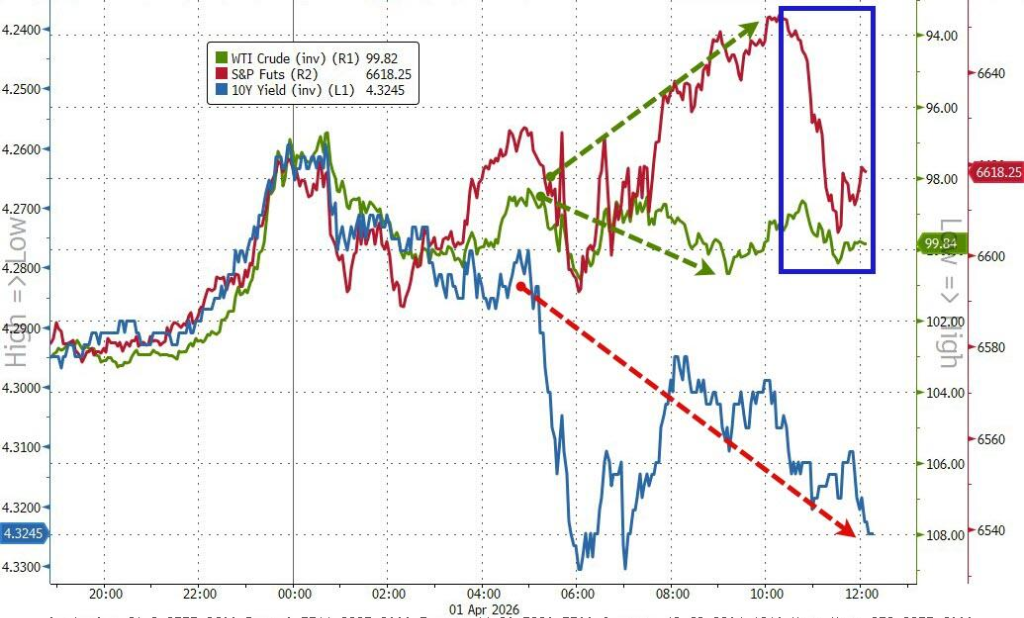

The Nasdaq Composite Index closed up 1.16%, having risen as much as 1.8% during intraday trading. The Philadelphia Semiconductor Index advanced for the second consecutive trading day, with the storage stock sector surging 8.2% in a single day, marking the second-largest daily gain on record. The energy sector remained under pressure throughout the session, dropping nearly 5% at one point to reach its lowest level in over a week; airline stocks rose amid a pullback in oil prices. U.S. Treasury yields initially fell but later rebounded, the U.S. dollar continued to weaken, and Brent crude oil fluctuated around the $100 mark.

Investors are betting that the US-Iran conflict is nearing an end, with US stocks rising for a second consecutive trading day. Technology stocks drove the Nasdaq up by more than 1%, while energy stocks fell under pressure. European equities generally rose on Wednesday, and emerging market stocks recorded their largest gains since 2022.

Meanwhile, US Treasury yields initially fell before rebounding, the dollar continued to weaken, and Brent crude oil fluctuated near $100 per barrel.

Trump stated on the same day that US military actions have rendered Iran incapable of possessing nuclear weapons, and the US will soon withdraw from Iran, but if necessary, it could carry out 'targeted strikes' again.

He will deliver a nationwide address on the issue of the Iranian war later in the evening, providing important updates on the situation.

Thomas Martin, Senior Portfolio Manager at Globalt Investments, said: 'Trump's statements often change. The market is trying to interpret his true intentions. Investors want to hear positive signals and hope the war will end.'

Against the backdrop of investors betting that US and Israeli military actions against Iran may soon come to an end, US stocks have risen for a second consecutive trading day. Over the past month, the conflict caused disruptions in oil transportation through the Strait of Hormuz, leading to a sharp spike in energy prices and triggering global inflation concerns.

