Source: Jinduan

Author: Yaohua

Pop Mart may not be adept at meeting market expectations, but it precisely understands the emotions of this era.

On March 25, $POP MART (09992.HK)$a remarkable set of financial results that could easily make the market envious was released: revenue reached 37.12 billion yuan, a year-on-year increase of 184.7%; net profit amounted to 13.012 billion yuan, with an almost threefold increase; overseas revenue contributed more than 40%. However, when management announced their expectation of "no less than 20% growth in 2026" during the earnings call, the market sentiment quickly turned sour. Compared to nearly double the growth projected for 2025, the guidance of 20% was interpreted as a signal of "deceleration."

Panic spread rapidly. The day after the earnings call, the stock price plummeted.

Panic spread rapidly. The day after the earnings call, the stock price plummeted.

The tug-of-war between bulls and bears in the market essentially represents a collision of two different time horizons. However, the real crux of this divergence does not lie in who is right or wrong, but rather that both sides are seeing different facets of the same company.

01. The bears are not without basis, but Wang Ning has greater foresight.

From the perspective of market reactions, the logic behind the bearish stance appears valid.

Over the past few years, Pop Mart's share price surged over 35 times from its low point, with its valuation stretched to the extreme. Capital markets have consistently priced it based on expectations of "high growth."

Revenue soared from 4.5 billion yuan to 37.1 billion yuan, with an annual compound growth rate of 70%, while gross margin increased by 10.7%. This performance record would be regarded as nothing short of a growth miracle for any consumer goods enterprise with annual revenue exceeding 1 billion yuan, naturally stirring up the most enthusiastic market sentiment.

However, when the management issued a guidance of 20% growth during the earnings call, this expectation was instantly shattered — from nearly 200% growth, it plummeted to 20%. Calculations show that the expected increment for 2026 may be only 7.5 billion, less than one-third of 2025, causing the halo of high growth to fade abruptly.

For a market accustomed to the belief that 'growth is justice,' this is undoubtedly a dangerous signal.

At the same time, the market believes that the explosive growth over the past year was largely due to the sudden emergence of a super IP. For investors skilled in financial calculations, a question naturally arises: Is this explosion sustainable? How long will Labubu's popularity last? Does the proactive slowdown indicate an overestimation of the operational value of the IP?

These questions are not without merit. The trendy toy industry still carries certain characteristics of 'non-standard valuation,' and the lifecycle of an IP has always been difficult to predict. Coupled with the stock price already being at a high level and substantial profit-taking positions, it is only natural for the market to become 'skittish,' with capital choosing to vote with their feet.

From this perspective, the judgment of the short sellers is based on visible facts — a shift in growth gears, reliance on hit products, and elevated valuations — leading to a rational deduction.

What the shorts see is a downward revision of growth, but in our view, the market panic essentially stems from a misinterpretation of the statements made during the earnings call.

From the perspective of the bulls' logic, we can identify two more objective pieces of direct evidence:

First, on March 26th and 27th, Pop Mart repurchased approximately 5.92 million shares over two consecutive days. After the earnings call, Wang Ning demonstrated strong confidence in the long-term value of Pop Mart by using real funds to repurchase shares, providing the most direct response: the market panic is essentially a misjudgment.

Second, according to Pop Mart's financial report, there are no obvious signs of a slowdown on the operational side. Both the unit economics of individual stores and operational costs performed well, indicating that the downward revision of expectations announced during the earnings call was a proactive slowdown aimed at longer-term development.

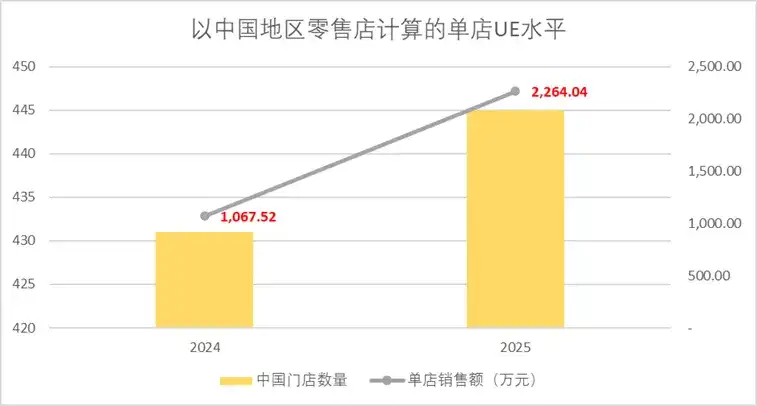

Upon closer inspection of the financials, it is not difficult to find that Pop Mart’s overall operational performance has not experienced any significant decline in organizational efficiency. Taking the domestic market as an example, retail store sales per store have more than doubled in a year.

