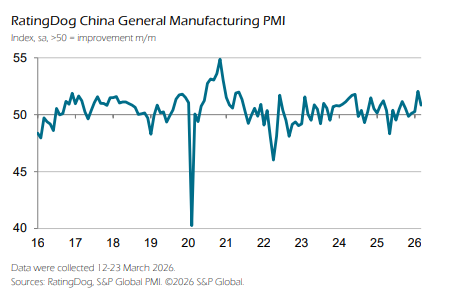

China's RatingDog Manufacturing PMI for March slowed significantly from February's 52.1, remaining the second-fastest level in nearly six months. However, input prices accelerated to their highest level since March 2022, and supplier delivery times lengthened at a pace not seen in over three years. Yao Yu, founder of RatingDog, stated that escalating international geopolitical conflicts are exacerbating volatility in the bulk raw materials market, and this imported inflation factor is expected to pose a 'severe test' to manufacturers’ costs in April.

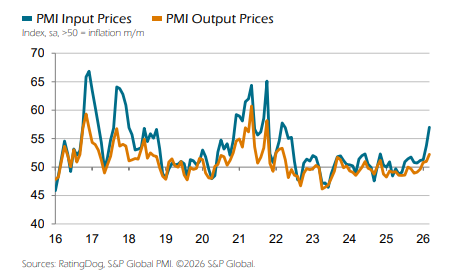

The RatingDog Manufacturing PMI report for China in March indicated that inflationary pressures were the highest since March 2022.

On April 1, S&P Global and RatingDog jointly released China’s latest Purchasing Managers' Index (PMI), showing that the RatingDog Manufacturing PMI for March stood at 50.8, remaining above the 50-point threshold for the fourth consecutive month, but fell notably from February's 52.1.

Meanwhile, input price inflation accelerated to its highest level since March 2022, with supplier delivery times lengthening at their fastest rate in over three years.

Meanwhile, input price inflation accelerated to its highest level since March 2022, with supplier delivery times lengthening at their fastest rate in over three years.

Yao Yu, founder of RatingDog, noted that although domestic policy remains broadly stable, ongoing international geopolitical tensions continue to drive up oil prices and amplify volatility in the bulk raw materials market. This imported inflationary pressure is expected to present a 'severe test' to manufacturers’ costs in April.

Expansion momentum slows, but employment records longest continuous increase in five years.

All five sub-indices of the PMI made positive contributions to the overall index in March.

New orders continued to grow, benefiting from recovering market demand, customer expansion, business growth, promotional activities, and improved price competitiveness. However, the pace of expansion slowed from February’s multi-year high, remaining the second-fastest level in nearly six months. New export orders also registered growth, albeit at a slower pace than the previous month.

Output expanded for the fourth consecutive month, with both consumer goods and intermediate goods producers reporting growth, while investment goods output remained largely unchanged. Due to slower production growth and continued inflow of orders, the backlog of unfilled orders increased at a faster rate, which companies attributed to rising customer demand, capacity constraints, and personnel changes.

In terms of employment, the manufacturing sector recorded job growth for the third consecutive month, marking the longest hiring streak since mid-2021. Procurement activity expanded simultaneously, though the rate of growth also moderated compared to February.

Price pressures surged sharply, with supply chains experiencing the greatest disruption in over three years.

The cost side was the most prominent risk signal in the March report.

Input price inflation accelerated significantly, reaching its highest level since March 2022 and surpassing the survey's long-term average. Driven by this, output price increases expanded to a four-year high, also above historical averages.

On the supply chain front, delivery times extended for the first time in five months, with the increase being the largest since December 2022. Companies attributed supplier delays to supply chain disruptions, elevated and volatile raw material prices, and constrained supplier capacity.

In terms of inventory, procurement stock increased slightly, consistent with the slowing pace of output; finished goods inventory contracted marginally, reflecting that firms utilized existing inventory to fulfill orders to some extent.

Production outlook remains optimistic, shaped by complex domestic and external dynamics.

Despite rising cost pressures, surveyed manufacturers maintained a positive outlook on production prospects over the next 12 months.

Sources of confidence include continued improvement in customer demand, investments in capacity and new products, efficiency gains, and government policy support. Overall optimism has declined from its February peak but remains stronger than in December last year and January this year.

Yao Yu pointed out that the macro environment presents a more complex picture for the manufacturing sector.

At the domestic level, the 2026 Government Work Report set a flexible GDP growth target range of 4.5% to 5%, broadly in line with market expectations and reflecting a policy orientation of 'stability with progress.' This is expected to provide moderate support to manufacturing activities.

Internationally, ongoing geopolitical conflicts have kept oil prices at elevated levels while exacerbating volatility and cost pressures in key raw material markets.

The data collection period for this survey was from March 12 to 23, 2026, covering approximately 650 manufacturers and jointly compiled by RatingDog and S&P Global.

Editor/Melody