On Wednesday, April 1, the military strikes by the United States and Israel against Iran entered their 33rd day, with the situation advancing amid intense exchanges of fire and diplomatic probing.

According to CCTV, US President Trump posted on social media on Wednesday claiming that Iran's 'new regime president' had requested a ceasefire, but the US would only consider it 'when the Strait of Hormuz is reopened and unobstructed,' otherwise, it would continue to strike Iran. Crude oil prices fell sharply, and US stocks opened higher.

Iran responded by stating that the strait would not be open to enemies, and the claimed ceasefire request was entirely fabricated. Oil prices quickly rebounded, and stock markets came under pressure accordingly.

During US stock trading hours, White House officials revealed that Trump would reiterate the timeline to end the war within two to three weeks during his nationwide address at 9 PM (Beijing time, April 2nd, 9 AM), which once again eased market sentiment.

After midday trading in the US stock market, according to CCTV citing US media reports, the US Department of Defense is doubling the number of A-10 attack aircraft deployed in the Middle East to enhance its strike capabilities against Iran and its proxy forces.

Market risk aversion briefly intensified, with the broader US stock market narrowing its intraday gains. The S&P 500 index, which had risen by as much as 1.2%, trimmed its gain to 0.72%, while the Nasdaq Composite closed up 1.16% after rising 1.8% at one point.

Thomas Martin, Senior Portfolio Manager at Globalt Investments, stated:

Trump’s statements themselves keep changing, and the market is trying to interpret what he really means. Meanwhile, the market’s hope is positive — it wants the war to end.

Michael Bailey, Director of Research at wealth management firm FBB Capital Partners, stated:

The strong rebound over the past two days may be due to savvy investors betting on easing tensions in the Middle East, or it could stem from market desperation driven by fear of missing out on a recovery opportunity. However, at elevated levels, any mixed or negative news could lead to a pullback.

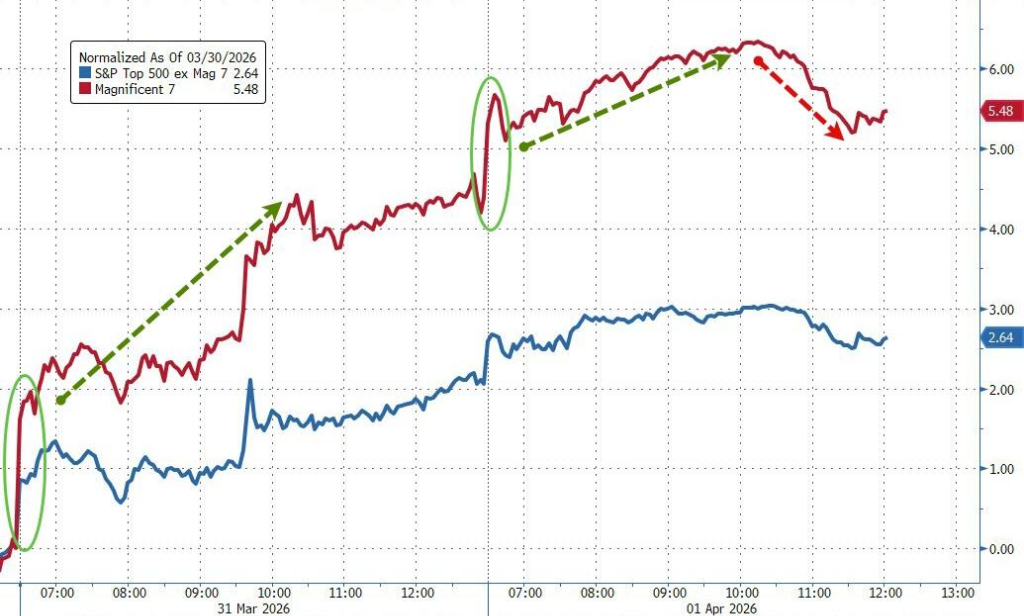

Despite multiple instances of 'rally-and-reversal' movements during the session, the technology sector remained the core driver of this rebound. Google surged over 3%, and the Mag 7 collectively delivered their best two-day performance in nearly a year.

