U.S. retail sales increased by 0.6% month-over-month in February, and the 'small non-farm payroll' figure for March exceeded expectations. Although short-term data appears favorable, the surge in oil prices by $4 due to tensions in the Middle East, along with turbulence in the U.S. stock market, is emerging as a potential 'recovery killer.'

Data released by the U.S. Department of Commerce on Wednesday showed that, driven by a rebound in automobile sales and warmer weather, retail sales in the United States grew by 0.6% month-over-month in February, slightly higher than market expectations. Although January's data had been slightly revised downward due to extreme weather, the rebound signal in February indicated that consumer groups, led by high-income households, still maintained strong spending momentum.

However, behind the impressive retail data lies a hidden concern. Due to the situation in the Middle East, global oil prices have surged over 50%, with the national average retail gasoline price in the U.S. breaking above $4 per gallon for the first time in three years.

The market widely worries that if energy prices continue to rise, it will not only offset the benefits brought by tax cuts but also weaken household consumption capacity in the coming months. Additionally, affected by the regional conflict that has lasted for more than a month, the S&P 500 Index and Dow Jones Industrial Average both recorded their largest single-month declines in recent years in March, which may further suppress consumer willingness as household net worth shrinks.

The market widely worries that if energy prices continue to rise, it will not only offset the benefits brought by tax cuts but also weaken household consumption capacity in the coming months. Additionally, affected by the regional conflict that has lasted for more than a month, the S&P 500 Index and Dow Jones Industrial Average both recorded their largest single-month declines in recent years in March, which may further suppress consumer willingness as household net worth shrinks.

In terms of employment, a report released by the human resources agency ADP on Wednesday showed that private sector employment increased by 62,000 people in March, surpassing the expected 39,000.

From an industry perspective, employment growth exhibited clear structural characteristics. Healthcare, education, and construction industries almost contributed all of the increase, with the education and healthcare sectors adding 58,000 jobs and the construction industry adding 30,000. In contrast, trade, transportation, and utilities sectors lost 58,000 employees, while manufacturing cut 11,000 positions.

Notably, in the service-oriented U.S. economy, March witnessed an unusual balance between job growth in goods production and services. From the perspective of business size, small businesses with fewer than 50 employees became the main force in hiring, expanding their workforce by 85,000 in a single month, while medium and large enterprises performed poorly, collectively cutting approximately 24,000 jobs.

Regarding salary performance, wage growth for retained employees remained at 4.5% year-over-year, while salary growth for job switchers rebounded to 6.6%, reflecting continued tightness in certain segments of the labor market.

ADP Chief Economist Nela Richardson pointed out that the healthcare industry is profoundly reshaping the current labor market landscape, and small businesses are recruiting against the trend partly to meet residents' demand for 'side gigs' or second jobs under inflationary pressures.

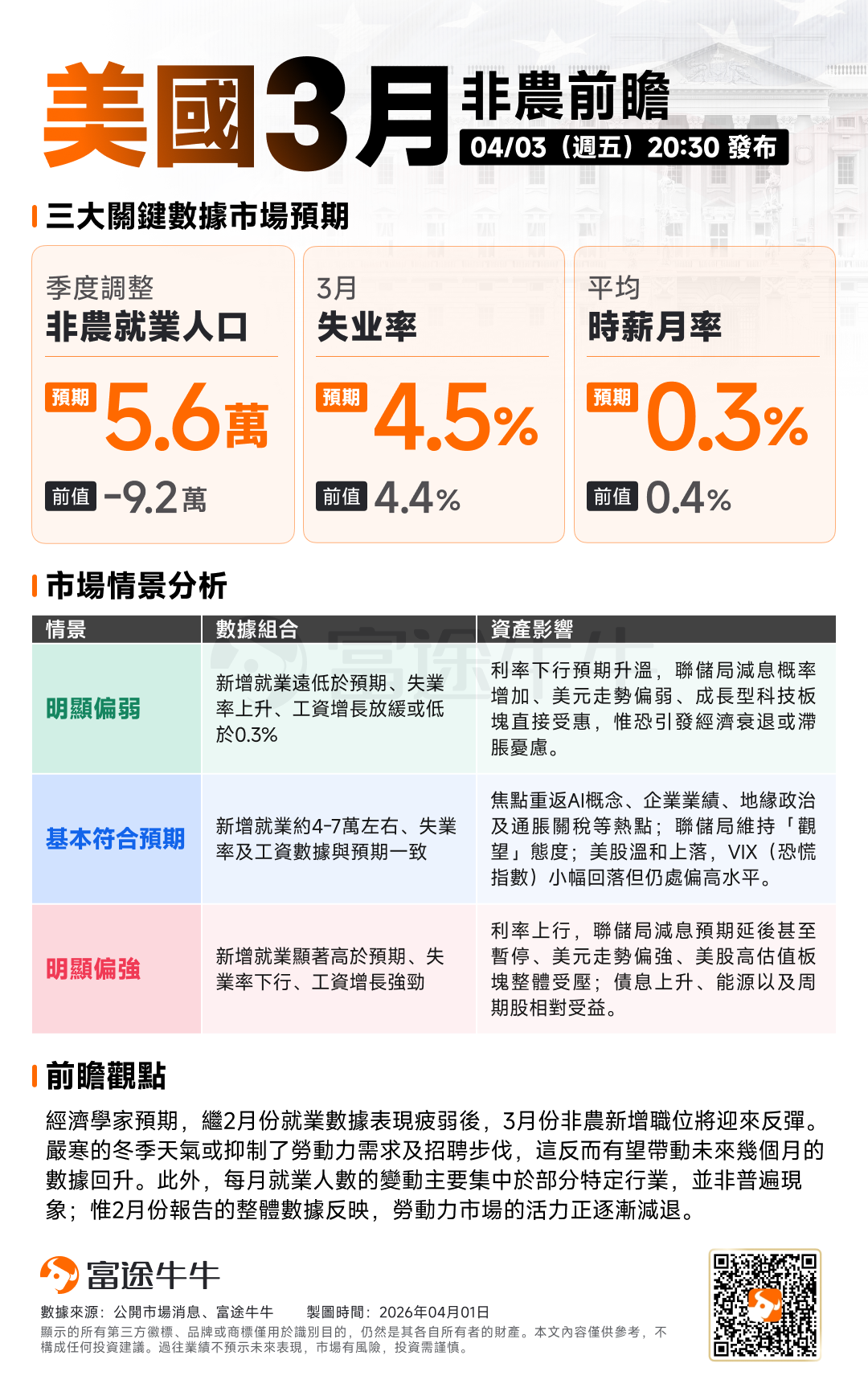

This Friday, the U.S. Bureau of Labor Statistics will release the highly anticipated nonfarm payrolls report. Wall Street currently expects that, following an unexpected decline in February, job growth is likely to rebound to an increase of 56,000 in March, with the unemployment rate projected to remain at 4.5%.

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Editor/Lambor