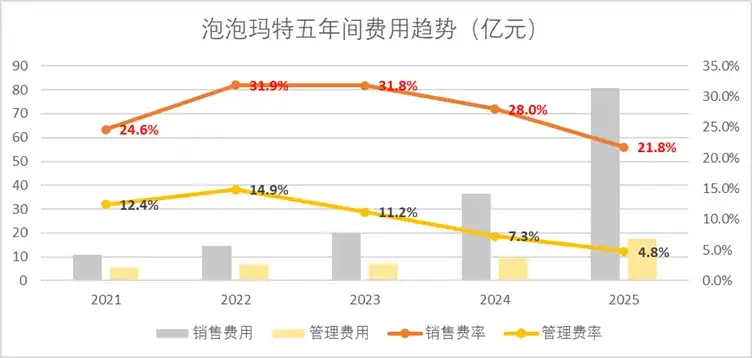

Moreover, Pop Mart has not encountered the issue of bloated expenses following its scale expansion. In 2025, the full-year sales expense ratio and management expense ratio were recorded at 21.8% and 4.8%, respectively, representing a decrease of 499 basis points and 250 basis points compared to 2024. The growth in expenses reflects a relatively reasonable and healthy increase under the context of scale expansion.

Therefore, the rapid growth in 2025 is actually$POP MART (09992.HK)$the release of a decade's worth of accumulation, representing a concentrated manifestation of operational capabilities. Acceleration of globalization, LABUBU becoming a world-class intellectual property (IP), and the growth of per-store efficiency—all these achievements are built upon the company's early ability to incubate hit products and its offline channel advantages.

This kind of competitive advantage derived from corporate operational accumulation must also be maintained over the long term. There is a concept in economics known as the 'capability trap.'

This theory was proposed by Harvard Business School professor Clayton Christensen in his seminal work *The Innovator's Dilemma*: A company’s past successful paths, accumulated capabilities, and established inertia often become the biggest obstacles when facing new-stage challenges.

This pattern has repeatedly played out throughout business history.

In 2008, Starbucks, which was still growing rapidly, experienced a decline in per-store sales. Over the previous decade, the number of Starbucks stores had soared from 1,000 to 7,000, with revenue growth at an astonishing pace. However, under prolonged high growth, it became inevitable that basic employee skills would be lacking, and product standards would decline, which in turn harmed the brand's reputation.

After Schultz, who had returned to rescue Starbucks for the third time, he voluntarily slowed down the pace of expansion and implemented a series of measures, including store closures and layoffs, retraining baristas, introducing semi-automatic coffee machines, improving the supply chain, and developing information technology systems. Although after lowering growth expectations, Wall Street analysts downgraded their ratings, claiming that Starbucks had “lost its growth momentum.” However, looking back with hindsight, the deliberate slowdown enhanced brand power, solidified the concept of the “third place,” and established the barriers that would define Starbucks’ success over the next decade. Facts have proven that Schultz was correct.

In 2026,$POP MART (09992.HK)$Pop Mart is experiencing a similar inflection point. Although Pop Mart has not yet shown obvious operational difficulties due to scale expansion, the principle of 'mending the net during leisure times and repairing the roof on sunny days' is always relevant.

As Wang Ning remarked during the earnings call, Pop Mart is akin to a novice race car driver abruptly thrust into an F1 competition. In the process of navigating at ultra-high speeds, both the driver and the vehicle are under immense pressure.

The driver understands that this speed cannot be sustained by short-term momentum from traffic dividends. If acceleration continues without upgrading the organization, optimizing processes, and strengthening the middle platform, the company will inevitably fall into a 'capability trap.' What Wang Ning seeks is healthy development rather than valueless growth.

