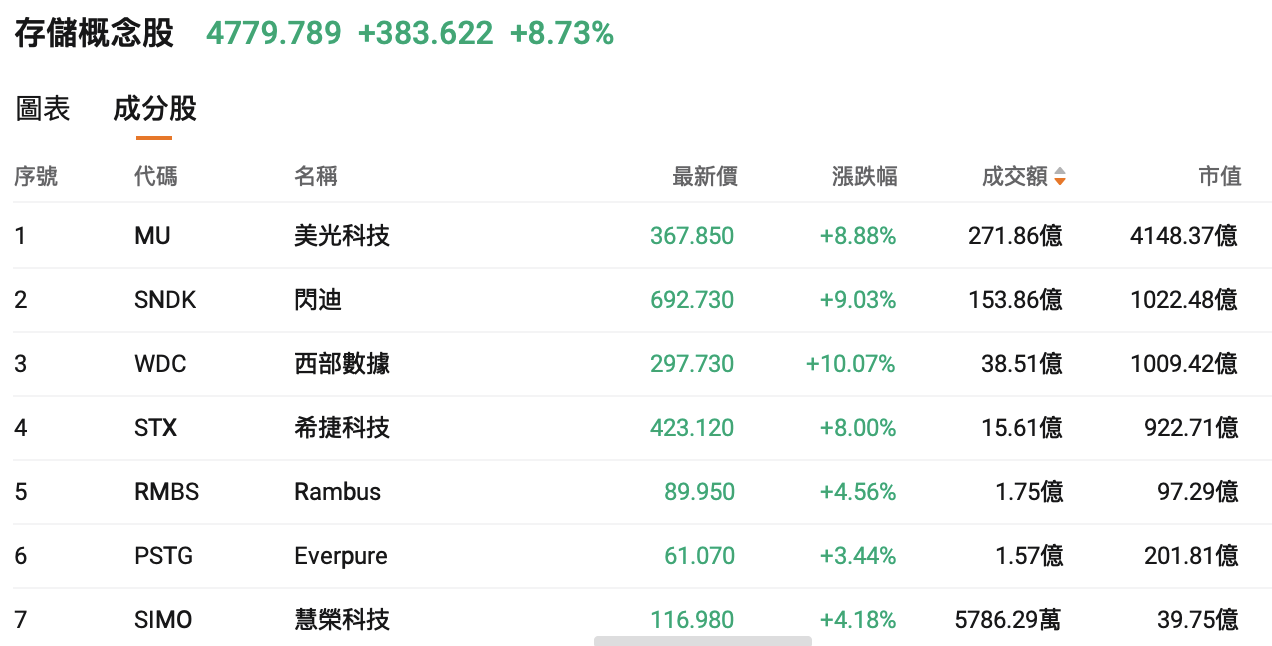

The storage sector surged by 8% in a single day. Micron Technology, SanDisk, Western Digital, and Seagate Technology all experienced gains exceeding 8%. Analysts believe the logic of AI-driven storage demand remains intact, allowing related stocks to benefit first when market sentiment recovers.

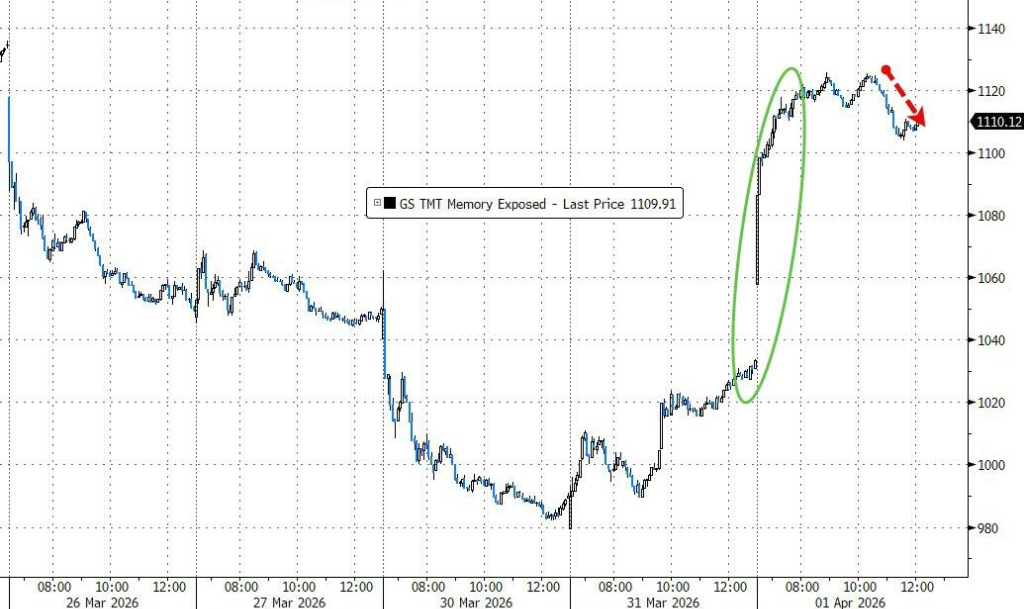

Technology momentum stocks made a strong comeback, with the memory and data storage sectors leading the market on Wednesday.

On Wednesday, April 1st, U.S. stocks rose for the second consecutive trading day, with technology stocks driving the Nasdaq index up by more than 1%. Among them, $Data storage stock (LIST23925.US)$ the stock sector surged 8% in a single day, marking the second-largest daily gain in the history of the index.

In terms of individual stocks, $Micron Technology (MU.US)$ The share price soared nearly 9%, while $SanDisk (SNDK.US)$ rose over 9%. The data storage duo, $Western Digital (WDC.US)$ and $Seagate Technology (STX.US)$ climbed 10% and 8%, respectively.

