The annual recurring revenue (ARR) of Zhipu's open platform API has reached 1.7 billion yuan, increasing approximately 60-fold compared to 12 months ago. JPMorgan noted that the token price of Zhipu's API platform has surged by 83% year-to-date, while demand continues to accelerate—both volume and price are rising simultaneously. Against the backdrop of intensifying price competition in China’s large model market, this phenomenon is extremely rare and directly demonstrates that Zhipu has established substantial pricing power in high-value scenarios such as programming and intelligent agents.

$KNOWLEDGE ATLAS (02513.HK)$ AI delivered a report card that caught Wall Street's attention, with annual revenue more than doubling year-over-year. However, what truly shocked the market was a real-time figure disclosed after the earnings release:

As of March 31, 2026, the company’s open-platform API Annual Recurring Revenue (ARR) had surged to approximately RMB 1.7 billion (about USD 250 million), representing an over 2.4-fold increase from around RMB 500 million at the end of 2025 and a nearly 60-fold growth compared to 12 months prior. Both Morgan Stanley and JPMorgan identified this as the biggest surprise in this earnings report. More convincingly, this growth was not purely driven by a 'volume-over-price' strategy.

According to Zuitrade, JPMorgan particularly highlighted in its research note that the token price for Zhimap API platform had risen 83% year-to-date, while demand continued to accelerate — simultaneous growth in both volume and price. This phenomenon is extremely rare amid the current intense price wars in China’s large model market, directly confirming Zhimap’s substantial pricing power in high-value scenarios such as programming and intelligent agents.

According to Zuitrade, JPMorgan particularly highlighted in its research note that the token price for Zhimap API platform had risen 83% year-to-date, while demand continued to accelerate — simultaneous growth in both volume and price. This phenomenon is extremely rare amid the current intense price wars in China’s large model market, directly confirming Zhimap’s substantial pricing power in high-value scenarios such as programming and intelligent agents.

From a profitability perspective, Zhimap’s loss structure is undergoing a qualitative transformation. In 2025, the company’s R&D expenditure reached approximately RMB 3.2 billion, roughly equivalent to its adjusted net loss. This indicates that the gross profit generated by existing models is already sufficient to cover sales and administrative expenses — core operations have achieved breakeven at the contribution margin level, and all losses essentially represent proactive investments in next-generation model iteration.

JPMorgan believes that with triple-digit revenue growth continuing and API gross margins expanding steadily (from just 3% in 2024 to 19% in 2025), the timeline for profitability is becoming increasingly clear, with expectations that the company will turn profitable by 2029.

ARR Explosion: From 'Year-End Target' to 'Already on Track'

The most critical highlight of this earnings report is the ARR data disclosed by Zhimap. As of March 31, 2026, the ARR for the open-platform API had reached approximately USD 250 million, representing a 6.4-fold increase from the beginning of the year and a nearly 60-fold growth compared to 12 months prior.

Management has set a year-end target of USD 1 billion, and current progress suggests that this goal is not an unattainable vision but rather a rapidly materializing trajectory.

Morgan Stanley, in its research report, listed the better-than-expected ARR performance as a 'core event reinforcing investment logic' and characterized it as a 'Major Surprise.'

In terms of business structure, cloud deployment revenue in the second half of 2025 grew by 431% year-over-year, far outpacing the 57% growth rate for private deployments. The proportion of cloud-based business in total revenue also rose rapidly from single digits to 26%. This structural shift signifies that Zhimap’s business model is evolving from project-based delivery, which is asset-heavy and low-repeat, toward a subscription-based API economy that is asset-light and highly sticky.

Dual Growth in Token Volume and Price: Pricing Power is the Scarcest Signal

Against the backdrop of widespread 'price undercutting' in the domestic large model sector, Zhipu's ability to achieve an 83% increase in token prices year-to-date while maintaining rising demand is a phenomenon worthy of in-depth analysis.

JPMorgan analyst Olivia Xu explicitly noted in her research report that simultaneous growth in volume and price is the clearest signal of growth driven by 'genuine model competitiveness' and 'high-value workloads.'

Specifically, customers in coding and agent-related scenarios have transitioned their payment logic from 'pay-per-use' to 'paying for task completion quality, throughput, and stability'—a fundamentally higher-dimensional business relationship. When clients are willing to pay a premium for better outcomes rather than merely seeking the lowest unit price, pricing power has quietly taken shape.

From the perspective of model iteration, Zhipu’s rapid evolution from GLM-4.5/4.6/4.7 to GLM-5, along with its continued investment in production-grade coding, long-context reasoning, and multi-step execution stability, forms the technical foundation supporting this pricing power.

Gross Margin Inflection Point: Cloud Business Transitions from Loss to Profitability

In the second half of 2025, the gross margin of Zhipu’s cloud deployment business surged from -0.4% in the first half to 22.4%, marking the formal crossing of the profitability threshold into a positive cycle driven by economies of scale.

From a group-wide perspective, the gross margin of the open platform API increased from 3% in 2024 to 19% in 2025, representing a 16-percentage-point improvement.

JPMorgan forecasts that as scale continues to expand and model inference efficiency improves, there remains significant room for further gross margin growth. According to their predictive model, the group’s overall gross margin will stabilize around 31% in 2026, rise further to 36% in 2027, and reach 37% in 2028.