In an era when the capital market is obsessed with chasing 'high-growth narratives,' Pop Mart’s decision to proactively lower expectations aligns with a long-term strategic vision, rather than signaling a simple decline in growth rate. For value investors, the market's skittish reactions lack logical grounding.

02. Actively adjusting pace is a required course for enduring enterprises.

"The greatest danger in times of turbulence is not the turbulence itself, but to act with yesterday’s logic" — Peter Drucker.

In fact, the proactive adjustment of growth rates to maintain core corporate value is a common practice among Western companies:

In 2016, Vox reported on Tim Cook’s transformation shortly after he took over Apple. Cook first slowed the pace of innovation in Apple’s product lines and then explained to Wall Street that Apple might lower its growth expectations. In response to Cook’s changes, public opinion was overwhelmingly pessimistic at the time. Forbes columnist Peter Cohen even wrote an article titled "Two Moths Eating Away at Apple’s Core," criticizing the slowdown in innovation post-Steve Jobs. The capital markets also voted with their feet. For a long period after Cook took office, Apple’s stock performance remained lackluster.

However, looking back ten years later, it was precisely this deliberate deceleration that built Tim Cook’s supply chain empire, propelling Apple’s market value from $300 billion to $3 trillion. Those who once mocked Cook for being 'only good at supply chain management' eventually came to understand the profound significance of his strategy.

In 2005, when Robert Iger assumed the role of CEO at Disney, the company was mired in an 'overabundance trap' of intellectual properties (IP). To chase market trends, Disney had released a slew of sequels and spin-offs within a few years—The Lion King 2, The Little Mermaid 2, The Hunchback of Notre Dame 2… Each brought short-term revenue but eroded the brand value of these IPs. Audiences grew fatigued, and the media ridiculed Disney for 'milking its own legacy.'

Iger did something that seemed 'counterintuitive' at the time: he deliberately slowed the pace of IP development and reduced the output of low-quality content. He disbanded the strategic planning department and concentrated resources on a select few projects with real potential. Simultaneously, he spearheaded a series of strategic acquisitions—Pixar, Marvel, Lucasfilm, and 21st Century Fox—infusing Disney with a fresh wave of IP vitality.

This decision was not understood by everyone at the time. The capital market was accustomed to Disney's rhythm of releasing more than a dozen animated films annually, and the sudden 'slowdown' triggered considerable doubts. However, looking back ten years later, it was precisely this proactive 'contraction' that helped Disney avoid the trap of over-exploiting intellectual property (IP). Later successes such as Frozen, Zootopia, and the Avengers series each became global cultural phenomena.

Perhaps the hallmark of a mature enterprise lies in its ability to proactively adjust its pace. From the current perspective, Pop Mart, after experiencing explosive growth, has also grown more mature.

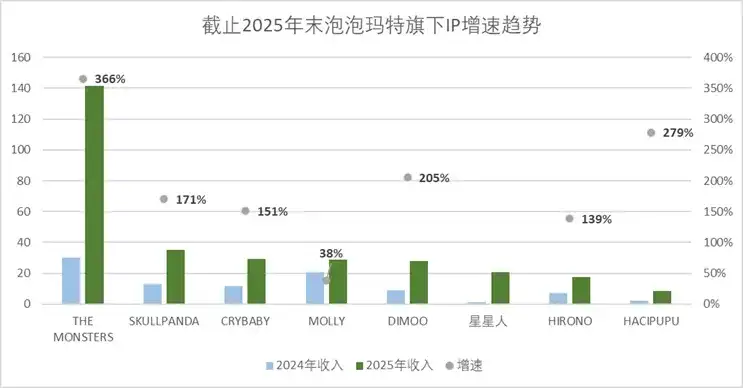

In 2025, LABUBU became a world-class super IP, contributing revenue of 14.1 billion yuan, a year-on-year increase of 366%. This is undoubtedly the most dazzling 'hit product' since Pop Mart’s establishment. However, Pop Mart clearly understands that relying on the breakout success of a single IP cannot sustain an entire ecosystem. Over the past few years, the company has been working hard to address this issue.

Wang Ning expressed a similar sentiment during the earnings call: 'Pop Mart is not just about LABUBU; even without LABUBU last year, we still achieved extremely rapid growth.' Behind this statement lies the company’s ongoing strategic shift from reliance on a single hit product to building a collaborative ecosystem with multiple IPs, multiple categories, and multiple channels.