In terms of individual stocks, $Micron Technology (MU.US)$ The share price soared nearly 9%, while $SanDisk (SNDK.US)$ rose over 9%. The data storage duo, $Western Digital (WDC.US)$ and $Seagate Technology (STX.US)$ climbed 10% and 8%, respectively.

This rally reflects a significant shift in investor sentiment. At the start of the second quarter, market funds flowed back into technology momentum stocks from previously risk-averse sectors such as energy.

The strong return of momentum stocks reversed the downturn seen in March.

In March, investors heavily sold off technology stocks amid heightened tensions over the war in Iran, shifting to defensive sectors like energy, with memory and storage stocks hit hardest.

Analysts believe that the inflow of funds this week indicates that market risk appetite has significantly recovered as the second quarter begins.

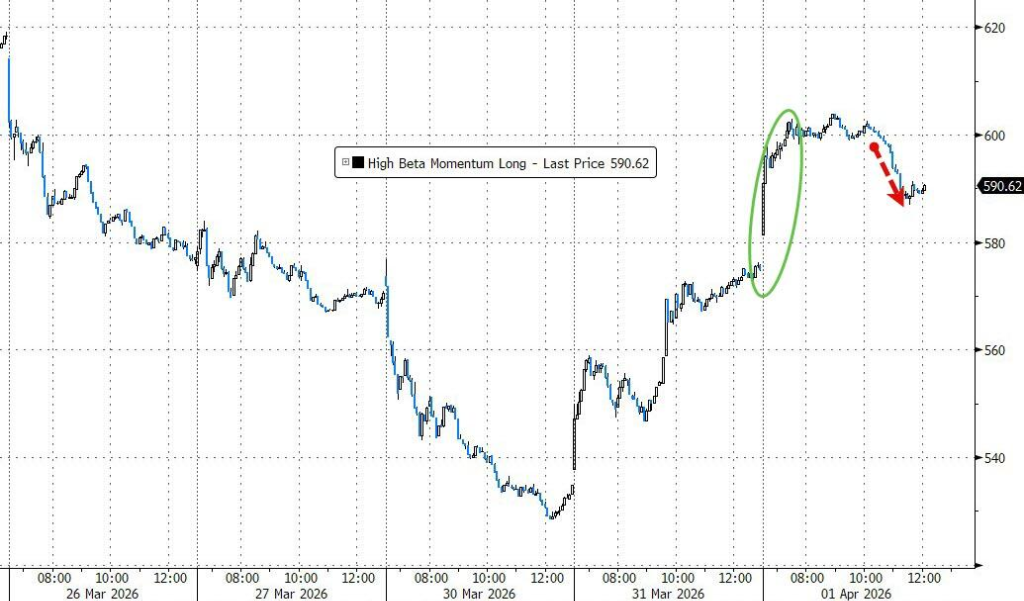

On Wednesday, the Invesco S&P 500 Pure Growth ETF rose 3.2%. Among its current holdings, SanDisk and Micron Technology are both among the top ten largest positions. Additionally, the Goldman Sachs Momentum Index also surged for two consecutive days.

(Goldman Sachs Momentum Index surged for two consecutive days)

Micron Technology, SanDisk, Western Digital, and Seagate Technology are typical representatives of momentum-style investing.

Last year, all four stocks ranked among the top gainers in the S&P 500, with triple-digit increases driven primarily by a surge in demand for memory chips and data storage fueled by the artificial intelligence wave.

This fundamental backdrop provided basic support for the current rebound. With expectations of continued expansion in AI-related capital expenditures, the long-term demand logic for memory and storage remains intact, allowing these stocks to benefit first when market sentiment improves.

Server demand is the true engine supporting the fundamentals of storage.

Previously, concerns over a sharp reduction in memory usage triggered by Google's latest TurboQuant compression algorithm, combined with concentrated selling from earlier stockpiling funds, caused DDR5 memory module prices in the U.S. and Chinese retail channels to plummet by nearly 30%.

As previously noted by Wall Street Wisdom, despite panic over a 'price collapse' in the retail sector, Wall Street and industry research institutions generally emphasize that the spot market is mainly composed of PCs and consumer electronics, which account for at most a low single-digit percentage of total market transactions.

Away from the noise of the spot market, signals from server-side demand are clear and strong.

The latest reports from Goldman Sachs and Daishin Securities of South Korea both indicate that the enterprise-level contract market has not been affected by this wave. Major cloud service providers still have an urgent need for server memory, and the supply-demand fundamentals have not undergone any substantive reversal.

According to Goldman Sachs' report, revenue from Taiwan's server ODM manufacturers (including Invetec, Quanta, Wistron, and Wistron Corporation) collectively increased by 84% year-over-year and 7% month-over-month in February, maintaining a year-over-year growth rate of over 80% for four consecutive months, mainly benefiting from the rapid ramp-up of rack-level AI server shipments and robust growth in ASIC AI servers.

February revenue for Aspeed, the world’s largest supplier of server BMC chips, grew 66% year-over-year, remaining stable even against the backdrop of a high base in February 2025. Meanwhile, Supreme Electronics, a storage distributor, saw its February revenue grow by 137% year-over-year, clearly reflecting strong channel-level demand.

A channel survey conducted by Daishin Securities also provided a more compelling detail: a major cloud service provider has decided to purchase server DDR4 at a price higher than HBM3e. Ryu Hyung-geun wrote:

If genuine demand has already started to weaken, it would be difficult to explain why buyers are willing to pay a premium for traditional products.

Editor/Doris