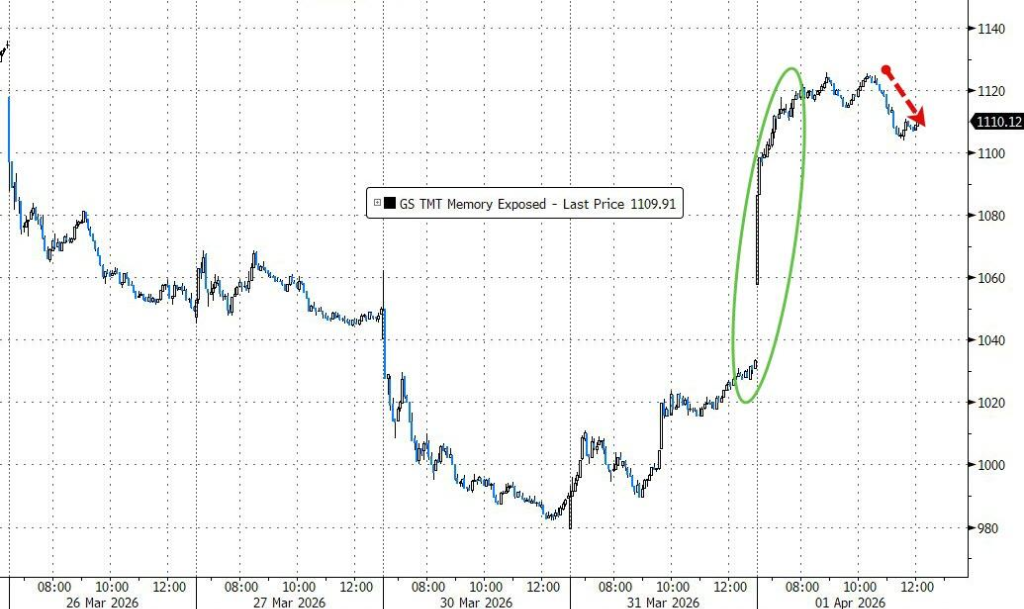

The Philadelphia Semiconductor Index rose for the second consecutive trading day, with the memory stock sector surging 8.2% in a single day, marking its second-largest daily gain on record.

In contrast, the energy sector remained under pressure throughout the day, falling nearly 5% at one point to reach its lowest level in more than a week; airline stocks rose as oil prices retreated.

