation facilities. However, this may allow Iran to maintain long-term control over the Strait in a lower-intensity manner, using it as political leverage against Gulf oil-producing countries. Some experts have already described the scenario of 'military operations ending without reopening the Strait' as 'incredibly irresponsible.'

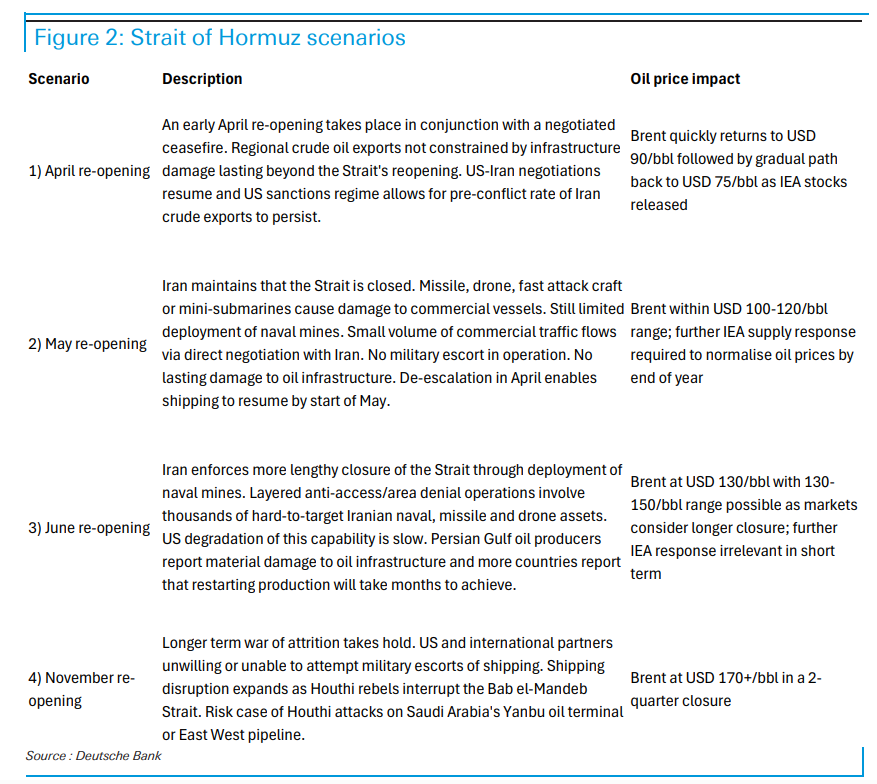

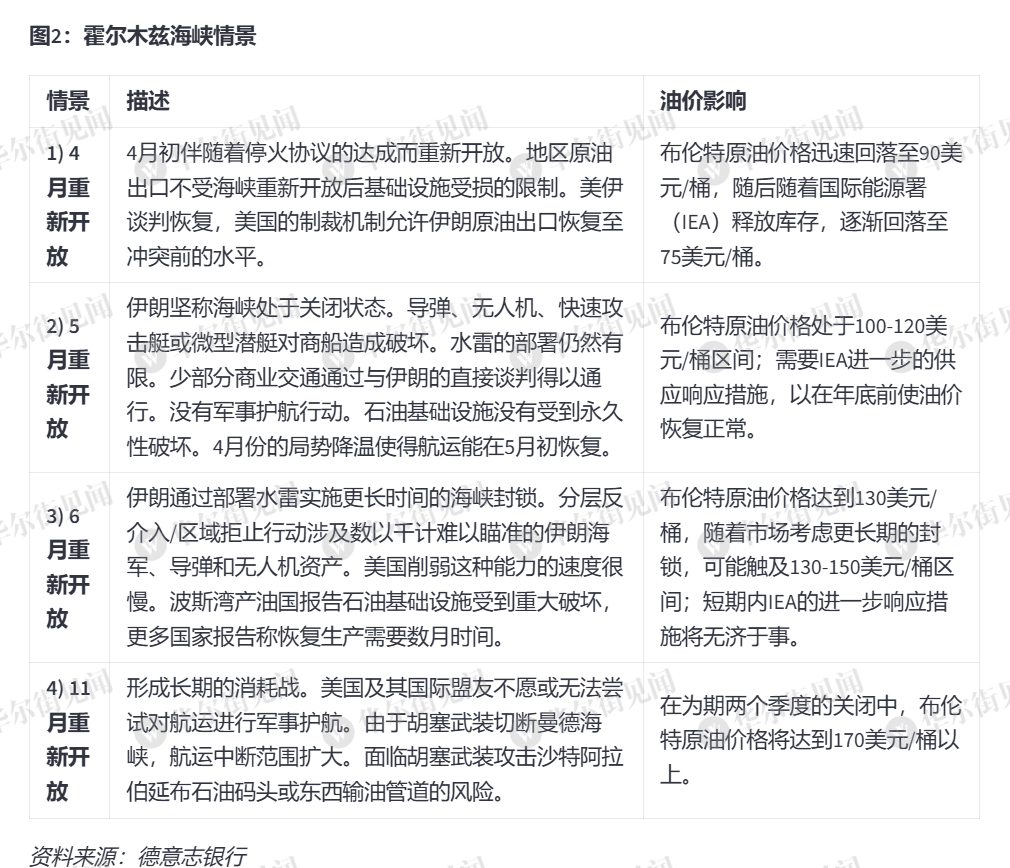

Four scenarios: oil prices could reach as high as $177 per barrel

Deutsche Bank constructed four scenarios with the duration of the Strait’s blockade as the core variable:

Scenario One: Reopening in April

Reopens in early April alongside the conclusion of a ceasefire agreement. Regional crude oil exports are not constrained by infrastructure damage following the reopening of the Strait. U.S.-Iran negotiations resume, and the U.S. sanctions regime permits Iran’s crude oil exports to return to pre-conflict levels.

$Brent Last Day Financial Futures (JUN6) (BZmain.US)$Prices quickly retreated to $90 per barrel and gradually returned to $75 per barrel with the release of IEA reserves.

Scenario Two: Reopening in May

Iran maintains the blockade. Iran insists that the strait remains closed. Missiles, drones, fast attack boats, or mini-submarines have caused damage to commercial vessels. The deployment of naval mines remains limited. A small portion of commercial traffic has been allowed passage through direct negotiations with Iran. No military escort operations are in place. Oil infrastructure has not suffered permanent damage. The situation de-escalated in April, allowing shipping to resume by early May.

$Brent Last Day Financial Futures (JUN6) (BZmain.US)$Prices remain within the range of $100 to $120 per barrel. Further releases of IEA reserves will be required before the end of the year to normalize oil prices.

Scenario Three: Reopening in June

Iran's extensive mining operations extend the blockade. The U.S.'s efforts to diminish this capability are proceeding slowly.$Brent Last Day Financial Futures (JUN6) (BZmain.US)$Prices reach $130 per barrel, fluctuating between $130 and $150 per barrel. The impact of releasing IEA reserves is limited in the short term.

Scenario Four: Reopening in November (Most Extreme Scenario)

A prolonged war of attrition ensues, with the Houthis intervening and blockading the Bab el-Mandeb Strait. Attacks may target Saudi Arabia’s Yanbu port or its East-West pipeline.$Brent Last Day Financial Futures (JUN6) (BZmain.US)$During the two-quarter blockade period, average prices reach $177 per barrel, fluctuating between $170 and $190 per barrel.

Notably, a Deutsche Bank survey indicates that 64% of respondents expect the strait blockade to end between May and September 2026 (with 25% expecting May, 16% expecting June, and 23% expecting the third quarter).

Reopening the Strait Proves More Challenging Than Anticipated

U.S. mine-clearing capabilities are not yet in position. Deutsche Bank notes that among the three U.S. Navy littoral combat ships equipped with mine-sweeping capabilities, the "Tulsa" and "Santa Barbara" were last reported docked in Malaysia and Singapore for routine maintenance, while the "Canberra" is located in the Indian Ocean, making them unable to participate immediately in reopening the strait.

Iran's conditions remain stringent. Iran has explicitly stated it will only cease hostilities upon the fulfillment of all five of its proposed conditions, including the closure of all U.S. regional bases and guarantees of non-aggression. These conditions are almost impossible for the U.S. to accept.

According to reports by Xinhua News Agency, Iranian President Masoud Pezeshkian stated on March 31 that Iran has the 'necessary willingness' to end the war, provided that the other party meets Iran's demands, particularly by providing assurances that it will not engage in further aggression.

Internal coordination within Iran's leadership is challenging. According to a U.S. media report on March 30, difficulties in internal coordination within Iran’s leadership will further delay the negotiation process, making the timeline for the reopening of the Strait even more uncertain.

There are significant differences regarding the timing of production restarts. Saudi Aramco CEO Amin Nasser previously stated that restarting production would take 'days, not weeks'; however, Kuwait Petroleum Corporation noted last week that restoring output after the war could take three to four months. The substantial gap reflects variations in geological conditions and surface infrastructure among oil-producing countries.

IEA Reserves: Enough for One Month – What Happens Next?

Data estimates indicate that the IEA’s initial coordinated release of 400 million barrels of reserves, after considering various mitigating factors, can cover approximately one month of the Strait blockade gap, expected to last until September to November 2026.

The issue lies in this: If the blockade lasts for two quarters, at a pace of releasing 400 million barrels every two quarters, a cumulative total of 2.4 billion barrels would need to be released, while the IEA’s actual reserves amount to only 1.8 billion barrels, resulting in a shortfall of about 800 million barrels.