Notably, the full-year gross profit for 2025 was approximately 297 million yuan, while combined sales and administrative expenses totaled about 896 million yuan, with R&D expenditure reaching approximately 3.2 billion yuan. Excluding R&D investments, gross profit has essentially covered non-R&D operational costs, indicating that Zhipu’s core business model has achieved self-sustaining capabilities. The current losses are entirely attributable to strategic R&D investments rather than flaws in the business model itself.

Private Deployment: Upgrade Potential of Existing Assets

In addition to the explosive growth of cloud-based API services, Zhipu's established foundation in private deployment within China’s regulated industries is also a key pillar of JPMorgan’s investment thesis. By the second half of 2025, revenue from private deployments reached 372 million yuan, representing a year-over-year increase of 57%, with an absolute scale more than double that of its cloud-based operations.

JPMorgan believes this extensive base of existing customers holds unique strategic value: as foundational models continue to iterate and improve, these deployed clients have a natural need for upgrades, which could evolve into recurring, predictable upgrade-driven revenue streams.

The heightened sensitivity to data security in regulated sectors such as finance, government services, and energy ensures that private deployment will remain an irreplaceable delivery model in the foreseeable future, forming a structural competitive moat for Zhipu distinct from purely cloud-based competitors.

JPMorgan significantly raises target price

JPMorgan maintains its "Overweight" rating and raises the target price from 800 Hong Kong dollars to 950 Hong Kong dollars, based on a 30-times forward price-to-earnings ratio for 2030, discounted to the end of 2026 using a weighted average cost of capital (WACC) of 15%. The 30-times valuation premium primarily reflects the company’s projected annual compound revenue growth rate exceeding 100% from 2026 to 2030.

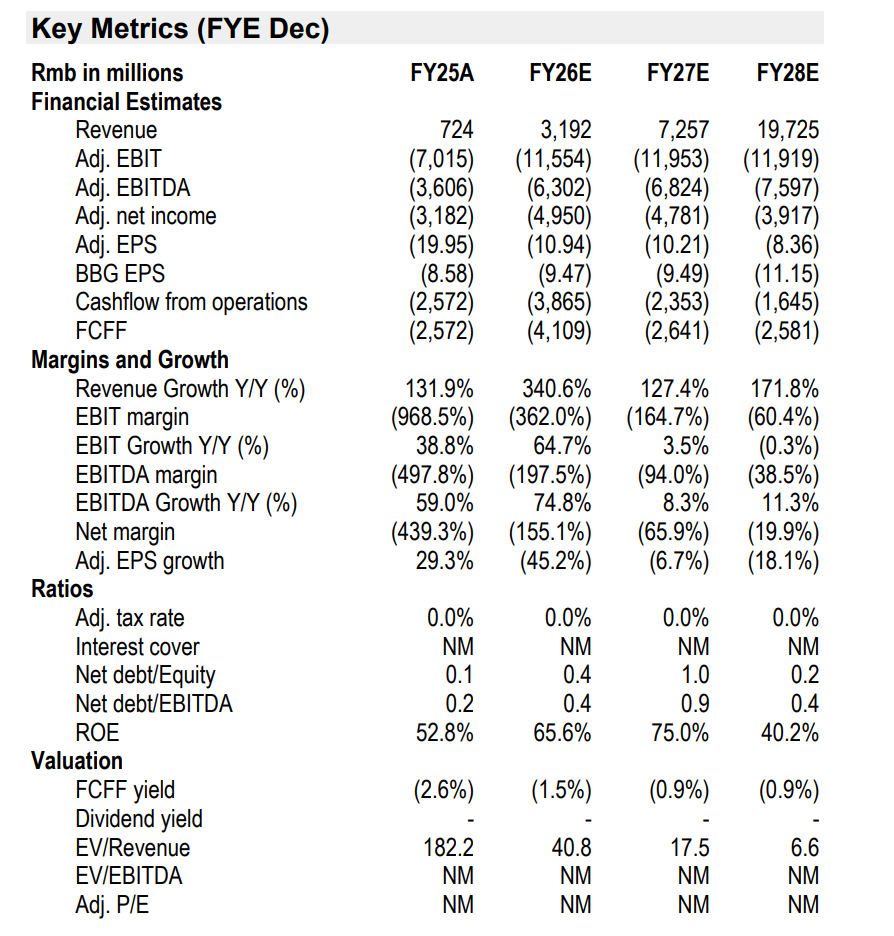

According to updated forecasts, Zhipu’s revenue for 2026 is expected to reach 3.192 billion yuan (a year-over-year increase of 341%), further rising to 7.257 billion yuan in 2027, surging to 19.725 billion yuan in 2028, and potentially surpassing 98.8 billion yuan by 2030. Adjusted net profit is forecast to turn positive by 2029 at 2.822 billion yuan and increase further to 20.36 billion yuan in 2030.

Morgan Stanley also maintains an "Overweight" rating with a target price of 560 Hong Kong dollars, employing a discounted cash flow (DCF) valuation methodology assuming a WACC of 15% and a perpetual growth rate of 3%, corresponding to approximately 53 times price-to-sales ratio for 2027. While there are methodological differences between the two institutions, their assessments of Zhipu’s long-term value are highly consistent.

Editor/KOKO