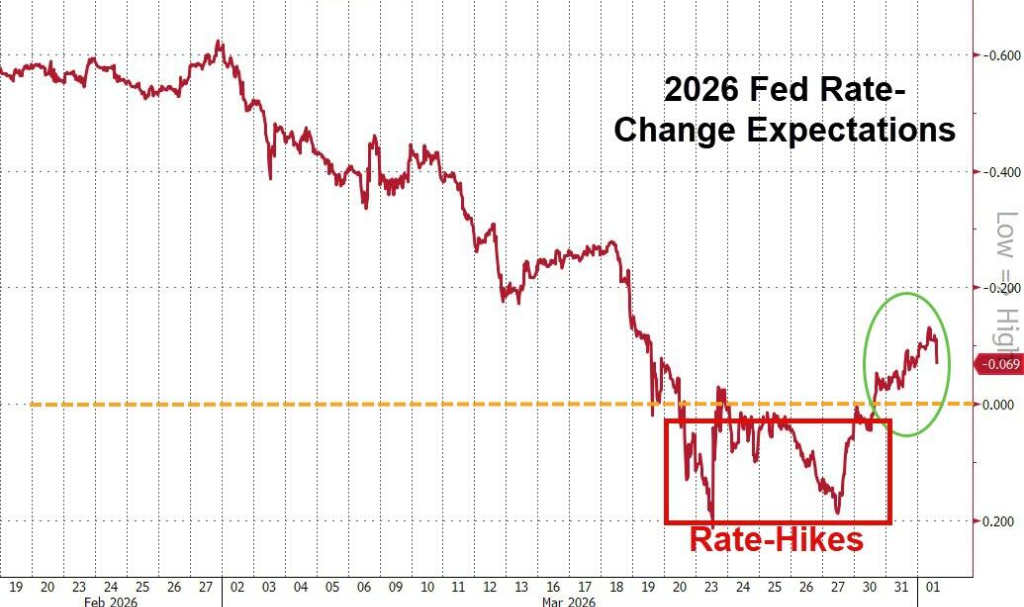

Notably, the economic data released that day showed overall strength in the U.S. economy. According to Wall Street News, the 'small non-farm' ADP employment report significantly exceeded expectations, while the month-on-month increase in February retail sales posted the largest gain in eight months; the ISM Manufacturing Index for March reached 52.7, hitting a three-year high.

However, the ISM manufacturing prices paid sub-index surged, indicating rising inflationary pressures, and this was before the full impact of the war situation on energy costs.

As a result, the market's expectation of an interest rate cut by the Federal Reserve within the year has slightly narrowed. The yields on key maturities of U.S. Treasuries initially fell by 5 basis points across the board but then rebounded in a V-shaped recovery to close flat.