Deutsche Bank believes that potential options to fill this gap include: IEA member states increasing production commitments, OPEC urgently ramping up production after the Strait reopens, and utilizing approximately 1.2 billion barrels of large-scale reserves.

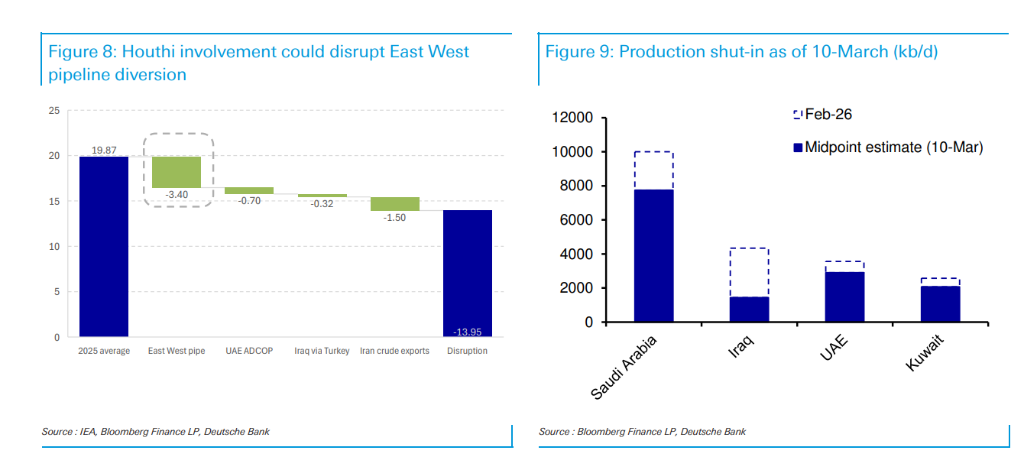

Houthi Forces: The Largest Variable of Uncertainty

The Houthi forces launched missile attacks on Israel this week, and their level of involvement is the most critical uncertainty factor.

If the Houthi forces merely block southbound shipping in the Red Sea, vessels can reroute through the Suez Canal, albeit with longer travel times and reduced cargo loads. However, if the 2022 Saudi-Houthi ceasefire agreement collapses, the Houthi missile capabilities would directly threaten Saudi infrastructure.

There are historical precedents: In May 2019, the Houthi forces attacked Saudi Arabia's East-West Pipeline, forcing its closure for 'condition assessment'; in September of the same year, the Houthis triggered a shutdown of the Abqaiq oil processing facility. On March 19 this year, Iran attacked the Yanbu Port, causing a brief production halt.

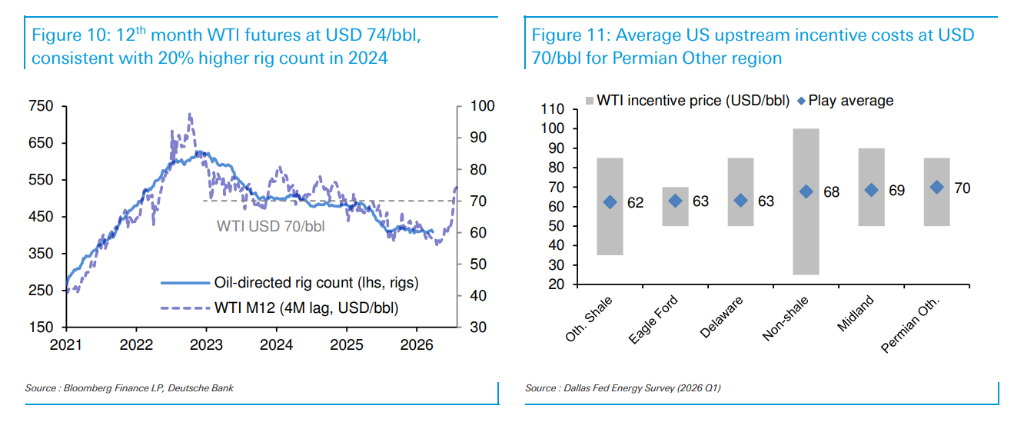

The US's own production increase: Insufficient to fill the gap in the short term.

Within the timeframes of Scenarios One to Three, the response speed of US production increases is too slow to have a substantial impact. Even within Scenario Four’s two-quarter window, the US upstream industry faces structural issues with the price curve—Bloomberg's WTI fair value currently averages about $73 per barrel in 2027 and approximately $70 in 2028, only slightly above or equal to the average upstream incentive cost in the Permian region.

More notably, from mid-March to the end of the month, the number of US oil drilling platforms slightly declined to its lowest level since December of the previous year. Deutsche Bank assessed that, under the current curve structure, it is unlikely that the US supply response will emerge at a sufficient scale and speed—unless Scenario Four materializes.

Seek more market analysis?Ask Futubull AI!Accurate answers, comprehensive insights, seize key opportunities!

Editor/Melody