The data from 2025 already shows the effectiveness of this transformation. The company now has six IPs generating revenue exceeding 2 billion yuan, and 17 IPs surpassing 100 million yuan. SKULLPANDA contributed 3.54 billion yuan, while CRYBABY, MOLLY, DIMOO, and Star Figures all exceeded 2 billion yuan. Aside from the older IP, Molly, the growth rates of the other IPs all surpassed 100%. The new IP, Star Figures, launched in 2024, achieved year-on-year growth of over 1,600%, indicating that Pop Mart is transitioning from 'single-point explosions' to 'matrix-driven' growth.

In other words,$POP MART (09992.HK)$Having accumulated sufficient capabilities to replicate blockbuster IPs does not mean there is no potential for explosive growth. However, if the company were to blindly pursue scale expansion at this stage, uncontrollable product issues could arise, inevitably depleting the lifespan of its IPs. The unchecked expansions of Disney and Starbucks around the millennium serve as prime cautionary examples. Wang Ning clearly recognizes this.

From Apple to Disney, from Jobs to Cook, from Iger to Wang Ning — the fundamental logic of business has never changed: great products can make a company, but only efficient organizations can endure through cycles.

The construction of capabilities never relies on short sprints; rather, it depends on the long-term philosophy of 'slow is fast.'

03, No need to worry, Pop Mart understands the emotions of the times best.

If viewed within the context of the broader cycles of the cultural industry,$POP MART (09992.HK)$Investors need to understand that Pop Mart should be extracted from the 'growth narrative' and placed into the 'emotional narrative'.

The cultural industry is one of the few sectors in the history of human commerce with an 'evergreen cycle.' As Professor David Hesmondhalgh of the University of Leeds, UK, stated in his book *The Cultural Industries*, the key difference between the cultural industry and other industries lies in the fact that it does not produce disposable functional products but rather 'texts and symbols that can be repeatedly consumed and continuously evoke emotional resonance,' making it one of the best businesses in human society.

The value of cultural products lies in the meaning, emotion, and identity attached to them—this gives the cultural industry an inherent resilience to 'transcend cycles.'

Whether it's Disney's Mickey Mouse, Marvel's superheroes, Hello Kitty, or Gundam, the life cycles of these IPs often span half a century or even longer. Their ability to transcend cycles is precisely due to the sustained emotional connections they build with users.

This emotional connection cannot be achieved through a sprint; it can only be built over time.

Mitsuru Miura, a renowned Japanese socio-economic scholar, expressed a similar view in his concept of the 'fifth era of consumption': after the sharing and minimalism of the fourth consumption era, people began to seek their 'true selves,' pursuing consumption that brings emotional resonance, spiritual fulfillment, and self-pleasure. This type of consumption is no longer about showing off or seeking belonging but about 'making oneself happy,' which has become the hallmark of this era.

$POP MART (09992.HK)$Pop Mart stands precisely at the intersection of this era. The explosive popularity of Molly and Labubu has proven to the market that Pop Mart is currently the consumer company that best understands this era.

Wang Ning said during the earnings call: 'One of the biggest differences between us and many consumer goods companies is that, even when entire families visit our stores, regardless of age, everyone will have a great experience.' This statement demonstrates to the market that Pop Mart has a deep understanding of 'self-pleasing consumption' and 'introspective consumption,' allowing consumers of all ages to find emotional resonance within its offerings.

In 2026, Pop Mart remains committed to this vision: Phase 1.5 of the theme park is nearing completion, the official announcement of the *THE MONSTERS* film series has been made, global exhibitions are being held in multiple cities, and costumed Labubu characters have appeared in the Macy's Thanksgiving Day Parade and on the covers of fashion magazines—all aimed at fostering deeper emotional connections between IPs and users.

In summary, while market bears see a slowdown in speed, Wang Ning sees a shift in the times. The growth logic of IPs and consumer goods has already changed as the cycle turned. It is essential to respect the market, understand the essence of self-pleasure, focus more on delivering higher-quality experiences, and strengthen emotional ties with consumers so that the stories of IPs can endure for longer.

Rest assured, Pop Mart may not be adept at meeting market expectations, but it truly understands the emotions of this era.

Editor /rice