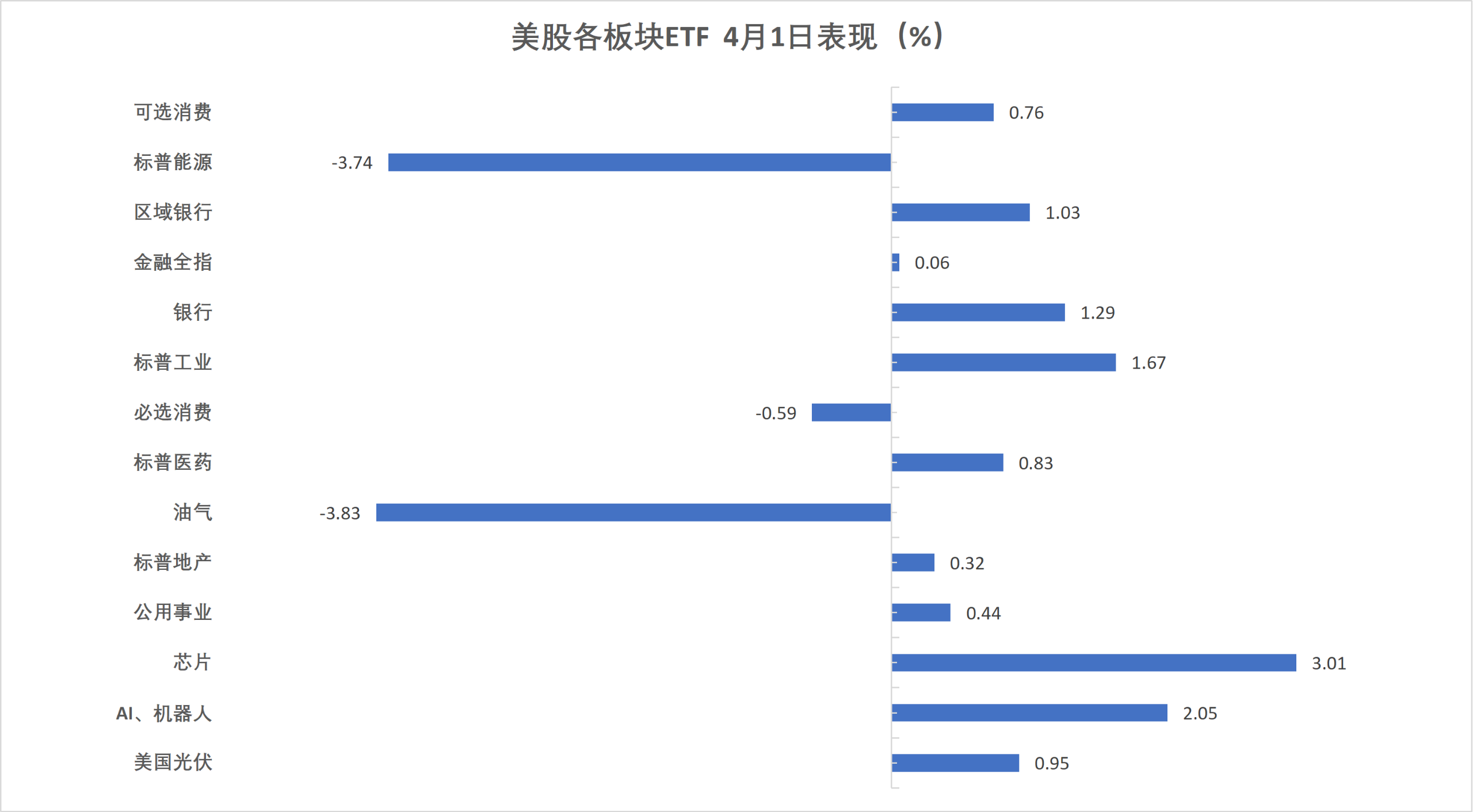

On Wednesday, the three major U.S. stock indexes continued their rebound and closed higher. The airline industry ETF rose 2.6%, leading gains among U.S. sector ETFs alongside the semiconductor ETF. The energy sector ETF fell more than 3.7%. Micron Technology surged 8.88%, while Western Digital soared 10%. Eli Lilly and Co gained 3.78% after the FDA approved its GLP-1 weight-loss drug.

U.S. Equity Benchmark Indices:

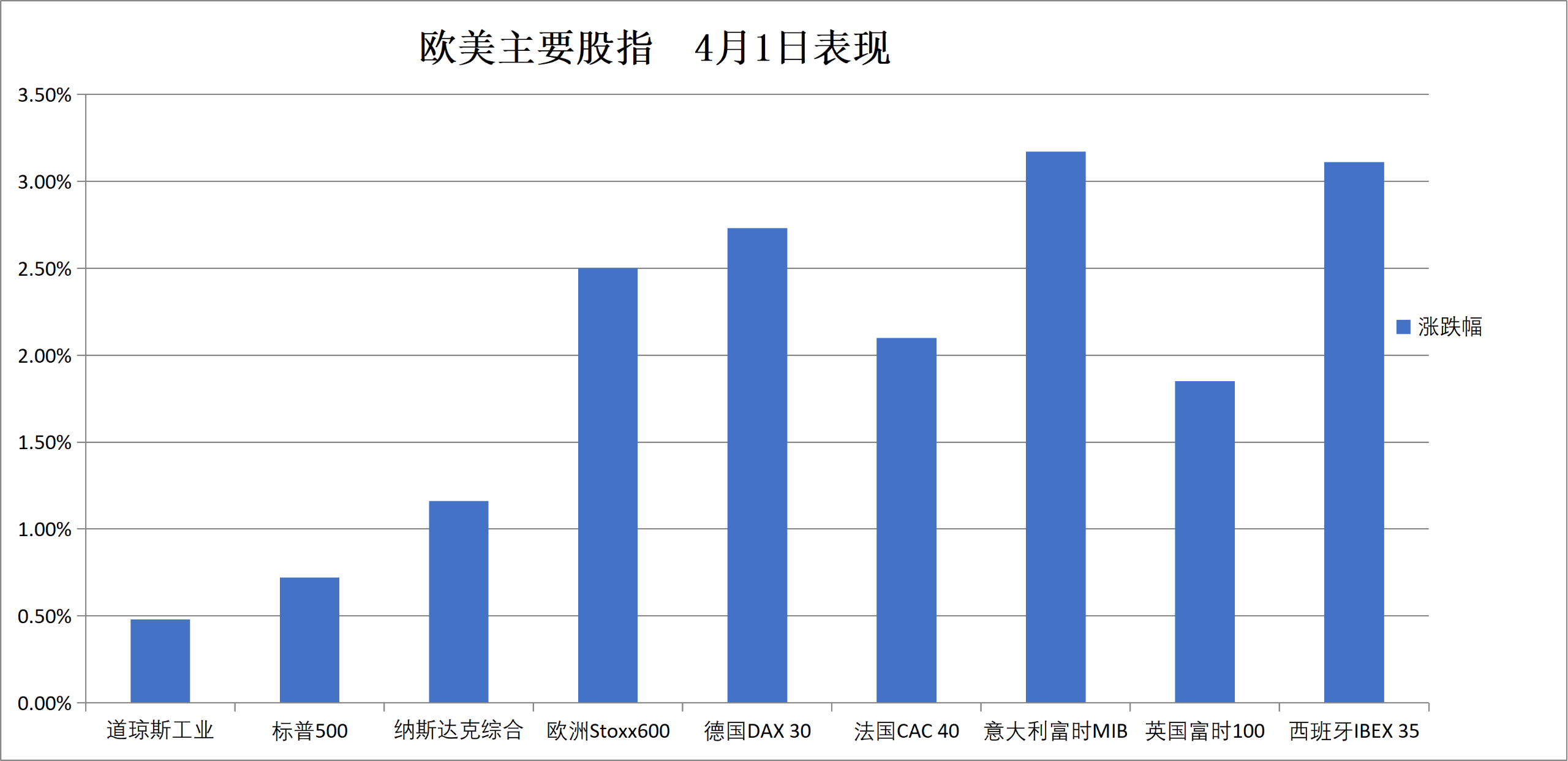

The S&P 500 Index rose 46.80 points, or 0.72%, to close at 6575.32.

The Dow Jones Industrial Average rose 224.23 points, or 0.48%, to close at 46565.74.

The Nasdaq Composite Index rose 250.319 points, or 1.16%, to close at 21840.947. The Nasdaq 100 Index rose 279.799 points, or 1.18%, to close at 24019.988.

The Russell 2000 Index rose 0.64% to close at 2512.368.

The VIX volatility index, also known as the 'fear gauge,' fell 2.85% to close at 24.53.

U.S. sector ETFs:

The global airline industry ETF rose 2.60%, the semiconductor ETF climbed 2.24%, the global technology stock index ETF and the technology sector ETF each gained at least 1.51%, the regional banking ETF rose 1.07%, and the energy sector ETF dropped 3.74%.

Mag 7:

The Mag 7 index rose by 0.35% to close at 176.37 points.

$Alphabet-A (GOOGL.US)$ Tesla rose by 2.56%, Meta gained 1.24%, Amazon increased by 1.10%, NVIDIA climbed 0.77%, Apple edged up 0.73%, while Microsoft slipped by 0.22%.

Semiconductor stocks:

The Philadelphia Semiconductor Index closed up 2.82% at 7802.311 points.

Taiwan Semiconductor ADR rose by 1.04%, and AMD surged 3.33%.

$Micron Technology (MU.US)$ Western Digital skyrocketed by 10%, $Intel (INTC.US)$ up 8.84%.

Chinese concept stocks:

The Nasdaq Golden Dragon China Index closed 0.31% higher at 6774.04 points.

Among popular Chinese stocks, Zai Lab closed up 8.13%, EHang gained 4.12%, Kingsoft Cloud rose by 4.04%, GDS Holdings, $Li Auto (LI.US)$ Up by as much as 3.4%, Nio, Huazhu, 21Vianet, and Xpeng rose by up to 2.82%, while Bilibili increased by 1.46%.

Other individual stocks:

Circle fell by 4.95%.

$Eli Lilly and Co (LLY.US)$ Increased by 3.78%, as the FDA approved Eli Lilly and Co's GLP-1 weight loss drug.

The Eurozone's blue-chip index closed up over 2.9%, with RHM rising approximately 9.5%, ASML Holding increasing by 6.1%, while energy stocks TotalEnergies and Eni fell more than 4%. The German stock market closed up over 2.7%, and Italy's banking sector rose over 4.5%.

Pan-European Index:

The European STOXX 600 Index closed up 2.50% at 597.69 points, experiencing continuous high volatility after a gap-up opening. Over the past three trading days, it has rebounded cumulatively by 3.89%, remaining above the 200-day moving average for three consecutive days, breaking through the 100-day moving average, and approaching the 50-day moving average.

The Eurozone STOXX 50 Index closed up 2.93% at 5732.71 points, rebounding by 4.12% over the last three days.

National indices:

The German DAX 30 Index closed up 2.73% at 23298.89 points, rebounding cumulatively by 4.48% over the past three trading days, with the 50-day moving average falling below the 100-day moving average.

The French CAC 40 Index closed up 2.10% at 7981.27 points.

The UK FTSE 100 Index closed up 1.85% at 10364.79 points.

Sector and Stock Performance:

Among blue-chip stocks in the Eurozone, Rheinmetall AG (RHM) closed up 9.48%, Siemens Energy rose 6.99%, ASML Holding climbed 6.11%, Infineon Technologies gained 5.66%, and UniCredit Bank increased by 5.64%.

Among all components of the European STOXX 600 Index, Pan African Resources (PAF.LN) closed up 10.19%, Babcock International Group surged 9.50%, with Rheinmetall AG (RHM) ranking third among defense stocks, Renk Group rising 8.18%, and ThyssenKrupp climbing 8.10%, marking the seventh-largest increase.

The yield on two-year UK government bonds fell more than 11 basis points, opening with a gap lower before trading in a narrow range throughout the day. German bond prices opened higher but declined later.

U.S. Treasury Bonds:

In late New York trading, the yield on the benchmark 10-year US Treasury bond ended flat at 4.317%, forming a V-shaped recovery.

The yield on two-year US Treasury bonds rose slightly by 0.19 basis points to 3.795%.

European debt:

In late European trading, the yield on 10-year German government bonds fell 1.8 basis points to 2.986%, trading within a range of 2.931%-3.004% during the session. After opening with a gap lower, it steadily recovered losses.

In late European trading, the yield on 10-year UK government bonds dropped 8.1 basis points to 4.835%. The yield on two-year UK government bonds fell 11.3 basis points to 4.295%.

The yields on 10-year government bonds in Italy and Greece fell more than 6 basis points.

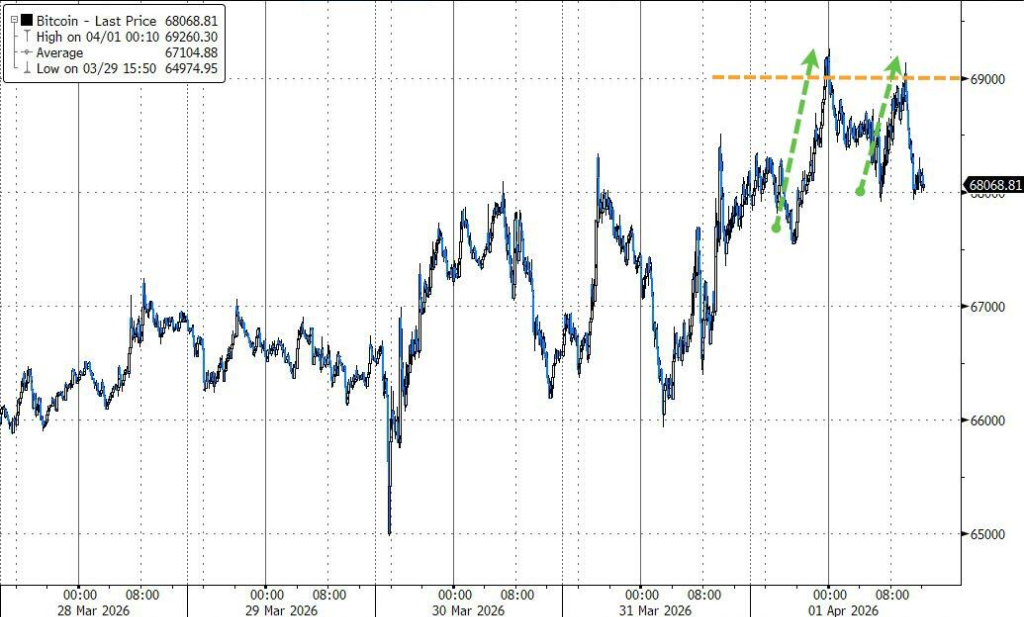

The US Dollar Index declined for the second consecutive day. Bitcoin briefly surged above $69,000 during the session but subsequently retraced its gains in tandem with the weakening momentum of the stock market rally.

US Dollar:

At the New York close, the ICE US Dollar Index fell by 0.33% to 99.634 points, with intraday trading ranging between 99.883 and 99.298 points.

The Bloomberg US Dollar Index dropped by 0.27% to 1212.17 points, with intraday trading fluctuating between 1215.61 and 1209.41 points.

Non-US Dollar Currencies:

At the New York close, the euro appreciated by 0.30% against the US dollar, while the British pound rose by 0.60% against the US dollar, and the US dollar declined by 0.63% against the Swiss franc.

Among commodity currencies, the Australian dollar gained 0.42% against the US dollar, while the New Zealand dollar remained flat against the US dollar.

Yen:

At the New York close, the US dollar increased by 0.11% against the Japanese yen, closing at 158.89 yen, with intraday trading ranging from 158.28 to 159.01 yen.

The euro appreciated by 0.38% against the Japanese yen, while the British pound gained 0.65% against the Japanese yen.

Offshore Renminbi:

At the New York close, the US dollar was quoted at 6.8774 yuan against offshore renminbi, up by 118 points compared to Tuesday's New York close, with overall intraday trading occurring in the range of 6.8909 to 6.8710 yuan.

Cryptocurrency:

At the New York close, Bitcoin briefly surpassed $69,000 during the session but retreated to unchanged levels as equities weakened, closing at $68,000.

Ethereum spot prices rose by 1.7%, closing at $2,140.

Abu Dhabi Murban crude oil futures in the Middle East fell by 3.64%, settling at $102.92 per barrel.

Crude Oil:

WTI crude oil futures for May closed down $1.26, with a decline of over 1.24%, at $100.12 per barrel.

Brent crude oil futures for June fell $2.81, with a drop of over 2.70%, to $101.16 per barrel.

Abu Dhabi Murban crude oil futures in the Middle East fell by 3.64%, settling at $102.92 per barrel.

Natural Gas:

NYMEX natural gas futures for May closed at $2.8190 per million British thermal units.

Gold accelerated its rebound, nearing $4800. Spot silver and New York copper experienced slight declines amid volatile trading.

Gold:

In late New York trading, spot gold rose 1.91% to $4757.17 per ounce, continuing an upward trend, with trading ranging between $4662.36 and $4793.11.

COMEX gold futures gained 2.27%, closing at $4784.90 per ounce, moving higher from $4690 to $4821.

Silver:

In late New York trading, spot silver edged down 0.09% to $75.0995 per ounce.

COMEX silver futures increased by 0.54%, closing at $75.320 per ounce.

Other metals:

In late New York trading, COMEX copper futures fell 0.49% to $5.6230 per pound.

Spot platinum rose by 0.58%, while spot palladium remained unchanged.

LME copper futures closed up by $99 at $12,434 per ton. LME tin futures closed up by $615 at $47,362 per ton. LME nickel futures closed up by $99 at $17,209 per ton. LME aluminum futures closed up by $64 at $3,532 per ton.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Stephen